- Industrial Machinery

- Braiding Machine Market

Braiding Machine Market Size, Share, and Growth Forecast 2026 – 2033

Braiding Machine Market by Machine Type (Vertical Braiders, Horizontal Braiders), Automation Level (Automated, Semi-automated/Manual), Application (Textile & Sporting, Industrial, Automotive), and Regional Analysis 2026 – 2033

Braiding Machine Market Size and Trends Analysis

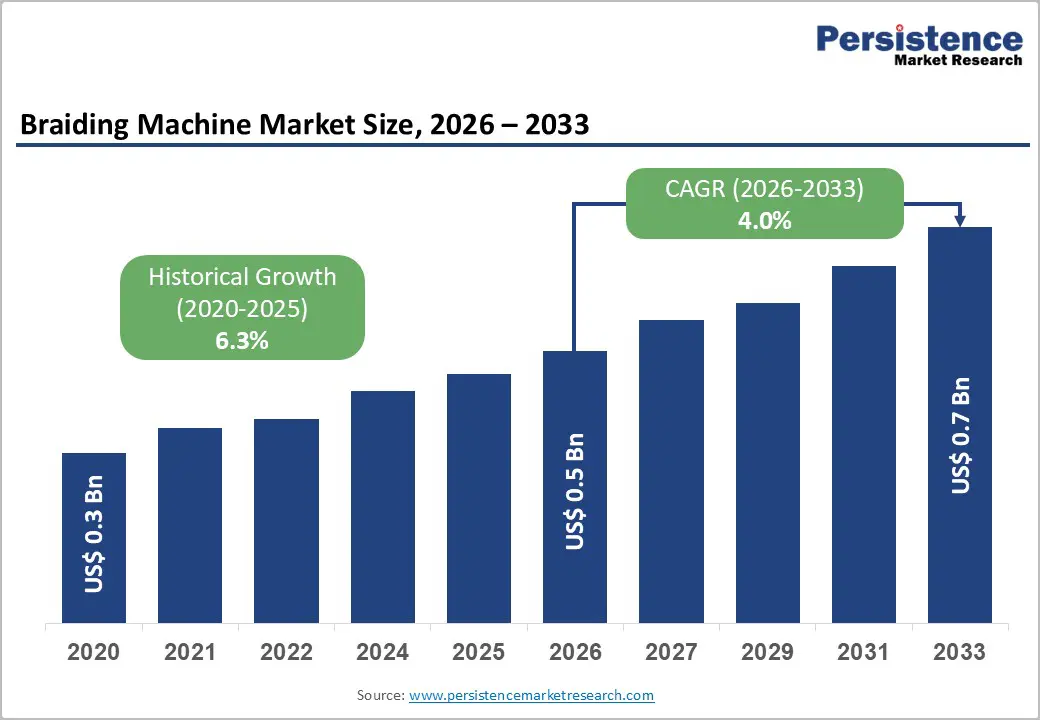

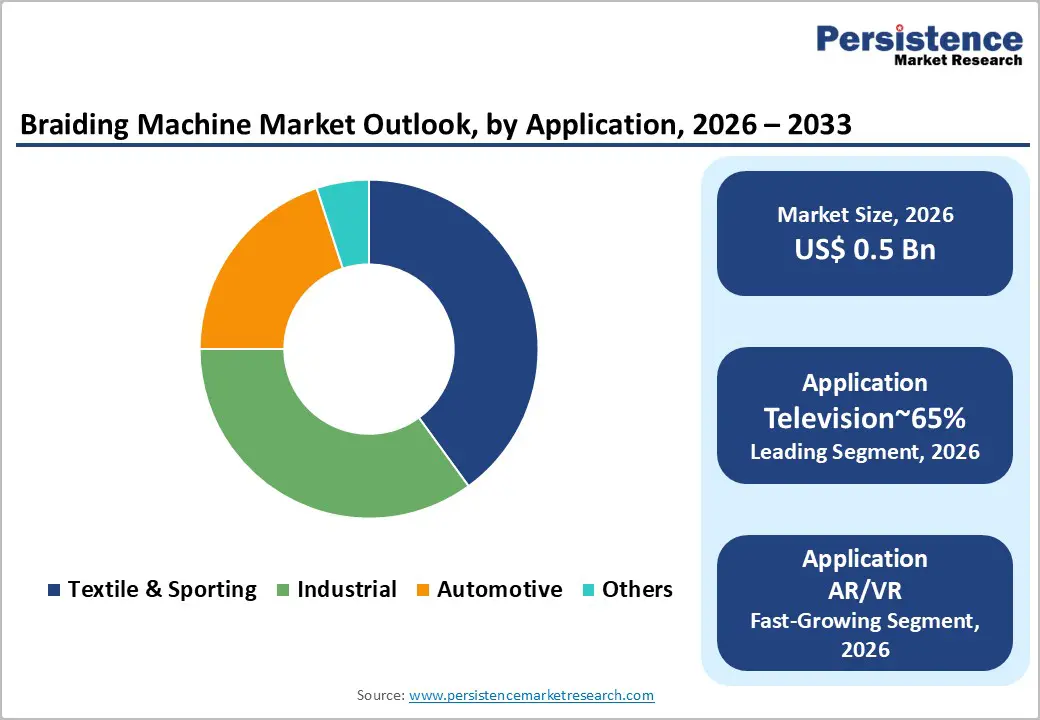

The global braiding machine market size is likely to be valued at US$0.5 billion in 2026 and is expected to reach US$0.7 billion by 2033, growing at a CAGR of 4.0% during the forecast period from 2026 to 2033, driven by the rising demand in automotive and industrial sectors for braided components offering abrasion resistance and flexibility.

The market is currently transitioning from standard textile applications toward high-performance technical braiding for automotive composites and medical devices.

Key Industry Highlights:

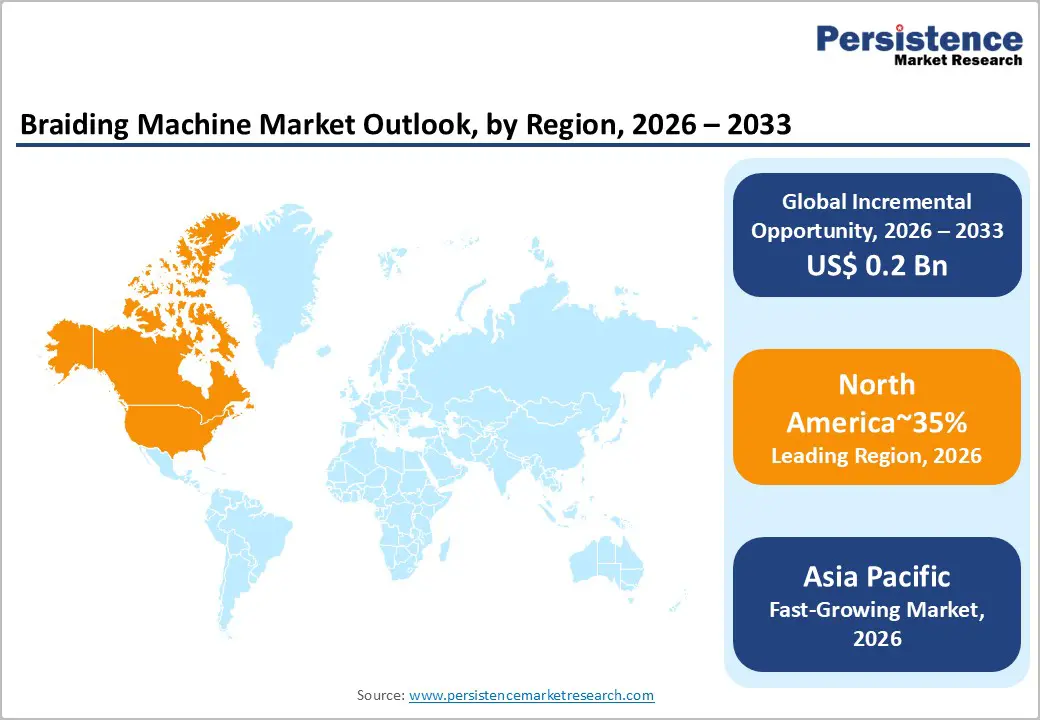

- Leading Region: North America is projected to capture about 35% of the market share in 2026, led by the U.S., driven by advanced automation, IoT-enabled manufacturing, and strong regulatory and industrial infrastructure supporting high-precision composite applications.

- Fastest-Growing Region: Asia Pacific is set to be the fastest-growing region, fueled by industrial modernization, major infrastructure projects, and government-driven innovation in China and India, alongside the rise of IoT-enabled machinery and smart factory initiatives.

- Leading Machine Type Vertical: Braiders are expected to lead the global braiding machine market with approximately 60% share in 2026, driven by versatility across medical tubing, aerospace components, and precision-engineered cables.

- Leading Automation Level: Semi-automated and manual systems are expected to lead with around 70% share in 2026, supported by cost-efficient production models, high labor availability, and flexibility for small batch sizes and customized braiding patterns.

| Key Insights | Details |

|---|---|

| Braiding Machine Market Size (2026E) | US$0.5 Bn |

| Market Value Forecast (2033F) | US$0.7 Bn |

| Projected Growth (CAGR 2026 to 2033) | 4.0% |

| Historical Market Growth (CAGR 2020 to 2025) | 6.3% |

Market Factors – Growth, Barriers, and Opportunity Analysis

Surge in Composite Material Demand for Electric Vehicles

The rapid expansion of electric vehicle production is structurally increasing demand for advanced composite materials as OEMs prioritize lightweighting to counterbalance battery mass and improve energy efficiency. Braided carbon fiber composites are gaining preference over traditional woven structures due to their ability to deliver controlled fiber orientation, including ±45° architectures that enhance torsional stiffness, fatigue performance, and crash energy absorption.

These properties are particularly critical in EV platforms, where components such as drive shafts, structural pillars, and battery protection elements are subjected to complex, multi-directional loads. As regulatory pressure on vehicle efficiency intensifies, automakers are accelerating the substitution of metallic components with braided composite solutions to meet performance and sustainability targets.

This material shift is directly translating into higher demand for braided preforms across the automotive value chain, reinforcing equipment investments among Tier 1 composite manufacturers. Industry data indicates that automotive demand for braided preforms is expanding at an annual rate exceeding 5.5%, driving procurement of high-speed horizontal braiders capable of handling heavy-tow carbon fibers at scale.

Consequently, braiding machinery suppliers are positioned as critical enablers of next-generation electric mobility architectures, with equipment performance and throughput becoming decisive factors in OEM and supplier capital allocation strategies. In June 2025, Researchers (China University of Geosciences) unveiled a new methodology for 3D braiding machine design.

Introduces a systematic design strategy validated by constructing an automatic 6-3 type 3D braiding machine, advancing complex preform production for aerospace and composites.

High Capital Investment and Maintenance Burden

Advanced automated braiding systems impose a substantial capital barrier, particularly as manufacturers increasingly integrate Industry 4.0 capabilities such as embedded sensors, real-time defect monitoring, and digitally synchronized production controls. These features, while enhancing precision and yield consistency, significantly elevate upfront equipment costs. As a result, adoption remains concentrated among large composite manufacturers and Tier 1 suppliers with access to strong balance sheets.

Small and mid-sized enterprises, especially in cost-sensitive or developing markets, face structural constraints in justifying such investments, limiting broader market penetration and slowing capacity expansion across the lower tiers of the supply chain.

Beyond initial acquisition, the total cost of ownership further restrains adoption. Automated braiding systems rely on proprietary software, specialized mechanical components, and OEM-certified service protocols, which restrict maintenance flexibility and raise long-term operating expenses. Downtime risks are amplified due to the limited availability of trained technicians and replacement parts, reinforcing dependence on original equipment manufacturers.

These factors collectively increase lifecycle costs and compress margins for smaller operators, discouraging rapid technology upgrades. Consequently, high capital intensity and maintenance complexity continue to act as structural headwinds, shaping a market environment where scale, financial resilience, and service access determine competitive viability.

Emerging Smart Textiles and Wearable Applications

The accelerating convergence of textiles with electronics is opening a structurally attractive opportunity for advanced braiding technologies. Smart textiles, increasingly embedded with sensing, heating, and signal-transmission functions, require precise fiber placement and stable integration of conductive yarns within complex architectures.

Braiding, particularly in vertical and multi-axial configurations, is well-suited to these requirements, enabling consistent mechanical performance while accommodating functional materials such as metallic or carbon-based conductors. As smart garments, medical monitoring fabrics, and responsive industrial textiles move from prototyping to scaled production, demand is shifting toward specialized braiding equipment capable of handling hybrid yarn systems without compromising throughput or quality.

Wearables and consumer electronics act as a parallel demand catalyst, reinforcing this opportunity across adjacent value chains. Applications such as textile-based biosensors, motion-tracking fabrics, and embedded antenna structures increasingly rely on braided preforms to balance flexibility, durability, and electrical continuity.

For equipment manufacturers, smart textiles represent an actionable expansion avenue, allowing diversification beyond traditional industrial composites while aligning with long-term growth in digital health, connected devices, and human–machine interface technologies. In December 2024, Mayer & Cie. delivered the first MR-11 braiding machine with 48 carriers. New high-capacity model enables larger inner diameters (up to 150 mm textile / 50 mm wire) with unchanged coil volumes and short setup times, expanding application range for hoses and technical textiles.

Category–wise Analysis

Machine Type Insights

Vertical braiders are expected to remain both the leading and fastest growing machine type, accounting for approximately 60% of total market share. Their dominance is projected to persist due to high versatility across end-use applications such as medical tubing, aerospace components, and precision-engineered cables.

The compact vertical configuration is anticipated to remain preferred where floor-space efficiency and controlled braiding accuracy are critical operational requirements. Increasing demand for tight-tolerance braided structures in high-value applications is expected to reinforce adoption across regulated manufacturing environments. Vertical systems are also expected to benefit from easier integration with automated production lines and quality monitoring systems. Collectively, these structural advantages position vertical braiders as the central anchor of market expansion over the forecast period.

Horizontal braiders are likely to account for approximately 40% of market share, supporting complementary demand growth across industrial segments. Adoption is anticipated to be driven by applications requiring enhanced stability and support for rigid mandrels and large-diameter components. Industries such as automotive, heavy machinery, and industrial textiles are expected to rely on horizontal configurations for complex braiding geometries.

The ability to handle heavier materials and longer production runs is projected to sustain relevance in scale-driven manufacturing environments. While comparatively less space-efficient, horizontal systems are expected to remain essential for specific technical requirements. Their role is forecast to remain structurally important within a diversified machine-type landscape.

Automation Type Insights

Semi-automated and manual systems are expected to lead, accounting for approximately 70% of the overall market share in 2026. The dominance is anticipated to persist due to continued reliance on cost-efficient production models across textile-focused manufacturing hubs in Asia and South America. These systems are expected to remain preferred where labor availability is high, and capital expenditure sensitivity shapes purchasing decisions.

Flexibility in handling small batch sizes and customized braiding patterns is projected to sustain adoption across decentralized production environments. Semi-automated setups are also expected to support gradual technology upgrades without full system replacement. Together, these factors position semi-automated and manual systems as the structural backbone of global installed capacity.

Automated systems are expected to be the fastest-growing automation segment, driven by rising labor constraints and increasing quality consistency requirements in advanced manufacturing regions. High-precision sectors such as medical devices and aerospace are expected to accelerate adoption due to stringent compliance and repeatability needs. Automated platforms are also projected to benefit from integration with smart factory frameworks and centralized production monitoring systems.

Enhanced process control and data traceability are expected to improve operational efficiency across complex braiding applications. As a result, automated systems are forecast to steadily expand their structural role within high-value manufacturing environments.

Regional Insights

North America Braiding Machine Market Trends

North America is expected to hold approximately 35% of the market share in 2026, reflecting a mature and structurally advanced regional position. The U.S. anchors regional demand, driven by high-precision applications in aerospace and medical device manufacturing. Advanced automation, digital controls, and IoT integration enhance production efficiency and enable predictive maintenance, supporting sophisticated manufacturing requirements.

Regulatory frameworks such as FDA compliance reinforce a focus on traceability, quality, and precision, particularly for critical components subraided catheters, stents, and lightweight composite aerospace parts. The region’s industrial infrastructure and R&D ecosystem further consolidate North America’s strong market position.

The region is likely to sustain steady growth as demand for technical textiles, composites, and specialty materials continues to rise. In medical device manufacturing, vertical and circular braiding machines produce intricate, small-diameter tubes requiring high tensile strength, flexibility, and biocompatibility. Canada contributes incremental expansion through innovation clusters and enterprise adoption, complementing the U.S. lead. Structural capabilities, high-value industrial applications, and advanced automation collectively support North America’s market stability and continued relevance in high-precision braiding technology.

Europe Braiding Machine Market Trends

Europe is expected to maintain a mature and technologically advanced market position, with Germany leading regional demand. Key engineering firms such as HERZOG GmbH, Mayer & Cie., and Spirka Schnellflechter drive high-end automation and precision.

European manufacturers are embracing Industry 4.0 technologies, including fully digitized 3D braiding machines, digital twins, and real-time data monitoring, to improve process control and product accuracy. Policy-driven sustainability initiatives promote the use of recycled yarns, bio-based filaments, and energy-efficient operations, reinforcing the region’s emphasis on compliance, quality, and eco-conscious manufacturing.

The region is projected to sustain steady growth as aerospace and automotive sectors continue to require lightweight, complex composite parts. Institutions such as ITA at RWTH Aachen University showcase advanced applications of 3D rotary braiding, producing near-net-shape preforms with reinforcement in all spatial directions, enabling high-pressure engine components and structural fuselage parts in a single automated step. Coupled with rigorous quality certifications, high-precision automation, and sector-specific expertise, Europe’s market remains innovation-driven and highly specialized.

Asia Pacific Braiding Machine Market Trends

Asia Pacific is expected to emerge as the fastest-growing region due to rapid industrial modernization and infrastructure-driven demand. China anchors regional growth, leveraging massive production capacity, government-backed innovation programs, and dominance in raw fiber supply. The region is experiencing widespread adoption of IoT-enabled and electronic braiding machines, supported by Smart Factory initiatives, which enhance production speed, real-time monitoring, and operational efficiency. High-value technical textiles for medical devices and aerospace components further strengthen adoption, complementing traditional large-scale manufacturing capabilities.

The region is likely to sustain accelerated growth as massive urbanization and energy infrastructure projects drive demand for heavy-duty braided products. In China and India, production of braided grounding jumpers, cable shielding, and reinforced hoses is expanding to support national power grids and high-speed rail networks.

These applications require high-volume, robust braiding machines capable of interweaving high-conductivity metals such ascopper and aluminum. Combined with local R&D and emerging automation, these structural and demand-driven factors reinforce Asia Pacific’s fastest-growing position in the global braiding machine market.

Competitive Landscape

The global braiding machine market is moderately consolidated at the high end, with the top five players, Herzog, Mayer & Cie, OMA, Steeger, and Wardwell, accounting for roughly 45–50% of revenue. These companies lead specialized segments such as medical devices and advanced composite manufacturing through precision engineering, technological innovation, and established global distribution networks. Key differentiators at this level include machine accuracy, automation, and service reliability, catering to clients with complex production needs.

In contrast, the lower-end and standard textile segments remain highly fragmented, particularly in Asia-Pacific, where regional manufacturers such as Xuzhou Henghui in China and smaller Indian SMEs compete mainly on price and delivery. Market concentration is stronger in Europe and North America, driven by mature industrial bases, while APAC exhibits a highly competitive, cost-sensitive environment. Across the market, the focus is on technical sophistication at the top tier and cost efficiency in fragmented regions.

Key Industry Developments:

- In November 2025, HERZOG hosted Open House 2025, showcasing its latest braiding and winding machines. The company presented advanced braiding technologies, winding solutions, and recent investments to international customers and partners.

- In April 2025, Medical Manufacturing Technologies (MMT) acquired FEPeeler, adding advanced braided catheter cutting solutions. This acquisition improved its ability to perform precise heat-shrink removal and cut braided medical tubing, boosting production efficiency in catheter manufacturing.

- In March 2025, Mayer & Cie. completed a major automation upgrade by installing new CNC lathes. The company installed the fourth of five state-of-the-art DMG Mori lathes to enhance manufacturing efficiency and precision of braiding machine components.

Companies Covered in Braiding Machine Market

- Wardwell Braiding Co.

- HERZOG GmbH

- Mayer & Cie. GmbH & Co. KG

- Steeger USA

- Cobra Braiding Machinery Ltd.

- Kyang Yhe Delicate Machine Co., Ltd.

- Talleres Ratera, S.A.

- Spirka Schnellflechter GmbH

- OMEC S.r.l.

- Alfa Flexitubes Pvt. Ltd.

- NIEHOFF Schwabach

- O.M.A. S.r.l.

- Magnatech International

- Braidwell Machines Co.

- Xuzhou Henghui Braiding Machine Co., Ltd.

- Lamb Knitting Machine Corp.

Frequently Asked Questions

The global braiding machine market is projected to be valued at US$0.5 billion in 2026 and is expected to reach US$0.7 billion by 2033, driven by the transition toward high-performance technical braiding for automotive and medical applications.

Demand is shifting due to the rapid expansion of electric vehicle production, which requires lightweight composite materials, and the growing need for high-precision braided components in medical devices, aerospace, and industrial sectors where abrasion resistance and flexibility are critical.

The braiding machine market is forecast to grow at a CAGR of 4.0% from 2026 to 2033, supported by advancements in automation and the rising adoption of smart textiles and composites.

Asia Pacific is the fastest-growing regional market, fueled by rapid industrial modernization, massive infrastructure projects in China and India, government-backed innovation programs, and the widespread adoption of IoT-enabled manufacturing.

Key players include Herzog GmbH, Mayer & Cie., OMA, Steeger, and Wardwell, among others. These companies dominate the high-end segment, focusing on precision engineering and automation for advanced technical applications.