- Specialty & Fine Chemicals

- Calcite Market

Calcite Market Size, Trends, Share, and Growth Forecast 2025 - 2032

Calcite Market by Form (Powder, Crystalline), Application (Paper & Pulp, Polymer & Plastic, Paints & Coatings, Cement & Concrete, Other), and Regional Analysis 2025 - 2032

Calcite Market Share and Trends Analysis

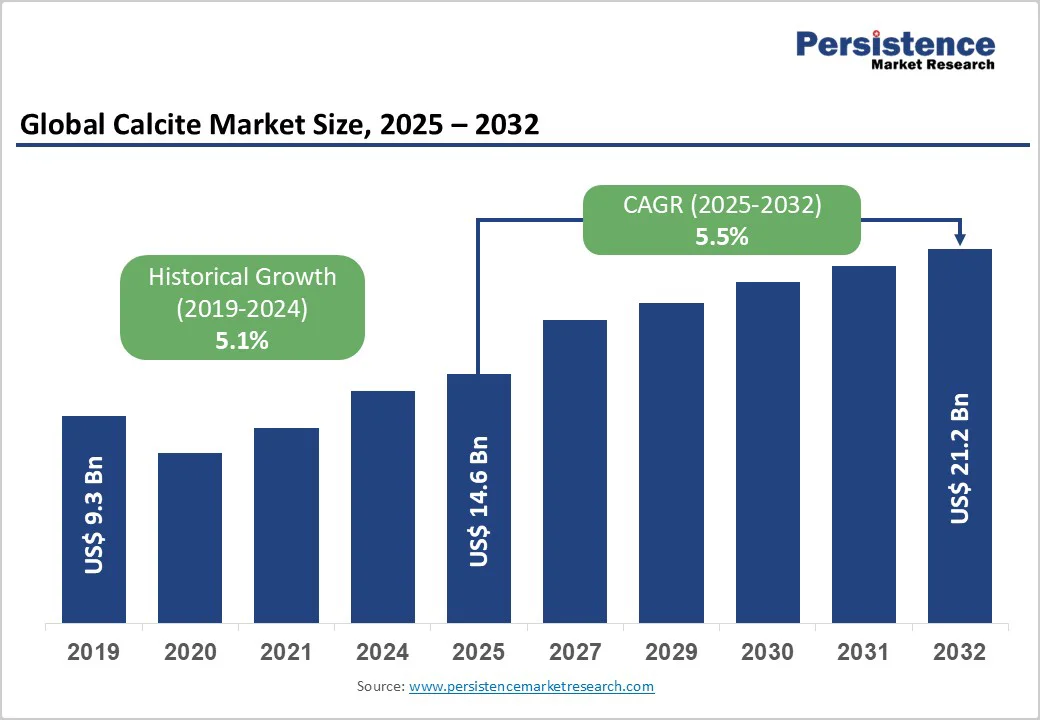

The global calcite market size is likely to be valued at US$14.6 billion in 2025 and is projected to reach US$21.2 billion by 2032, growing at a CAGR of 5.5% between 2025 and 2032.

This robust growth trajectory reflects calcite's essential role as a versatile industrial mineral across diverse applications. The market expansion is driven by rising demand from construction activities, paper manufacturing, and the growing adoption of calcium carbonate as an eco-friendly filler material in polymer and plastic applications.

Key Market Highlights:

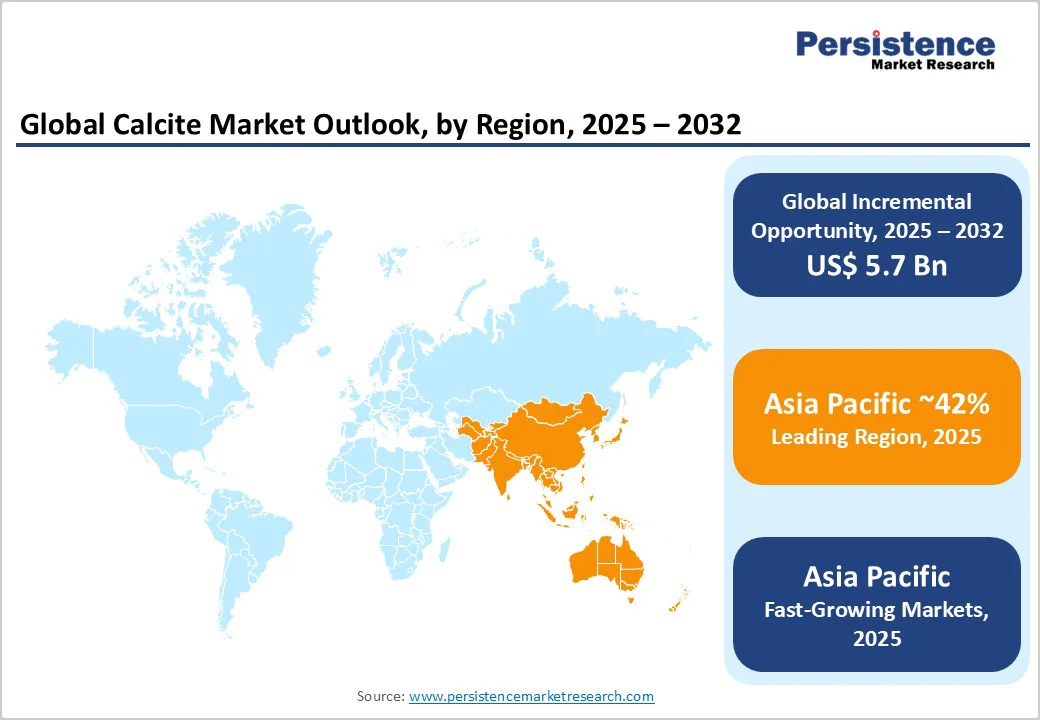

- Leading Region: Asia Pacific dominates global calcite consumption with over 35% market share, driven by rapid industrialization in China and India across construction and manufacturing sectors.

- Fastest-Growing Region: Asia Pacific is the fastest-growing regional market, driven by accelerating demand from infrastructure development, paper manufacturing, and polymer applications in emerging economies.

- Leading Form Segment: Powder form maintains market leadership with 62% segment share, driven by superior processing characteristics, versatility, and cost-effectiveness for industrial applications.

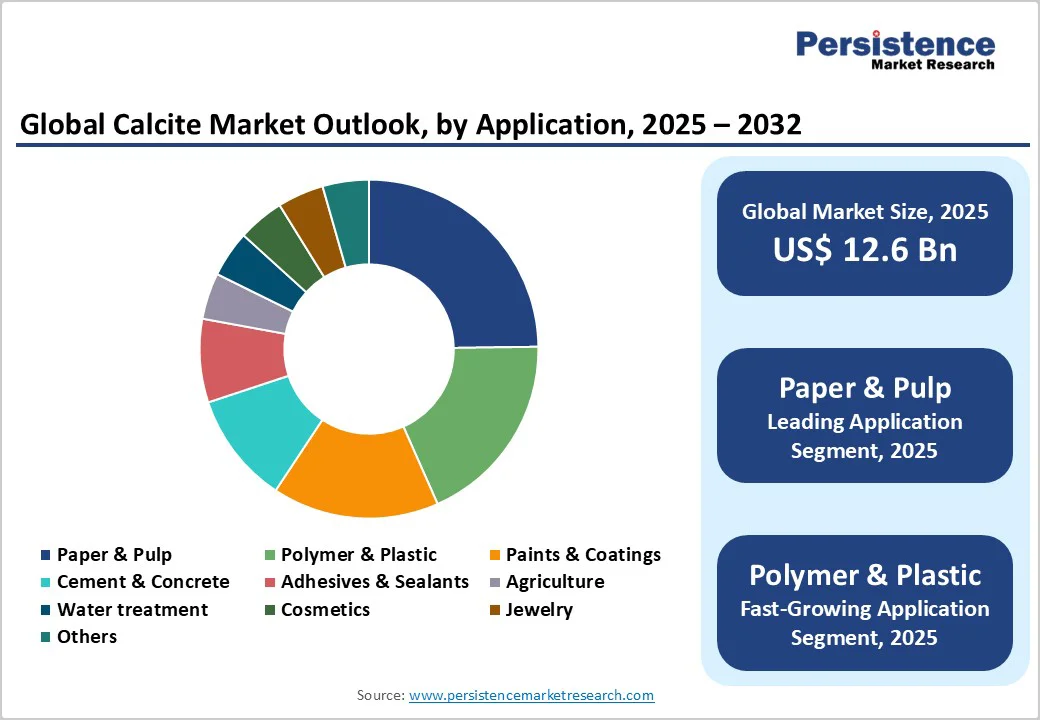

- Leading Application Segment: Paper & Pulp applications hold a dominant 28% market share, driven by the essential calcium carbonate requirements of modern alkaline papermaking processes.

- Key Market Opportunity: Sustainable material applications offer significant growth potential as manufacturers seek eco-friendly alternatives and consumers demand environmentally conscious product formulations.

| Key Insights | Details |

|---|---|

| Calcite Market Size (2025E) | US$14.6 billion |

| Market Value Forecast (2032F) | US$21.2 billion |

| Projected Growth CAGR (2025 - 2032) | 5.5% |

| Historical Market Growth (2019 - 2024) | 5.1% |

Market Dynamics

Driver - Expanding Paper and Pulp Industry Applications

The paper and pulp industry remains a pivotal growth driver for the calcite market, as calcium carbonate serves as a crucial filler and coating agent in paper manufacturing. Calcite enhances brightness, opacity, and print quality while reducing production costs by replacing costly wood pulp fibers. Its widespread use results from the compound’s ability to improve paper smoothness and reduce ink absorption, thereby optimizing printing efficiency.

The industry’s transition from acid-based to neutral and alkaline papermaking processes has further strengthened the adoption of calcite. The ongoing “digitalization paradox”, where demand for packaging, hygiene products, and specialty papers continues despite the decline in newsprint, sustains the need for calcite-based fillers. This steady demand underpins the mineral’s vital role in modern papermaking and ensures its long-term importance across global pulp and paper operations.

Rising Construction and Infrastructure Development

Continuous expansion of the global construction sector significantly fuels calcite market growth, particularly through cement, concrete, and composite building materials. Ground Calcium Carbonate (GCC) is an essential additive that enhances mechanical strength, durability, and finish quality while serving as a cost-effective alternative to traditional raw materials. The mineral’s role in improving material performance has made it indispensable in infrastructure and residential development projects.

Recent data highlights rising infrastructure investments across major economies. In March 2025, U.S. construction activities reached an annualized rate of US$2,196.1 billion, marking a 2.8% year-on-year increase. Similarly, India allocated nearly US$208 billion to infrastructure in FY 2023 - 2024, representing 5.87% of its GDP. These developments reflect robust construction momentum, directly translating into heightened demand for calcite in cement, coatings, and concrete formulations.

Restraints - Competition from Synthetic Alternatives

The calcite market is increasingly challenged by the growing preference for synthetic substitutes such as Precipitated Calcium Carbonate (PCC) and other engineered mineral fillers. These alternatives offer highly controlled particle size, purity, and surface modification options, allowing manufacturers to achieve superior consistency and performance. Industries such as plastics, coatings, and pharmaceuticals often prioritize these characteristics to meet stringent product specifications that natural calcite may not always fulfill.

As a result, natural calcite struggles to maintain its position in high-performance and specialty applications where precision and uniformity are critical. The shift toward synthetic minerals reflects a broader industry trend favoring materials that offer predictable results and customizable properties, thereby constraining calcite’s growth potential in premium market segments.

Raw Material Availability and Mining Regulatory Constraints

Calcite extraction is increasingly impacted by tightening mining regulations and sustainability mandates across major producing regions. Environmental policies and permitting requirements have increased operational costs and restricted access to high-quality limestone reserves, limiting a consistent supply of raw material. These regulatory hurdles add complexity to the production process, particularly for small and medium-scale miners.

The high transportation costs associated with bulk mineral products affect competitiveness, especially in export-oriented operations. When coupled with fluctuating energy prices and logistical challenges, these constraints create cost pressures that influence supplier selection and regional availability. Consequently, mining regulations and raw material constraints remain key barriers to the stable expansion of the calcite market worldwide.

Opportunity - Growth in Sustainable and Eco-Friendly Material Applications

The global shift toward sustainability and eco-conscious production offers substantial opportunities for the calcite market. As industries prioritize reducing environmental footprints, calcite’s natural composition, biodegradability, and lower carbon impact make it an attractive alternative to synthetic fillers. Manufacturers are increasingly incorporating calcite into biodegradable packaging, sustainable plastics, and environmentally friendly coatings to align with corporate green goals and consumer expectations for eco-certified materials.

Technological advancements in nanocalcite production are enhancing its functionality in advanced applications, such as high-performance composites and specialty coatings, while preserving its natural advantages. The rising demand for natural calcium sources in the health and nutrition sectors further broadens market prospects, as nutraceutical and pharmaceutical manufacturers explore calcite for use in calcium supplements and dietary products aimed at health-conscious consumers worldwide.

Expanding Asia Pacific Manufacturing and Infrastructure Development

The Asia Pacific region represents a major growth hub for the calcite market, supported by rapid industrialization, urbanization, and infrastructure expansion. China continues to dominate global calcite production and consumption, driven by extensive construction and manufacturing activities. Simultaneously, India’s growing industrial base and rising middle-class consumption have created strong demand across cement, plastics, paints, and paper sectors, offering long-term opportunities for calcite suppliers.

Increasing infrastructure investments by regional governments and the private sector are bolstering demand for calcite-based materials in construction, coatings, and industrial applications. While North America and Europe show stable demand, the Asia Pacific markets remain dynamic, benefiting from manufacturing capacity expansion and favorable economic growth. The parallel growth of the regional lime industry also reinforces calcite consumption, particularly in construction and industrial end-use segments.

Category-wise Analysis

Form Insights

The powder form dominates the global calcite market, commanding approximately 62% market share due to its superior processing characteristics and widespread industrial applicability.

Powdered calcite offers exceptional versatility for manufacturers, enabling easy incorporation into various formulations while providing consistent particle size distribution and surface area properties critical for performance optimization. The powder form's advantages include enhanced mixing capabilities, uniform dispersion in liquid systems, and compatibility with automated processing equipment used across paper, plastic, and coating applications.

Industrial preference for powder calcite stems from its cost-effectiveness in bulk applications, reduced transportation volumes compared to crystalline forms, and ability to achieve desired product specifications through controlled grinding and classification processes. The segment benefits from established supply chains, standardized quality parameters, and technical support services that facilitate adoption across diverse end-use industries.

Application Insights

Paper & Pulp applications represent the largest segment in the calcite market, accounting for approximately 28% market share, driven by calcium carbonate's essential role as a filler and coating material in modern papermaking processes.

This segment's dominance reflects calcite's unique ability to enhance paper brightness, opacity, and printability while reducing production costs through wood fiber substitution. The transition to alkaline papermaking processes has solidified calcium carbonate's position as the preferred mineral filler, with most global paper manufacturers incorporating calcite in their production formulations.

Industry data indicates that calcium carbonate serves multiple functions in paper production, including pH adjustment, retention aid, calendering agent, and coating additive, making it indispensable for achieving desired paper quality standards. The segment benefits from ongoing demand for packaging materials, hygiene products, and specialty papers that require high-performance mineral additives for optimal functionality.

Regional Insights

North America Calcite Trends

North America maintains a significant market position characterized by advanced processing capabilities and stringent quality standards that drive demand for premium-grade calcite products.

The region's emphasis on regulatory compliance and environmental safety has positioned calcite favorably compared to alternative mineral fillers in critical applications. United States manufacturing facilities demonstrate strong demand across the construction, plastics, and paper industries, with established supply chains that support consistent product availability and technical service capabilities.

The region's mature U.S. Calcium Carbonate Market reflects sophisticated end-user requirements and specialized applications that command premium pricing for high-purity calcite grades.

Recent investments by major industry players, including Imerys' capacity expansion initiatives in North America, demonstrate continued confidence in regional market growth prospects. The North American market benefits from proximity to high-quality limestone deposits, advanced processing infrastructure, and established relationships between suppliers and key industrial customers across diverse application sectors.

Europe Calcite Trends

European markets demonstrate steady growth driven by stringent environmental regulations and increasing adoption of sustainable material solutions across industrial applications.

The region's regulatory framework, particularly EU directives on chemical safety and environmental protection, has created favorable conditions for natural mineral products like calcite. Key markets, including Germany, France, and the United Kingdom, show strong adoption across paper, plastics, and construction applications where regulatory compliance and product safety are paramount concerns.

European Chemical Agency (ECHA) classifications and REACH regulations have facilitated market standardization while encouraging the adoption of environmentally friendly mineral alternatives to synthetic materials.

The region's emphasis on circular economy principles and waste reduction initiatives positions calcite advantageously for industries seeking sustainable material solutions. Ongoing investments in renewable energy infrastructure and industrial modernization programs across Europe continue to drive specialized calcite demand, particularly in high-performance applications requiring consistent quality and regulatory compliance.

Asia Pacific Calcite Trends

Asia Pacific is the fastest-growing region for calcite consumption, with China and India leading market expansion driven by rapid industrialization and infrastructure development.

The region accounts for over 35% of the global calcite market share, reflecting substantial manufacturing capacity and growing domestic consumption across multiple end-use sectors. China's position as both the largest producer and consumer of calcite demonstrates the country's integrated supply chain capabilities and extensive industrial mineral processing infrastructure.

India's expanding manufacturing sector, construction activities, and growing middle-class population drive increased calcite demand across paper, plastics, and construction applications.

The Asia Pacific region benefits from cost-competitive production, abundant raw material resources, and government support for infrastructure development projects that require substantial mineral inputs. Regional growth dynamics are supported by increasing foreign investment, technology transfer initiatives, and expanding export capabilities, positioning the Asia Pacific as a global calcite production hub serving both domestic and international markets.

Competitive Landscape

The global calcite market is moderately consolidated, with manufacturers adopting vertical integration strategies encompassing mining, processing, and distribution to strengthen control over the value chain. These producers prioritize capacity expansion and geographic diversification to meet rising demand across construction, paper, plastics, and coatings sectors while ensuring consistent product supply and quality.

Manufacturers also focus on innovation, customer service, and tailored technical support to differentiate themselves in a competitive environment. Strategic collaborations, mergers, and partnerships are increasingly common, allowing producers to enhance operational efficiency, access emerging markets, and develop advanced formulations that cater to evolving industrial and environmental requirements.

Key Market Developments

- In May 2023, Omya AG announced the construction of seven calcium carbonate plants in China and Indonesia with a combined capacity of approximately 1 million tons per year, scheduled for commissioning in 2023-2024.

- In September 2022, Huber Engineered Materials completed the acquisition of Natural Soda LLC, expanding its specialty minerals platform and diversifying its product portfolio beyond traditional calcium carbonate applications.

- In April 2022, Imerys S.A. initiated the expansion of calcium carbonate manufacturing capacity in North America, nearly doubling current production capability to meet growing regional demand.

Companies Covered in Calcite Market

- Imerys S.A.

- Omya AG

- Minerals Technologies Inc.

- Huber Engineered Materials

- Gulshan Polyols LTD.

- Nordkalk Corporation

- Wolkem India LTD.

- Sibelco

- Esen Mikronize Maden

- Mississippi Lime Company

- Carmeuse

- Jay Minerals

- US Aggregates

- Columbia River Carbonates

- Golden Lime Public Company Limited

Frequently Asked Questions

The global calcite market was valued at US$ 14.6 billion in 2025 and is projected to reach US$ 21.2 billion by 2032, growing at a CAGR of 5.5% during the forecast period.

Market growth is primarily driven by expanding paper and pulp industry applications where calcite serves as essential filler and coating material, and rising construction and infrastructure development requiring calcium carbonate in cement and building materials.

The powder form dominates the market with approximately 62% market share due to superior processing characteristics, widespread industrial applicability, and cost-effectiveness for bulk applications.

Asia Pacific leads the global market with over 35% market share, driven by rapid industrialization in China and India, expanding manufacturing activities, and substantial infrastructure development investments.

Significant opportunities include growth in sustainable and eco-friendly material applications as manufacturers seek natural alternatives, and expanding Asia Pacific manufacturing and infrastructure development creating substantial demand across multiple end-use industries.

Major market players include Imerys S.A., Omya AG, Minerals Technologies Inc., Huber Engineered Materials, Gulshan Polyols LTD., and Nordkalk Corporation among others.