- Industrial Machinery

- Braiding Machine Spindles Market

Braiding Machine Spindles Market Size, Share, Trends, Growth, Regional Forecasts, 2026 to 2033

Braiding Machine Spindles Market by Product Type (Horizontal, Vertical), Application (Textile, Automotive, Aerospace, Medical), Material (Steel, Aluminum, Composite Materials), and Regional Analysis for 2026-2033

Braiding Machine Spindles Market Share and Trends Analysis

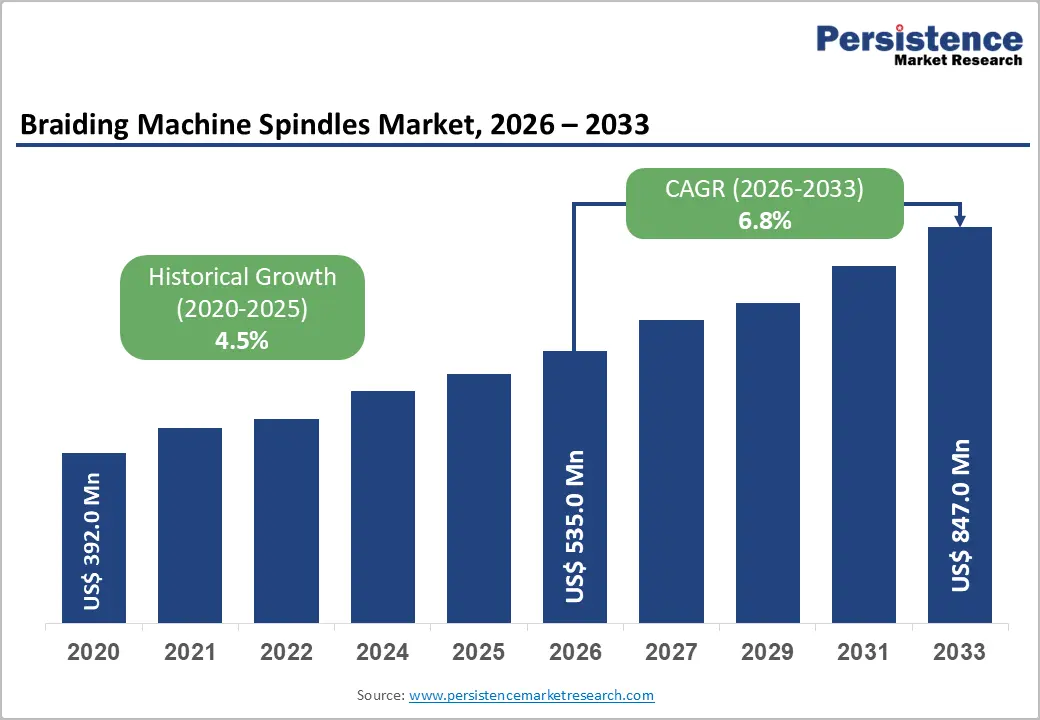

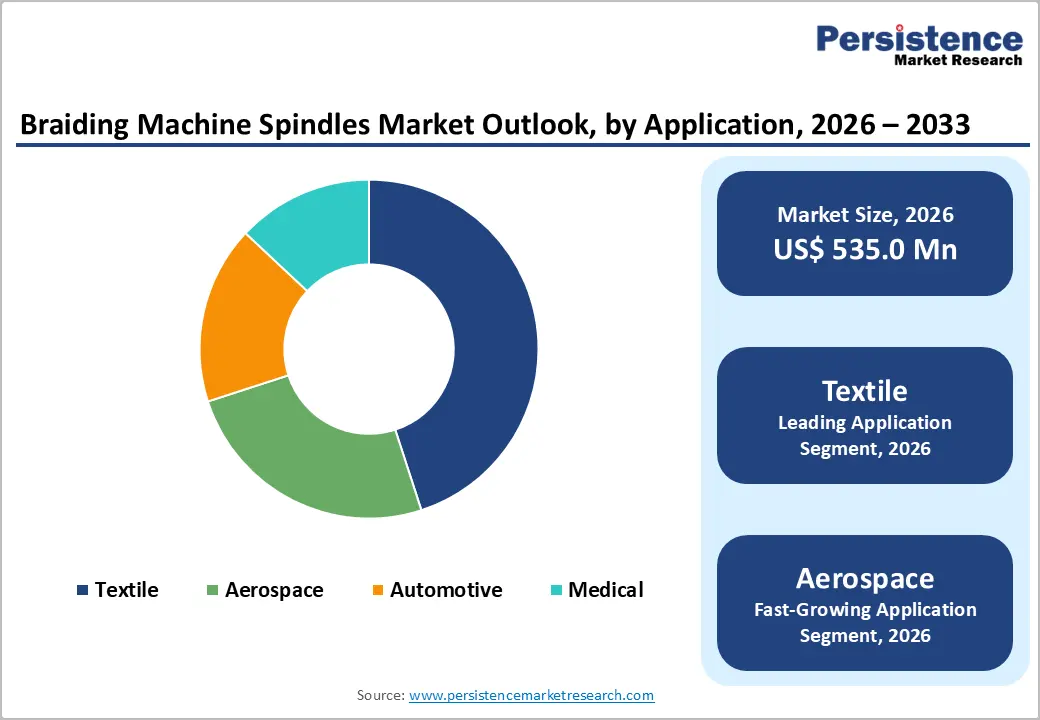

The global braiding machine spindles market size is likely to be valued at US$ 535.0 million in 2026, and is projected to reach US$ 847.0 million by 2033, growing at a CAGR of 6.8% during the forecast period 2026−2033.

The steady expansion of the market is underpinned by rising industrial demand for precision-engineered textile and composite-reinforcement machinery, particularly in aerospace, automotive lightweighting, and medical device manufacturing.

The accelerating adoption of advanced braided composites in structural applications, combined with ongoing modernization of textile production infrastructure in emerging economies, is creating robust demand for high-performance spindle systems. Furthermore, technological innovation in spindle materials ranging from hardened tool steels to ceramic-coated alloys is enhancing operational lifespans and reliability, directly stimulating replacement and capacity-expansion cycles across key end-use industries globally.

Key Industry Highlights

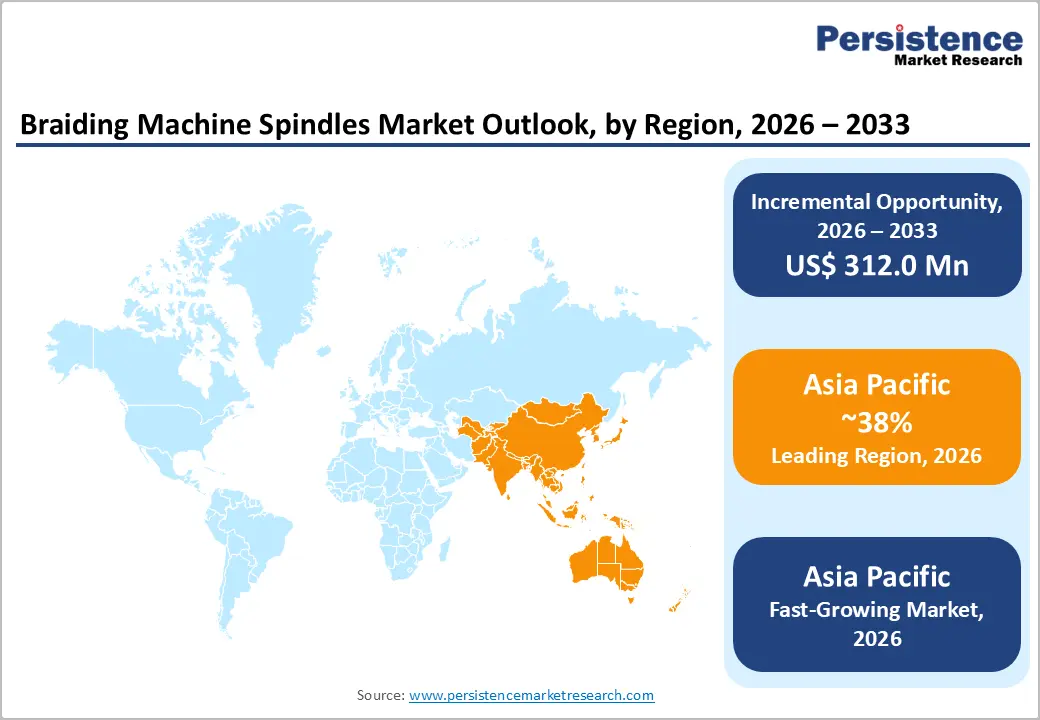

- Dominant Region & Fastest-growing Market: Asia Pacific is likely to be both the dominant region as well as the fastest-growing market through 2033, supported by sustained investments in production infrastructure by regional stakeholders.

- Leading & Fastest-growing Product Type: Horizontal spindles are set to lead with about 58% revenue share in 2026, with vertical spindles growing the fastest during the 2026-2033 forecast period.

- Leading & Fastest-growing Application: Textile industry is slated to capture approximately 42% revenue share in 2026, while aerospace industry is expected to be the fastest-growing over the 2026-2033 forecast period.

- Market Opportunities: IoT-enabled sensors integrated into braiding machine spindles are revolutionizing manufacturers' approaches to performance monitoring and maintenance.?

| Key Insights | Details |

|---|---|

| Braiding Machine Spindles Market Size (2026E) | US$ 535.0 Mn |

| Market Value Forecast (2033F) | US$ 847.0 Mn |

| Projected Growth (CAGR 2026 to 2033) | 6.8% |

| Historical Market Growth (CAGR 2020 to 2025) | 4.5% |

DRO Analysis

Surging Demand from Aerospace & Automotive Composite Manufacturing

The composites sector is increasingly driving demand for braiding machine spindles, with manufacturers ramping up the adoption of advanced materials. Regulatory frameworks such as the Federal Aviation Administration (FAA) Next Generation Air Transportation System (NextGen) program and the European Union (EU) Fit for 55 climate packages are pushing aerospace companies to adopt lighter and stronger structures. Aircraft manufacturers are integrating braided fiber reinforced polymer (FRP) components to improve fuel efficiency and structural performance. This shift is requiring continuous installation of advanced braiding systems, and each system is depending on high precision spindles to maintain quality and consistency.

Production facilities are scaling operations to meet these evolving requirements, and spindle demand is rising in direct response to this transition. A similar transformation is unfolding in the automotive sector as manufacturers are advancing electric vehicle (EV) platforms with a focus on weight reduction and durability. Engineers are incorporating carbon fiber reinforced materials into battery enclosures and chassis structures to enhance performance and safety. This material shift is increasing the reliance on braiding technologies, which are enabling complex geometries and superior strength characteristics. Equipment suppliers are developing more efficient and durable spindles to support continuous production cycles.

Industrial Modernization & Textile Machinery Upgradation in Developing Economies

Government-backed industrialization efforts across Asia and Africa are accelerating investment in textile and technical fabric manufacturing. Policy frameworks such as India’s Production Linked Incentive (PLI) Scheme for Textiles and China’s Made in China 2025 initiative are encouraging companies to modernize production capabilities and adopt advanced machinery. Manufacturers are installing high performance braiding equipment to improve efficiency and product quality in response to rising demand for specialized fabrics. These programs are creating a supportive environment where local and international players are expanding capacity with a long-term focus on competitiveness.

Industry momentum is also reflecting a clear shift toward technical textiles, where applications are becoming more complex and performance-driven. Companies are replacing conventional machines with high-speed braiding systems that can handle advanced materials and intricate designs. This transition is generating steady demand for spindles across original equipment manufacturer (OEM) and aftermarket segments. Equipment providers are responding by offering durable and efficient spindle solutions that support higher production cycles. Modernization efforts are continuing, the industry will have built a stronger foundation for sustained spindle demand driven by ongoing equipment upgrades and maintenance requirements.

Competitive Pressure from Alternative Fiber Placement Technologies

Filament winding and automated fiber placement (AFP) are gaining traction in selected composite manufacturing processes, positioning them as credible alternatives to braiding and intensifying competitive pressure within the segment. These methods are offering high precision material placement and improved control over fiber orientation, which is making them suitable for complex aerospace structures. Companies such as Coriolis Composites, Electro impact, and Fives are advancing automated systems that are being adopted for structural panels and other high-performance components. Aerospace manufacturers are increasingly evaluating these technologies to achieve consistent quality and reduce material waste. This shift is gradually influencing equipment selection decisions, particularly in applications where precision and repeatability are critical.

This competitive pressure is shaping the growth outlook for braiding technologies in premium segments. Manufacturers are continuing to use braiding for applications that require flexibility and complex tubular structures, yet some high value programs are transitioning toward automated fiber placement systems. As this transition is progressing, the demand for braiding machine spindles is facing constraints in specific use cases. Equipment suppliers are responding by improving spindle durability and efficiency to remain relevant in evolving production environments. The industry will have adapted by focusing on niche applications where braiding continues to offer distinct performance and cost advantages.

Supply Chain Fragility for Specialty Alloys

High performance spindles are relying on advanced materials such as hardened tool steel, titanium alloys, and ceramic composites to ensure durability and precision during operation. These materials are enabling manufacturers to maintain consistent performance under demanding production conditions. Supply chains for these inputs are becoming increasingly complex due to geopolitical developments and trade restrictions. Export controls on critical minerals and alloy precursors are disrupting sourcing strategies and are creating uncertainty in procurement cycles. Manufacturers are actively seeking alternative suppliers and are adjusting inventory strategies to reduce dependency on limited sources. These changes are unfolding, production planning is becoming more cautious, and companies are prioritizing material efficiency to manage risks associated with fluctuating availability.

The Russia-Ukraine war has severely disrupted aerospace raw material supplies, as Ukraine provided ~50-70% of global semiconductor-grade neon (halting production from key plants) and both nations supplied critical titanium sponge and palladium, leading to price surges like 90% for titanium since 2022. Spindle producers are experiencing cost pressures and are absorbing higher input expenses while trying to maintain competitive pricing. Delays in material availability are affecting manufacturing timelines and are extending delivery schedules for end users. Companies are investing in material innovation and process optimization to reduce reliance on constrained resources. The industry will have strengthened its resilience by diversifying supply chains and improving cost management practices to sustain long term operational stability.

Smart Spindle Systems & Industry 4.0 Integration

The integration of Internet of Things (IoT)-enabled sensors into braiding machine spindle assemblies is reshaping how manufacturers are managing performance and maintenance. Advanced features such as real time tension monitoring and condition tracking are allowing operators to detect irregularities at an early stage. Spindle systems are increasingly incorporating microelectromechanical systems (MEMS) based sensors to measure vibration and temperature with high accuracy. This approach is helping manufacturers improve operational reliability while reducing unplanned downtime. Equipment producers are designing intelligent spindle units that are continuously collecting and transmitting data, which is supporting more informed decision making across production environments.

A strong commercial advantage is emerging as companies are leveraging predictive maintenance capabilities to create new revenue streams. Original equipment manufacturers (OEMs) are offering service models that rely on continuous data analysis and remote diagnostics. These offerings are enabling long term customer engagement while improving equipment lifecycle management. Spindle manufacturers are positioning premium products with embedded intelligence to differentiate themselves in a competitive market. This shift is encouraging closer collaboration between machinery providers and end users to optimize system performance. The industry will have moved toward a more service driven model where data enabled solutions are playing a central role in enhancing efficiency, reliability, and overall value creation.

Expansion in Infrastructure & Energy Sectors Composites for Renewables

The transition toward renewable energy is accelerating demand for advanced composite structures used in critical infrastructure. Sectors such as wind energy and hydrogen storage are expanding rapidly as governments and industries are prioritizing low carbon solutions. Organizations such as the International Renewable Energy Agency are highlighting the need for large scale capacity additions, which is encouraging manufacturers to scale up production capabilities. In wind turbine manufacturing, braided composite preforms are being used in structural sections such as spar caps and root areas to enhance strength and fatigue resistance. This shift is requiring reliable and high precision braiding equipment, which is directly increasing the importance of spindle performance in maintaining production efficiency and product quality.

Hydrogen infrastructure is also creating new opportunities as manufacturers are developing advanced storage systems for clean energy applications. Production facilities are adopting braiding technologies to meet strict safety and durability requirements. This expansion is pushing equipment suppliers to deliver more robust and efficient spindle solutions that can support continuous and high-volume manufacturing. Renewable energy projects are advancing across regions, the industry will have unlocked new growth avenues where spindle demand is being driven by evolving material requirements and the need for consistent manufacturing precision.

Category-wise Analysis

Product Type Insights

Horizontal braiding machine spindles are likely to be the dominant product types, commanding approximately 58% of the market revenue share in 2026. These systems are supporting continuous manufacturing of tubular and cylindrical structures used in industries such as automotive and industrial textiles. Their design is allowing stable operation, ease of maintenance, and efficient material handling, which is making them suitable for large scale facilities. Producers are preferring horizontal configurations due to their compatibility with existing production lines and lower operational complexity. Demand is increasing for consistent and cost-effective output this segment is maintaining its dominance across established applications.

Vertical braiding machine spindles is likely to be the fastest-growing segment during the 2026-2033 forecast period. Systems are enabling precise fiber placement and better control over intricate geometries required in aerospace and energy applications. Manufacturers are adopting vertical configurations to produce components with superior strength and lightweight characteristics. Their ability to handle advanced materials is attracting investments in next generation production setups. Innovation is accelerating in sectors such as renewable energy and aerospace this segment will have gained strong momentum driven by increasing demand for specialized and high precision manufacturing solutions.

Application Insights

Textile industry is anticipated to secure an estimated 42% of the braiding machine spindles market revenue share in 2026, due to the deepening focus of manufacturers on improving product quality and design flexibility. Growing demand for advanced fabrics is encouraging companies to adopt modern production technologies that can deliver precision and consistency. Braiding processes are enabling the creation of complex patterns that are essential for technical and functional textiles. Spindle performance is playing a critical role in ensuring smooth operations and minimizing defects. Production requirements are evolving textile manufacturers are increasingly relying on advanced spindle systems to achieve higher efficiency and maintain competitive standards.

Aerospace industry is expected to be the fastest-growing segment over the 2026-2033 forecast period. Manufacturers are prioritizing lightweight and high strength components. Products such as aircraft cables and wiring harnesses are requiring advanced braiding techniques to ensure durability and performance. Precision and reliability are essential in this sector, which is driving the adoption of high-quality spindle systems that can deliver consistent results. Production processes are becoming more sophisticated as new aerospace technologies are evolving. Aircraft manufacturing activity is expanding, the demand for efficient and accurate braiding solutions will have increased, supporting steady growth in this segment.

Regional Insights

Asia Pacific Braiding Machine Spindles Market Trends

Asia Pacific is likely to be both the leading and fastest-growing regional market for braiding machine spindles through 2033, accounting for approximately 38% of the market share. Countries such as China, India, and Japan are strengthening their positions through sustained investments in production infrastructure. Strong growth in sectors such as automotive and textiles is increasing the need for advanced braiding technologies that can deliver efficiency and precision. Manufacturers are upgrading facilities to support higher output and improved product quality. This regional momentum is encouraging both domestic and international companies to expand their operations, which is reinforcing the demand for reliable spindle systems across diverse industrial applications.

A deeper shift is taking place as companies are focusing on technological advancement and process optimization to stay competitive. Production units are integrating modern equipment that supports automation and consistent performance. Governments are promoting innovation driven manufacturing through policy support and infrastructure development. This environment is enabling faster adoption of advanced machinery, including high performance spindles that can meet evolving production requirements. Industries are progressing toward more specialized and value-added products the region will have strengthened its leadership by building a resilient manufacturing ecosystem supported by continuous technological adoption and skilled workforce development.

Europe Braiding Machine Spindles Market Trends

Europe is emerging as a strong opportunity area for the braiding machine spindles market as its manufacturing sector is maintaining high standards of precision and quality. Countries such as Germany, France, and United Kingdom are leading industrial activity through well-established automotive and aerospace industries. Manufacturers are focusing on producing high performance components that require advanced braiding technologies. This demand is encouraging the adoption of reliable spindle systems that can support consistent and accurate production. Industrial players are continuously refining processes to meet strict regulatory and performance requirements, which is strengthening the role of precision equipment across the region.

Sustainability is becoming a central theme as companies are aligning operations with environmental goals and efficient resource utilization. Production facilities are integrating advanced technologies to reduce waste and improve energy efficiency. Automation and digital monitoring systems are gaining traction as manufacturers are aiming to enhance productivity and maintain quality benchmarks. Research and development efforts are supporting innovation in materials and manufacturing techniques, which is further expanding the scope of braiding applications. The region will solidify its leadership through the fusion of advanced technology and sustainable practices, fostering enduring industrial expansion.?

North America Braiding Machine Spindles Market Trends

North America is maintaining a strong position in the braiding machine spindles market as advanced industries are driving consistent demand for precision manufacturing. Sectors such as aerospace and medical devices are requiring high performance braided components that meet strict quality and safety standards. The United States is playing a central role due to its well-established industrial base and focus on technological advancement. Manufacturers are investing in modern equipment to improve production accuracy and efficiency.

This environment is encouraging the use of advanced braiding systems that rely on durable and reliable spindle assemblies to support continuous and high-quality output. Innovation is shaping the regional landscape as companies are prioritizing research and development to stay competitive in global markets. Production facilities are adopting advanced materials and digital manufacturing techniques to enhance product performance. Industries are expanding the use of braided structures in applications that require strength, flexibility, and precision. Medical device manufacturers are increasingly using braiding technologies for specialized products that demand consistent quality.

Competitive Landscape

The global braiding machine spindles market structure is moderately fragmented, dominated by leading players such as Herzog GmbH, Steeger USA, Karg Industrie-Produkte AG, and Mayer & Cie. GmbH & Co. KG. These players collectively capture 35-40% of the market share. The market is becoming highly competitive as both established manufacturers and emerging companies are actively strengthening their positions. Market participants are focusing on innovation and cost efficiency to differentiate their offerings and improve profitability.

Companies are also investing heavily in research and development (R&D) to enhance spindle performance, durability, and precision across diverse applications. Product development efforts are addressing industry specific requirements, which is helping manufacturers expand their customer base. Strategic collaborations and partnerships are also gaining importance as firms are combining technical expertise and resources to accelerate innovation and broaden their presence in regional and global markets.

Key Industry Developments

- In January 2026, Comflex Industrial completed and prepared for shipment a wire braiding machine and bobbin winder to Iran, following comprehensive inspection and trial operations to ensure performance and compliance. The delivery highlights the company’s manufacturing capabilities, with the equipment designed for stable operation, high efficiency, and consistent product quality to meet customer production requirements.

Companies Covered in Braiding Machine Spindles Market

- Herzog GmbH

- Steeger USA

- Karg Industrie-Produkte AG

- HERZOG Flechtmaschinen GmbH

- Mayer & Cie. GmbH & Co. KG

- Murata Machinery Ltd.

- Spirka Schnellflechtter GmbH

- Braiding Technology

- Ratera S.A.

- Cobra Braiding Machinery

- Talleres Ratera S.L.

- Hsing Cheng (H.C.) Machinery

- Shanghai Jiulong Textile Machinery

- Hangzhou Gland Packing Co., Ltd.

Frequently Asked Questions

The global braiding machine spindles market is projected to reach US$ 535.0 million in 2026.

Rising demand from textiles, automotive, and aerospace for lightweight braided materials is driving growth.

The market is poised to witness a CAGR of 6.8% from 2026 to 2033.

Customized high-capacity spindles for niche applications and Industry 4.0 integration offer expansion opportunities.

Herzog GmbH, Steeger USA, Karg Industrie-Produkte AG, and Mayer & Cie are some of the key players in the market.