- Industrial Goods & Service

- Clad Pipe Market

Clad Pipe Market Size, Trends, Share, and Growth Forecasts 2025 - 2032

Clad Pipe Market Analysis By Manufacturing Process (Metallurgical Bonding, Mechanical Bonding, Weld Overlay), Thickness (3 to 6mm, 6 to 18mm, 18 to 36mm), End-use (Oil & Gas, Chemical & Petrochemical, Water Treatment & Desalination), and Regional Analysis 2025 - 2032

Clad Pipe Market Share and Trends Analysis

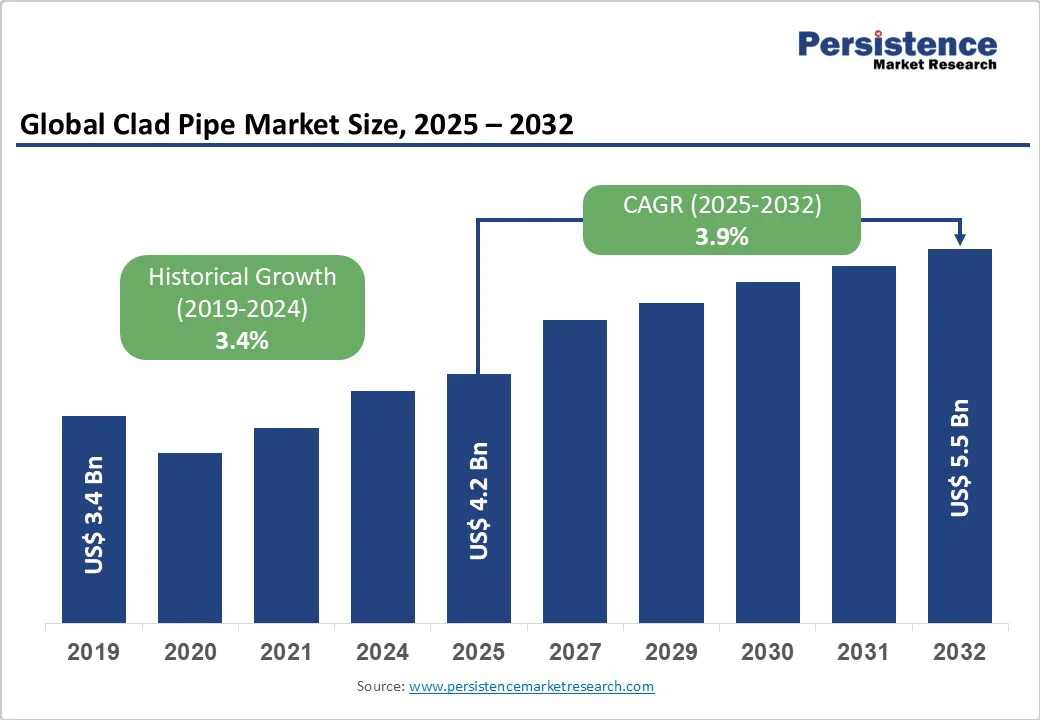

The global clad pipe market size is likely to be valued at US$4.2 billion in 2025 and is projected to reach US$5.5 billion by 2032, growing at a CAGR of 3.9% between 2025 and 2032.

The market expansion is driven by increasing demand for corrosion-resistant piping solutions in harsh environments and growing offshore oil and gas exploration activities.

Rising investments in infrastructure development across oil and gas, chemical processing, and water treatment sectors are creating sustained demand for clad pipe technologies.

Key Market Highlights

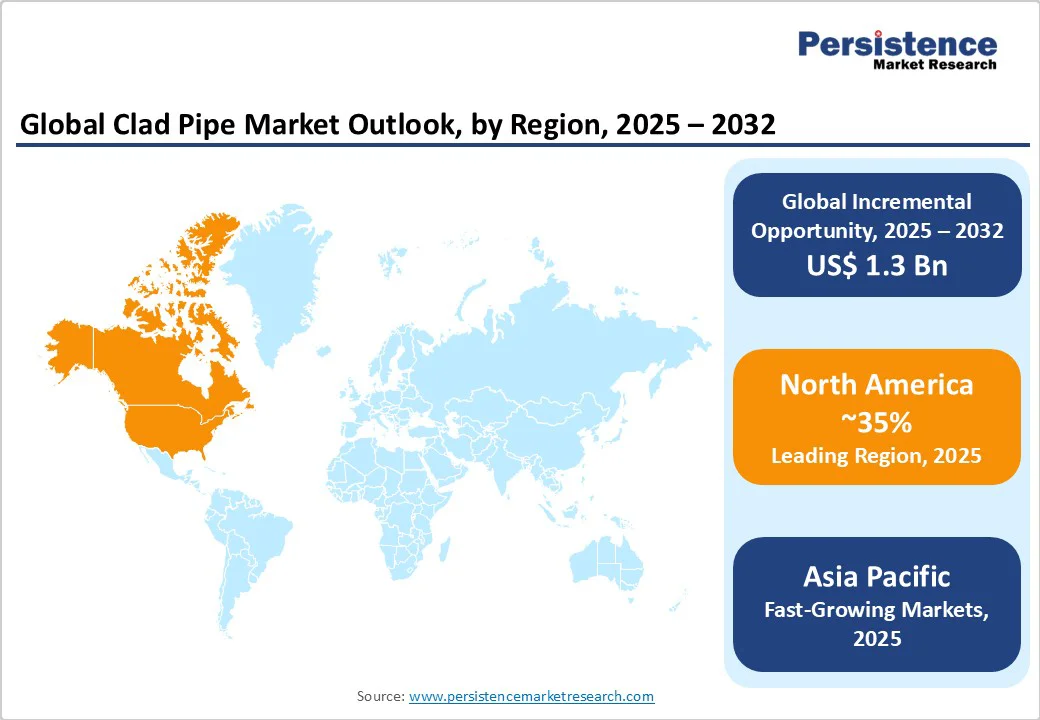

- Leading Region: North America leads the global clad pipe market with 35% share, driven by advanced offshore infrastructure and established regulatory frameworks supporting specialized materials technology adoption.

- Fastest-Growing Region: Asia Pacific represents the fastest-growing regional market at 6.2% CAGR, fueled by massive infrastructure investments in China, India, and ASEAN countries expanding energy and industrial capabilities.

- Leading Manufacturing Process: Metallurgical bonding dominates manufacturing processes with 55% market share due to superior durability and performance characteristics essential for critical industrial applications and harsh environments.

- Leading End-use: Oil & Gas emerges as the fastest-growing end-use segment, expanding at a 4.5% CAGR driven by deepwater exploration activities and increasing demand for corrosion-resistant pipeline solutions.

- Key Market Opportunity: Water treatment and desalination infrastructure present the most significant market opportunity, with US$ 50 billion in Middle Eastern investments creating sustained demand for specialized piping solutions.

| Key Insights | Details |

|---|---|

| Clad Pipe Market Size (2025E) | US$ 4.2 Bn |

| Market Value Forecast (2032F) | US$ 5.5 Bn |

| Projected Growth CAGR (2025-2032) | 3.9% |

| Historical Market Growth (2019-2024) | 3.4% |

Market Dynamics

Driver - Rising Offshore Oil and Gas Exploration Activities

The expansion of offshore drilling operations remains a key driver for the clad pipe market, as global offshore oil production is expected to rise by nearly 8% annually, according to the International Energy Agency (IEA). Offshore conditions expose pipelines to seawater, hydrogen sulfide, and carbon dioxide, making corrosion-resistant materials indispensable. Clad pipes, featuring metallurgically bonded layers of stainless steel or nickel alloys over carbon steel, offer the durability required in such hostile environments.

Deepwater and ultra-deepwater projects, which operate at depths exceeding 3,000 meters, are increasingly reliant on clad pipes for long-term reliability. Industry leaders such as BP, Shell, ExxonMobil, and Chevron are investing heavily in subsea infrastructure, fueling a 25% increase in clad pipe adoption over the last five years. Their role in ensuring pipeline integrity under extreme pressure and corrosion makes them vital for sustaining offshore oil and gas operations.

Infrastructure Modernization and Industrial Expansion

Industrial expansion, coupled with the immediate replacement of aging infrastructure, significantly boosts the demand for advanced piping systems. In 2024, the U.S. Department of Energy allocated over US$15 billion to upgrade pipelines, with a strong focus on corrosion-resistant solutions. Their superior performance in handling aggressive process fluids has positioned them as essential components in chemical and petrochemical plants, where demand is increasing by nearly 15% annually.

Water treatment and desalination plants also represent a growing application area, with clad pipes offering 30-40% longer service life compared to conventional options. Global sustainability goals further encourage investment in high-performance infrastructure, where modern welding and explosive bonding technologies enhance pipe quality and production efficiency. This combination of durability, cost-effectiveness, and adaptability makes clad pipes a preferred choice across industrial and municipal projects worldwide.

Restraint - High Manufacturing Costs and Complex Production Processes

Clad pipe manufacturing relies on advanced metallurgical techniques that require specialized equipment and highly skilled personnel, resulting in production costs that are 20-30% higher than those of conventional piping solutions. Processes such as explosive bonding and weld overlay demand precise control over temperature and pressure, resulting in longer production cycles and higher energy consumption compared to standard steel pipes.

Additionally, fluctuations in raw material prices, particularly for high-performance alloys such as stainless steel 316L, Inconel 625, and Hastelloy C-276, introduce economic uncertainty. These cost variations can significantly impact project budgets and procurement decisions, making clad pipes less attractive for cost-sensitive infrastructure projects despite their superior performance in corrosive and high-pressure environments.

Limited Manufacturing Capacity and Supply Chain Constraints

The highly specialized nature of clad pipe production has led to a concentrated supplier landscape, with only a few manufacturers globally capable of delivering large-scale orders. This limited capacity restricts market responsiveness and creates potential bottlenecks when demand surges for critical applications in oil, gas, and chemical sectors.

Supply chain disruptions further complicate production and delivery timelines. Shortages of key components, such as semiconductors for automated welding equipment, combined with geopolitical issues affecting raw material availability, can cause delays of 8-12 weeks for standard pipe specifications. Rigorous quality assurance processes, including non-destructive testing and metallurgical certification, add further time and complexity, challenging manufacturers to meet tight project schedules.

Opportunity - Expanding Water Treatment and Desalination Infrastructure

The global water scarcity challenge is driving large-scale investments in desalination and water treatment facilities, creating substantial growth opportunities for manufacturers of clad pipes. Desalination plants, particularly seawater reverse osmosis (SWRO) systems, operate under high pressures of up to 100 bar and in highly corrosive environments, making corrosion-resistant clad pipes critical for intake, high-pressure, and brine discharge lines.

Middle Eastern countries, including Saudi Arabia, the UAE, and Qatar, are collectively investing around US$50 billion in desalination projects over the next decade, many specifying clad pipe solutions for critical sections. The technology’s combination of structural strength and superior corrosion resistance allows manufacturers to develop specialized products tailored to the rigorous demands of modern water treatment infrastructure, positioning them strategically in this high-value market segment.

Advanced Manufacturing Technology Integration

Technological advancements in clad pipe production are enabling manufacturers to expand market reach through increased cost-efficiency and production capabilities. Innovations such as laser cladding and automated welding systems are reducing manufacturing costs by 15-20% while maintaining stringent quality standards, improving competitiveness against alternative materials.

The adoption of artificial intelligence, machine learning, and digital twin technology in manufacturing processes optimizes bonding parameters, reduces defect rates, and accelerates product development cycles. These technologies enable customization for specialized applications in emerging sectors, such as renewable energy, carbon capture, and hydrogen transportation. Companies embracing Industry 4.0 solutions are gaining significant competitive advantages through improved efficiency, higher yields, and enhanced ability to meet the demands of complex infrastructure projects worldwide.

Category-wise Insights

Manufacturing Process Analysis

Metallurgical bonding leads the clad pipe market with around 55% share, owing to its exceptional mechanical strength and durability in critical applications. This process forms a permanent metallurgical bond between the base pipe and cladding material through techniques such as hot rolling, explosive bonding, and co-extrusion, producing pipes that can withstand extreme pressures and temperatures. The Butting Group has supplied over 130 kilometers of metallurgically bonded pipes for major oil and gas projects, highlighting the technology’s reliability in offshore environments.

This method eliminates delamination risks and supports high-performance alloys such as Inconel 625, Hastelloy C-276, and duplex stainless steels, which resist pitting, stress corrosion, and hydrogen sulfide. Although capital-intensive, metallurgical bonding extends service life by 25-30% over mechanically bonded alternatives, making it a preferred choice for high-stakes industrial applications where long-term integrity is critical.

Thickness Analysis

The 18-36 mm wall thickness segment accounts for roughly 38% of the clad pipe market, offering an optimal balance between strength and material efficiency. This range provides sufficient wall integrity for medium to high-pressure systems while controlling material costs, making it ideal for offshore pipelines and long-distance transport applications. Standard pipe fittings and welding procedures are compatible with this thickness, ensuring seamless integration with existing infrastructure.

Compliance with DNV-ST-F101 pipeline design standards further drives adoption in subsea applications operating at depths up to 2,000 meters. Manufacturing within this thickness range optimizes rolling and bonding processes, achieving consistent metallurgical properties without the need for heavy-duty machinery or extended processing cycles required for thicker alternatives, thereby improving production efficiency and cost-effectiveness.

End-use Analysis

The oil and gas sector dominates the clad pipe market, with an estimated 47% share, driven by the critical requirement for corrosion-resistant solutions in harsh production environments. Offshore exploration and deepwater projects expose pipelines to seawater, hydrogen sulfide, carbon dioxide, and hydrocarbons at high pressures and temperatures, rapidly degrading conventional materials. Major operators, such as Saudi Aramco, Petrobras, and Statoil, have specified clad pipes for key projects where pipeline integrity is crucial for safety and environmental protection.

Clad pipes are essential for subsea production systems handling multiphase flows containing sand, scale inhibitors, and corrosive gases, ensuring structural integrity over 25-30 years. The growing demand for deepwater exploration and the industry’s focus on asset integrity management and total cost of ownership optimization continue to drive the adoption of these advanced materials, despite their higher upfront costs, highlighting their long-term operational and economic benefits.

Regional Insights

North America Clad Pipe Market Trends

North America leads the global clad pipe market due to its mature shale oil production and extensive offshore operations in the Gulf of Mexico. Established regulatory frameworks, including API 5L specifications and ASME B31 pipeline codes, provide clear standards for critical applications. Major operators such as ExxonMobil, Chevron, and ConocoPhillips utilize specialized piping solutions to handle high-pressure, high-temperature conditions and corrosive fluids, particularly in deepwater projects.

Technological leadership in advanced manufacturing enhances market growth, with companies like NobelClad pioneering explosive bonding and DetaPipe technologies for high-performance applications. Innovation hubs around Houston, Oklahoma City, and Calgary drive the development of specialized alloys and manufacturing techniques. Coupled with infrastructure modernization programs targeting aging pipelines, the region maintains sustained demand for corrosion-resistant clad pipes across energy and industrial sectors.

Europe Clad Pipe Market Trends

Europe’s clad pipe market growth is driven by mature North Sea offshore operations and stringent environmental regulations that favor the use of advanced materials. Countries such as Norway, the UK, the Netherlands, and Denmark rely on high-integrity pipelines to protect the environment and ensure operational safety. The EU Green Deal initiatives further promote sustainable infrastructure, making clad pipes attractive due to their extended service life and reduced maintenance needs.

Germany contributes advanced manufacturing capabilities through firms like Butting Group and EEW Group, which lead in metallurgical bonding technologies for global projects. Harmonized EU regulations streamline certification and quality standards, easing market access for specialized products. The focus on circular economy principles also aligns with the benefits of clad pipes, including material efficiency, longevity, and recyclability of alloy components at end-of-life.

Asia Pacific Clad Pipe Market Trends

Asia Pacific is the fastest-growing regional market, projected to expand at a 6.2% CAGR through 2032, driven by extensive infrastructure projects in China, India, and ASEAN nations. China’s offshore oil and gas expansion in the South China Sea and the Belt and Road Initiative create significant demand for high-performance corrosion-resistant piping solutions.

Japan contributes technological leadership through The Japan Steel Works, supplying clad pipes for LNG terminals and petrochemical facilities, with energy security initiatives driving diversified infrastructure investments. India’s expanding refinery and chemical processing sectors, coupled with the Make in India program, encourage domestic manufacturing of critical piping components. Collectively, these developments position the Asia Pacific region as a high-growth market for advanced clad pipe solutions.

Competitive Landscape

The global clad pipe market is moderately consolidated, with established players dominating through technological expertise and advanced manufacturing capabilities. The top companies account for roughly 55-60% of the market, reflecting high barriers to entry and the specialized nature of metallurgical bonding, welding, and quality assurance processes. Market leaders focus on vertical integration, controlling raw material sourcing, production processes, and stringent testing to ensure consistent product performance in critical applications.

Significant investments in research and development drive innovation in automated manufacturing, alloy composition, and welding technologies to enhance efficiency and reduce costs. Emerging business models emphasize lifecycle solutions, including installation support, integrity monitoring, and maintenance services, enabling differentiation beyond traditional product offerings.

Key Market Developments

- In February 2024, Butting Group: Butting Group announced the completion of a €25 million facility expansion in Germany, increasing clad pipe production capacity by 40%. This expansion aims to meet the growing demand from offshore oil and gas projects worldwide, enhancing the company’s ability to deliver high-performance corrosion-resistant piping solutions.

- In July 2024, NobelClad: NobelClad launched its DetaPipe technology, featuring advanced explosive bonding processes for titanium and zirconium cladding applications. The innovation targets chemical processing and marine environments with extreme corrosion challenges, enabling enhanced durability, structural integrity, and reliability in critical pipelines exposed to aggressive fluids and high-pressure subsea conditions.

- In September 2024, EEW Group: EEW Group secured a US$150 million contract to supply clad pipes for Saudi Aramco’s offshore development project. The deal highlights growing demand for specialized, corrosion-resistant materials in Middle Eastern energy infrastructure, reinforcing EEW Group’s position as a key supplier of high-performance piping solutions for critical offshore applications.

Companies Covered in Clad Pipe Market

- Butting Group

- The Japan Steel Works (JSW)

- NobelClad

- Proclad

- Inox Tech

- Gieminox

- Eisenbau Kramer

- Cladtek Holdings

- Tenaris

- Precision Castparts Corporation

- EEW Group

- IODS Pipe Clad

- Canadoil Group

- Gautam Tube Corporation

- Zhejiang Jiuli Group

Frequently Asked Questions

The global clad pipe market is projected to reach US$ 5.5 billion by 2032, growing from US$ 4.2 billion in 2025 at a CAGR of 3.9% during the forecast period.

Market growth is driven by increasing offshore oil and gas exploration activities, infrastructure modernization requirements, and growing demand for corrosion-resistant piping solutions in harsh industrial environments.

Metallurgical bonding leads the market with approximately 55% share due to its superior mechanical properties, permanent bond integrity, and proven performance in critical applications.

Asia Pacific represents the fastest-growing regional market with 6.2% CAGR projected through 2032, driven by infrastructure investments in China, India, and ASEAN countries.

Water treatment and desalination infrastructure presents the most significant opportunity, with US$ 50 billion in Middle Eastern investments and global water scarcity driving demand for specialized piping solutions.

Key market players include Butting Group, The Japan Steel Works (JSW), NobelClad, Tenaris, and EEW Group, with established technological expertise and global manufacturing capabilities.