- Renewable Energy

- Solar PV Panels Market

Solar PV Panels Market Size, Share, and Growth Forecast, 2026 - 2033

Solar PV Panels Market by Technology Type (Crystalline Silicon, Thin-Film), Application (Residential, Commercial, Industrial, Utilities), and Regional Analysis for 2026 - 2033

Solar PV Panels Market Size and Trends Analysis

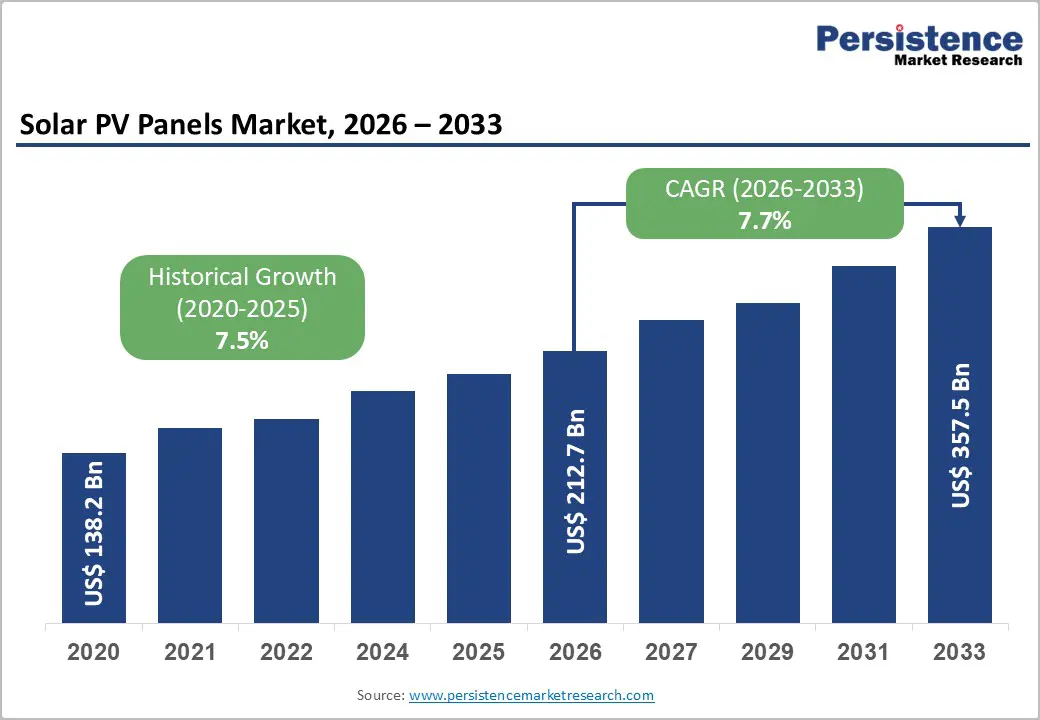

The global solar PV panels market size is likely to be valued at US$212.7 billion in 2026 and is expected to reach US$357.5 billion by 2033, growing at a CAGR of 7.7% during the forecast period from 2026 to 2033, driven by the continued decline in solar module prices, improving cost competitiveness of solar power versus conventional energy sources, and strong government support through subsidies, tax incentives, and renewable energy mandates across major economies.

Growing concerns about climate change, energy security, and the need to reduce carbon emissions are driving the worldwide adoption of solar photovoltaic (PV) systems across residential, commercial, industrial, and utility-scale sectors. Technological progress, including high-efficiency crystalline silicon panels, bifacial modules, and advanced cell architectures, combined with the expanding integration of solar PV with energy storage solutions, is improving system performance, reliability, and grid stability, thereby further accelerating market growth.

Key Industry Highlights:

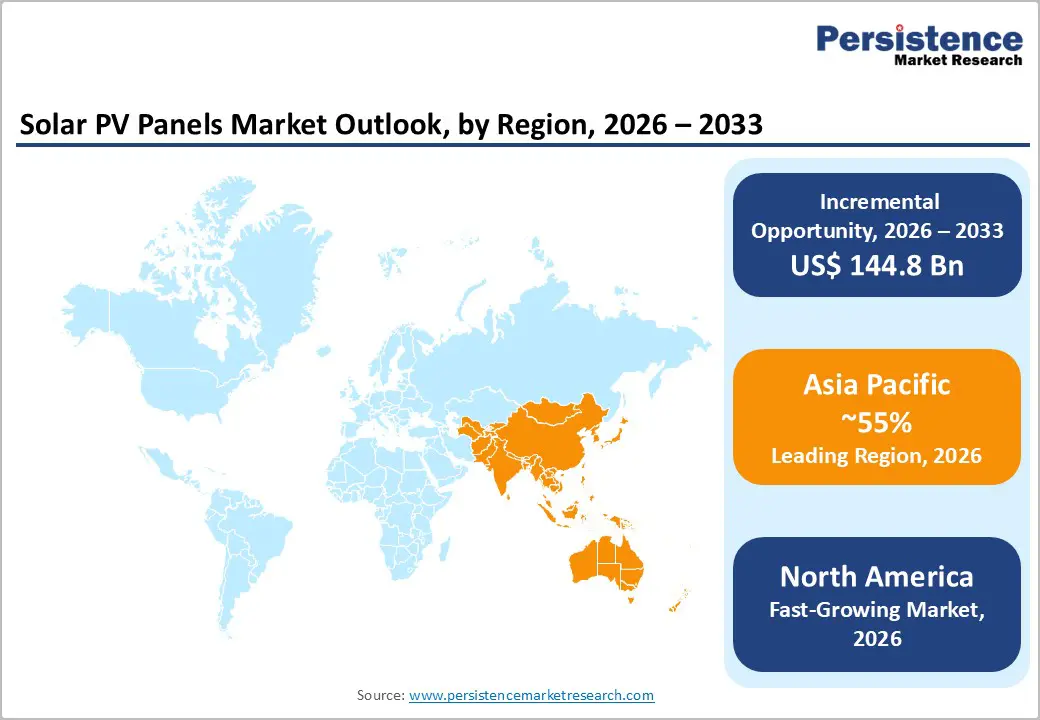

- Leading Region: Asia Pacific is anticipated to be the leading region, accounting for a market share of 55% in 2026, driven by strong manufacturing capacity in China, supportive government policies in India, and rising solar adoption across Japan and ASEAN economies.

- Fastest-growing Region: North America is likely to be the fastest-growing region in solar PV panels in 2026, supported by strong policy incentives, corporate renewable procurement, and growing utility-scale solar and storage deployments.

- Leading Technology Type: The crystalline silicon segment is projected to represent the leading technology type in 2026, accounting for 90% of the revenue share, supported by high efficiency, reliability, and a well-established global supply chain.

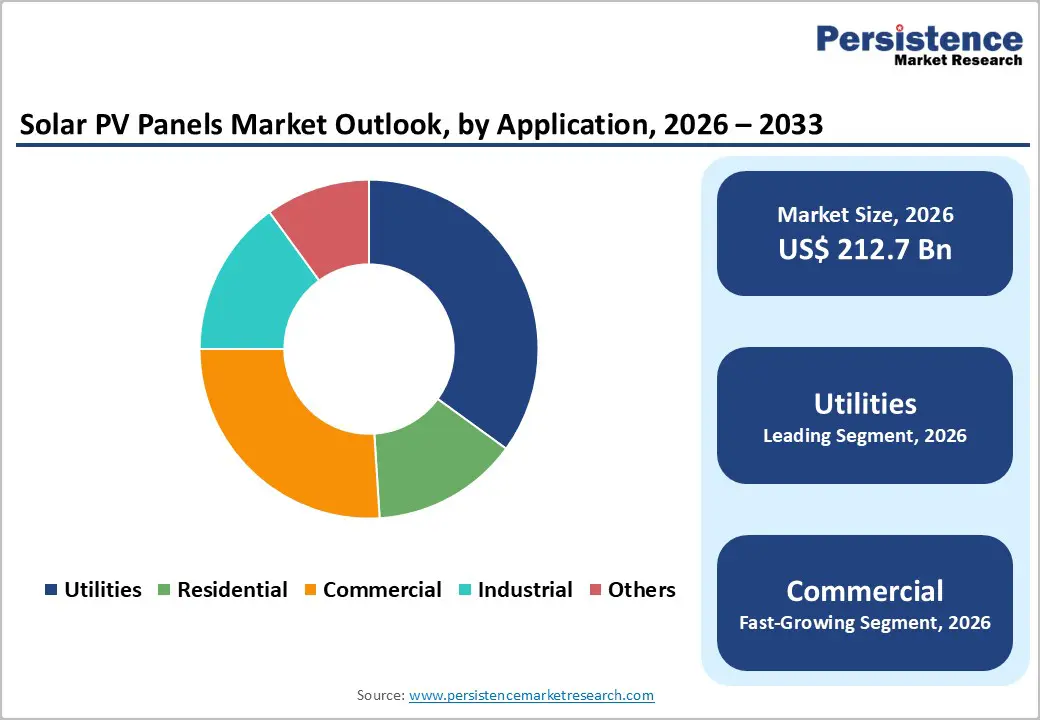

- Leading Application: Utilities are anticipated to be the leading application type, accounting for over 60% of the revenue share in 2026, driven by large-scale solar farms and cost-effective power generation.

| Key Insights | Details |

|---|---|

| Solar PV Panels Market Size (2026E) | US$212.7 Bn |

| Market Value Forecast (2033F) | US$357.5 Bn |

| Projected Growth (CAGR 2026 to 2033) | 7.7% |

| Historical Market Growth (CAGR 2020 to 2025) | 7.5% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Supportive Government Policies and Incentives

In major markets such as the U.S., the Inflation Reduction Act (IRA) has been a cornerstone policy, providing robust federal tax credits, including a 30% Investment Tax Credit (ITC) for residential and commercial solar installations and production and investment tax credits for utility-scale and storage projects, which enhance project economics and accelerate deployment.

National and state-level incentives such as net metering programs, state rebates, and Solar Renewable Energy Certificates (SRECs) augment solar adoption by allowing owners to offset electricity costs and create additional revenue streams. Across Europe, governments are considering looser state aid rules to enable direct grants, tax incentives, subsidized loans, and guarantees, all designed to support clean technology projects, including solar PV manufacturing and deployment.

In Asia, supportive government initiatives have been instrumental in scaling solar PV adoption and expanding domestic manufacturing capabilities. China’s long-term industrial policies include a suite of subsidies, tax rebates, and low-interest loans aimed at reducing panel production costs and fostering technological advancements, helping the country dominate global PV manufacturing. India’s policy environment combines direct consumer subsidies, tax benefits, and manufacturing support to drive both demand and supply growth in its solar industry.

Central programs such as rooftop solar subsidies, production-linked incentive (PLI) schemes for high-efficiency solar PV modules, and reduced Goods and Services Tax (GST) rates directly lower the cost of solar installations for residential and commercial adopters, while accelerated depreciation benefits and customs duty exemptions incentivize businesses to invest in solar assets.

Grid Integration and Interconnection Delays

Utility-scale and distributed solar installations grow rapidly, and electricity grids in many regions are struggling to accommodate the intermittent and decentralized nature of solar power. Existing transmission and distribution infrastructure in several markets, particularly in emerging economies, often lacks the capacity or flexibility to absorb large volumes of variable solar generation, causing delays in connecting new projects to the grid.

Regulatory approval processes and lengthy permitting procedures for grid interconnection exacerbate these delays, leading to extended project timelines and increased costs for developers. The need for technical upgrades, such as advanced inverters, energy storage, and smart grid management systems, adds complexity and capital expenditure requirements.

Grid integration and interconnection challenges remain significant barriers to the solar PV panels market, especially as utility-scale projects and rooftop solar systems expand simultaneously. In countries such as India, China, and parts of Europe, rapid solar deployment has outpaced grid readiness, resulting in curtailment of solar output, delayed commissioning, and financial losses for project developers.

Lengthy approval processes for grid connection, including compliance with technical standards, environmental assessments, and coordination between multiple authorities, can extend project timelines by several months or even years. Grid congestion from limited transmission and load imbalances can be eased with storage and smart grid solutions, though they need high upfront investment.

Integration with Energy Storage and Hybrid Systems

Traditional solar PV generation is limited by daylight availability and weather variations, which can create gaps in supply and limit grid reliability. By pairing solar arrays with battery storage technologies such as lithium-ion, flow, and emerging solid-state systems, producers can store excess daytime generation for use during peak demand or low insolation periods.

This capability improves grid stability, reduces the need for fossil fuel-based peaking plants, and supports smoother load balancing, making solar more dispatchable and economically viable. In utility-scale deployments, integrated storage enables solar plants to participate in ancillary services markets and provide capacity during critical evening demand peaks.

Hybrid energy systems that integrate solar PV panels with complementary power sources, such as wind turbines, diesel generators, or microgrid control platforms, create broader deployment opportunities, particularly in off-grid, rural, and industrial environments. These hybrid systems leverage the unique characteristics of each energy source to provide reliable power where grid infrastructure is limited or expensive to build.

For example, solar-wind hybrids balance variable solar irradiance with wind patterns, reducing overall output variability and enhancing capacity factors. Integrating storage into hybrid systems elevates performance by capturing surplus energy from both sources and deploying it during demand spikes or lulls, enabling consistent power delivery.

Category-wise Analysis

Technology Type Insights

Crystalline silicon (c-Si) is projected to dominate the solar PV panel market in 2026, contributing roughly 90% of the total revenue. This leadership is driven by its broad adoption across utility-scale, commercial, and residential installations. Utility developers particularly favor c-Si modules due to their proven reliability, predictable energy output, and lower long-term degradation rates.

For instance, LONGi Solar, a major producer of monocrystalline panels, continues to supply high-efficiency modules for large solar projects in China and India, leveraging economies of scale and cost-efficient manufacturing. Supportive government policies, incentives, and renewable energy targets further strengthen the position of crystalline silicon as the preferred PV technology in both developed and emerging markets.

The thin-film segment is expected to be the fastest-growing category over the forecast period. Its growth is supported by advantages such as reduced material usage, lightweight design, and strong performance under low-light and high-temperature conditions. These features make thin-film panels well-suited for building-integrated photovoltaics (BIPV), flexible systems, and installations on curved or unconventional surfaces.

For example, First Solar, a leading producer of cadmium telluride (CdTe) modules, has successfully deployed thin-film technology in large U.S. solar farms, demonstrating higher energy yields in diffuse sunlight and hot climates. Ongoing advances in materials and manufacturing processes have enhanced efficiency and lowered costs, positioning thin-film technology as an appealing option for specialized applications where traditional crystalline silicon panels are less effective.

Application Insights

Utilities are expected to remain the dominant end-user segment, accounting for approximately 60% of the total market revenue in 2026. This leadership is driven by the continued expansion of large-scale, ground-mounted solar farms that benefit from economies of scale and attractive project economics. Utility-scale developments represent the majority of global solar capacity additions, as governments and independent power producers invest heavily in large PV plants to achieve renewable energy targets and secure long-term power purchase agreements (PPAs).

The Bhadla Solar Park in India, one of the largest solar installations worldwide, exemplifies how utility-scale projects contribute significantly to market growth while capitalizing on declining module costs and improved financing structures. As a result, utilities achieve a lower levelized cost of electricity (LCOE) than smaller installations, enhancing solar power’s competitiveness with traditional energy sources.

The commercial segment is anticipated to be the fastest-growing application in 2026. Growth is being fueled by corporate sustainability commitments, increasing on-site energy consumption, and opportunities for cost savings. Companies are progressively deploying rooftop and on-site solar PV systems to lower electricity expenses, enhance energy reliability, and meet environmental, social, and governance (ESG) objectives.

For example, Walmart’s widespread rooftop solar installations across its U.S. stores demonstrate how commercial solar systems can deliver both economic and environmental value. Falling solar equipment prices, combined with advances in smart energy management and storage solutions, are enabling businesses to better manage energy usage, store surplus power, and engage in demand response programs.

Regional Insights

North America Solar PV Panels Market Trends

North America is likely to be the fastest-growing region, driven by strong policy support, corporate commitments to renewable energy, and increasing investment in utility-scale and distributed solar projects. Central to this trend is the influence of the Inflation Reduction Act (IRA), which provides long-term tax incentives and production credits that have significantly improved the economics of solar installations across the U.S. These incentives have encouraged utilities, developers, and end-users to accelerate capacity additions, driving demand for high-efficiency crystalline silicon modules. The growing adoption of hybrid solar systems paired with battery storage is being driven by utility operators and large commercial users seeking enhanced grid reliability and energy resilience.

Technology diversification and supply chain localization are shaping key trends in the North America solar PV panels market. Manufacturers and project developers are increasingly prioritizing domestic production to reduce dependence on imported panels and mitigate tariff-related risks.

For example, First Solar, a U.S.-based thin-film solar module producer, has expanded its manufacturing footprint to support local demand and supply utility-scale projects with high-performance cadmium telluride (CdTe) modules. This strategy aligns with federal incentives that favor domestically produced solar components under prevailing policy frameworks, strengthening the regional market’s resilience.

Europe Solar PV Panels Market Trends

Europe is likely to be a significant market for solar PV panels in 2026, driven by technology adoption and changing installation patterns, shaping the region’s renewable energy landscape. Solar PV remains a key pillar in the European Union’s decarbonization strategy, with installed capacity and generation contributing significantly to national energy mixes. Germany, Spain, and Italy remain leading markets, with robust project pipelines and supportive frameworks such as feed-in premiums, competitive auctions, and streamlined permitting processes driving momentum.

For example, Iberdrola has invested in large solar PV installations across Spain and Italy, including the 500 MW Núñez de Balboa plant, illustrating how major developers are backing Europe’s transition to clean energy and leveraging advanced bifacial module technologies to optimize performance while integrating with grid infrastructure.

The Europe solar PV market is witnessing a notable shift toward residential, commercial, and hybrid energy solutions, reflecting growing interest in self-generation, energy resilience, and integrated systems. Distributed solar, particularly rooftop installations paired with battery storage and smart energy management technologies, is gaining traction as consumers and businesses seek to lower electricity costs and enhance energy independence.

Policy measures in several member states are promoting building-integrated photovoltaics (BIPV) and simplified permitting for rooftop projects, helping drive uptake in urban and suburban environments. The emphasis on grid flexibility is also encouraging investment in solutions that address intermittency and enable smoother integration of solar generation.

Asia Pacific Solar PV Panels Market Trends

The Asia Pacific region is anticipated to be the leading region, accounting for a market share of 55% in 2026, driven by the rapid deployment of distributed and utility-scale solar projects, continued cost declines, and expanding policy support across major economies. The rise of rooftop and decentralized solar installations in both urban and rural areas, driven by falling PV module prices and government incentives, makes solar increasingly accessible to residential and commercial consumers.

Countries such as Australia have seen millions of rooftop systems installed, showcasing how decentralized generation is enhancing energy independence by reducing reliance on traditional grid power and lowering electricity costs for end-users.

Asia Pacific solar PV panels market is the regional diversification and technological advancement of manufacturing capacity, as demand for solar energy increases and supply chains evolve. While China remains the dominant global producer and installer of PV panels, other regional players are scaling production and expanding local capabilities, reducing dependency on imports and strengthening supply resilience.

For example, JA Solar has been expanding its footprint in the region by establishing manufacturing facilities and partnerships that support both domestic demand and export markets, enabling faster delivery times and cost efficiencies for solar projects in countries such as Vietnam and Indonesia.

Competitive Landscape

The global solar PV panels market exhibits a moderately fragmented structure, driven by strong demand growth, technological innovation, and intense competition among both established giants and emerging regional players. Market concentration remains significant, with the top manufacturers such as JinkoSolar, JA Solar, Trina Solar, LONGi Solar, and Canadian Solar collectively accounting for a large portion of production capacity and revenue, supported by their extensive global supply chains, vertical integration, and continuous investment in R&D to improve efficiency and lower production costs.

With key leaders including First Solar, SunPower Corporation, Hanwha Q-CELLS, and Risen Energy, competition intensifies as each company seeks to expand its share across residential, commercial, industrial, and utility segments through innovation, partnerships, and regional growth strategies. These players compete through technological differentiation, cost leadership, quality and bankability, and strategic collaborations, often differentiating themselves by focusing on advanced module performance, hybrids with energy storage, or specialized product lines for specific applications.

Key Industry Developments:

- In April 2025, National Capital Region Transport Corporation (NCRTC) launched a first-of-its-kind pilot project titled “Solar on Track” at the Namo Bharat Depot in Duhai, marking the first deployment of solar panels directly on train tracks within any RRTS or Metro network in India. Under this initiative, 28 solar panels of 550 Wp each were installed along the pit wheel track, creating a total installed capacity of 15.4 kWp across a 70-metre stretch. The project forms part of NCRTC’s broader renewable energy strategy, which aims to source 70% of its total energy requirement from renewable sources. As part of this roadmap, NCRTC plans to develop 15 MW of solar power capacity, primarily through rooftop installations across stations and depots, with 5.5 MW already operational.

- In May 2025, Oman took a significant step toward developing a domestic solar manufacturing industry by signing a land lease agreement with JA Solar OM (FZC) SPC at the SOHAR Freezone. Under this agreement, JA Solar will invest USD 565 million to establish a large-scale solar manufacturing facility spanning 32.5 hectares in Phase 2 of the Freezone. The plant is planned to have an annual capacity of 6 GW for solar cells and 3 GW for solar modules, with commercial operations expected to commence in Q1 2026. This project supports Oman’s Vision 2040 objectives by enhancing local renewable energy supply chains, lowering carbon emissions, and positioning the country as a regional hub for solar manufacturing and clean energy exports.

Companies Covered in Solar PV Panels Market

- JinkoSolar

- JA Solar

- Trina Solar

- LONGi Solar

- Canadian Solar

- Hanwha Q-CELLS

- Risen Energy

- GCL-SI

- First Solar

- SunPower Corporation

Frequently Asked Questions

The global solar PV panels market is projected to reach US$212.7 billion in 2026.

Declining module costs, supportive government policies, rising demand for clean energy, and global decarbonization initiatives.

The solar PV panels market is expected to grow at a CAGR of 7.7% from 2026 to 2033.

Integration of solar PV with energy storage and hybrid systems, expansion of utility-scale and commercial installations, growth in emerging markets, and advancements in high-efficiency panel technologies.

JinkoSolar, JA Solar, Trina Solar, LONGi Solar, Canadian Solar, Hanwha Q-CELLS, and Risen Energy are the leading players.