- Bulk Chemicals

- Caprolactam Market

Caprolactam Market Size, Share, and Growth Forecast 2026 - 2033

Caprolactam Market by Raw Material (Phenol, Cyclohexane, Toluene, Others), Application (Nylon 6 Fibers: Textiles, Carpets, Industrial Yarns; Nylon 6 Resins: Automotive Parts, Electrical & Electronics, Engineering Plastics, Films & Coatings, Consumer Goods, Others), and Regional Analysis, 2026 - 2033

Caprolactam Market Size and Trend Analysis

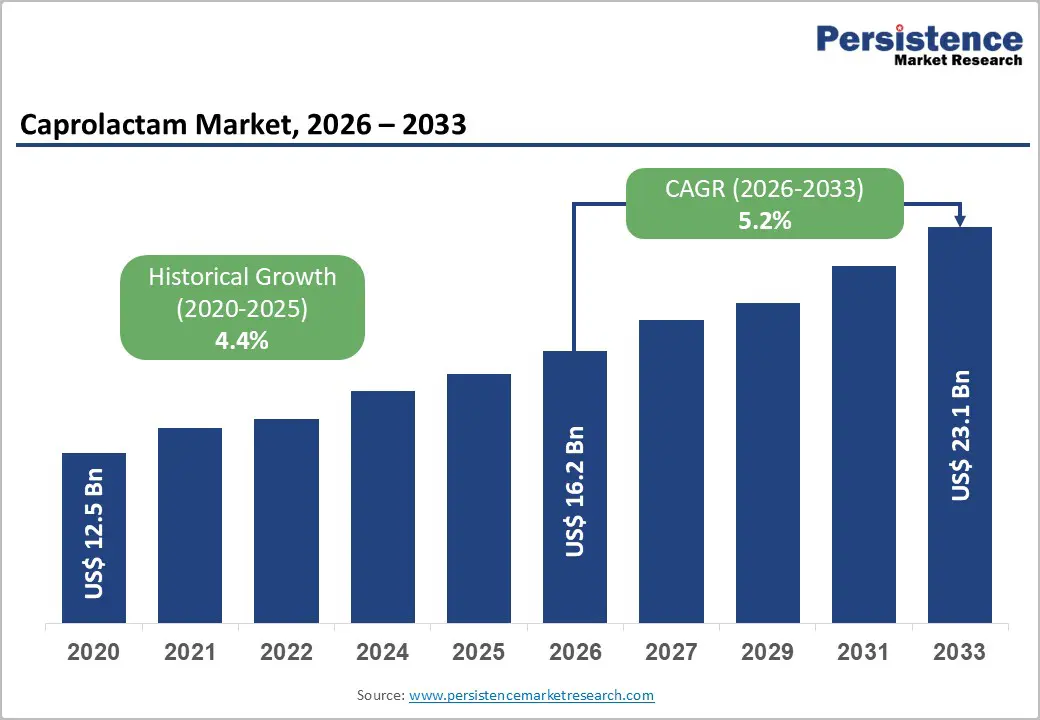

The global caprolactam market size is expected to be valued at US$ 16.2 billion in 2026 and is projected to reach US$ 23.1 billion by 2033, growing at a CAGR of 5.2% between 2026 and 2033. This consistent growth is primarily driven by robust global demand for Nylon 6, the primary downstream derivative of caprolactam, across automotive lightweighting applications, expanding textile and carpet markets in the Asia Pacific, and the growing adoption of Nylon 6 engineering plastics in high-performance electrical and electronics components.

The market grew from US$ 12.5 billion in 2020 at a historical CAGR of 4.4%, supported by rising polyamide demand from the automotive sector's transition to lightweight materials, China's dominant position as both the world's largest caprolactam producer and consumer, and expanding industrial yarn demand from the construction and geotextile sectors in the Asia Pacific and Latin America.

Key Industry Highlights

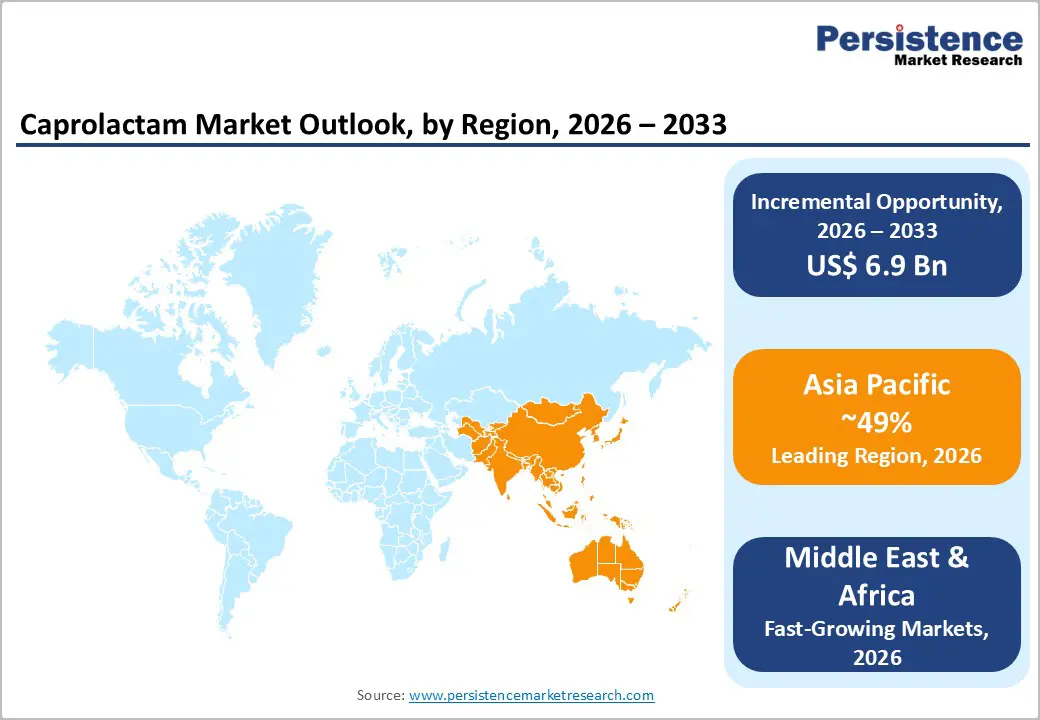

- Leading Region: Asia Pacific commands ~49% global caprolactam market share in 2026, anchored by China's 65% intra-regional dominance as the world's largest Nylon 6 fiber producer, India's PLI textile scheme driving consumption growth, and Japan's advanced Toray-led engineering resin production.

- Fastest Growing Region: MEA is the fastest growing caprolactam region through 2026–2033, driven by SABIC's engineering plastics expansion, Vision 2030 petrochemical integration, Morocco and South Africa automotive cluster growth, and Africa's emerging export-oriented apparel and textile manufacturing sectors.

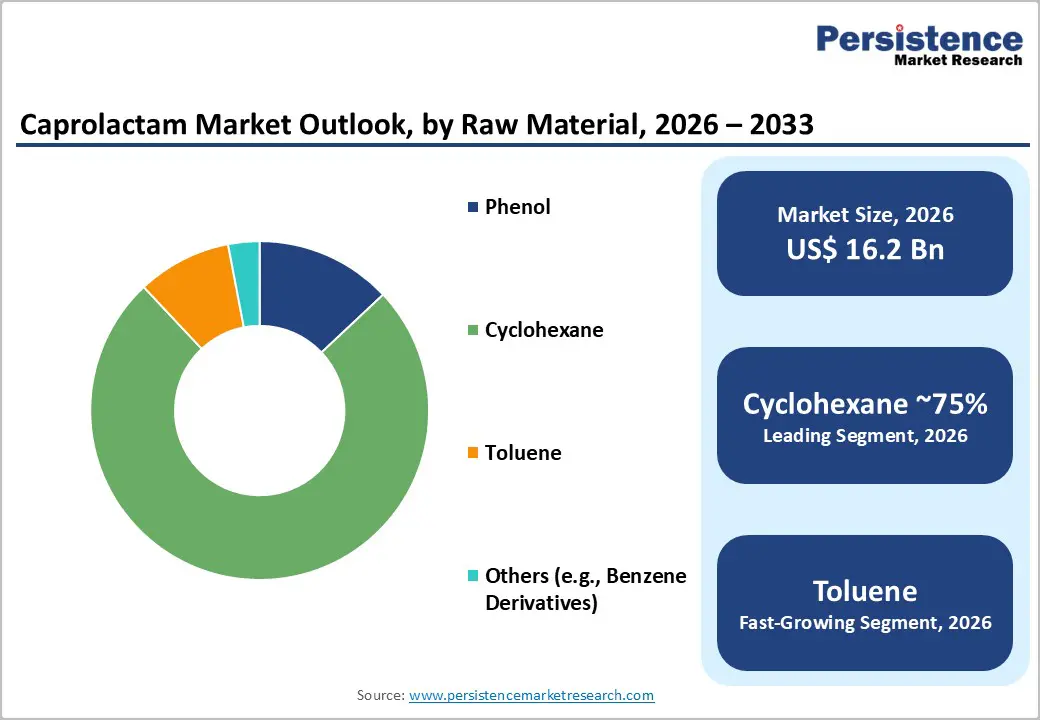

- Leading Raw Material Type: Cyclohexane holds ~75% raw material shares in 2026, dominating through established global production infrastructure from benzene hydrogenation, the highest Beckmann rearrangement yield efficiency, and BASF, DSM, and Sinopec's fully integrated cyclohexane-to-caprolactam-to-Nylon 6 manufacturing platforms.

- Fastest Growing Raw Material Type: Nylon 6 resins are the fastest growing application at ~6% CAGR (2026–2033), driven by OICA-documented 90 million vehicles annually with 15–20 kg polyamide content, EV powertrain component specifications, and electronics miniaturization requiring precision-moldable high-thermal-stability Nylon 6 compound grades.

- Key Opportunity: Toray Industries' bio-caprolactam development program and BASF's expansion of its EV-grade Nylon 6 compound target the converging sustainable materials and electric mobility megatrends, enabling premium pricing, regulatory compliance, and first-mover positioning in the growing circular-economy caprolactam segment through 2033.

DRO Analysis

Drivers - Automotive Lightweighting Megatrend Driving Nylon 6 Engineering Plastics Demand

The automotive industry's accelerating transition toward lightweight materials, driven by fuel-economy regulations and electric-vehicle range optimization, is creating strong structural demand for Nylon 6 engineering plastics derived from caprolactam. Under-the-hood automotive components include manifolds, radiator tanks, cable ties, brake fluid reservoirs, and air-cooling system parts, which increasingly specify glass-fiber-reinforced Nylon 6 compounds for their combination of thermal resistance, chemical durability, and weight savings versus metal alternatives.

The International Organization of Motor Vehicle Manufacturers (OICA) reports global vehicle production at approximately 90 million units annually, with each vehicle incorporating 15–20 kg of polyamide components, according to industry estimates. EV adoption, where battery thermal management, motor housing, and structural components increasingly specify high-performance polyamides, creates incremental caprolactam demand per vehicle above conventional ICE vehicle levels, adding structural growth momentum through the forecast period.

Expanding Asia Pacific Textile and Carpet Industry Sustaining Nylon 6 Fiber Demand

Nylon 6 staple fiber and filament yarn, the primary textile application for caprolactam, are experiencing growing demand from Asia Pacific's expanding apparel, home textiles, and carpet manufacturing industries. The International Textile Manufacturers Federation (ITMF) documents consistent growth in global synthetic fiber production, with polyamide (Nylon 6 and Nylon 66) fibers expanding in activewear, outdoor apparel, and performance textile applications due to superior strength-to-weight ratio, moisture management, and durability.

China's dominant position in textile exports, accounting for approximately 36% of global apparel exports according to WTO data, drives enormous domestic demand for caprolactam fiber. India's rapidly expanding textile manufacturing sector under the Production Linked Incentive (PLI) Scheme for Textiles is adding significant incremental domestic Nylon 6 fiber capacity, stimulating caprolactam consumption growth across the Indian production base.

Restraints - Competition from Nylon 66 and Bio-Based Polyamide Substitutes

Caprolactam-derived Nylon 6 faces sustained competition from Nylon 66, produced from adipic acid and hexamethylenediamine, in premium engineering plastic applications, including automotive structural components and high-performance electrical connectors, where Nylon 66's superior heat resistance and mechanical stiffness justify its premium pricing. Additionally, the emerging segment of bio-based polyamides (PA 11, PA 12) derived from castor oil is capturing niche premium markets, particularly in oil & gas flexible pipelines and high-performance sporting equipment, that would otherwise be addressable by Nylon 6, constraining caprolactam's addressable application expansion at the margin.

Benzene and Cyclohexane Feedstock Price Volatility and Petrochemical Market Exposure

Caprolactam production economics are directly exposed to cyclohexane and benzene feedstock price cycles, both derivatives of the crude oil and naphtha cracking petrochemical value chain. The IEA documents crude oil price fluctuations of 40–60% during demand/supply cycle extremes, directly impacting cyclohexane and benzene prices, which constitute 60–70% of caprolactam's variable production cost. This feedstock cost volatility makes caprolactam producer margins highly cyclical, creating earnings uncertainty that can discourage capital investment in new production capacity and transmission to downstream pricing volatility.

Opportunities - Nylon 6 Resins Fastest Growing Segment: EV and Electronics Industry Expansion

Nylon 6 resins, encompassing engineering plastic compounds, films, and coatings, represent the fastest-growing caprolactam application, with an approximate 6% CAGR through 2026–2033, driven by the electric vehicle industry's structural transition and the proliferation of advanced electronics requiring high-performance polymer housings and structural components. EV battery modules, motor end shields, and high-voltage connector housings are increasingly specifying glass or mineral-filled Nylon 6 compounds for their combination of dielectric properties, thermal management capability, and dimensional stability.

The Society of Automotive Engineers (SAE) technical standards for EV powertrain materials increasingly cite polyamide specifications that directly benefit caprolactam demand. Consumer electronics miniaturization requires precision-moldable, thermally stable polymer housings for smartphones, wearables, and IoT devices, which adds a high-value demand channel for specialty Nylon 6 resin grades.

Middle East & Africa Regional Expansion: Caprolactam Demand from Emerging Automotive and Textile Sectors

The Middle East & Africa region represents the fastest-growing regional market for caprolactam, driven by Saudi Arabia and the UAE's active petrochemical downstream integration strategies under Vision 2030 and Operation 300bn, which include polyamide and Nylon 6 resin production as target value-added chemical sectors. Africa's rapidly expanding apparel and textile manufacturing base, particularly in Ethiopia, Morocco, and Egypt, is generating growing Nylon 6 fiber consumption as these countries develop export-oriented garment industries.

SABIC's engineering plastics expansion and regional automotive manufacturing growth in Morocco (Renault, Stellantis production facilities) and South Africa's established automotive cluster collectively sustain growing demand for Nylon 6 resin. The region's petrochemical cost advantages from subsidized energy and integrated feedstock access make it an attractive location for future caprolactam capacity investment by major producers targeting growing MEA domestic market demand.

Category-wise Analysis

Raw Material Insights

Cyclohexane is the dominant raw material for caprolactam production, accounting for approximately 75% market share in 2026. The cyclohexane-based route, which proceeds through cyclohexanone oxime and a Beckmann rearrangement to yield caprolactam, is the globally dominant production pathway due to its excellent feedstock availability from benzene hydrogenation, well-established industrial-scale process technology, and the highest per-pass caprolactam yield efficiency among available synthetic routes.

Major global caprolactam producers, including BASF SE, DSM, Sinopec, and Toray Industries, operate large-scale cyclohexane-based caprolactam facilities that benefit from decades of process optimization, catalyst development, and energy efficiency improvements. The cyclohexane route's global infrastructure investment and the large installed base of downstream Nylon 6 polymerization equipment designed around its caprolactam product specifications create substantial switching cost barriers that entrench its dominant position.

Application Insights

Nylon 6 fibers are the leading application segment, accounting for approximately 62% of global caprolactam consumption in 2026. The fiber application dominance reflects the enormous scale of the global textile and carpet industries, which collectively represent the world's largest single consumption channel for Nylon 6. Nylon 6 BCF (Bulked Continuous Filament) carpet yarn is the dominant flooring fiber globally for residential and commercial applications, valued for its superior resilience, soil resistance, and dyeability.

ITMF data confirms that polyamide fibers are a growing segment of synthetic fiber production, particularly for performance apparel, outdoor textiles, and technical nonwoven applications. Asia Pacific's textile manufacturing dominance, anchored by China's 36% global apparel export share, sustains the Nylon 6 fiber application segment's commanding revenue leadership through the forecast period.

Regional Insights

North America Caprolactam Market Trends and Insights

North America is a mature, innovation-focused caprolactam market characterized by high-value Nylon 6 engineering resin applications for automotive and electronics sectors, active EV-related polyamide demand growth, and a technically advanced downstream compounding industry. The region's strong automotive OEM base drives consistent procurement of engineering plastics, while carpet fiber demand, particularly in residential replacement cycles, sustains Nylon 6 BCF yarn consumption in the U.S.

U.S. Caprolactam Market Size

The United States accounts for approximately 78% of the North American caprolactam market revenue in 2026. The U.S. automotive sector, producing approximately 10 million vehicles annually per OICA, drives consistent demand for Nylon 6 engineering plastic from compounders, including BASF and Lanxess, serving Detroit-area OEMs. The U.S. residential carpet market, served by major BCF yarn producers, sustains Nylon 6 fiber consumption. U.S. CAGR is projected at approximately 4.8% through 2033.

Europe Caprolactam Market Trends and Insights

Europe is a technology-intensive caprolactam market with a strong focus on high-value Nylon 6 engineering compounds for automotive and electrical applications. The European Automobile Manufacturers' Association (ACEA) documents consistent EU automotive production, sustaining Nylon 6 resin demand, while the region's advanced compounding industry, featuring BASF SE, DSM, and Lanxess, develops specialty Nylon 6 grades for precision-engineering applications.

Germany Caprolactam Market Size

Germany holds approximately 26% of the European caprolactam market revenue in 2026. Germany's world-leading automotive cluster, with BMW, Volkswagen, and Mercedes-Benz, generates premium Nylon 6 engineering plastic demand for structural and under-hood components. BASF SE's Ludwigshafen operations are Europe's primary caprolactam and Nylon 6 polymerization facility. Germany is projected at approximately 4.6% CAGR through 2033.

U.K. Caprolactam Market Size

The United Kingdom represents approximately 11% of the European caprolactam market revenue in 2026. The UK's active automotive manufacturing sector (Jaguar Land Rover, MINI) and growing EV ecosystem (Nissan Sunderland) sustain Nylon 6 resin demand. UK carpet manufacturing, one of Europe's largest, drives Nylon 6 BCF yarn consumption from domestic fiber producers. UK CAGR is projected at approximately 4.5% through 2033.

France Caprolactam Market Size

France accounts for approximately 10% of the European caprolactam market revenue in 2026. France's automotive manufacturing base, including Stellantis and Renault Group, drives consistent engineering polyamide demand. French specialty chemical groups, including Arkema, are active in the development of high-performance polyamides, with downstream caprolactam resin applications in specialty coatings and films.

Asia Pacific Caprolactam Market Trends and Insights

Asia Pacific dominates global caprolactam production and consumption, with China accounting for approximately 65% of Asia Pacific demand, reflecting the country's position as the world's largest producer of Nylon 6 fiber and resin. China's domestic caprolactam production capacity has grown substantially over the past decade, with producers including Sinopec, China Petroleum & Chemical Corporation, and Luxi Chemical Group operating large-scale facilities. India, Japan, and Southeast Asia are secondary but rapidly growing markets for caprolactam.

India Caprolactam Market Size

India represents approximately 10% of the Asia Pacific caprolactam market revenue in 2026. India's rapidly expanding textile industry under the PLI Scheme for Textiles and growing automotive Nylon 6 resin demand from Maruti Suzuki, Tata Motors, and international OEM plants drive caprolactam consumption. India is projected to grow at approximately 7.5% CAGR through 2033, among the region's fastest-growing markets.

Japan Caprolactam Market Size

Japan contributes approximately 7% of the Asia Pacific caprolactam market revenue in 2026. Japan's advanced Nylon 6 engineering resin industry, anchored by Toray Industries, Toyobo, and Ube Industries, produces high-performance specialty Nylon 6 grades for automotive, electronics, and industrial applications. Japan's precision manufacturing tradition drives high-value Nylon 6 compound specification in domestic OEM supply chains. Japan is projected at approximately 4.4% CAGR through 2033.

Southeast Asia Caprolactam Market Size

Southeast Asia collectively represents approximately 8% of the Asia Pacific caprolactam market revenue in 2026. Vietnam, Thailand, and Indonesia are experiencing rising Nylon 6 fiber consumption driven by expanding textile export industries and Nylon 6 resin demand from growing automotive assembly operations.

Competitive Landscape

The global caprolactam market exhibits a moderately consolidated competitive structure, with a limited number of large integrated chemical producers controlling the majority of global capacity. BASF SE, DSM (now DSM-Firmenich), Sinopec, Toray Industries, and AdvanSix Inc. collectively represent significant global caprolactam output. Key competitive differentiators include feedstock integration depth, downstream Nylon 6 polymer and compounding capabilities, and specialty product grade development for EV and electronics applications.

Emerging strategic trends include bio-based caprolactam R&D programs aimed at reducing dependence on petroleum-derived cyclohexane, and co-development of Nylon 6 recycling pathways for circular economy compliance. China-based producers are competing aggressively on cost through scale and energy-cost advantages.

Key Developments:

- In April 2025, BASF SE announced the expansion of its Nylon 6 compounding capacity in Asia Pacific, targeting the rapidly growing EV powertrain and consumer electronics sectors requiring high-performance glass-fiber-reinforced Nylon 6 grades with enhanced thermal and dielectric properties.

- In November 2024, AdvanSix Inc. completed a strategic review of its caprolactam and ammonium sulfate production integration at its Hopewell, Virginia facility, announcing optimized production scheduling to improve yield per unit of cyclohexane feedstock and reduce co-product ammonium sulfate logistics costs.

- In March 2023, Toray Industries announced a joint development program for bio-based caprolactam using sugar-derived cyclohexanone pathways, targeting commercially viable bio-caprolactam production that would enable certified bio-Nylon 6 for premium sustainable apparel and automotive applications by the late 2020s.

Global Caprolactam Market – Key Insights & Details

| Key Insights | Details |

|---|---|

|

Historical Market Value (2020) |

US$ 12.5 Billion |

|

Current Market Value (2026) |

US$ 16.2 Billion |

|

Projected Market Value (2033) |

US$ 23.1 Billion |

|

CAGR (2026–2033) |

5.2% |

|

Leading Region |

Asia Pacific, ~49% market share (2026) |

|

Dominant Category – Raw Material |

Cyclohexane, ~75% share (2026) |

|

Top-Ranking Category – Application |

Nylon 6 Fibers, ~62% share (2026) |

|

Incremental Opportunity (2026–2033) |

US$ 6.9 Billion |

Companies Covered in Caprolactam Market

- AdvanSix Inc.

- Alpek S.A.B. de C.V.

- The Aquafil Group

- BASF SE

- Capro Co.

- China Petrochemical Development Corporation

- Domo Chemicals

- Grupa Azoty

- Gujarat State Fertilizers & Chemicals Limited

- Highsun Group

- KuibyshevAzot PJSC

- Lanxess AG

- Luxi Chemical Group Co., Ltd.

- China Petroleum & Chemical Corporation (Sinopec)

- Spolana

Frequently Asked Questions

The global caprolactam market is projected to be valued at US$ 16.2 billion in 2026, growing from US$ 12.5 billion in 2020. The market is forecast to reach US$ 23.1 billion by 2033 at a CAGR of 5.2%, representing an absolute dollar opportunity of US$ 6.9 billion.

Primary drivers include automotive lightweighting with OICA-documented 90 million vehicles produced annually and 15–20 kg of polyamide per vehicle driving Nylon 6 resin demand, and Asia Pacific textile sector growth.

Asia Pacific leads with approximately 49% market share in 2026, with China accounting for ~65% of intra-regional demand as the world's largest Nylon 6 fiber and resin producer.

Nylon 6 resins at ~6% CAGR represent the highest-growth application, particularly for EV powertrain and advanced electronics, with SAE polyamide specifications gaining adoption in battery management housings and motor end shields.

Key companies include BASF SE, DSM (dsm-firmenich), Sinopec, Toray Industries, AdvanSix Inc., Lanxess AG, Ube Industries, Asahi Kasei Corporation, Toyobo Co. Ltd., Sumitomo Chemical, Luxi Chemical Group, and DOMO Chemicals GmbH.