- Specialty & Fine Chemicals

- Bulletproof Vests Market

Bulletproof Vests Market Size, Share, and Growth Forecast 2026 - 2033

Bulletproof Vests Market by Product Type (Soft, Hard), Protection Level (Level II, Level IIIA, Level III, Level IV), End-user (Military & Defense, Law Enforcement & Security, Civilians), and Regional Analysis, 2026–2033

Bulletproof Vests Market Size and Trend Analysis

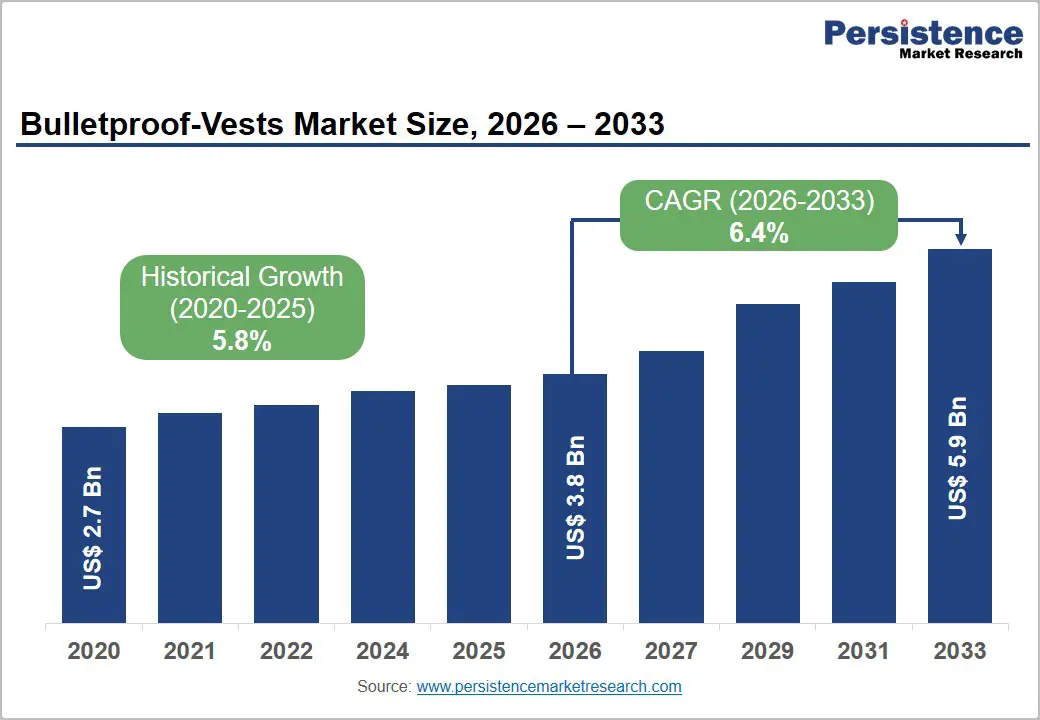

The global bulletproof vests market size is expected to be valued at US$ 3.8 billion in 2026 and projected to reach US$ 5.9 billion, growing at a CAGR of 6.4% between 2026 and 2033. This sustained growth is driven by the rise in geopolitical tensions, defense budget allocations globally, and growing law enforcement procurement programs for enhanced personal protection equipment. According to NATO defense expenditure data, member states collectively spent over US$ 1.2 trillion on defense in 2023, with personal protective equipment representing a significant and growing procurement category. Simultaneously, increasing urbanization-related crime rates and the expansion of private security industries across the Asia Pacific and Latin America are broadening the addressable market beyond traditional military procurement channels.

Key Industry Highlights:

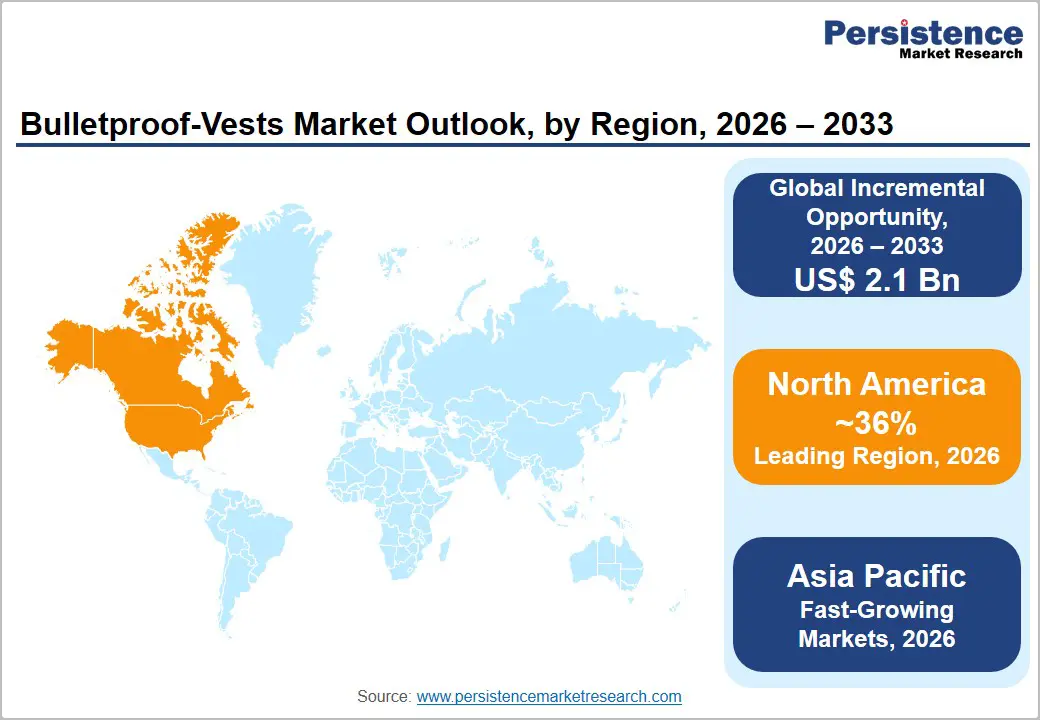

- Leading Region: North America leads the global bulletproof vests market with 36% market share in 2026, anchored by large U.S. DoD military body armor procurement contracts, 800,000+ law enforcement officers on NIJ-certified 5-year replacement cycles, and federal Byrne JAG grant-funded police procurement programs.

- Fastest Growing Region: Asia Pacific is projected to register the high CAGR, driven by China’s PLA modernization, India’s Make in India defense procurement (MKU Limited), and rapidly increasing defense budget allocations across South Korea, Japan, and ASEAN member states.

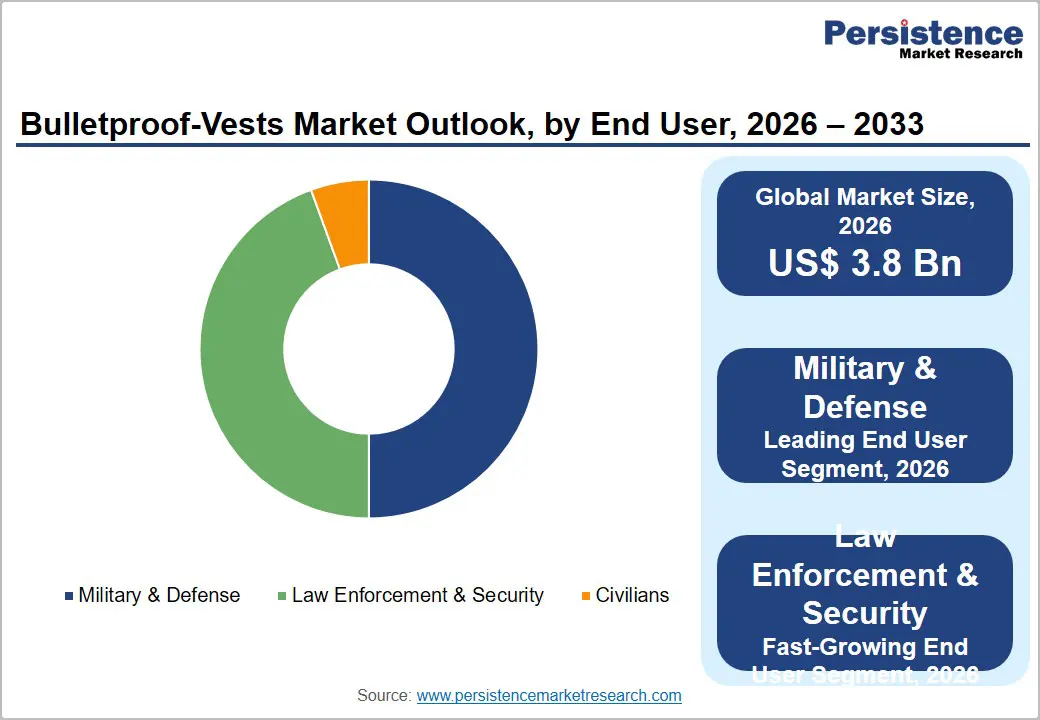

- Dominant Segment: Military & defense commands approximately 45% share in 2026, driven by mandatory personal protective equipment issuance protocols in NATO member states, U.S. DoD SPS programs serving 450,000+ active-duty soldiers, and large-scale military modernization contracts in Asia Pacific and the Middle East.

- Fastest Growing Segment: Law Enforcement & security is the fast-growing end-user segment at 7% CAGR in the forecast period, driven by fatal incident response mandates, rising counter-terrorism protective equipment investment in Europe, and expanding police body armor grant programs funded by U.S. DOJ Byrne JAG allocations.

- Key Market Opportunity: The growing civilian direct-to-consumer body armor segment and next-generation UHMWPE lightweight armor platform development represent an incremental US$ 2.1 billion absolute dollar opportunity between 2026 and 2033, supported by rising personal safety awareness and active shooter response preparedness globally.

DRO Analysis

Drivers - Rising Global Defense Budgets and Military Modernization Programs

Escalating geopolitical instability and active conflict zones across Eastern Europe, the Middle East, and Sub-Saharan Africa are compelling governments to substantially increase defense spending, with personal body armor representing a priority procurement category. NATO reported that 11 of 31 member states met the 2% GDP defense spending target in 2023, with several committing to further increases.

The U.S. Department of Defense (DoD) consistently allocates billions annually to personal protective equipment modernization programs, including the Next Generation Squad Weapons (NGSW) initiative which includes updated body armor specifications. These elevated defense spending commitments across major economies create large, recurring government procurement contracts that underpin market revenue growth.

Growing Law Enforcement Procurement and Active Shooter Incident Response Policies

The rising frequency of active shooter incidents globally is compelling law enforcement agencies to accelerate body armor procurement and replacement programs. The FBI Active Shooter Incidents Report documented 61 active shooter incidents in the U.S. in 2023, maintaining high baseline procurement urgency. The Officer Safety and Wellness Group within the U.S. Department of Justice (DOJ) consistently advocates for universal body armor programs across all law enforcement agencies.

Several U.S. states have implemented body armor grant programs funded through federal Byrne JAG allocations, ensuring continuous equipment refresh cycles. Internationally, European and Asian law enforcement agencies are similarly upgrading to higher-protection-level vests in response to terrorism threats.

Restraints - Stringent Government Export Controls and End-User Certification Requirements

Bulletproof vests are classified as controlled defense articles under the U.S. International Traffic in Arms Regulations (ITAR) and the EU Common Military List, requiring detailed export licensing that significantly extends sales cycles and limits market access for manufacturers targeting international government and commercial clients.

Export compliance costs, documentation requirements, and the risk of license denial create material operational burdens, particularly for smaller manufacturers attempting to expand into Middle East or Asian markets. These regulatory barriers fragment the global market and restrict supply chain optimization for international body armor manufacturers.

Heat, Weight, and Comfort Limitations Constraining Extended-Wear Adoption

Despite advances in materials science, bulletproof vests, particularly Level III and Level IV hard armor plates, remain heavy, heat-retaining, and uncomfortable for extended wear in high-temperature operational environments. Research published in the Journal of Occupational and Environmental Hygiene has documented significant heat stress-related physiological burden among military personnel wearing full body armor systems in warm climates.

These ergonomic limitations reduce compliance rates among civilian and some law enforcement users, constrain the addressable market for continuous-wear configurations, and create persistent incentives to delay vest replacement, moderating replacement cycle velocity.

Opportunities - Expanding Civilian and Private Security Market Driven by Rising Safety Awareness

The civilian body armor segment represents a rapidly growing commercial opportunity, driven by heightened personal safety concerns, active shooter awareness programs, and the proliferation of online direct-to-consumer body armor retail platforms. In the U.S., civilian body armor sales are legal in 49 out of 50 states (Connecticut restricts in-person purchase for convicted felons), and demand is rising among journalists covering conflict zones, private security contractors, and safety-conscious individuals.

Brands including Safe Life Defense and BulletBlocker have successfully established DTC e-commerce channels targeting civilian buyers. Internationally, private security firms operating in Latin America and Sub-Saharan Africa are driving growing procurement demand for concealable soft armor vests, expanding the total addressable market beyond government contracts.

Advanced Material Technologies Enabling Lighter, Higher-Performance Next-Generation Armor

The development of next-generation ballistic materials including ultra-high-molecular-weight polyethylene (UHMWPE) composites, graphene-enhanced fabrics, and novel ceramic-composite hybrid plates is creating premium product replacement cycles across military and law enforcement customers. Companies including Point Blank Enterprises and Armor Express are commercializing multi-threat vests offering combined ballistic, stab, and spike protection in sub-5-pound platforms, a significant improvement over legacy system.

The U.S. Army Soldier Protection System (SPS) program is actively evaluating next-generation materials targeting 25–35% weight reduction versus current issue systems. As military and law enforcement agencies implement technology refresh programs, premium advanced-material armor is expected to command above-average revenue growth through 2033.

Category-wise Analysis

Product Type Insights

Soft body armor leads the product type category, accounting for the dominant share of the bulletproof vests market in 2026. Soft vests, constructed from flexible ballistic fabrics including Kevlar® (DuPont), Dyneema® (DSM), and Spectra® (Honeywell), are the standard daily-wear personal protection solution for law enforcement officers globally due to their concealability under uniforms, full-torso mobility, and all-day wearability.

According to the Bureau of Justice Statistics (BJS), approximately 71% of local U.S. police officers were issued soft body armor as standard duty equipment. The large installed base of law enforcement globally, the U.S. alone has approximately 800,000 full-time sworn officers per BJS data, generates consistent replacement demand on 5-year replacement cycles mandated by NIJ certification standards.

Protection Level Insights

Level IIIA soft body armor represents the leading protection level segment in the bulletproof vests market in 2026, favored for its optimal balance between ballistic protection, weight, and concealability for law enforcement daily-wear applications. NIJ Standard 0101.06 and the updated NIJ 0101.07 (ballistic resistance of body armor) classifications establish Level IIIA as the highest-rated soft armor protection level, providing protection against .44 Magnum and 9mm FMJ threats.

The majority of U.S. police departments issue NIJ-certified Level IIIA vests as standard duty equipment, creating consistent high-volume procurement demand. The availability of concealable Level IIIA vests from multiple manufacturers including Point Blank Enterprises, Safe Life Defense, and U.S. Armor Corporation ensures broad market availability and competitive pricing at this protection tier.

End-user Insights

Military & defense represents the dominant end-user segment in the bulletproof vests market, accounting for approximately 45% share in 2026. This leadership is driven by large government procurement contracts, mandatory personal protective equipment issuance protocols, and continuous military modernization programs across NATO member states, the U.S. DoD, China’s PLA, and India’s Ministry of Defence. Military procurement involves multi-year framework contracts for high volumes of body armor systems, ensuring predictable revenue streams for qualified suppliers.

The U.S. Army alone fields body armor to over 450,000 active-duty soldiers, with regular replacement cycles governed by PEO Soldier acquisition programs. Global military force expansion and modernization in Asia Pacific and the Middle East further sustain the segment’s dominant position.

Regional Insights

North America Bulletproof Vests Market Trends and Insights

North America leads the global bulletproof vests market with 36% market share in 2026, driven by the world’s largest law enforcement body armor procurement programs, active U.S. military modernization contracts, and a growing civilian direct-to-consumer market. Federal Byrne JAG and COPS grant programs continue to fund local law enforcement body armor procurement, while the U.S. DoD Soldier Protection System (SPS) program sustains military upgrade demand.

U.S. Bulletproof Vests Market Size

The United States accounts for approximately 88% of North American revenues, driven by 800,000+ law enforcement officers requiring NIJ-certified body armor on 5-year replacement cycles, over 450,000 active-duty military personnel under continuous equipment modernization, and a growing civilian market estimated to represent 10–12% of total U.S. body armor sales.

Europe Bulletproof Vests Market Trends and Insights

Europe is the second-largest regional market, characterized by rising NATO defense commitments following the Russia-Ukraine conflict, expanded police body armor procurement across EU member states, and growing counter-terrorism protective equipment investment. National defense budget increases in Germany, Poland, and Nordic states are driving multi-year military body armor framework contracts.

Germany Bulletproof Vests Market Size

Germany contributes approximately 22–25% of European market revenues, supported by the Bundeswehr’s ongoing equipment modernization programs and recent Zeitenwende (“turning point”) policy committing Germany to 2% GDP defense spending. Growing GSG 9 and federal police body armor procurement under BMI (Federal Ministry of Interior) frameworks drives consistent revenue.

U.K. Bulletproof Vests Market Size

The U.K. accounts for approximately 17–19% of European revenues, driven by British Army personal protection equipment contracts and Home Office-funded police body armor procurement programs. The College of Policing mandates body armor for frontline officers, sustaining consistent replacement cycle demand across 43 territorial police forces throughout England and Wales.

France Bulletproof Vests Market Size

France contributes approximately 13–15% of European market revenues, driven by Armée de Terre (French Army) procurement and Gendarmerie Nationale and Police Nationale body armor contracts managed through DGA (Direction Générale de l’Armement). France’s ongoing counter-terrorism operational posture sustains above-average per-officer armor investment.

Asia Pacific Bulletproof Vests Market Trends and Insights

Asia Pacific is the fastest growing regional market for bulletproof vests in the forecast period, driven by the rise in defense spending across China, India, South Korea, and Australia. China’s PLA modernization programs include personal protective equipment upgrades for all combat branches, while domestic manufacturers are developing advanced UHMWPE and ceramic armor systems under Made in China 2025 defense technology objectives, reducing import dependency.

India Bulletproof Vests Market Size

India accounts for approximately 20% of Asia Pacific revenues, driven by large-scale Ministry of Defence procurement for the Indian Army and Central Armed Police Forces (CAPFs). India’s Make in India defense manufacturing initiative is promoting domestic body armor production from companies including MKU Limited, reducing import reliance and building export capability.

Japan Bulletproof Vests Market Size

Japan contributes approximately 14% of Asia Pacific market revenues, supported by Japan Self-Defense Forces (JSDF) modernization programs and growing National Police Agency (NPA) procurement under Japan’s expanded defense posture following the 2022 National Security Strategy that doubled defense spending commitments to 2% GDP by 2027.

Southeast Asia Bulletproof Vests Market Size

Southeast Asia accounts for approximately 10–12% of Asia Pacific revenues, with Indonesia, Philippines, Thailand, and Vietnam driving procurement through military modernization and counter-insurgency operational requirements. Growing private security industries across the ASEAN region and expanding border security programs are additional demand catalysts.

Competitive Landscape

The global bulletproof vests market is moderately fragmented, with established leaders including Point Blank Enterprises, Safariland, Armor Express, and MKU Limited competing alongside a large number of regional manufacturers. Key competitive differentiators include NIJ certification compliance, materials technology (UHMWPE vs. aramid), multi-threat protection capability, and government contract qualification status.

DTC civilian-focused brands including Safe Life Defense and AR500 Armor are disrupting traditional distribution models through online retail. R&D trends focus on weight reduction, multi-threat designs combining ballistic, stab, and spike protection, and smart armor with embedded biometric or sensor systems.

Key Developments:

- In March 2025, Point Blank Enterprises received a U.S. Army contract for next-generation Soldier Protection System body armor inserts under the PEO Soldier program, expanding its military plate carrier and soft armor system supply to U.S. combat forces.

- In October 2024, MKU Limited received a large-scale Indian Ministry of Defence contract for advanced multi-threat body armor systems under India’s Make in India defense procurement framework, reinforcing its position as India’s leading domestic armor manufacturer.

- In February 2024, Safe Life Defense launched its updated FRAS® (Flexible Rifle-Armor System) vest series with Level III+ protection in a sub-5-pound soft armor configuration, targeting law enforcement and civilian buyers seeking lightweight rifle-threat protection.

Global Bulletproof Vests Market – Key Insights

| Key Insights | Details |

|---|---|

|

Historical Market Value (2020) |

US$ 2.7 Billion |

|

Current Market Value (2026) |

US$ 3.8 Billion |

|

Projected Market Value (2033) |

US$ 5.9 Billion |

|

CAGR (2026–2033) |

6.4% |

|

Leading Region |

North America, 36% market share (2026) |

|

Dominant End-User (Category-3) |

Military & Defense, 45% market share (2026) |

|

Top-ranking Protection Level (Category-2) |

Level IIIA, leading share (2026) |

|

Incremental Opportunity |

US$ 2.1 Billion (2026–2033) |

Companies Covered in Bulletproof Vests Market

- AR500 Armor

- Blackhawk

- BulletBlocker

- Canadian Armour Ltd

- Imperial Armour

- Point Blank Enterprises

- PPSS Group

- Survival Armor

- Safe Life Defense

- Armor Express

- Safariland

- U.S. Armor Corporation

- MKU Limited

- EnGarde Body Armor

- RMA Armament

Frequently Asked Questions

The global bulletproof vests market is projected to be valued at US$ 3.8 billion in 2026, and is projected to reach US$ 5.9 billion by 2033, growing at a CAGR of 6.4% between 2026 and 2033.

Primary drivers include escalating geopolitical instability accelerating military procurement and rising active shooter incidents with the FBI documenting 61 incidents in the U.S. in 2023 alone.

North America leads with approximately 36% market share in 2026, anchored by the U.S. DoD’s continuous Soldier Protection System procurement for 450,000+ active-duty soldiers, 800,000+ law enforcement officers on federally mandated NIJ certification replacement cycles, and a growing civilian DTC market driven by rising personal safety awareness.

The most significant opportunities are the expanding civilian DTC body armor segment, with brands like Safe Life Defense and BulletBlocker growing through e-commerce channels, and next-generation UHMWPE and ceramic-composite hybrid armor platforms targeting 25–35% weight reduction versus legacy systems under U.S. Army SPS modernization programs, creating premium replacement cycle demand across military and law enforcement customers through 2033.

Key players include Point Blank Enterprises, Safariland, Armor Express, MKU Limited, Safe Life Defense, AR500 Armor, U.S. Armor Corporation, RMA Armament, EnGarde Body Armor, BulletBlocker, Blackhawk, PPSS Group, Canadian Armour Ltd, Imperial Armour, Survival Armor, BAE Systems (Personal Armor), and Protective Products International, among others.