- Beverages

- Birch Water Market

Birch Water Market Size, Share, and Growth Forecast, 2025 - 2032

Birch Water Market by Product Type (Unflavoured, Flavoured), Application (Beverages, Cosmetics & Personal Care, Pharmaceuticals), Distribution Channel (B2B, B2C), and Regional Analysis for 2025 – 2032

Birch Water Market Size and Trends Analysis

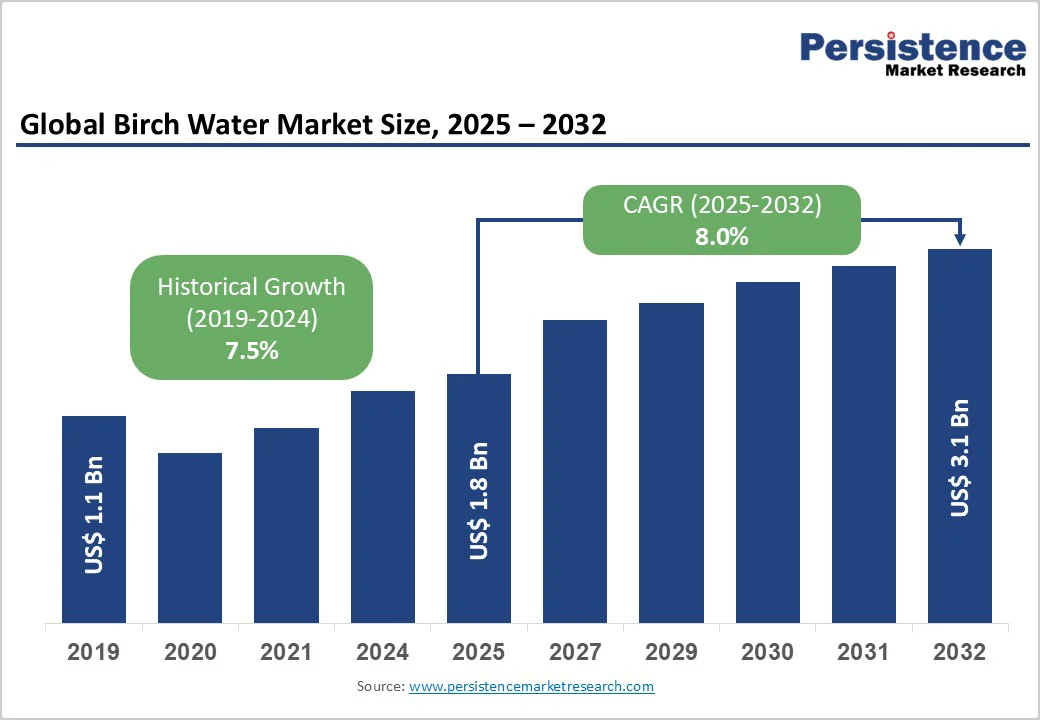

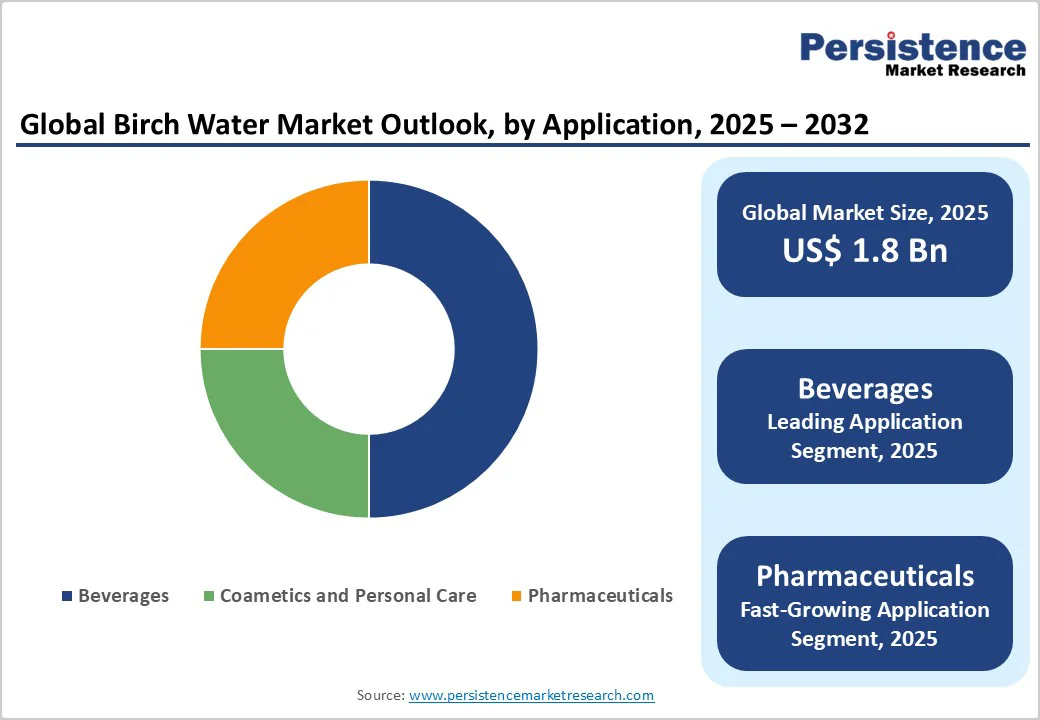

The global birch water market size is likely to be valued US$1.8 Bn in 2025, projected to reach at US$3.1 Bn by 2032 with growing at a CAGR of 8.0% during the forecast period from 2025 to 2032 driven by the increasing consumer preference for natural, low-calorie functional beverages, rising health consciousness regarding hydration and detoxification, and expanding applications in cosmetics and pharmaceuticals.

The market is further propelled by innovations in flavoured variants and sustainable sourcing, catering to preferences for clean-label products. The growing acceptance of birch sap as a versatile superfood ingredient, especially in premium beverages and skincare, is a key growth factor.

Key Industry Highlights:

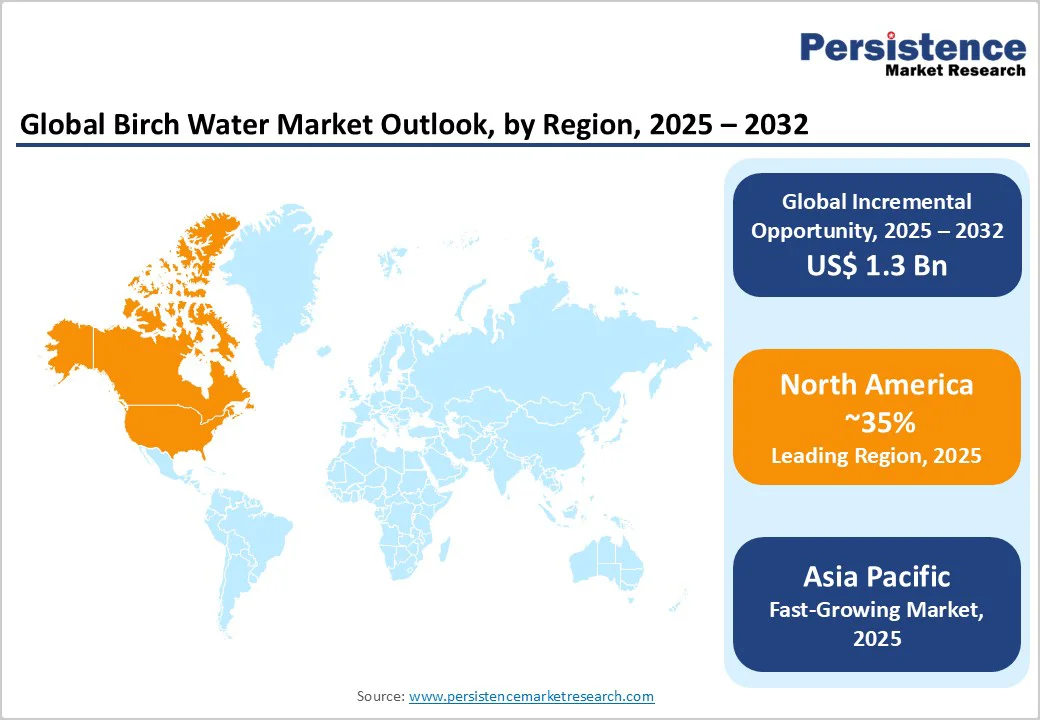

- Leading Region: North America, commanding a 35% market share in 2025, driven by high wellness trends, advanced e-commerce penetration, and strong demand in the U.S. for natural hydration solutions.

- Fastest-growing Region: Asia Pacific, fueled by rapid urbanization, rising disposable incomes, and investments in functional foods in countries such as China and India.

- Dominant Product Type: Unflavoured, holding approximately 60% of the market share, due to its purity, natural taste, and widespread use in health-focused applications.

- Leading Application: Beverages, accounting for over 50% of market revenue, driven by demand for ready-to-drink functional drinks.

- Leading Distribution Channel: B2C, contributing nearly 55% of market revenue, owing to direct-to-consumer sales via online platforms and retail.

- Key Market Driver: Growing awareness of natural, low-calorie, and functional beverages is boosting demand.

- Growth Opportunity: Advancements in flavoured and infused variants, enabling expansion in cosmetics and pharmaceuticals for anti-aging and detox benefits.

| Key Insights | Details |

|---|---|

| Birch Water Market Size (2025E) | US$1.8 Bn |

| Market Value Forecast (2032F) | US$3.1 Bn |

| Projected Growth (CAGR 2025 to 2032) | 8.0% |

| Historical Market Growth (CAGR 2019 to 2024) | 7.5% |

Market Dynamics

Rising Health Consciousness and Demand for Natural Functional Beverages

The market is significantly driven by rising health consciousness and increasing demand for natural functional beverages. Consumers are increasingly aware of the link between diet and overall wellness, prompting a shift away from sugary sodas and artificially flavoured drinks toward natural, low-calorie alternatives. Birch water, rich in minerals, antioxidants, and electrolytes, is perceived as a clean, health-promoting beverage that supports hydration, detoxification, and general wellness. Its functional benefits resonate with fitness enthusiasts, urban professionals, and wellness-focused individuals seeking convenient ways to incorporate natural health solutions into their daily routines.

The trend is reinforced by a broader move toward plant-based, organic, and clean-label products. Consumers are scrutinizing ingredients and favouring beverages that offer measurable health benefits without synthetic additives. Birch water’s natural origin and minimal processing appeal to this segment, making it an attractive choice for both direct consumption and inclusion in wellness drinks, smoothies, and functional formulations.

Seasonal Availability and High Production Costs

Birch Water Market faces challenges due to seasonal availability and high production costs, which influence supply stability and pricing. Birch sap can only be harvested during a limited period in early spring, typically lasting a few weeks, depending on regional climate conditions. This short harvesting window restricts annual production volumes, making supply highly seasonal and subject to weather variability. Adverse weather events, such as unseasonably warm temperatures or frost, can significantly reduce sap yield, impacting both domestic and export markets.

High production costs further constrain market expansion. Sustainable tapping practices, which are essential to prevent long-term damage to birch trees, require skilled labour and careful monitoring, adding to operational expenses. Processing birch sap into a stable, packaged beverage involves refrigeration, filtration, and pasteurization, all of which are energy-intensive.

Expansion in Cosmetics and Pharmaceuticals with Infused Formulations

Expansion in cosmetics and pharmaceuticals, driven by the growing consumer preference for natural, functional ingredients. In the cosmetics sector, forest water is valued for its hydrating, antioxidant-rich, and skin-soothing properties. It is increasingly incorporated into skincare formulations such as facial mists, moisturizers, serums, and masks, often combined with botanical extracts or vitamins to enhance efficacy. The trend aligns with the rising demand for clean-label, eco-friendly, and organic personal care products, with consumers favouring natural alternatives over synthetic chemicals. This has prompted both established beauty brands and startups to launch birch water-infused premium product lines.

In pharmaceuticals and nutraceuticals, birch tree juice is gaining traction as an ingredient in functional supplements, particularly those targeting hydration, detoxification, and immune support. Its mineral and electrolyte profile makes it suitable for oral rehydration formulations, while its antioxidants are promoted in wellness supplements.

Category-wise Analysis

Product Type Insights

Unflavoured dominates the market, account 60% of the share in 2025. Its popularity stems from perceived purity, natural electrolyte content, and appeal to health-conscious consumers. Preferred by wellness enthusiasts and used extensively in direct hydration products, unflavoured sap water is positioned as a clean, natural alternative for functional hydration and detox-focused routines.

Flavoured is the fastest-growing segment, driven by consumer demand for improved taste and variety in functional beverages. Infusing sap water with fruits such as berries or citrus enhances flavor while retaining its health appeal, supporting premium product launches and accelerating adoption across retail and online consumer markets worldwide.

Application Insights

Beverages leads with 50% share, driven by the popularity of ready-to-drink formats and growing consumer interest in functional hydration products. Positioned as a natural detox and rehydration drink, forest water appeals to health-conscious consumers seeking clean-label, low-calorie alternatives to conventional soft drinks and sugary beverages.

Pharmaceuticals are the fastest-growing, driven by its integration into nutraceutical and functional supplement formulations. Rich in antioxidants, vitamins, and minerals, sap water is increasingly used in immune-support and detox products. This aligns with rising consumer preference for natural, science-backed health solutions promoting holistic wellness and disease prevention.

Distribution Channel Insights

B2C dominates the sector holds 55% share, driven by the growing popularity of online and retail channels that offer direct consumer access. Easy product availability through supermarkets, health stores, and e-commerce platforms, coupled with rising consumer awareness of natural wellness beverages, has strengthened B2C’s lead over other distribution models.

B2B is the fastest-growing, fueled by rising bulk demand from beverage producers and cosmetic formulators. Manufacturers are increasingly incorporating forest water into functional drinks, skincare, and wellness products for its hydrating and antioxidant properties, driving large-scale procurement and strengthening industrial partnerships across the health and beauty sectors.

Regional Insights

North America Birch Water Market Trends

North America accounts for 35% in 2025, driven by a strong wellness boom and rapid expansion of e-commerce platforms in the U.S. and Canada. Consumers in these countries are increasingly turning toward natural hydration and plant-based beverages, favouring organic and unflavoured birch water for its purity and detoxifying properties. The growing emphasis on clean labels, sustainable sourcing, and reduced sugar intake aligns perfectly with birch water’s positioning as a functional, low-calorie drink.

Major retailers and online health stores are expanding their offerings, enhancing accessibility and brand visibility. The U.K. market though part of Europe exhibits similar consumer behavior, marked by rising imports of sap water products and increasing popularity of detox and wellness routines, often influenced by NHS-endorsed hydration and sugar reduction campaigns. The collective shift across these markets toward healthier beverage choices and transparency in ingredients is reinforcing birch water’s status as a premium, natural alternative to conventional soft drinks and flavoured waters.

Europe Birch Water Market Trends

Europe holds about 30% market share, led by Germany and France emerging as key contributors. The region’s growth is largely supported by strict EU organic certification standards and a well-established consumer preference for clean-label, sustainably sourced products. European consumers are highly health-conscious, driving demand for natural hydration solutions such as forest water that align with organic and eco-friendly lifestyles.

The strong spa and wellness culture across Germany, France, and Nordic countries has further elevated birch water’s popularity, as it is often associated with detoxification, skin health, and natural rejuvenation. Birch water is increasingly featured in wellness resorts, spas, and organic retail outlets, promoted for its antioxidant and mineral-rich profile. Moreover, the presence of leading brands such as Sibberi, Sealand Birk, and TreeVitalise has strengthened regional market penetration.

Asia Pacific Birch Water Market Trends

Asia Pacific commands around 20% share and is the fastest-growing region, driven by rapid urbanization, rising disposable incomes, and expanding health tourism in countries such as China and India. The growing awareness of natural and functional beverages as healthier alternatives to sugary drinks is boosting birch water consumption among urban consumers. Increasing adoption of wellness lifestyles and preventive health habits, along with the influence of global fitness and detox trends, has accelerated market growth.

In India and China, the rise of wellness resorts, yoga retreats, and spa tourism has also created demand for premium hydration beverages such as birch water. Additionally, expanding e-commerce platforms and modern retail formats are improving accessibility and brand visibility. International brands are entering the region through partnerships with local distributors, while domestic players are introducing innovative flavours to cater to regional tastes.

Competitive Landscape

The global birch water market is highly competitive, with leading players striving to differentiate through sustainability, innovation, and wellness-driven offerings. Companies such as Sibberi, Treo Brands, Sealand Birk, and TreeVitalise are investing in ethical sourcing practices, tapping birch trees responsibly to ensure ecological balance and long-term resource availability. The competition is fueled by rising consumer preference for natural, low-calorie, and functional beverages as alternatives to sugary drinks.

To stand out, brands are expanding product portfolios with flavoured birch waters, sparkling versions, and formulations enriched with vitamins, antioxidants, or electrolytes. Marketing strategies emphasize purity, natural origin, and wellness benefits such as detoxification and hydration. Moreover, companies are adopting eco-friendly packaging and transparent labelling to appeal to environmentally conscious consumers. Digital marketing and e-commerce expansion have further intensified competition, enabling smaller brands to reach niche audiences globally.

Key Industry Developments:

- In July 2025, Sibberi expanded its product range by introducing a new line of flavored birch water infused with added vitamins. This move aligns with the growing consumer demand for natural, low-calorie beverages that offer functional benefits. The new flavored variants aim to provide the same hydrating and detoxifying properties as the original birch water, while offering enhanced taste profiles to appeal to a broader audience.

- In February 2023, Beauty brand LUMENE launched the Nordic Hydra Birch Dew Jelly, a skincare product featuring a unique formulation of organic Nordic birch sap, innovative moisture spheres, and triple hyaluronic acid for deep hydration. This serum-in-moisturizer is packaged in sustainable, recyclable Eastman Cristal One E Renew resin, which provides the brilliance and thickness of glass while incorporating 50% certified recycled content.

Companies Covered in Birch Water Market

- Sibberi

- BelSeva

- Treo Brands, LLC

- Birch Tree Water Co.

- Sealand Birk

- Sapp

- Nature on Tap

- DrinkBirk

- TreeVitalise

- Byarozavik

Frequently Asked Questions

The global birch water market is projected to reach US$1.8 Bn in 2025, driven by surging demand for natural, low-calorie functional beverages amid health trends.

Growing awareness of natural, low-calorie, and functional beverages is boosting demand.

The market is poised to witness a CAGR of 8.0% from 2025 to 2032, supported by innovations in flavoured variants and cosmetics applications.

Expansion in pharmaceuticals and cosmetics offers key opportunities, enabling birch water-infused products for anti-aging and detox benefits.

Key players include Sibberi, BelSeva, Treo Brands, Birch Tree Water Co., and Sealand Birk, leading through sustainable sourcing and premium formulations.