- Hardware & Software IT Services

- Debt Settlement Solution Market

Debt Settlement Solution Market Size, Share, and Growth Forecast, 2026 - 2033

Debt Settlement Solution Market by Debt Type (Credit Card, Personal Loan, Medical), End-User (Individuals, Small & Medium Enterprises (SMEs), Large Enterprises), Component (Software, Services), and Regional Analysis for 2026 - 2033

Debt Settlement Solution Market Share and Trends Analysis

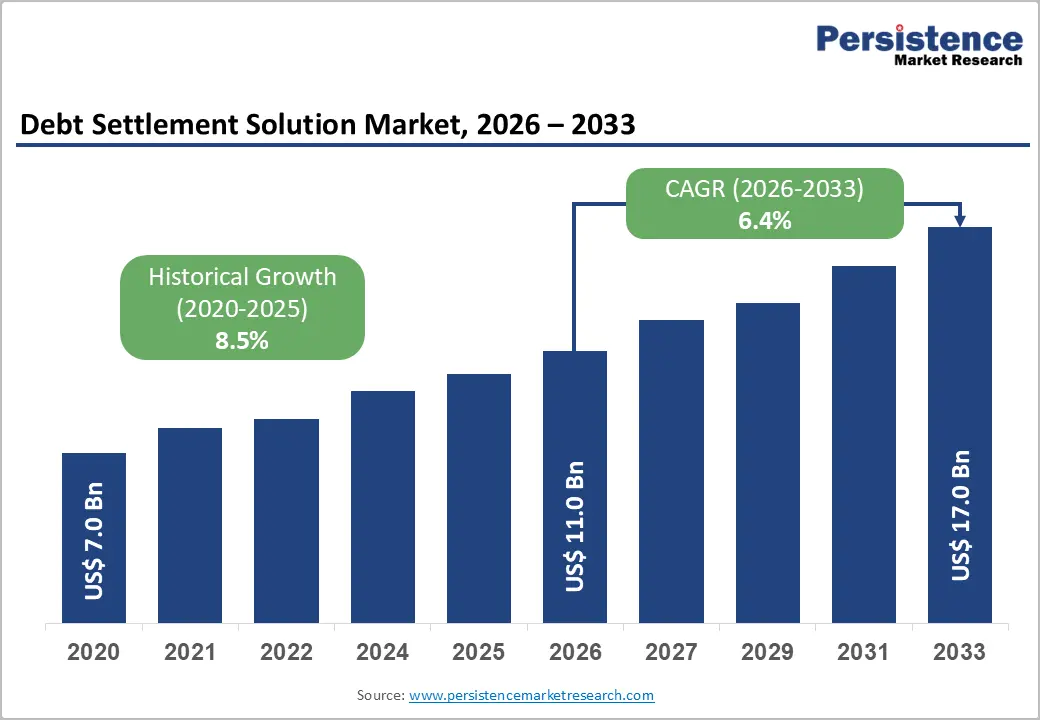

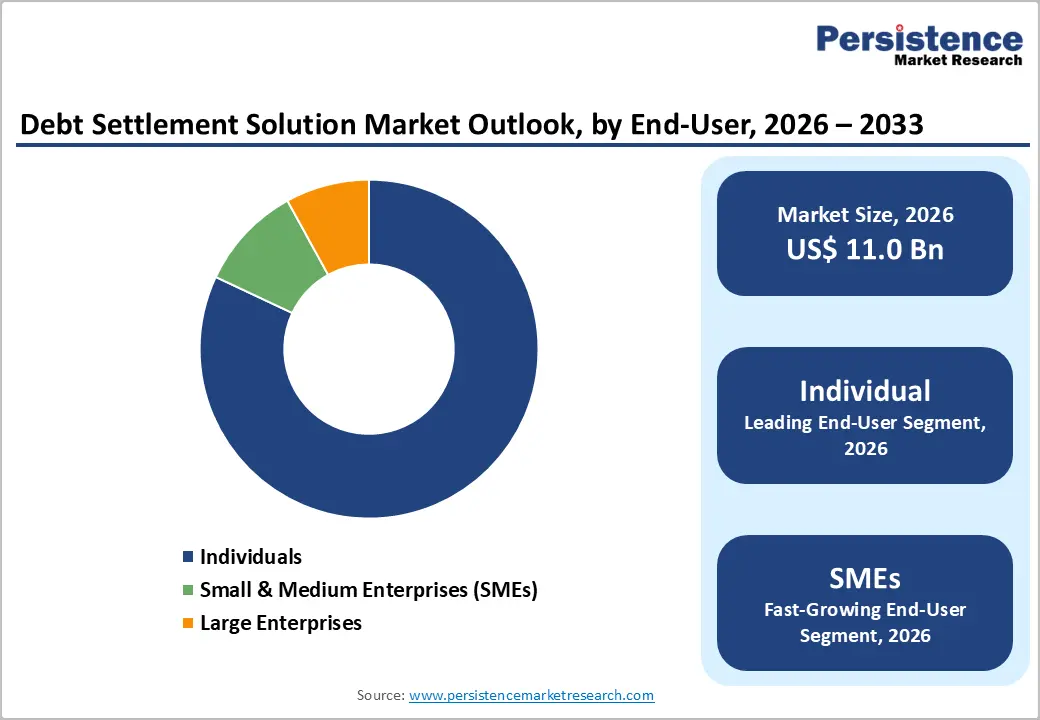

The global debt settlement solution market size is likely to be valued at US$ 11.0 billion in 2026, and is projected to reach US$ 17.0 billion by 2033, growing at a CAGR of 6.4% during the forecast period 2026 - 2033.

Persistently high consumer debt levels across developed economies, particularly in unsecured credit categories such as credit cards and personal loans, is aiding market expansion. As repayment stress is increasing, individuals and small businesses are actively seeking structured alternatives to bankruptcy and prolonged delinquency. Market development is also being accelerated by the rapid adoption of digital debt management and settlement platforms that simplify negotiation, tracking, and compliance processes. Regulatory frameworks in several jurisdictions are increasingly recognizing and formalizing alternative debt resolution mechanisms, which is improving consumer confidence and institutional participation. Rising financial literacy is enabling borrowers to engage more proactively with settlement options, while fintech-enabled providers are improving scalability and cost efficiency. Solution providers that combine regulatory alignment, transparent pricing models, and data-driven negotiation tools are positioning themselves to capture sustained demand as economic uncertainty continues to shape borrower behavior.

Key Industry Highlights

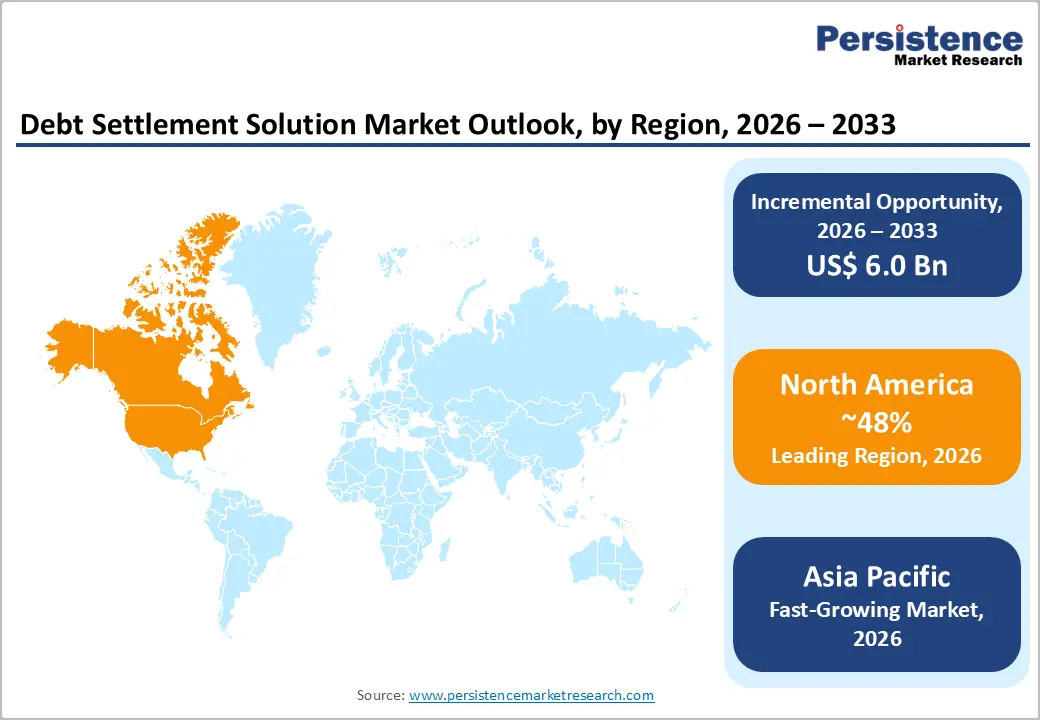

- Dominant Region: North America is slated to dominate with approximately 48% market share in 2026, supported by a combination of high consumer indebtedness, a sophisticated financial services ecosystem, and a mature regulatory environment.

- Fastest-growing Regional Market: Asia Pacific is anticipated to emerge as the fastest-growing market through 2033, on account of soaring consumer indebtedness and rapid uptake of digital financial services.

- Leading & Fastest-growing Debt Type: Credit card debt is likely to lead with about 55% revenue share in 2026, while personal loan is projected to be the fastest-growing segment during the 2026 - 2033 forecast period.

- Major Driver: Consumer debt pressures have become a structural concern across major economies, prompting financial institutions and policymakers to reassess how households manage obligations such as credit cards, personal loans, and mortgages.

- Attractive Opportunity: Commercial debt settlement is emerging as a strategic extension of traditional consumer-focused models, yet it remains less developed and less systematically addressed than the retail segment.

- April 2025: Kikoff introduced an AI-powered debt negotiator designed to help consumers in the United States manage and reduce their debt more effectively by automating negotiation processes and providing personalized repayment guidance.

| Key Insights | Details |

|---|---|

| Debt Settlement Solution Market Size (2026E) | US$ 11.0 Bn |

| Market Value Forecast (2033F) | US$ 17.0 Bn |

| Projected Growth (CAGR 2026 to 2033) | 6.4% |

| Historical Market Growth (CAGR 2020 to 2025) | 8.5% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Rising Global Consumer Debt Burden

Consumer debt pressures have become a structural concern across major economies, prompting financial institutions and policymakers to reassess how households manage obligations such as credit cards, personal loans, and mortgages. The Federal Reserve Bank of New York’s quarterly report on household debt and credit shows that total U.S. household debt reached about US$ 18.59 trillion in Q3 2025. Rising borrowing costs and tighter lending conditions are eroding repayment capacity for many segments, particularly vulnerable and lower-income households. In this context, organizations that offer debt settlement solutions play an increasingly strategic role by translating complex financial distress into structured, time-bound resolution plans that both borrowers and creditors can accept. This role now sits at the intersection of consumer finance, risk management, and financial well-being advisory services.

The debt settlement industry operates as a specialized intermediary that helps borrowers assess their overall liability position, prioritize obligations, and negotiate revised terms with lenders, such as reduced balances, adjusted repayment schedules, or fee concessions. Effective providers do more than negotiate discounts; they also support clients with credit rebuilding, budgeting discipline, and long-term cash flow planning so that settlements serve as a turning point rather than a temporary relief. For creditors, professional settlement firms can enhance recovery outcomes and lower legal and collection costs by converting high-risk accounts into structured, predictable repayment arrangements.

Regulatory Compliance Complexity and Operational Restrictions

Debt settlement providers now operate in a regulatory environment that is significantly more complex and demanding, particularly for firms that serve clients across multiple regions. Regulatory bodies such as the Federal Trade Commission (FTC) have introduced rules that restrict how and when providers can collect fees, pushing many companies toward contingency-based revenue models and increasing pressure on working capital management. At the same time, state-level authorities impose distinct licensing frameworks, disclosure requirements, and conduct standards, which forces organizations to maintain detailed compliance maps and robust governance structures.

In practice, leadership teams must treat compliance as a core strategic function rather than a back-office activity and must integrate it into product design, pricing, and client onboarding. Variation in state-level regulations, such as different fee caps, documentation standards, and audit expectations, increases operational complexity for firms that aim to scale nationally. Smaller and mid-sized providers experience this most acutely because they must invest in legal counsel, compliance monitoring systems, and ongoing staff training without having sufficient scale to absorb these expenses. As a result, barriers to entry rise, and only firms with disciplined risk management and strong internal controls can expand into multiple jurisdictions sustainably.

B2B Debt Settlement Services and Commercial Debt Management

Commercial debt settlement is emerging as a strategic extension of traditional consumer-focused models, yet it remains less developed and less systematically addressed than the retail segment. Households increasingly use structured settlement programs, while many businesses still depend on ad hoc negotiations or legal action to resolve unpaid invoices, disputed receivables, and broken payment terms. Small and medium enterprises often lack in-house expertise in areas such as credit risk, multi-party negotiation, and cross-border enforcement, which leaves them vulnerable when buyers delay or withhold payments. This structural gap creates a clear opportunity for specialized providers to design tailored solutions for business-to-business obligations such as trade credit, project-based contracts, and recurring supply agreements.

The commercial segment requires a more advisory-driven, industry-aware approach that integrates legal insight, negotiation capability, and operational process redesign. Firms that build sector-specific knowledge in areas such as manufacturing, construction, logistics, and professional services can position settlements not only as collections but also as relationship-preserving resolutions that stabilize supply chains and protect future revenue. Integrating settlement workflows with enterprise resource planning (ERP) platforms and accounting systems can provide both creditors and service providers with clearer visibility into aging receivables, dispute patterns, and counterparty risk.

Category-wise Analysis

Debt Type Insights

Credit card debt is poised to represent the dominant segment in 2026, accounting for an estimated 55% of the debt settlement solution market revenue share in 2026. Credit card debt has become a critical focus area in the debt settlement landscape due to its widespread use and relatively high interest rates. Many consumers struggle with persistent revolving balances, which makes specialized credit card debt settlement services particularly relevant. As households increasingly rely on credit cards to cover routine expenses and unexpected financial shocks, the importance of targeted debt management and structured relief programs in this segment continues to grow.

The personal loan segment is projected to be the fastest-growing during the 2026 - 2033 forecast period. Personal loans form another important category within the debt settlement landscape, as borrowers frequently use them for diverse personal needs and can accumulate multiple obligations over time. When repayment pressures build, these loans can become difficult to manage alongside other financial commitments, increasing the risk of delinquency. In such situations, debt settlement services support individuals by restructuring and negotiating their personal loan obligations, helping to create a clearer and more manageable repayment path.

End-User Insights

Individual consumers constitute the leading end-user segment, accounting for approximately 82% of total market revenue. Rising household debt burdens, stagnant wage growth in key demographics, and unexpected financial disruptions have created sustained demand for consumer debt settlement services. The segment encompasses diverse consumer profiles, including medical debt holders, credit card over extenders, and borrowers affected by life events such as divorce, job loss, or health crises. Service providers targeting this segment emphasize accessibility, transparent fee structures, and educational resources that empower consumers throughout the settlement process.

Small & medium enterprises (SMEs) represent the fastest-growing end-user segment. Several SMEs face persistent financial pressure due to cash flow gaps, shifting economic conditions, and unforeseen costs. When these pressures intensify, debt settlement services designed specifically for SMEs can help them restructure obligations, stabilize finances, and redirect management attention toward core operations and growth. As the global SME base expands and business environment uncertainty remains elevated, demand is strengthening for specialized debt settlement solutions that reflect the unique needs, risk profiles, and capital constraints of smaller businesses.

Component Insights

Software platforms are expected to lead, capturing an estimated 62% of market revenue share in 2026. Cloud-based debt management systems, creditor negotiation platforms, and client communication portals now form core infrastructure for modern settlement providers, rather than optional add-ons. Software-as-a-Service (SaaS) deployment models support scalable operations, real-time performance monitoring, and data analytics that help teams refine strategies and improve settlement effectiveness. Leading platforms also integrate payment processing, document management, compliance monitoring, and customer relationship management into a single environment, reducing manual work, lowering error rates, and enhancing overall operational efficiency.

Service is expected to be the fastest-growing segment during the 2026 - 2033 forecast period. Service-based offerings represent the more traditional side of the debt settlement market, delivered by financial specialists, advisory firms, and legal professionals. This segment typically covers creditor negotiations, financial counselling, and tailored debt management guidance that reflects each client’s specific circumstances and risk profile. Even as digital platforms gain prominence, advisory services remain essential because many individuals and businesses place high value on human judgment, empathy, and nuanced interpretation of complex financial situations.

Regional Insights

North America Debt Settlement Solution Market Trends

North America is poised to dominate in 2026, accounting for approximately 48% of the debt settlement solution market share in 2026. This region’s leadership reflects a combination of high consumer indebtedness, a sophisticated financial services ecosystem, and a mature regulatory environment that supports structured debt settlement activity. Within North America, the United States stands out as the primary market, driven by large credit card balances and substantial student loan obligations that sustain demand for specialized resolution services. Strong adoption of digital financial services and broad use of advanced debt management technologies further accelerate market development, as providers can deliver more scalable and data-driven settlement solutions across the region.

Key growth in the region is driven by leadership in technological innovation, with fintech companies in hubs such as Silicon Valley developing artificial intelligence (AI)-enabled debt management platforms that enhance segmentation, engagement, and recovery strategies. Widespread consumer openness to alternative debt resolution options and the presence of a comprehensive credit reporting infrastructure support more sophisticated risk assessment and targeted settlement approaches. Market leaders such as Freedom Debt Relief and National Debt Relief strengthen their positions by combining substantial marketing spending with robust technology and analytics capabilities, allowing them to reach large customer bases and manage complex portfolios at scale.

Europe Debt Settlement Solution Market Trends

Europe is slated to emerge as the second-largest regional hub for debt settlement solutions, supported by a diversified mix of household and commercial debt, a strong banking sector, and a more structured regulatory environment that recognizes the need for formalized resolution mechanisms. Germany, the United Kingdom, France, and Spain anchor regional activity, each generating distinct patterns of demand shaped by local credit cultures, legal frameworks, and economic structures. In the United Kingdom, the presence of established debt management firms and a long history of consumer credit usage have created a relatively mature market in which structured repayment plans and negotiated settlements are widely understood by both borrowers and creditors.

Growth in the regional market increasingly reflects the combined influence of macroeconomic stress, regulatory harmonization, and the rapid digitization of financial services. Post-pandemic income volatility and higher borrowing costs have put pressure on household finances, while many small and medium-sized enterprises face working capital challenges, making structured settlements more relevant in both consumer and commercial markets. Digital regulation and open banking initiatives, such as frameworks that support secure data sharing and payment initiation, are also helping providers embed automated payment plans, real-time status tracking, and analytics-driven risk monitoring into their settlement workflows.

Asia Pacific Debt Settlement Solution Market Trends

Asia Pacific is anticipated to emerge as the fastest-growing market for debt settlement solutions between 2026 and 2033. Rising consumer indebtedness, greater financial awareness, and the rapid adoption of digital financial services are collectively driving strong market expansion across this region. Households are engaging more actively with formal credit while also seeking structured ways to address repayment stress, creating a natural opening for professional debt settlement offerings. For example, according to recent data from the Reserve Bank of India (RBI), outstanding credit card dues in India currently hover around INR 2.91 lakh crore, or US$ 32.91 billion. Major economies such as China and India play a central role, combining large populations with fast-growing financial ecosystems and vibrant fintech sectors that make digital-first debt solutions more accessible.

As awareness of structured debt management options increases and technology-led platforms become more ubiquitous, demand for debt settlement services in the Asia Pacific is set to deepen across both urban and emerging semi-urban segments. However, regulatory frameworks remain underdeveloped in many markets, creating operational uncertainties. Competitive landscape characteristics include dominance by local providers with regulatory expertise and cultural understanding, creating partnership opportunities for international firms seeking market entry. Investment trends favor technology platform development, regulatory-compliance infrastructure, and strategic acquisitions of regional players with established client bases and operational licenses.

Competitive Landscape

The global debt settlement solution market is maintaining a moderately fragmented structure. Established providers such as Freedom Debt Relief, National Debt Relief, Accredited Debt Relief, United Debt Relief, and Guardian Debt Relief collectively account for an estimated 35-40% of the total market revenue. No single firm is exercising dominant control, as customer acquisition is being distributed across multiple providers with varying service models, fee structures, and regulatory footprints. Market positioning is increasingly influenced by brand trust, compliance credibility, and the ability to deliver measurable debt reduction outcomes.

Competitive intensity is heating up as demand for structured debt resolution services continues to expand, and digital engagement becomes central to service delivery. Providers are actively enhancing online onboarding, case management automation, and customer communication tools to improve efficiency and transparency. The entry of financial technology companies is further reshaping the landscape by introducing data-driven negotiation, user-friendly interfaces, and faster resolution cycles. Firms that combine strong regulatory compliance with scalable digital platforms and personalized client support are positioning themselves to compete effectively as consumer and small-business debt challenges persist.

Key Industry Developments

- In September 2025, Meedaf, an Abu Dhabi-based financial services platform, partnered with Australian AI-powered collections leader InDebted, including an investment in its UAE entity to expand across GCC markets. The collaboration merges Meedaf's regional networks with InDebted's empathetic, tech-driven debt resolution for banks, fintechs, government, and telecoms.

- In June 2025, Relief, an AI-driven consumer debt resolution platform, raised new growth capital from National Debt Relief, the largest US debt settlement company, alongside forming a strategic commercial partnership. Relief will use the funding and partnership to expand in-app negotiated settlements, real-time offers, new product lines, and position itself as the core digital infrastructure for large-scale consumer debt resolution.

- In May 2025, Debt Relief India expanded its settlement services across India, building on its track record of negotiating reduced payoffs with lenders for personal loans, credit cards, and other unsecured debts. The move addresses rising household indebtedness amid economic pressures, offering customized resolution plans to consumers to avoid bankruptcy while aiming for 40-60% savings on outstanding balances.

Companies Covered in Debt Settlement Solution Market

- Freedom Debt Relief

- National Debt Relief

- Accredited Debt Relief

- CuraDebt

- New Era Debt Solutions

- Pacific Debt Relief

- Debt Relief USA

- Rescue One Financial

- Guardian Debt Relief

- Accredited Financial Services

- Century Support Services

- Premier Debt Help

- Clear One Advantage

- United Debt Relief

- DebtBlue

Frequently Asked Questions

The global debt settlement solution market is projected to reach US$ 11.0 billion in 2026.

The market is primarily driven by rising consumer and business indebtedness, stricter credit conditions, and growing acceptance of structured, third-party mediated debt resolution.

The market is poised to witness a CAGR of 6.4% from 2026 to 2033.

Key opportunities lie in digital-first and omnichannel platforms, underserved segments such as SMEs and commercial receivables, where formal debt resolution frameworks and financial inclusion are expanding.

Freedom Debt Relief, National Debt Relief, Accredited Debt Relief, United Debt Relief and Guardian Debt Relief are some of the key players in the market.