- Biotechnology

- Cell-based Assays Market

Cell-based Assays Market Size, Share, and Growth Forecast, 2025 - 2032

Cell-based Assays Market By Products and Services (Reagents, Assay Kits, Microplates), Application (Basic Research, Drug Discovery), End-user (Pharmaceutical and Biotechnology Companies), and Regional Analysis for 2025 - 2032

Cell-based Assays Market Size and Trends Analysis

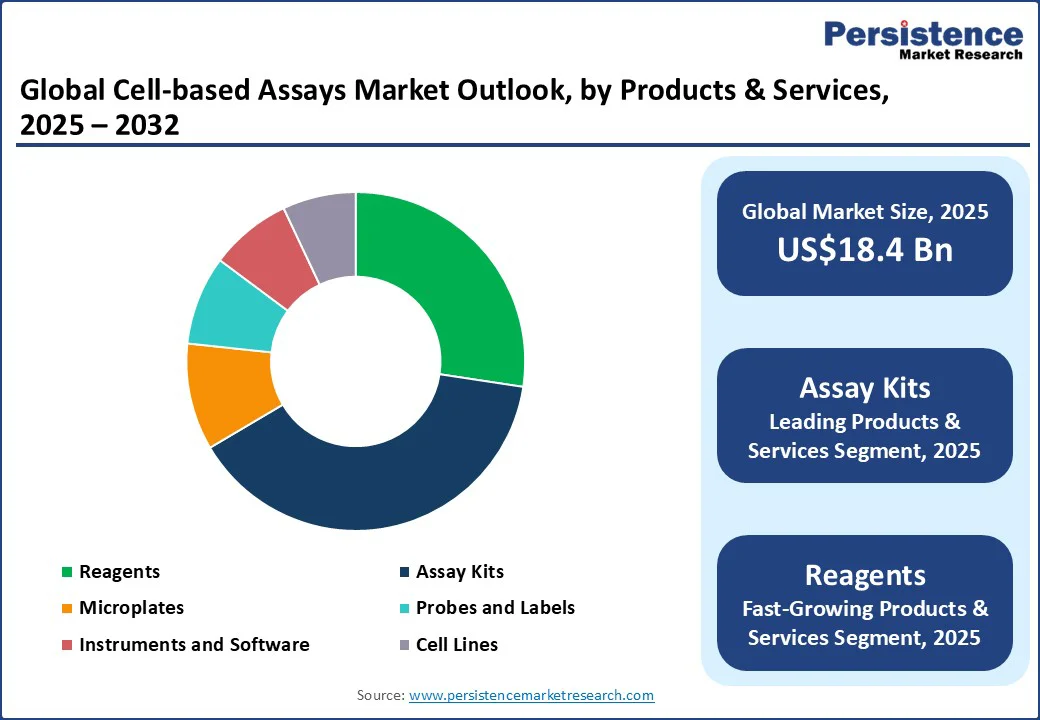

The global cell-based assays market size is likely to be valued at US$ 18.4 Bn in 2025 and is estimated to reach US$ 33.3 Bn in 2032, growing at a CAGR of 8.9% during the forecast period 2025 - 2032, driven by the rising prevalence of complex diseases, regulatory encouragement for human-relevant models, and surging demand for reproducible workflows.

Key Industry Highlights:

- Leading Products and Services: Assay kits hold nearly a 39.1% share in 2025, as ready-to-use formats reduce development time and ensure reproducibility across labs.

- Dominant Application: Drug discovery holds approximately 41.8% of the cell-based assays market share in 2025, since cell-based assays provide human-relevant models that accelerate target validation.

- Recent Collaboration: In June 2025, Axxam S.p.A. joined hands with Molecular Health GmbH to boost the identification and validation of novel therapeutic targets across a wide range of therapeutic areas. Both companies aim to deliver precise and clinically driven disease-to-target and target-to-lead solutions to the pharmaceutical and biotechnology industry.

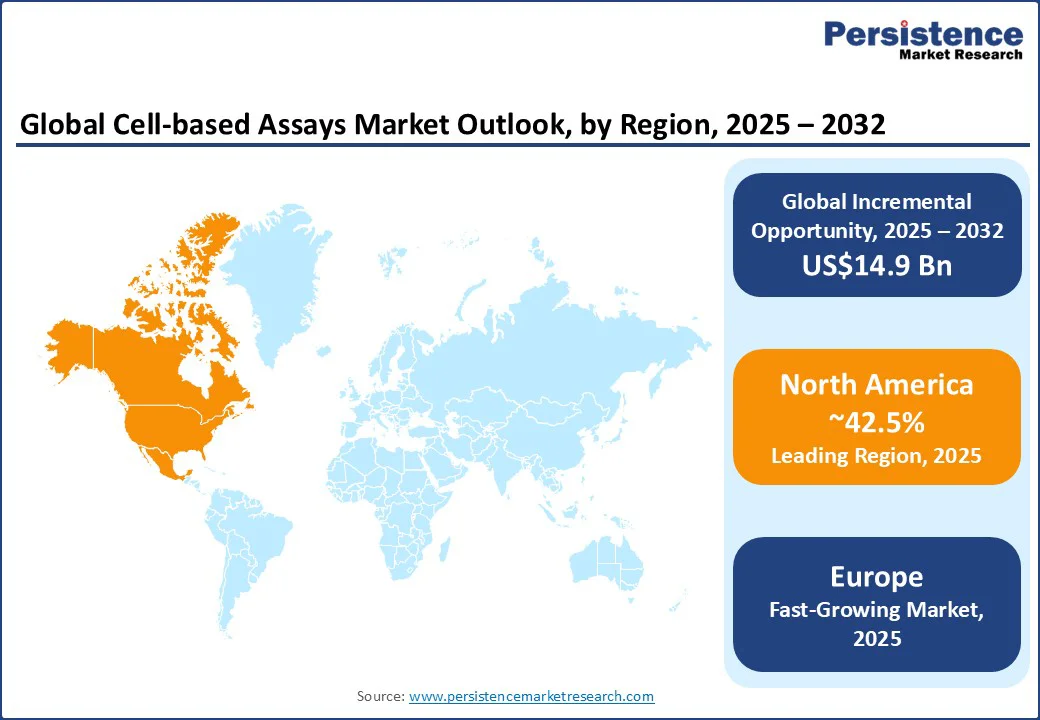

- Leading Region: North America with around 42.5% share in 2025, owing to regulatory support for New Approach Methodologies and early adoption of AI-based imaging platforms.

- Fastest-growing Region: Europe, accelerated by academic-industry collaborations and integration of predictive in vitro models into preclinical workflows.

| Global Market Attribute | Key Insights |

|---|---|

| Cell-based Assays Market Size (2025E) | US$18.4 Bn |

| Market Value Forecast (2032F) | US$33.3 Bn |

| Projected Growth (CAGR 2025 to 2032) | 8.9% |

| Historical Market Growth (CAGR 2019 to 2024) | 7.7% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Rise in Complex Diseases Increase Reliance on Human-relevant Cell-based Assays

The rising prevalence of complex diseases is driving demand for cell-based assays, as traditional 2D culture systems and animal models often fail to replicate human-relevant biology. Cancer research, for instance, mainly relies on patient-derived organoids and 3D spheroid assays to study tumor heterogeneity and drug response. Infectious diseases, primarily emerging viral pathogens, are another factor fueling demand.

The COVID-19 pandemic highlighted the requirement for rapid, human-relevant screening platforms. By 2024, several laboratories in Singapore and Japan were using iPSC-derived lung epithelial cell assays to study SARS-CoV-2 variants.

These assays enabled quick evaluation of antiviral candidates without relying solely on animal models. Similarly, dengue and chikungunya research in Thailand is embracing human endothelial and immune cell co-culture assays to study virus-host interactions in a controlled environment.

Extended Organoid and Co-culture Maturation Raises Operational Costs

Lengthy culture processes hamper the adoption of cell-based assays, as various new models, including 3D organoids and co-culture systems, require weeks to months to reach functional maturity.

For example, in 2024, a study published in the National Institutes of Health (NIH) revealed that generating liver organoids for drug metabolism studies could take up to six weeks, delaying timelines for high-throughput screening. Such extended preparation not only slows the pace of discovery but also increases costs for laboratories that maintain specialized incubators, monitoring systems, and media over long periods.

Inherent biological variability also hampers adoption, as small differences in cell sources, culture conditions, or differentiation protocols can produce widely divergent results.

In addition, patient-derived models worsen this challenge as genetic and epigenetic differences between donors introduce variability that is difficult to standardize. For instance, tumor organoids used in oncology research often display heterogeneous drug responses due to intrinsic genetic differences between patient samples.

Automation and Miniaturization Expand Throughput and Reproducibility

Increased automation and miniaturization are creating new opportunities in cell-based assays. These are allowing complex experiments to be run extensively while reducing manual variability and resource consumption.

High-throughput robotic systems now enable hundreds of parallel experiments with consistent timing and handling. It was previously infeasible for labor-intensive 3D or organoid models. Miniaturization is further reducing reagent costs and enabling studies that would otherwise be prohibitive.

By shrinking assay volumes to micro- or nanoscale, companies tend to perform multiplexed readouts in single wells or chips. For example, Revvity’s 2025 microplate-compatible phospho-protein assays allow simultaneous monitoring of multiple signaling pathways in a single miniaturized setup.

These help in cutting reagent use and experimental costs. This opens the door for small biotech firms and academic labs to access high-content and human-relevant models that were previously limited to large companies.

Category-wise Analysis

Products and Services Insights

Based on products and services, the market is divided into reagents, assay kits, microplates, probes and labels, instruments and software, and cell lines. Among these, assay kits are anticipated to account for nearly 39.1% of the market share in 2025, as they collapse long development timelines into plug-and-play workflows.

It is valuable in cell-based studies, where assay design tends to be technically demanding. Another driver is their popularity due to high reproducibility across various sites and experiments. Global pharma teams often run discovery campaigns across facilities in different countries. Assay kits ensure uniform performance no matter where the study is conducted.

Reagents are gaining impetus as they have become the backbone of assay customization and sensitivity in an era where labs are moving toward complex cell models. These provide researchers with the flexibility to tweak conditions for specific cell types, co-cultures, or 3D organoids.

Their compatibility with novel detection systems is also augmenting the segment. The shift toward high-content imaging and AI-based analysis has increased the demand for bright, stable, and multiplexed reagents.

Application Insights

In terms of application, the market is trifurcated into basic research, drug discovery, and others. Out of these, drug discovery is predicted to hold around 41.8% of the market share in 2025, since cell-based assays now act as the closest in vitro proxy to human biology.

These provide pharmaceutical companies with fast and predictive insights before committing to costly animal or clinical studies. This trend highlights a broad move toward front-loading translational fidelity into the discovery stage, minimizing the late-stage attrition. Cell-based assays also help replicate complex processes such as receptor internalization, metabolic activity, or immune checkpoint signaling.

Basic research is a key application for cell-based assays as they deliver a controlled, yet dynamic environment to study fundamental biological processes that cannot be easily dissected in vivo.

Another reason basic research relies heavily on cell-based assays is their ability to model developmental biology and disease progression at the cellular level. The flexibility of reagents and assay design also makes them indispensable for answering ‘what if’ questions in academic laboratories.

Regional Insights

North America Cell-based Assays Market Trends - Regulatory Support for New Approach Methodologies Spurs Growth

In 2025, North America will likely account for approximately 42.5% of the market share due to regulatory changes, specifically the U.S. Food and Drug Administration’s (FDA) support for New Approach Methodologies (NAMs). A defining moment came when Emulate’s Liver-Chip was accepted into the FDA’s ISTAND pilot program in late 2024.

It created a precedent for organ-on-chip data to be considered in regulatory submissions for drug-induced liver injury. This shift means pharmaceutical and biotech companies are now viewing cell-based assays as tools capable of generating evidence that regulators might accept.

The U.S. cell-based assays market is moving away from simple endpoint assays toward integrated platforms designed for 3D biology and long-term live-cell analysis. Another notable development is the central role of CROs and service providers in mainstreaming novel assays.

Small biotechnology companies often lack the infrastructure for organoid or organ-on-chip studies. Hence, they rely heavily on CRO partnerships. At the laboratory level, research teams are moving toward multiplexed, label-free, and AI-supported readouts instead of traditional fluorescent endpoint assays.

Europe Cell-based Assays Market Trends - ECHA Encourages Validated Cell-based Assays for Toxicology

In Europe, the market is being propelled by regulatory reforms and the continent’s push toward animal testing alternatives. The EU’s updated chemicals strategy under REACH and its ongoing commitment to the 3Rs (Replacement, Reduction, Refinement) have accelerated the demand for novel cell-based systems as validated substitutes for animal models.

A recent example is the European Chemicals Agency (ECHA) encouraging the adoption of in vitro assays and organ-on-chip systems for toxicology assessments. It is evident in the cosmetics and chemicals segments, where animal testing bans are strict.

Pharmaceutical and biotech hubs across Germany, Switzerland, and the U.K. are investing heavily in 3D cell culture and organoid-based assays.

For instance, AstraZeneca’s Cambridge-based research unit has been running collaborations with organoid specialists to integrate 3D human-derived assays into its pre-clinical pipeline. It is aiming for better translational outcomes. Academic-industry consortia play a key role in Europe, often serving as incubators for validation and standardization.

Asia Pacific Cell-based Assays Market Trends - Japan Focuses on Regenerative Medicine and Stem Cell-derived Models

In Asia Pacific, cell-based assays are being augmented by government-backed biotech expansion and the ongoing integration of AI-enabled imaging in research hubs.

China’s 14th Five-Year Plan emphasizes new drug development and alternatives to toxicology testing. It has pushed local CROs and biotech firms to adopt cell-based systems. Local start-ups are providing human-induced Pluripotent Stem Cell (iPSC)-derived cardiomyocyte assays for cardiac safety, catering to global pharma outsourcing into Shanghai and Suzhou.

Japan’s scenario is distinct due to its tight link between regenerative medicine and cell-based assays. Domestic players are investing in stem cell-derived models, reflecting the country’s leadership in iPSC technology. India is emerging as a service hub in the market, backed by cost advantages and increasing collaborations with pharmaceutical companies in the West. In Australia, the market is growing due to translational research in oncology and infectious diseases.

Competitive Landscape

The global cell-based assays market is constantly evolving, with companies differentiating themselves through platform developments, assay chemistries, and novel biological models. Instrument providers are upgrading traditional imaging systems into live-cell and 3D-ready ecosystems.

Agilent’s BioTek Cytation C10, showcased at Analytica 2024, was upgraded with spinning-disk confocal and water-immersion optics, specifically targeting thick 3D tissue models and spheroids. A new wave of competition is emerging around organ-on-chip platforms and advanced 3D models, which are beginning to transform the definition of cell-based assays.

Key Industry Developments

- In May 2025, AstraZeneca announced its acquisition of biotechnology company EsoBiotec for up to US$1 Bn. This move aims to improve AstraZeneca's cell therapy capabilities, specifically in cancer and autoimmune diseases.

- In April 2024, Bio-Rad Laboratories, Inc., collaborated with Oncocyte Corporation to develop and commercialize transplant monitoring products using Bio-Rad’s Droplet Digital PCR instruments and reagents. Bio-Rad secured exclusive commercial rights in certain markets to commercialize Oncocyte’s assay for transplant monitoring research.

Companies Covered in Cell-based Assays Market

- Bio-Rad Laboratories, Inc.

- Merck KGaA

- Corning Incorporated

- Becton, Dickinson and Company (BD)

- Charles River Laboratories

- Lonza Group AG

- F. Hoffmann-La Roche Ltd. (Roche Holdings AG)

- Danaher Corporation

- Perkin Elmer Inc.

- Thermo Fisher Scientific Inc.

- Promega Corporation

Frequently Asked Questions

The cell-based assays market is projected to reach US$18.4 Bn in 2025.

The rising prevalence of complex diseases and the regulatory push for human-relevant models are the key market drivers.

The cell-based assays market is poised to witness a CAGR of 8.9% from 2025 to 2032.

Integration of organ-on-chip platforms and expansion of patient-derived iPSC models are the key market opportunities.

Bio-Rad Laboratories, Inc., Merck KGaA, and Corning Incorporated are a few key market players.