- Hardware & Software IT Services

- Debt Collection Software Market

Debt Collection Software Market Size, Share, and Growth Forecast, 2026 - 2033

Debt Collection Software Market by Component Type (Services, Software), Deployment (On-Premise, Cloud), End-user (Healthcare, Financial Institutions, Collection Agencies, Government, Telecom & Utilities, Others), and Regional Analysis for 2026 - 2033

Debt Collection Software Market Size and Trends Analysis

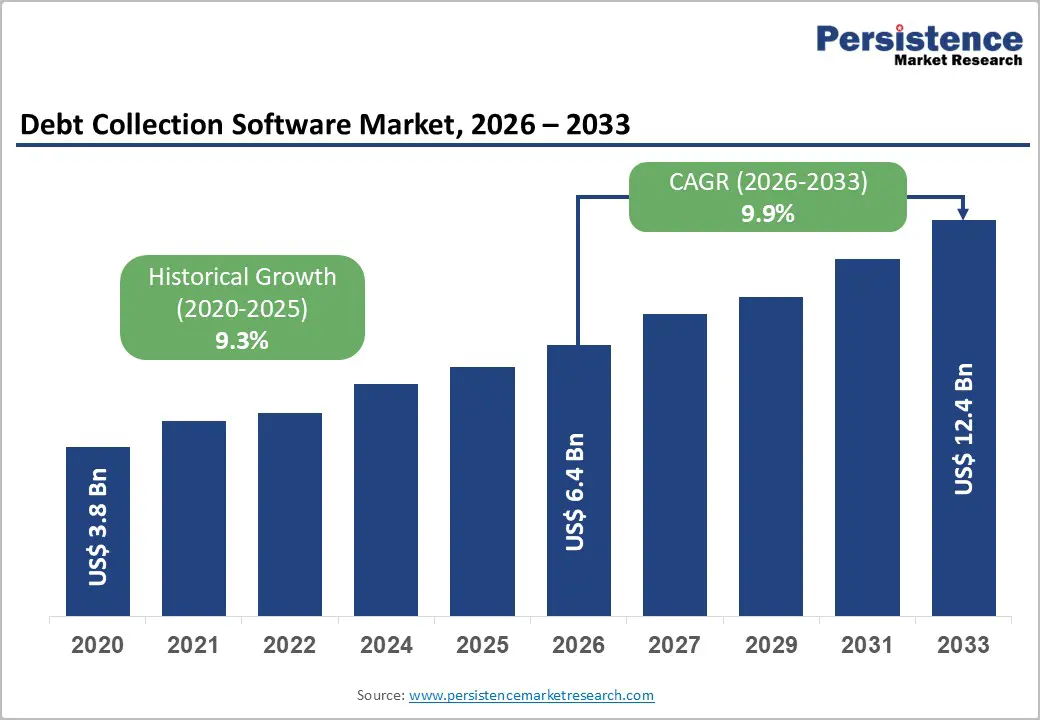

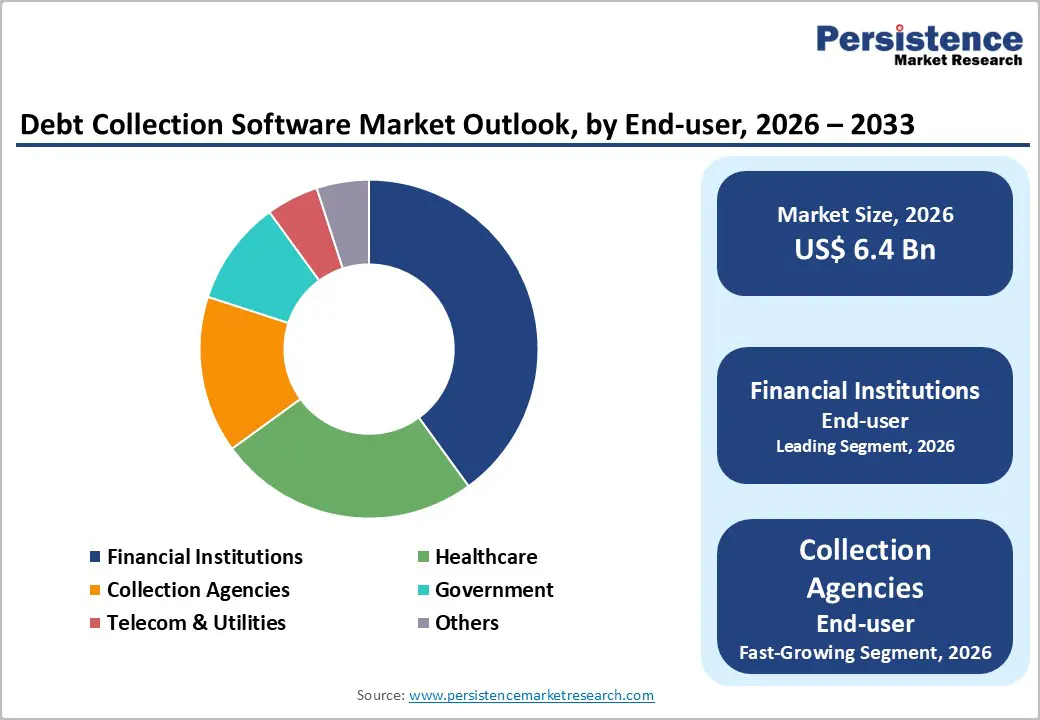

The global debt collection software market size is likely to be valued at US$6.4 billion in 2026, and is expected to reach US$12.4 billion by 2033, growing at a CAGR of 9.9% during the forecast period from 2026 to 2033, driven by the rise in non-performing loans, increasing digitalization of financial services, and the need for automated, compliant debt recovery solutions across industries. Increasing adoption of AI-powered analytics, omnichannel communication, and cloud-based platforms for efficient debt management remains a major growth driver.

Key Industry Highlights:

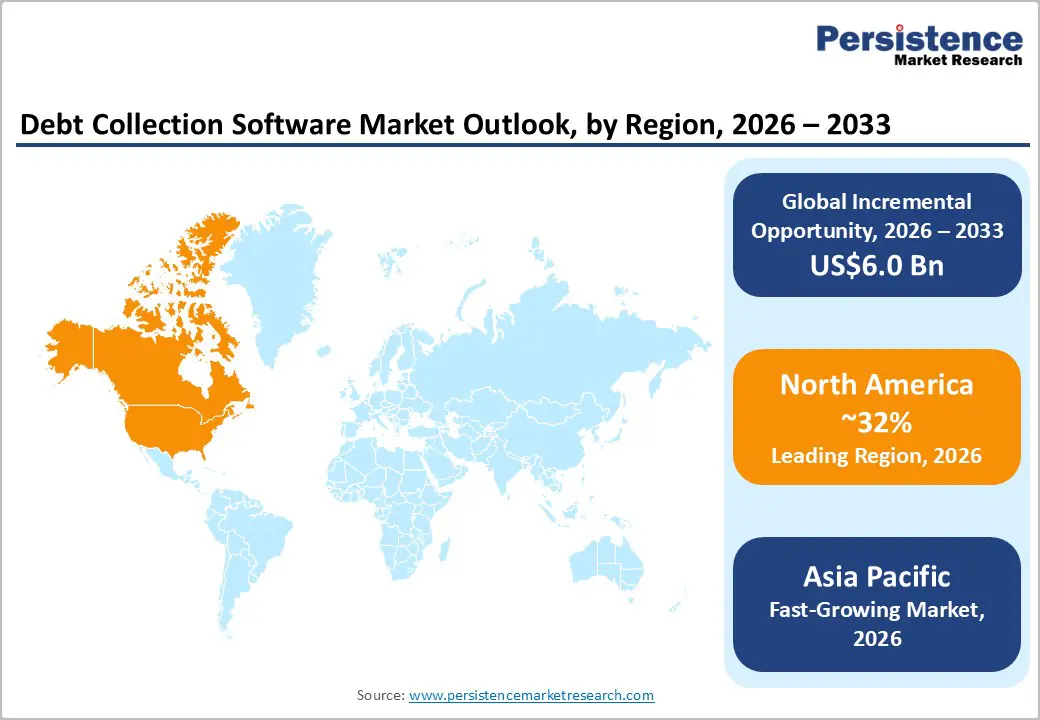

- Leading Region: North America, anticipated to account for a 32% market share in 2026, driven by advanced financial infrastructure and high adoption of automation in the U.S.

- Fastest-growing Region: Asia Pacific, fueled by rising consumer debt, digital banking expansion, and growing fintech investments in China and India.

- Dominant Component: Software, to hold approximately 65% of the market share, as it remains the core solution for automation and compliance.

- Leading Deployment: Cloud, set to dominate due to scalability, lower costs, and real-time accessibility.

| Key Insights | Details |

|---|---|

|

Debt Collection Software Market Size (2026E) |

US$6.4 Bn |

|

Market Value Forecast (2033F) |

US$12.4 Bn |

|

Projected Growth CAGR (2026-2033) |

9.9% |

|

Historical Market Growth (2020-2025) |

9.3% |

Market Factors - Driver, Restraint, and Opportunity Analysis

Driver Analysis - Rising Volume of Debt & Non-Performing Assets (NPAs)

The growing burden of unpaid loans and delinquent accounts is a major force shaping the adoption of debt collection software. As access to credit expands across credit cards, personal loans, mortgages, and digital lending platforms, a larger pool of borrowers increases the probability of missed or delayed payments. Economic volatility, such as inflation, job uncertainty, and fluctuating interest rates, further strains borrowers’ repayment capacity, leading to a steady rise in defaults.

Financial institutions and lenders are therefore dealing with higher volumes of non-performing accounts that require timely and efficient recovery strategies. Traditional, manual collection methods struggle to keep pace with this scale, often resulting in inefficiencies, delayed follow-ups, and lower recovery rates. This creates a strong need for automated systems that can manage large portfolios of delinquent accounts simultaneously. Debt collection software addresses this challenge by enabling intelligent segmentation of borrowers, prioritization of high-risk accounts, and automated communication through multiple channels.

Growing Need for Automated & Efficient Debt Recovery

Managing delinquent accounts through manual processes has become increasingly impractical as loan volumes and customer bases expand. Traditional approaches relying on spreadsheets, call lists, and fragmented communication often lead to delays, human errors, and inconsistent follow-ups. This not only reduces recovery rates but also increases operational costs and compliance risks.

Modern debt collection software addresses these challenges by automating end-to-end workflows, from account allocation and prioritization to payment tracking and reporting. It enables organizations to set predefined rules for contacting customers, schedule reminders, and trigger actions based on borrower behavior. Such automation ensures timely engagement, minimizes missed opportunities, and improves overall efficiency. These platforms support multi-channel communication, including SMS, email, and digital portals, allowing borrowers to respond conveniently and make payments faster.

Restraint Analysis - Complex Integration with Legacy Systems

Many financial institutions still operate on outdated core systems that were not designed to support modern, API-driven applications. Connecting new debt collection software to these legacy platforms can be technically challenging, often requiring extensive customization and middleware to enable data exchange. Differences in data formats, limited interoperability, and a lack of standardized interfaces further complicate integration efforts.

These challenges can lead to longer implementation timelines, higher costs, and potential disruptions to existing operations. In some cases, critical customer or account data may be siloed across multiple systems, making it difficult to achieve a unified view needed for effective collections. Inconsistent or delayed data synchronization can also impact decision-making and reduce recovery efficiency.

Budget Constraints & Economic Uncertainty

Limited financial flexibility within organizations often slows the adoption of new debt collection technologies. During periods of economic instability, businesses tend to prioritize essential operations and cost control over investments in software upgrades or digital transformation initiatives. Even when the long-term benefits are clear, the upfront costs associated with implementation, licensing, training, and system upgrades can be difficult to justify in tight budget environments.

Uncertain market conditions, such as fluctuating interest rates, inflation, or reduced consumer spending, also make financial planning more conservative. Companies may delay or scale down technology investments to preserve cash flow and reduce risk exposure. This cautious approach can limit the adoption of advanced debt collection solutions, particularly among small and mid-sized organizations.

Opportunity Analysis - Adoption of AI, Machine Learning & Advanced Analytics

The integration of intelligent technologies is transforming how organizations approach debt recovery. Advanced algorithms can analyze large volumes of historical and real-time data to identify patterns in borrower behavior, predict the likelihood of repayment, and segment accounts based on risk levels. This allows collection teams to focus their efforts on high-priority cases and apply the most effective strategies for each segment.

Machine learning models continuously improve over time by learning from past interactions, enabling more accurate forecasting and decision-making. For example, systems can recommend the best time to contact a borrower, preferred communication channel, or suitable repayment plan, increasing the chances of successful recovery. This level of personalization enhances customer engagement while maintaining efficiency. Advanced analytics also provide deeper insights into portfolio performance, agent productivity, and recovery trends, helping organizations refine their strategies. Automation powered by these technologies reduces manual intervention, minimizes errors, and accelerates the overall collection cycle.

Digital Transformation in Banking & Financial Services

Banks and financial institutions are rapidly modernizing their operations to meet evolving customer expectations and remain competitive in a digital-first environment. Traditional, paper-based processes are being replaced with integrated digital platforms that enable faster, more transparent, and data-driven decision-making. This shift is extending beyond core banking functions to include areas such as risk management, customer engagement, and debt recovery.

As institutions digitize their lending and customer management systems, the volume of digital data available for analysis has increased significantly. This creates an opportunity to implement advanced debt collection solutions that can seamlessly integrate with existing digital ecosystems. Such tools allow real-time monitoring of delinquent accounts, automated workflows, and personalized communication strategies. Customers increasingly prefer digital interactions, including online payment portals, mobile notifications, and self-service options. Debt collection software supports these preferences by offering omni-channel communication and convenient repayment methods, improving customer experience and recovery rates.

Category-wise Analysis

Component Type Insights

The software segment is anticipated to dominate, with over 65% share in 2026, fueled by its central role in automating and optimizing debt recovery processes. Organizations increasingly rely on dedicated platforms to manage large volumes of delinquent accounts, streamline workflows, and ensure consistent communication with borrowers. These solutions offer features such as real-time tracking, analytics, compliance management, and multi-channel engagement, which significantly enhance efficiency and recovery rates. The growing adoption of cloud-based systems makes deployment more scalable and cost-effective. FICO’s Debt Manager platform is an enterprise-grade debt collection software widely used by banks and financial institutions. This solution leverages advanced analytics and automation to optimize collection strategies, enabling organizations to prioritize accounts, personalize customer interactions, and improve recovery rates.

The services segment represents the fastest-growing component, driven by the increasing need for support, customization, and ongoing system optimization. Organizations often require assistance with implementation, integration, training, and maintenance to fully utilize debt collection platforms. As systems become more advanced, demand for consulting and managed services is rising to ensure smooth operations and regulatory compliance. Additionally, many companies prefer outsourcing collection processes or technical management to reduce internal workload and focus on core activities. Experian provides not only debt collection software but also a wide range of value-added services, including consulting, strategy optimization, analytics, and portfolio evaluation. Its Collections & Recoveries suite combines software with advisory and managed services, helping organizations improve recovery strategies and operational performance.

Deployment Insights

Cloud deployment is expected to dominate, with nearly 70% share in 2026, owing to its scalability, flexibility, and cost-efficiency. Unlike on-premise systems, cloud-based platforms allow organizations to deploy solutions quickly without heavy infrastructure investments. They enable real-time data access, remote operations, and seamless updates, which are essential for managing dynamic debt portfolios. Cloud solutions support integration with digital channels and analytics tools, enhancing overall efficiency. FICO’s Debt Manager cloud solution was adopted by Raiffeisen Bank International, a major European bank. The bank implemented the cloud-based version of FICO Debt Manager to modernize its collections operations and reduce costs.

On-premise deployment is likely to be the fastest-growing, propelled by organizations with strict data security and regulatory requirements seeking greater control over sensitive financial information. This model allows companies to store and manage data within their own infrastructure, reducing exposure to external cyber risks. It is particularly preferred by large banks and institutions operating in highly regulated environments. Collect! by Comtech Systems is a well-established debt collection platform that offers fully on-premise (premise-based) deployment options for businesses. The software can be installed directly on an organization’s internal servers, allowing complete control over data storage, security, and system configuration.

Regional Insights

North America Debt Collection Software Market Trends

North America is expected to dominate, accounting for 32% revenue in 2026, powered by strong adoption of advanced technologies and a highly regulated operating environment. Financial institutions and collection agencies are increasingly leveraging automation to handle large volumes of delinquent accounts more efficiently. The use of artificial intelligence and data analytics is becoming more prominent, enabling better debtor segmentation, predictive recovery strategies, and personalized communication approaches that improve repayment outcomes.

Cloud-based deployment is gaining traction as organizations seek scalable and cost-effective solutions that support remote access and real-time data management. There remains a steady demand for secure, compliant systems that align with strict regulatory requirements governing debt collection practices and consumer data protection. There is a shift toward omni-channel communication, where companies engage borrowers through digital platforms such as email, SMS, mobile apps, and self-service portals. This approach enhances the customer experience.

Europe Debt Collection Software Market Trends

Europe's market growth is shaped by a strong focus on regulatory compliance, digital transformation, and evolving customer expectations. One of the most defining trends is the emphasis on data protection and transparency, driven by strict frameworks such as GDPR. Organizations are prioritizing software solutions that ensure secure handling of personal data, auditability, and adherence to legal requirements, as non-compliance can result in significant penalties.

The growing adoption of digital and automated collection processes is a key trend. Financial institutions are increasingly replacing manual workflows with automated systems to improve efficiency, reduce operational costs, and handle rising volumes of overdue payments. A large proportion of European enterprises are already integrating digital tools into their operations, including debt recovery functions. The market is also witnessing increased use of AI-driven analytics and predictive modeling, enabling better segmentation of borrowers and more personalized collection strategies. This improves recovery rates while maintaining customer-centric approaches.

Asia Pacific Debt Collection Software Market Trends

Asia Pacific is likely to be the fastest-growing region, fueled by its strong digital adoption and expanding financial ecosystems. One of the key trends is the rise of digital lending, fintech platforms, and financial inclusion initiatives, which are significantly increasing the volume of borrowers and, consequently, delinquent accounts. This is creating a strong demand for scalable and automated collection solutions across the region.

There is growing adoption of automation and AI-driven analytics. Organizations are increasingly using intelligent systems to optimize collection strategies, improve debtor engagement, and enhance operational efficiency. The availability of large digital datasets further supports predictive modeling and personalized recovery approaches. The region is also witnessing a shift toward multi-channel and mobile-first communication, including SMS, email, WhatsApp, and app-based interactions. This aligns with high smartphone penetration and changing customer preferences for digital engagement.

Competitive Landscape

The global debt collection software market is highly competitive, driven by a mix of established technology providers and specialized fintech companies. These players continuously invest in innovation to differentiate their offerings, focusing on features such as artificial intelligence, machine learning, and predictive analytics to enhance recovery efficiency and improve debtor engagement. Compliance capabilities are another key area of competition, as organizations increasingly seek solutions that ensure adherence to complex regulatory frameworks across different regions.

Cloud-based deployment and scalable architectures are becoming essential, enabling providers to offer flexible, cost-effective, and remotely accessible solutions that appeal to both large financial institutions and growing fintech firms. Companies are pursuing strategic partnerships with banks, payment processors, and technology integrators to expand market reach and provide end-to-end collection services.

Key Industry Developments

- In March 2026, InDebted launched Comply, a standalone API that checks debt collection communications for compliance before sending. Already used across seven markets, the system monitors messages at scale, flags customer vulnerabilities, and ensures regulatory adherence. Unlike previous internal tools, InDebted offers Comply to lenders, fintechs, and creditors as a separate product, enabling them to embed real-time compliance into their workflows.

- In May 2025, Vymo, used by over 350,000 financial sales professionals, launched CollectIQ, entering the debt collection space. The solution uses AI-driven prioritization and automation to help banks and NBFCs improve recovery outcomes and streamline collection workflows.

Companies Covered in Debt Collection Software Market

- Experian

- Fair Isaac Corporation

- Constellation Software Inc.

- CGI Group Inc.

- TransUnion

- Nucleus Software Exports Ltd.

- Chetu Inc.

- CDS Software

- Pegasystems Inc.

- Temenos Group AG

- AMEYO

- PAIR Finance

- Credgenics

Frequently Asked Questions

The global debt collection software market is projected to reach US$6.4 billion in 2026.

Rising unpaid loans and economic volatility are driving increased adoption of debt collection software.

The debt collection software market is poised to witness a CAGR of 9.9% from 2026 to 2033.

AI and advanced analytics are enabling targeted, efficient debt recovery by predicting repayment and prioritizing high-risk accounts.

Key players in the debt collection software market include Experian, Fair Isaac Corporation, TransUnion, Pegasystems Inc., Temenos Group AG, and Nucleus Software Exports Ltd.