- Medical Devices

- Cryotherapy Market

Cryotherapy Market Size, Share, Trends, Growth, and Regional Forecast, 2026 - 2033

Cryotherapy Market by Product (Cryosurgical Instruments, Cryogenic Chambers, Cryosaunas, Localized Cryotherapy Devices, Others), Application (Surgical Application, Pain Management, Sports Medicine & Recovery, Dermatology & Aesthetic, Others), End-user (Hospitals & Specialty Clinics, Cryotherapy & Wellness Centers, Others), and Regional Analysis from 2026 - 2033

Cryotherapy Market Share and Trends Analysis

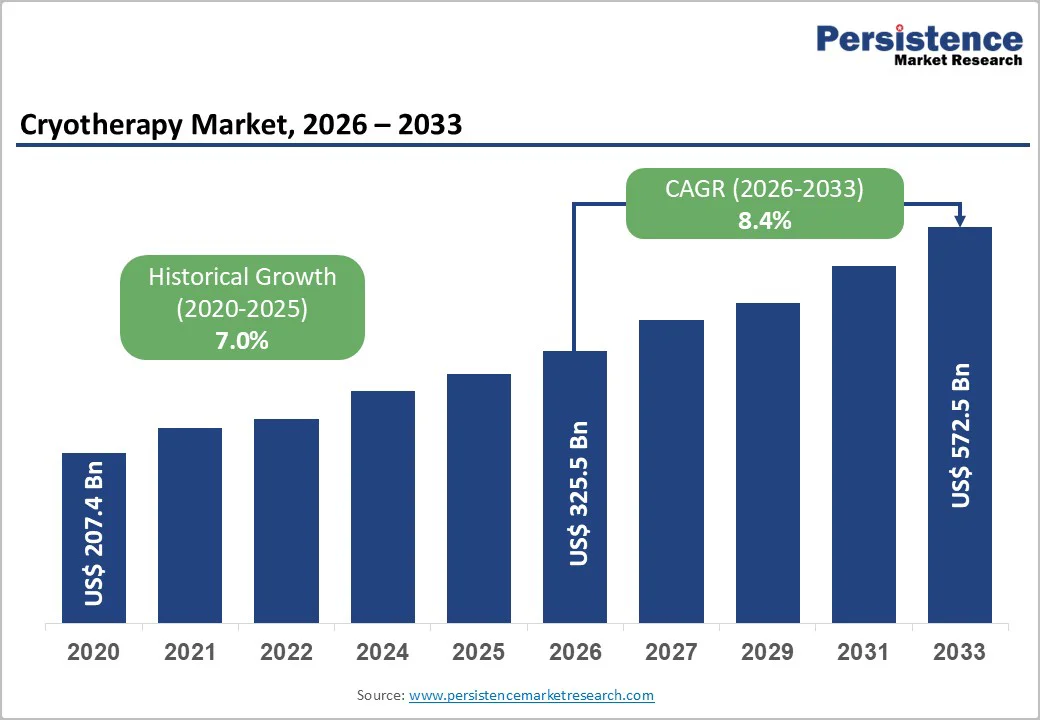

The global cryotherapy market size is estimated to grow from US$ 325.5 billion in 2026 to US$ 572.5 billion by 2033, growing at a CAGR of 8.4% during the forecast period from 2026 to 2033.

The market is expanding, driven by rising demand for minimally invasive treatments, growing sports and fitness culture, and broader use in pain management and aesthetics. North America dominates due to strong infrastructure, early technology adoption, and reimbursement support. Asia Pacific is the fastest-growing region, propelled by increasing wellness investments and rapid healthcare modernization.

Key Industry Highlights:

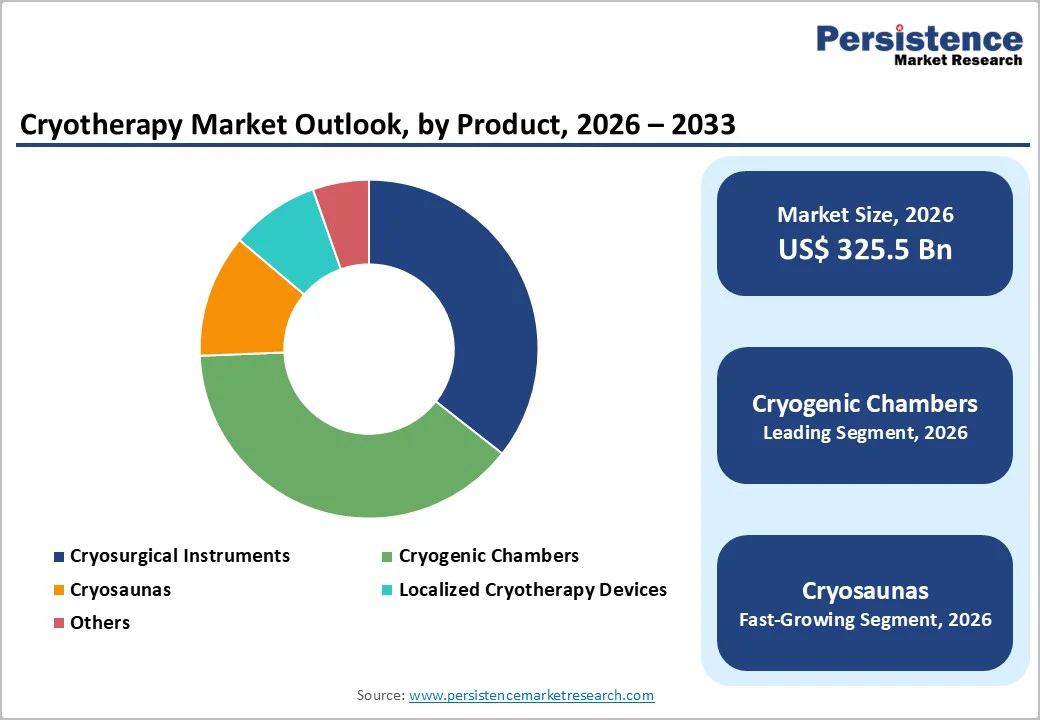

- Dominant Segment: Cryogenic chambers lead the cryotherapy market in 2025 with 38.8% share, as the dominant product segment, supported by their widespread adoption in sports recovery, pain management, and holistic wellness therapies. These chambers offer controlled, full-body exposure to ultra-low temperatures, enabling faster muscle recovery, reduced inflammation, and enhanced athletic performance.

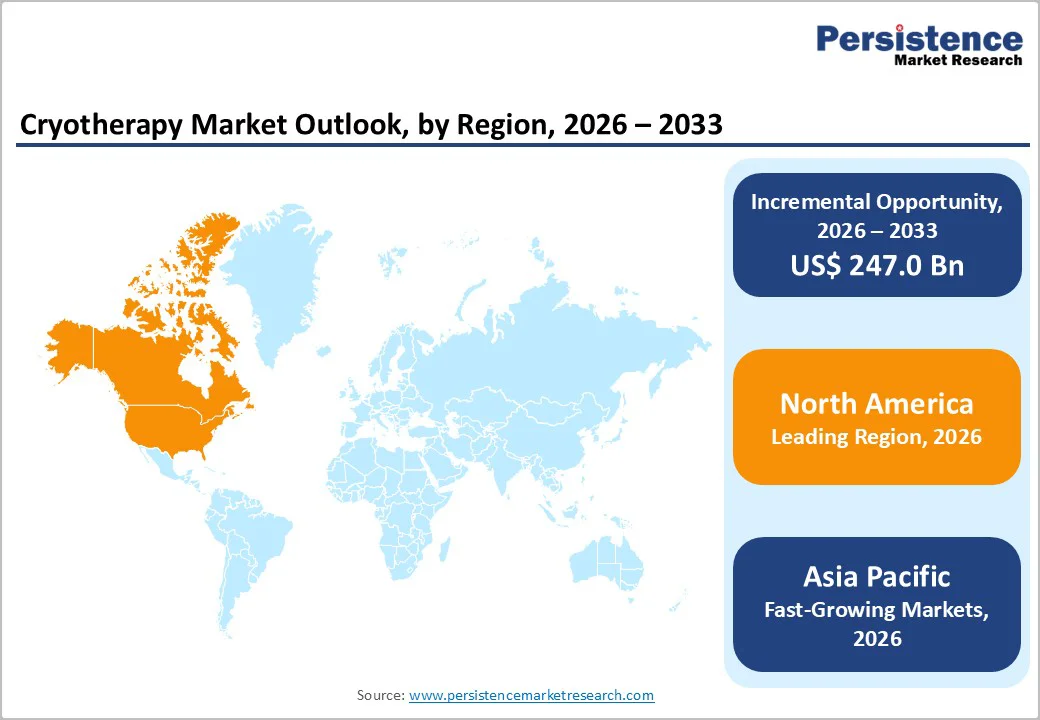

- Dominant Region: North America remains the leading region due to advanced healthcare infrastructure, strong adoption in sports medicine, and a well-developed wellness and fitness ecosystem. Asia Pacific is the fastest-growing region, propelled by rising consumer wellness spending, expanding medical tourism, and increasing use of localized and whole-body cryotherapy across hospitals, clinics, and premium fitness centers.

- Market Drivers: Growth is fueled by the rising prevalence of chronic pain and musculoskeletal disorders, increased demand for non-invasive rehabilitation therapies, expanding use in sports recovery, and growing awareness of aesthetic and wellness benefits. Technological advancements such as electric cryo-chambers and safer localized devices also support broader adoption across medical and non-medical settings.

- Market Opportunity: Key opportunities include next-generation electric cryochambers, portable localized cryotherapy devices, integration with physiotherapy and sports-recovery programs, expansion into dermatology and aesthetic clinics, and growing adoption in emerging markets. Partnerships with fitness chains, rehabilitation centers, and wellness studios, along with improved affordability and service-based cryotherapy models, can unlock long-term market expansion.

| Key Insights | Details |

|---|---|

|

Global Cryotherapy Market Size (2026E) |

US$ 325.5 Bn |

|

Market Value Forecast (2033F) |

US$ 572.5 Bn |

|

Projected Growth (CAGR 2026 to 2033) |

8.4% |

|

Historical Market Growth (CAGR 2020 to 2025) |

7.0% |

Market Dynamics

Driver - Growing Adoption in Sports Medicine and Fitness Recovery

The growing adoption of cryotherapy in sports medicine and fitness recovery is a significant driver of the Cryotherapy Market. Whole-body and localized cryotherapy are increasingly used for post-exercise recovery, pain management, and injury rehabilitation. Studies indicate that athletes experience improved joint flexibility and reduced muscle stiffness, which helps lower the risk of re-injury and accelerates recovery after intense workouts. Cold therapy modalities, including cryosaunas and cryogenic chambers, are widely integrated into sports medicine clinics and physiotherapy centers to manage inflammation and control acute injuries. Delayed-onset muscle soreness is also effectively reduced, allowing athletes to resume training or competition sooner. The perception of faster recovery and enhanced performance is driving gyms, athletic training facilities, and professional sports teams to adopt cryotherapy solutions. This recurring demand encourages the installation of cryochambers and localized devices, supporting stable revenue streams and stimulating market expansion in both medical and wellness-focused segments.

Restraints - Lack of Standardized Treatment Protocols

The lack of standardized treatment protocols is a major restraint for the cryotherapy market, limiting consistent adoption and clinical confidence. Whole-body cryotherapy treatments vary widely, with chamber temperatures ranging from –110 °C to –140 °C and exposure times from 1 to 4 minutes or more, with no consensus on optimal conditions. This variability leads to inconsistent outcomes, as some studies report measurable benefits in reducing inflammation and accelerating recovery, while others show minimal effects or potential drawbacks, such as blunted muscle adaptation. Safety guidelines also differ across centers, with variations in contraindications and monitoring practices, which can increase the risk of adverse events. This inconsistency makes clinicians hesitant to recommend cryotherapy routinely and reduces patient trust, particularly in medical and rehabilitation settings. Additionally, the lack of universal protocols complicates training, regulatory approval, and device adoption, slowing market growth despite rising awareness and demand in sports medicine, wellness, and pain management.

Opportunity - Next-Generation Cryotherapy Devices

The emergence of next-generation cryotherapy devices, especially electrically powered, nitrogen-free cryochambers and compact portable units, is unlocking a new growth frontier. Modern devices such as the first electric whole-body chambers reach ultra-low temperatures (down to –140 °C) without reliance on liquid nitrogen, improving safety, ease of installation, and operation. Electric chambers have recently accounted for nearly half of new cryotherapy installations, replacing traditional gas-based systems. At the same time, compact cryosaunas and portable/localized cryo-units make cryotherapy viable for gyms, spas, rehabilitation clinics, and even home-use, dramatically expanding the potential customer base beyond hospitals. As wellness centers, sports recovery facilities, and fitness studios increasingly adopt these user-friendly, energy-efficient systems, overall market demand is growing. Thus, technological evolution toward safer, more accessible, and lower-cost cryotherapy solutions represents a significant growth opportunity for the global cryotherapy market.

Category-wise Analysis

By Product Insights

Cryogenic Chambers dominate with 38.8% share of the global market in 2025, as they offer a rapid, full-body cold exposure that enhances recovery and reduces pain efficiently. Studies show that whole-body cryotherapy reduces post-exercise muscle soreness in approximately 80% of cases and improves performance in about 70% of users. A typical session lasts only 2–4 minutes, allowing high throughput in gyms, wellness centers, and rehabilitation clinics compared with traditional ice therapy or cold-water immersion. The systemic exposure triggers anti-inflammatory and analgesic responses, lowering oxidative stress and supporting rehabilitation from musculoskeletal injuries and chronic pain. Their effectiveness for both athletic recovery and broader wellness applications, combined with growing installation in fitness, sports, and clinical facilities, has made cryogenic chambers the leading product segment, capturing the largest share of the global Cryotherapy Market.

By Application Insights

Surgical applications dominate the cryotherapy market because cryosurgery and cryoablation are widely used in oncology and other medical fields for tumors in the kidney, liver, lung, prostate, and breast. For early-stage renal-cell carcinoma (tumors ≤3 cm), cryoablation has demonstrated outcomes comparable to traditional surgery, with low cancer-specific mortality. The procedure offers key advantages, including minimal blood loss, shorter recovery times, reduced hospitalization, and lower complication rates, making it a preferred choice in hospitals and specialized clinics. As global cancer incidence rises, demand for effective, minimally invasive tumor ablation grows, directly driving adoption of cryotherapy in surgical settings. These clinical benefits, coupled with expanding hospital infrastructure and physician preference, solidify surgical applications as the largest segment in the global Cryotherapy Market.

Regional Insights

North America Cryotherapy Market Trends

North America dominates the cryotherapy market with 39.2% share in 2025, due to a high prevalence of chronic diseases and strong healthcare and wellness infrastructure. Approximately 129 million adults in the U.S. have at least one major chronic condition, many experiencing chronic pain or musculoskeletal issues, driving demand for non-invasive therapies like cryotherapy. Additionally, over 35% of U.S. adults are obese, increasing the need for recovery, pain management, and wellness interventions. The region’s well-established sports, fitness, and rehabilitation culture, with widespread gyms, athletic programs, and physiotherapy centers, supports rapid adoption of cryogenic chambers and localized cryotherapy devices. High consumer awareness, advanced healthcare infrastructure, and integration of cryotherapy in both medical and wellness settings make North America the largest and most mature cryotherapy market globally.

Europe Cryotherapy Market Trends

Europe is a key region in the cryotherapy market due to its high prevalence of obesity and musculoskeletal disorders, which drive demand for non-invasive therapies. Approximately 59% of adults in the EU are overweight or obese, with one in six adults classified as obese, increasing the risk of chronic pain, joint disorders, and cardiovascular conditions. Musculoskeletal disorders affect around 30% of the EU population, with more than 60 million adults experiencing persistent back or neck pain and over 63 million dealing with osteoarthritis. The widespread prevalence of obesity-related comorbidities and chronic pain makes cryotherapy highly relevant for pain management, rehabilitation, and wellness. Combined with advanced wellness infrastructure, an aging population, and rising demand for minimally invasive recovery solutions, Europe represents a large and growing market opportunity.

Asia Pacific Cryotherapy Market Trends

Asia Pacific is witnessing a sharp rise in obesity and overweight rates: the region accounts for nearly 1 billion overweight or obese adults, about two in five adults locally. The surge is driven by urbanization, sedentary lifestyles, and dietary shifts. Rapid growth in obesity raises demand for recovery, pain-management, and wellness treatments, fueling cryotherapy adoption. Meanwhile, the fitness and physical-activity market in the Asia Pacific is expanding fast — regional consumers increasingly spend on gyms, wellness centers, and recovery therapies. Growing middle-class disposable income, rising health awareness, and strengthening wellness infrastructure further support the rapid uptake of cryogenic chambers and localized cryotherapy services across the region.

Competitive Landscape

The competitive landscape of the global Cryotherapy Market is moderately fragmented, with a mix of established medical device manufacturers and specialized therapeutic equipment firms vying for market share. Leading companies include Zimmer MedizinSysteme GmbH, Medtronic, Boston Scientific Corporation, CryoConcepts LP, Impact Cryotherapy, and Erbe Elektromedizin GmbH, among others. These players compete through continuous product innovation, expanded geographic reach, and strategic collaborations to enhance device performance, safety, and clinical adoption. Many focus on diversifying offerings across cryochambers, localized cryotherapy systems, and cryoablation devices to serve applications in pain management, dermatology, oncology, and wellness sectors. Smaller niche manufacturers and regional firms also contribute to market dynamics by targeting specific segments such as portable and consumer cryotherapy solutions. Strong brand positioning, technological advancements, and robust distribution networks remain central to gaining a competitive advantage in this evolving market.

Key Industry Developments:

- In July 2025, A new cryotherapy technique was successfully used to remove a foreign body from a child, offering a minimally invasive alternative to traditional surgical procedures. The method involved freezing and extracting the object safely, reducing tissue damage and recovery time.

- In May 2025, Recovery Suite launched a new mobile recovery solution, aiming to revolutionize accessibility to advanced therapies. The solution offered patients convenient, on-demand access to recovery treatments without the need to visit specialized clinics or wellness centers. By combining portability with state-of-the-art technology, the mobile platform enhanced patient experience, enabling broader adoption of recovery therapies across home, fitness, and rehabilitation settings.

Companies Covered in Cryotherapy Market

- C A Manufacturing Sp zoo

- Cryo Innovations

- CRYO Science

- CryoBuilt, Inc.

- CryoLiving

- Cryomed

- CRYONiQ

- CYRO-XS

- MECOTEC GmbH

- Vacuactivus

- Others

Frequently Asked Questions

The global cryotherapy market is projected to be valued at US$ 325.5 Bn in 2026.

Rising chronic pain, sports recovery demand, wellness trends, technological advances, and growing aesthetic applications drive growth.

The global cryotherapy market is poised to witness a CAGR of 8.4% between 2026 and 2033.

Emerging markets, portable devices, next-generation chambers, aesthetic applications, and partnerships for distribution and patient engagement.

C A Manufacturing Sp zoo, Cryo Innovations, CRYO Science, CryoBuilt, Inc., CryoLiving, Cryomed