- Medical Devices

- Cytocentrifuge Market

Cytocentrifuge Market Size, Share, and Growth Forecast, 2026 - 2033

Cytocentrifuge Market by Product Type (High Speed Centrifuge, Low Speed Centrifuge, Accessories Top of Form), Application (Cytology, Immunology, Others), End-user (Hospital Laboratories, Diagnostic Laboratories, Others), and Regional Analysis for 2026 – 2033

Cytocentrifuge Market Size and Trends Analysis

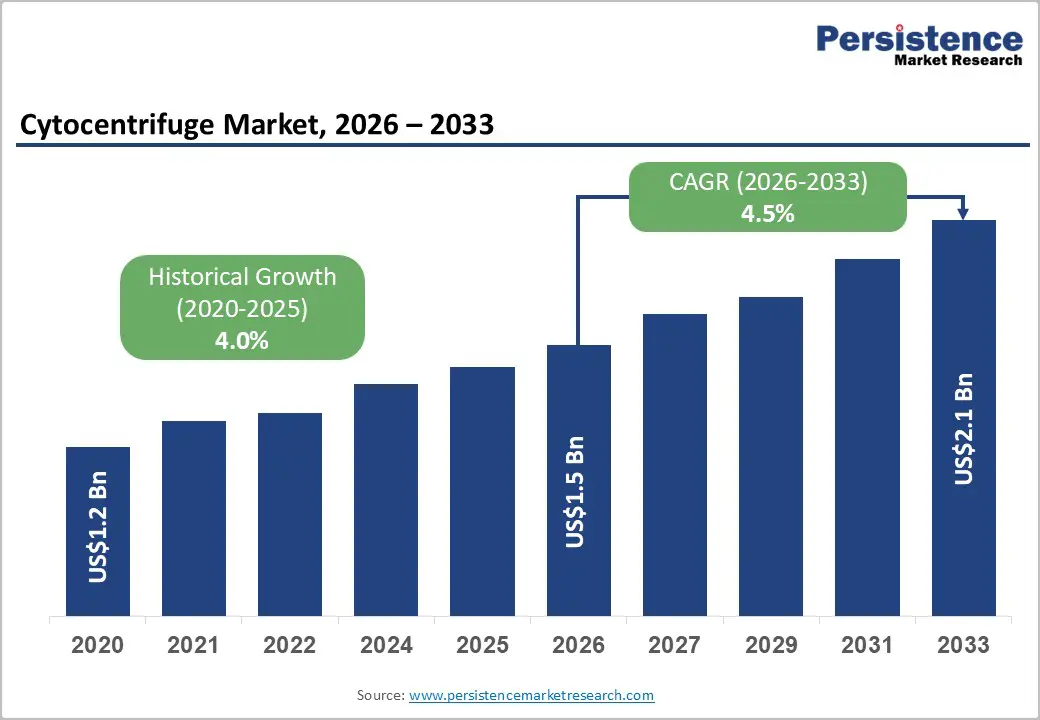

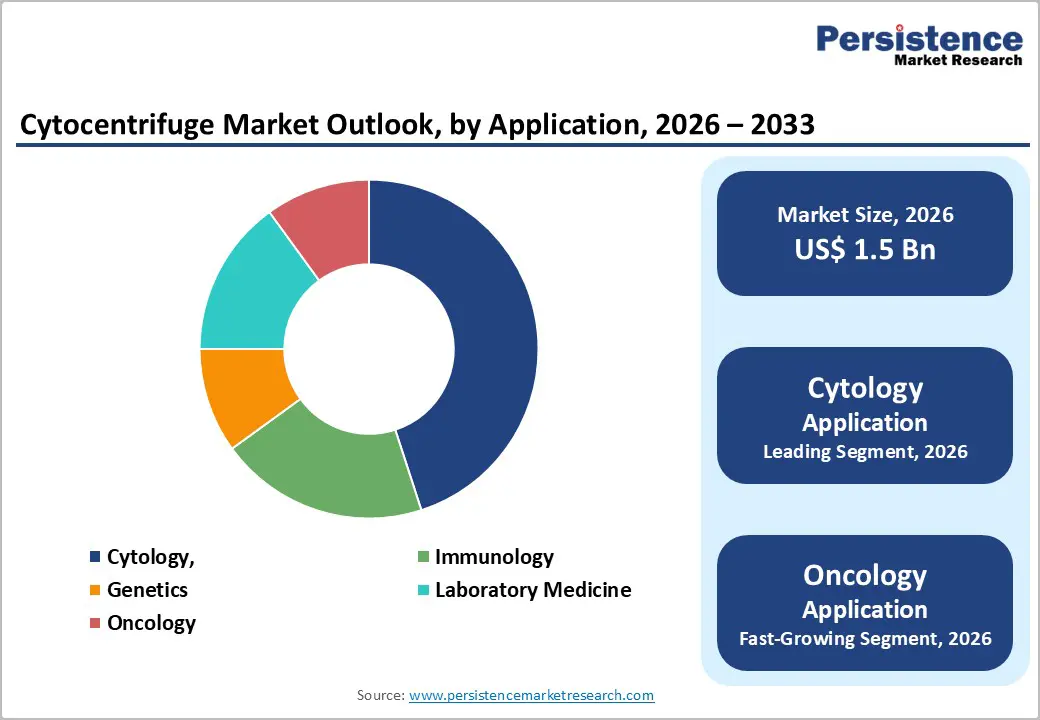

The global cytocentrifuge market size is likely to be valued at US$1.5 billion in 2026, and is expected to reach US$2.1 billion by 2033, growing at a CAGR of 4.5% during the forecast period from 2026 to 2033, driven by the increasing prevalence of cancer and infectious diseases requiring precise cytological diagnosis, rising demand for automated sample preparation in diagnostic laboratories, and growing adoption of cytocentrifuges in oncology research and hospital pathology departments. Increasing recognition of cytocentrifuges as critical for high-quality slide preparation, accurate morphological analysis, and early disease detection in emerging diagnostic and research markets remains a major driver of market growth.

Key Industry Highlights:

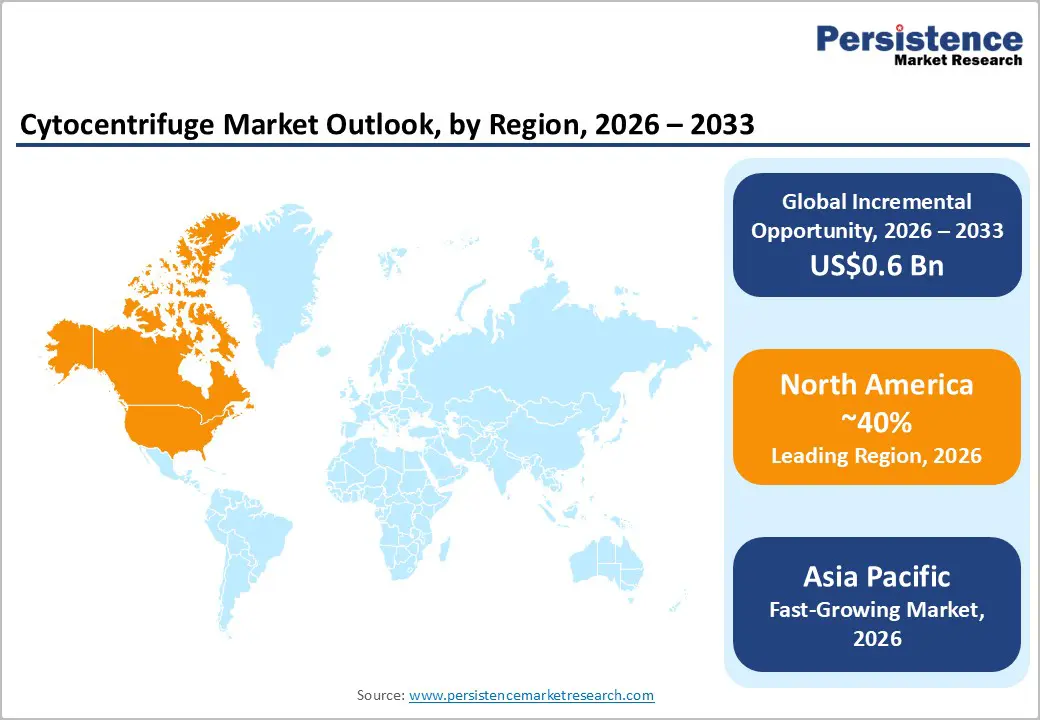

- Leading Region: North America, anticipated to account for a 40% market share in 2026, driven by advanced diagnostic infrastructure, high cancer screening rates, and strong demand in the U.S.

- Fastest-growing Region: Asia Pacific, fueled by rising cancer incidence, expanding laboratory networks, and increasing healthcare investments in India and China.

- Dominant Product Type: Low speed centrifuge, to hold approximately 55% of the market share, as it remains the workhorse for routine cytological preparations.

- Leading Application: Cytology, contributing nearly 45% of the market revenue, due to the highest routine usage volume.

| Report Attribute | Details |

|---|---|

|

Cytocentrifuge Market Size (2026E) |

US$1.5 Bn |

|

Market Value Forecast (2033F) |

US$2.1 Bn |

|

Projected Growth CAGR (2026-2033) |

4.5% |

|

Historical Market Growth (2020-2025) |

4.0% |

Market Factors – Growth, Barriers, and Opportunity Analysis

Growth Analysis – Rising Cancer Incidence and Diagnostic Laboratory Expansion

The growing burden of oncology cases worldwide is significantly increasing the demand for advanced laboratory equipment used in sample preparation, cell separation, and molecular analysis. As cancer screening programs expand and awareness improves, healthcare systems are processing a higher volume of biopsies, blood samples, and cytology specimens. This surge in diagnostic workloads is pushing laboratories to adopt faster, more reliable centrifugation solutions that can handle high-throughput testing while maintaining accuracy and consistency in results.

The rapid expansion of diagnostic laboratories is strengthening market growth. Investments in hospital labs, standalone diagnostic centers, and private testing facilities are rising to meet the demand for early detection, routine screening, and personalized treatment monitoring. Modern laboratories are upgrading infrastructure to improve turnaround time, automate workflows, and comply with stricter quality and safety standards. This transition is increasing the need for advanced centrifuges that offer higher speed, precision, and durability.

Increasing Automation and Point-of-Care Cytology

Laboratories and healthcare facilities are rapidly shifting toward automated workflows to improve efficiency, accuracy, and turnaround time. Automation reduces manual handling of samples, minimizes human error, and supports consistent processing of large test volumes. As diagnostic demand grows, automated centrifugation systems are becoming essential for streamlining routine procedures such as blood component separation, cell preparation, and sample clarification. These systems integrate easily with modern laboratory equipment, enabling faster processing and better utilization of skilled staff. The push toward automation is also driven by workforce shortages and the need to standardize results across multiple testing sites, making advanced, user-friendly centrifuges a preferred choice for clinical and research environments.

The adoption of point-of-care cytology is expanding diagnostic capabilities beyond centralized laboratories. Hospitals, clinics, and remote healthcare settings increasingly require compact and portable devices to enable rapid sample preparation near the patient. Point-of-care testing supports quicker clinical decisions, particularly in oncology screening, infectious disease diagnostics, and emergency care. This shift is driving demand for smaller, energy-efficient centrifuges that are easy to operate, maintain, and transport.

Barrier Analysis – High Equipment and Maintenance Costs

The high cost of laboratory centrifuges and their ongoing maintenance remains a major restraint for market growth, particularly in cost-sensitive healthcare and research settings. Advanced centrifuge systems require significant upfront investment due to precision engineering, high-grade materials, safety features, and automation capabilities. For small diagnostic laboratories, academic institutions, and clinics in developing regions, these capital expenses can delay or limit equipment upgrades.

In addition to purchase costs, maintenance and operational expenses add to the financial burden. Regular servicing, calibration, replacement of rotors and accessories, and compliance with safety standards increase total ownership costs over time. Downtime caused by equipment failure can also disrupt laboratory workflows and impact turnaround time for diagnostic results.

Skilled Labor Shortage and Training Requirements

Limited availability of trained laboratory professionals and the growing complexity of diagnostic equipment are creating challenges for the widespread adoption of advanced centrifuge systems. Modern centrifuges require skilled operators to handle sample preparation, optimize protocols, ensure safety compliance, and perform routine calibration. In many healthcare and research settings, especially in emerging regions, laboratories face difficulties in recruiting and retaining personnel with the required technical expertise.

Training new staff also involves time and financial investment, as operators must learn equipment handling, maintenance procedures, and quality control practices. Frequent staff turnover further increases the burden on laboratories to provide continuous training, which can slow operational efficiency and increase the risk of errors.

Opportunity Analysis – Growth in Automated Cytocentrifuges and Oncology Diagnostics

Advancements in laboratory automation are reshaping how cytology samples are prepared and analyzed, with automated cytocentrifuges gaining strong adoption across clinical and research settings. These systems standardize cell deposition on slides, reduce manual handling, and improve consistency in sample preparation. By minimizing variability, automated cytocentrifuges support more accurate microscopic evaluation and digital pathology workflows. Their ability to process higher sample volumes with minimal operator intervention also helps laboratories manage rising diagnostic workloads while improving turnaround times and operational efficiency.

The growing focus on oncology diagnostics is accelerating demand for reliable cytology and molecular testing tools. Early detection, disease monitoring, and treatment response assessment rely heavily on high-quality sample preparation from blood, body fluids, and tissue aspirates. As cancer care increasingly moves toward precision medicine, laboratories require equipment that can deliver reproducible results across large patient populations. Automated cytocentrifuges address these needs by enhancing slide quality, reducing contamination risks, and integrating smoothly into modern laboratory automation ecosystems.

Aftermarket Services and Consumables

Aftermarket services and consumables represent a strong and recurring growth avenue for the centrifuge and cytocentrifuge market. Once equipment is installed in laboratories, hospitals, and research centers, end users require continuous support to ensure smooth and reliable operation. Regular servicing, preventive maintenance, calibration, and timely repairs are essential to maintain performance, accuracy, and compliance with safety standards. Service contracts and extended warranties not only reduce unexpected downtime for laboratories but also help manufacturers build long-term customer relationships and stable revenue streams.

Consumables such as rotors, buckets, tubes, slide chambers, filters, and sample accessories require periodic replacement due to wear and contamination risks. As testing volumes increase, the demand for these components grows proportionally, creating predictable, repeat purchase cycles. Laboratories also prefer certified and compatible consumables to avoid equipment damage and ensure consistent test results. This dependency on approved accessories strengthens brand loyalty and opens opportunities for bundled service-and-consumable offerings.

Category-wise Analysis

Product Type Insights

Low speed centrifuge is anticipated to dominate the market, accounting for 55% of the market share in 2026. Its dominance is driven by its wide usage across routine clinical and laboratory applications. These systems are commonly used for blood separation, urine analysis, cytology sample preparation, and basic cell processing, making them essential equipment in hospitals and diagnostic laboratories. Their ease of operation, lower acquisition cost, and reduced maintenance requirements compared to high-speed models encourage broader adoption, especially in high-volume testing environments. The Shandon Cytospin 4 from Thermo Fisher Scientific is designed to efficiently concentrate cells from fluid specimens onto slides, facilitating precise morphological analysis for diagnostic purposes.

High speed centrifuge represents the fastest-growing product type, due to increasing use in research applications and expanding inclusion in molecular cytology and their expanding role in advanced diagnostics and biomedical research. These systems enable rapid separation of fine cellular components, nucleic acids, proteins, and subcellular fractions, which are essential for molecular biology, genomics, and oncology workflows. Increasing adoption of precision medicine and complex diagnostic assays is driving demand for higher rotational speeds and better temperature control to preserve sample integrity. The CYTOfast Cytology Centrifuge from Hospitex International is a high-speed benchtop cytocentrifuge (up to ~4,000 rpm) that efficiently concentrates and deposits cells onto slides for consistent microscopic analysis. Its optimized rotor and rapid processing capabilities make it ideal for advanced cytology, research, and diagnostic applications requiring precise cell morphology.

Application Insights

The cytology segment is expected to dominate the market, contributing nearly 45% of revenue in 2026, fueled by its use for routine screening, early disease detection, and cancer diagnostics. Procedures such as Pap smears, fine needle aspiration, and fluid cytology rely heavily on centrifugation to concentrate and prepare cells for microscopic examination. The high volume of samples processed daily in hospitals and diagnostic laboratories increases continuous demand for centrifuges and cytocentrifuges. iFuge CYTO CYTOSLIDE CENTRIFUGE, this cytology-specific centrifuge is designed to prepare cell smears for microscopic examination, particularly useful in cervical cytology testing (e.g., Pap smears) where cell suspension samples are concentrated and spread on slides for diagnostic evaluation.

The oncology segment represents the fastest-growing application, propelled by rising demand for early cancer detection, disease monitoring, and treatment response assessment. Oncology diagnostics rely heavily on high-quality sample preparation from blood, body fluids, and tissue aspirates, which increases the use of centrifuges and cytocentrifuges in routine workflows. Advances in precision medicine and targeted therapies also require frequent molecular and cytological testing, driving higher sample volumes in clinical laboratories. In cancer diagnostics laboratories, high-speed centrifugation is routinely used to prepare and isolate cell-free DNA (cfDNA) from patient plasma samples for molecular testing of oncogenic mutations such as EGFR in non–small cell lung cancer. Studies have shown that applying an additional high-speed centrifugation step improves the sensitivity of detecting EGFR mutations in commercial in vitro diagnostic assays used to guide targeted therapy decisions.

Regional Insights

North America Cytocentrifuge Market Trends

North America is projected to dominate, accounting for nearly 40% of the share in 2026, driven by the region’s high cancer screening rates, advanced pathology infrastructure, and high public awareness of diagnostic accuracy benefits. Distribution systems in the United States and Canada provide extensive support for cytocentrifuge programs, ensuring wide accessibility across low-speed, cytology, and hospital laboratory populations. Increasing demand for automated, convenient, and easy-to-use forms is further accelerating adoption, as these formats improve slide quality and reduce barriers associated with manual preparation.

Innovation in cytocentrifuge technology, including stable high-speed, improved aerosol-tight delivery, and targeted oncology enhancement, is attracting significant investment from both public and private sectors. Government initiatives and CDC campaigns continue to promote use against diagnostic risks, accuracy concerns, and emerging cancer threats, creating sustained market demand. The growing focus on oncology grades and specialty uses, particularly for cytology and others, is expanding the target applications for cytocentrifuges.

Europe Cytocentrifuge Market Trends

Europe's growth is supported by increasing awareness of cytological diagnosis benefits, strong regulatory systems, and government-led cancer screening programs. Countries such as Germany, France, the U.K., and Italy have well-established pathology frameworks that support routine cytocentrifuge use and encourage adoption of innovative low-speed delivery methods. These high-precision formulations are particularly appealing for cytology populations, regulation-conscious labs, and hospital users, improving accuracy and coverage rates.

Technological advancements in cytocentrifuge development, such as enhanced rotor systems, application-targeted delivery, and improved high-speed grades, are further boosting market potential. European authorities are increasingly supporting research and trials for cytocentrifuges against both routine and specialized needs, strengthening market confidence. The growing emphasis on convenient, reliable options is aligned with the region’s focus on preventive cancer detection and lab efficiency. Public awareness campaigns and promotion drives are expanding reach in both hospital laboratories and diagnostic centers, while suppliers are investing in automated models and novel variants to increase efficacy.

Asia Pacific Cytocentrifuge Market Trends

Asia Pacific is likely to be the fastest-growing market for cytocentrifuges in 2026, driven by rising cancer incidence, increasing government initiatives, and expanding application programs across the region. Countries such as China, India, Japan, and South Korea are actively promoting cytocentrifuge campaigns to address diagnostic growth and emerging oncology needs. Cytocentrifuges are particularly attractive in these regions due to their cost-effective administration, ease of adoption, and suitability for large-scale hospital laboratories and cytology drives in both urban and semi-urban populations.

Technological advancements are supporting the development of stable, effective, and easy-to-use cytocentrifuges, which can withstand challenging sample conditions and minimize artifact dependence. These innovations are critical for reaching domestic labs and improving overall diagnostic coverage. Growing demand for low-speed, cytology, and hospital laboratory applications is contributing to market expansion. Public-private partnerships, increased healthcare expenditure, and rising investment in cytocentrifuge research and production capacity are further accelerating growth. The convenience of cytocentrifuge delivery, combined with improved accuracy and reduced risk of misdiagnosis, positions it as a preferred choice.

Competitive Landscape

The global cytocentrifuge market reflects a split between established life-science instrument leaders and nimble automation specialists. In North America and Europe, Thermo Fisher Scientific and SLEE Medical GmbH maintain leadership through sustained R&D investment, deep laboratory networks, and strong ties with pathology workflows. Their portfolios span reliable low-speed platforms for routine cytology and higher-performance systems for research labs, helping standardize slide quality and reduce preparation artifacts at scale.

Across Asia Pacific, regional manufacturers compete on value, delivering cost-competitive systems that improve access for fast-growing diagnostic labs. Partnerships, collaborations, and targeted acquisitions are consolidating expertise, widening product ranges, and accelerating commercialization cycles. Meanwhile, high-speed solutions address demanding research workflows and support oncology testing by improving sample purity and throughput.

Key Industry Developments:

- In March 2025, Thermo Fisher Scientific Inc., a global leader in serving science, introduced new lines of floor-model centrifuges that provided more sustainable solutions without compromising performance or sample security. The company launched the Thermo Scientific™ Cryofuge™, Thermo Scientific™ BIOS, and Thermo Scientific™ LYNX centrifuges as the first floor-model centrifuges to feature natural refrigerant cooling systems compliant with European Union (E.U.) and U.S. Environmental Protection Agency (EPA) F-gas regulations.

- In June 2024, Sphere Bio, a provider of microfluidics-based solutions for single-cell analysis and isolation, announced the launch of Cyto-Cellect®PLUS. In conjunction with the company’s Cyto-Mine® platform, the new assay delivered a streamlined method to measure antibody production in single cells by rapidly detecting secreted human IgG. The solution enabled researchers to identify and select the highest-productivity cells, improving efficiency in cell line development.

Companies Covered in Cytocentrifuge Market

- Thermo Fisher Scientific Inc.

- SLEE Medical GmbH

- Histo Line Laboratories

- Sigma Diagnostics Inc.

- HemoCue America

- Ortoalresa

- SCILAB Co., Ltd.

- Simport

- Centurion Scientific

Frequently Asked Questions

The global cytocentrifuge market is projected to reach US$1.5 billion in 2026.

Rising cancer incidence and diagnostic laboratory expansion are key drivers.

The cytocentrifuge market is poised to witness a CAGR of 4.5% from 2026 to 2033.

Automated cytocentrifuges and oncology diagnostics and expansion in Asia Pacific and home-based diagnostics are key opportunities.

Thermo Fisher Scientific, SLEE Medical, Sigma Diagnostics, HemoCue America, and Ortoalresa are the key players.