- Food Ingredients & Additives

- Chitin Market

Chitin Market Size, Share, Trends, Growth, and Regional Forecast, 2026 to 2033

Chitin Market by Product Type (Chitosan, Glucosamine, Others), End-user (Food & Beverages, Agriculture/Agrochemicals, Healthcare/Biomedical, Water Treatment, Cosmetics & Personal Care, Others), and Regional Analysis for 2026 - 2033

Chitin Market Share and Trends Analysis

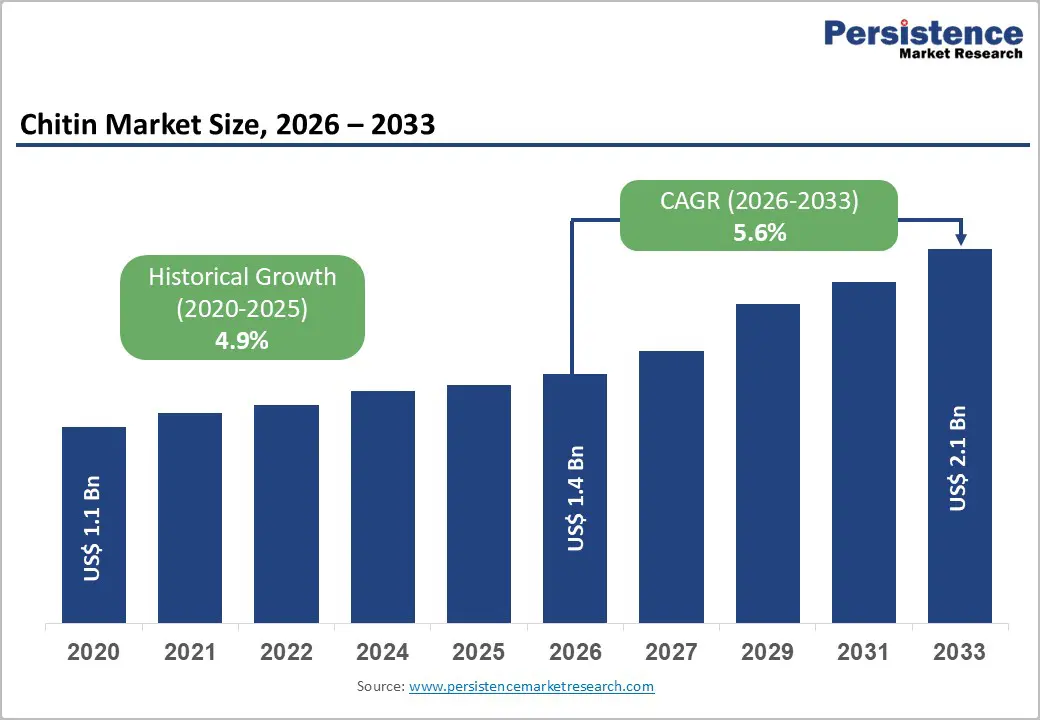

The global chitin market size is expected to be valued at US$ 1.4 billion in 2026 and projected to reach US$ 2.1 billion by 2033, growing at a CAGR of 5.6% between 2026 and 2033.

The global expansion of the market is fundamentally driven by a transition toward sustainable, bio-based polymers as industries seek to reduce reliance on synthetic derivatives. Chitin, a naturally occurring nitrogenous polysaccharide, has gained immense traction due to its abundance in crustacean waste and its inherent biodegradability. Environmental regulations implemented by organizations such as the United States Environmental Protection Agency (EPA) and the European Chemicals Agency (ECHA) have accelerated the adoption of chitosan as a non-toxic flocculant in water treatment. Furthermore, the increasing integration of biocompatible materials in the healthcare and biomedical sectors for advanced wound-healing and drug-delivery systems is establishing a robust, value-added revenue stream for manufacturers.

Key Industry Highlights

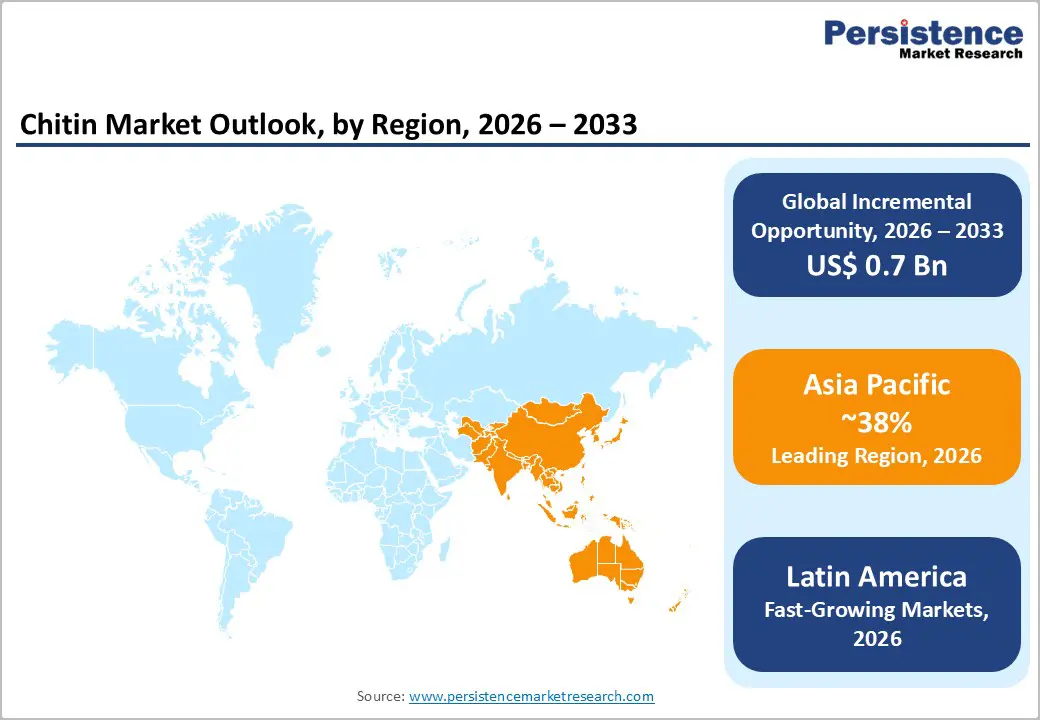

- Leading Region: Asia Pacific, holding around 38% market share, supported by abundant seafood-processing raw materials, large-scale extraction capacity, and strong demand from water treatment, pharmaceuticals, and cosmetics across China, India, and Southeast Asia.

- Fastest-Growing Region: Latin America, driven by the modernization of aquaculture, expanding pharmaceutical usage of glucosamine, and rising adoption of bio-based coagulants in municipal water infrastructure across Brazil and Mexico.

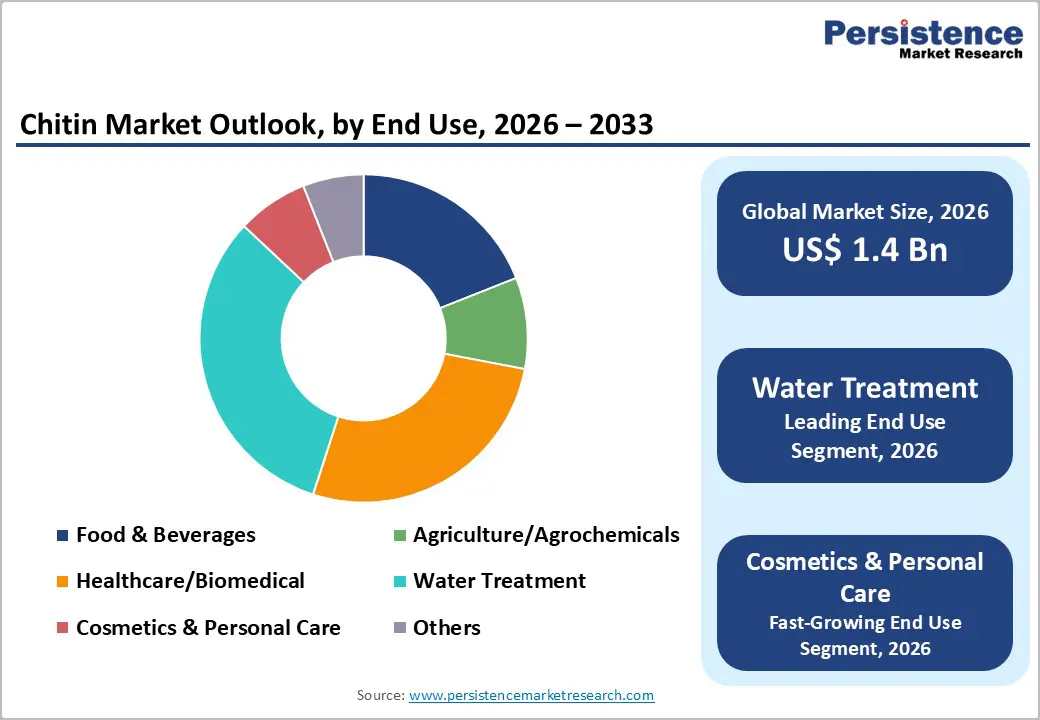

- Dominant End-user: Water Treatment, accounting for approximately 32% share, fueled by high-volume use of chitosan as a non-toxic bio-flocculant for industrial effluents and municipal wastewater compliance.

- Fastest-Growing Application Segment: Cosmetics & Personal Care, propelled by clean beauty trends, rising preference for bio-based film-formers, and demand for antimicrobial, skin-friendly polymers in premium skincare and haircare formulations.

- Growth Indicators: Accelerated integration of chitosan in advanced wound care, drug delivery systems, and regenerative medicine, supported by rising chronic disease incidence and demand for biocompatible, non-allergenic biomaterials.

- Opportunities: Expanding use of chitin-based bioplastics and compostable packaging, leveraging circular bioeconomy models and growing brand willingness to pay premiums for sustainable, high-barrier materials.

| Key Insights | Details |

|---|---|

| Global Chitin Market Size (2026E) | US$ 1.4 Bn |

| Market Value Forecast (2033F) | US$ 2.1 Bn |

| Projected Growth (CAGR 2026 to 2033) | 5.6% |

| Historical Market Growth (CAGR 2020 to 2025) | 4.9% |

Market Dynamics

Driver - Rapid Integration of Biopolymers in Advanced Wound Care and Pharmaceuticals

The secondary growth engine is the burgeoning biomedical sector, in which the biocompatibility and antimicrobial properties of chitosan are highly valued. Medical research journals highlight that chitin derivatives facilitate rapid hemostasis and promote tissue regeneration, making them ideal for surgical dressings and scaffolds. The International Diabetes Federation (IDF) estimates that the prevalence of chronic ulcers is rising, thereby increasing demand for specialized wound care products. Additionally, the pharmaceutical industry is using chitin nanoparticles for controlled drug delivery, as they can cross biological barriers and are non-allergenic. This transition from conventional plastics to therapeutic biopolymers in healthcare is generating high-value revenue pockets for companies like FMC Corporation and KitoZyme S.A., which focus on high-purity medical-grade extracts.

Restraints - Stringent Regulatory Frameworks for Healthcare and Food Grade Applications

The chitin market is subject to rigorous scrutiny regarding its use in consumer products and medical devices. Regulatory bodies such as the U.S. Food and Drug Administration (FDA) and the European Food Safety Authority (EFSA) have established strict labeling requirements regarding allergen risks, as crustacean-derived products can trigger severe allergic reactions. Achieving "Generally Recognized as Safe" (GRAS) status for new food applications is a lengthy and expensive endeavor. This regulatory environment necessitates continuous investment in toxicological testing and safety documentation, which can deter smaller players from entering high-value segments. The lack of standardized international monographs for certain chitosan grades also creates compliance challenges for global exporters, thereby slowing the commercialization of innovative delivery systems in the pharmaceutical and cosmetics sectors.

Opportunity - Expansion of Sustainable Packaging and Bioplastic Solutions

The burgeoning global movement against single-use plastics presents a lucrative opportunity for the development of chitin-based bioplastics. Manufacturers are increasingly seeking biodegradable film-forming materials that provide high mechanical strength and gas barrier properties. Chitin whiskers and fibers can be used to reinforce starch-based polymers, thereby enabling fully compostable packaging that aligns with the United Nations Sustainable Development Goals (SDGs). Research indicates that approximately 20% of global packaging firms are actively seeking alternative materials to replace polyethylene. Companies that successfully implement scalable production of chitin films can capture a significant share of the retail and grocery markets, where "Clean Beauty" and "Sustainable Food" brands are willing to pay a premium for eco-friendly packaging that maintains product shelf life and integrity.

Category-wise Analysis

By End-user Insights

The water treatment segment held the leading position in the chitin market in 2025, accounting for 32% of the market. This dominance is primarily attributed to the spirit of environmental stewardship and the non-toxic nature of chitosan, which acts as a superior bio-flocculant for removing metal ions, dyes, and organic pollutants from industrial effluent. Unlike synthetic polymers like polyacrylamide, chitin-based coagulants do not pose long-term toxicity risks to aquatic life. The justification for its leadership is further supported by the increasing number of municipal wastewater facilities in the Asia-Pacific region that are integrating sustainable purification technologies to comply with new government mandates. While Healthcare/Biomedical applications are high-value, the sheer volume consumption in industrial water purification ensures this segment remains the primary revenue driver for the foreseeable future.

Cosmetics & Personal Care Emerges as the Fastest-Expanding Application Segment

The cosmetics & personal care segment is identified as the fastest-growing application area during the forecast period. This growth is driven by rising consumer demand for "Skin-Positive" and bio-based ingredients that provide moisturizing, anti-aging, and UV-protective properties. Chitosan and its derivatives are increasingly used in high-end hair care and skincare formulations due to their film-forming properties and their ability to deliver active ingredients effectively. Data suggests that the trend toward "Clean Beauty" is prompting manufacturers to replace synthetic silicones with natural polymers. Furthermore, chitosan's antimicrobial efficacy makes it a desirable preservative in organic cosmetics. As disposable incomes rise in the Asia-Pacific and Latin American regions, demand for premium, natural personal care products is expected to surge, driving volume growth in this category.

Region-wise Insights

North America Chitin Market Trends

North America remains a significant hub for innovation, characterized by a highly mature healthcare infrastructure and a robust regulatory environment that favors advanced biotechnological materials. The United States leads the region, with intensifying demand for medical-grade chitosan in the pharmaceutical sector for controlled-release drug systems and orthopedic implants. According to reports from the National Institutes of Health (NIH), the aging population's need for advanced wound care and regenerative medicine is a critical driver for market growth.

The region's innovation ecosystem is also heavily influenced by the trend toward "Organic Agriculture," in which chitin-derived biopesticides are used to enhance crop resilience without chemical runoff. Environmental policies in the U.S. and Canada that promote natural water treatment solutions further stimulate market demand. Strategic partnerships between biotechnology firms and academic institutions are fostering breakthroughs in nano-chitin applications. Furthermore, the presence of major industry players such as FMC Corporation ensures that the region remains at the forefront of high-purity extraction technology, serving the burgeoning "Sustainable Consumer" demographic in urban centers.

Asia Pacific Chitin Market Trends

Asia-Pacific accounted for the largest share of the global chitin market, with 38% in 2025. This dominance is underpinned by the region's status as the global epicenter for seafood production and processing. Nations such as China, India, Vietnam, and Thailand possess abundant supplies of raw materials, providing a significant competitive advantage in production costs. In China, the government's focus on "Green Development" has led to a skyrocketing demand for sustainable industrial chemicals, particularly in the Water Treatment and textile industries.

Growth dynamics in India are characterized by a burgeoning pharmaceutical industry that extensively uses chitosan as an excipient. Japan remains a leader in high-end cosmetic applications, where the traditional use of marine ingredients provides a cultural foundation for market adoption. The region's manufacturing advantage is further bolstered by lower labor costs and large-scale refined processing facilities. Additionally, the growth of the ASEAN aquaculture sector is increasing demand for chitin-based feed additives. As urban centers expand and environmental regulations tighten, the region is expected to maintain its leadership through both high-volume industrial consumption and the export of refined chitin derivatives to Western markets.

Latin America Chitin Market Trends

Latin America is recognized as the fastest-growing regional market, projected to record a high CAGR through 2032. The market dynamics in this region are primarily shaped by the rapid modernization of the agricultural and aquaculture sectors in Brazil and Mexico. As global demand for sustainably produced seafood increases, local producers are adopting chitin-based treatments to enhance the health and immune function of farmed shrimp, thereby reducing reliance on antibiotics.

Regulatory harmonization across the Mercosur trade bloc is facilitating the intra-regional trade of biopolymers, helping manufacturers scale their operations. In Mexico, the pharmaceutical sector is seeing a rise in the use of glucosamine for joint health supplements, reflecting the growing health awareness among the middle class. The region also benefits from a high "manufacturing advantage" due to its extensive coastline and abundant raw material supply from the seafood processing industry. Furthermore, government initiatives to improve municipal water infrastructure are creating steady demand for bio-coagulants, positioning Latin America as a high-potential frontier for both domestic production and international export.

Competitive Landscape

The chitin market is characterized by a moderate level of concentration, with a small number of large-scale industrial players and a growing number of specialized niche innovators. Dominant global firms such as Golden-Shell Pharmaceutical Co., Ltd. and FMC Corporation control a significant portion of the primary supply chain, leveraging their extensive vertically integrated processing facilities. These market leaders maintain their dominance through robust R&D in filtration technologies and strategic vertical integration to secure raw material sources. Key differentiators employed by leaders include the achievement of medical-grade certifications and the development of proprietary "Animal-Free" extraction methods. Emerging business model trends show a pivot toward "Circular Bioeconomy" partnerships, where seafood processors and chemical firms collaborate to maximize waste valorization. Competitive intensity is expected to rise as more firms enter the sustainable packaging segment, pushing manufacturers to innovate in product functionality and cost-efficiency.

Key Developments:

- In February 2025, Nordic Seafarm and FutureLab & Partners formed a joint venture, Manatee Biomaterials, to develop sustainable biomaterials derived from seaweed, strengthening innovation in marine-based, renewable material solutions.

Companies Covered in Chitin Market

- FMC Corporation

- Golden-Shell Pharmaceutical Co., Ltd.

- G.T.C. Bio Corporation

- Kunpoong Bio Co., Ltd.

- Panvo Organics Pvt. Ltd.

- KitoZyme S.A.

- Primex Ehf

- Bio21 Co., Ltd.

- Heppe Medical Chitosan GmbH

- Advanced Biopolymers AS

- Others

Frequently Asked Questions

The global chitin market is expected to reach a valuation of approximately US$ 1.4 billion in 2026, following a period of steady growth as industrial demand for bio-based materials intensifies.

The primary driver is the rising global need for eco-friendly water treatment solutions and the increasing integration of biocompatible materials in the advanced healthcare and pharmaceutical sectors.

The global Chitin market is poised to witness a CAGR of 5.6% between 2026 and 2033.

Significant growth potential lies in the expansion of sustainable packaging solutions and the development of plant-based fungal chitin to cater to the burgeoning vegan consumer segment.

Key market participants include global leaders such as FMC Corporation, Golden-Shell Pharmaceutical, G.T.C. Bio Corporation, and high-purity specialists like KitoZyme S.A. and Heppe Medical Chitosan.