- Biotechnology

- Biosimulation Market

Biosimulation Market Size, Share, Growth, and Regional Forecast, 2026 to 2033

Biosimulation Market by Component (Software, Services), Application (Drug Development, Drug Discovery, Others), Deployment (Cloud-based, On-premise, Hybrid), End User, and Regional Analysis from 2026 to 2033

Biosimulation Market Share and Trends Analysis

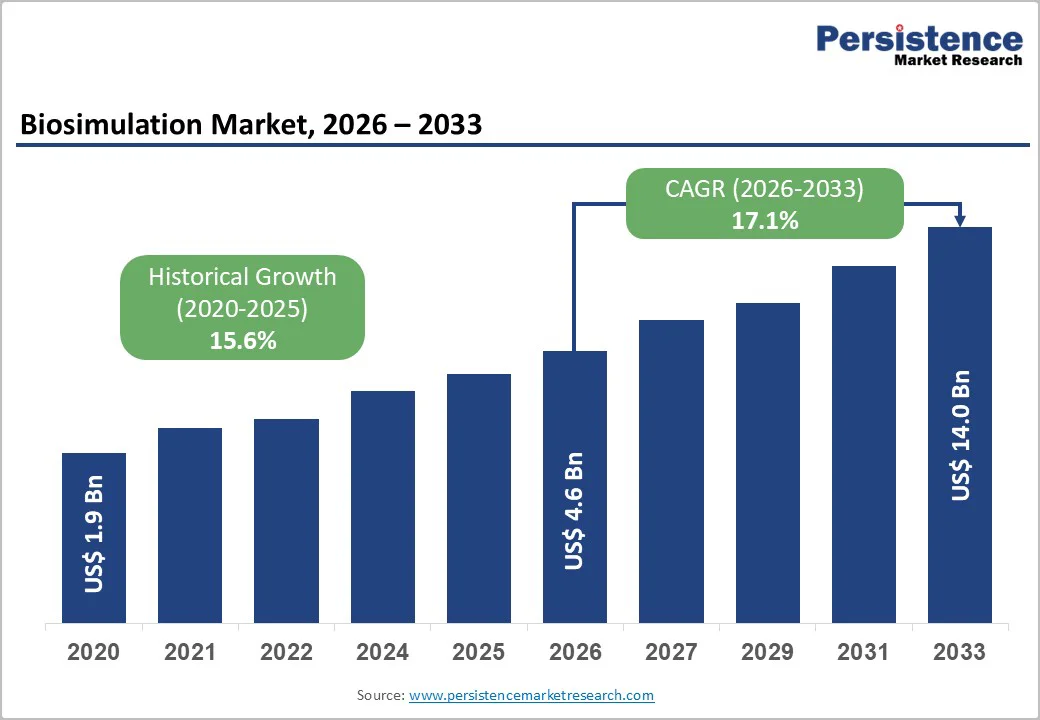

The global biosimulation market size is estimated to reach US$ 4.6 billion in 2026 and is projected to reach US$ 14.0 billion by 2033, growing at a CAGR of 17.1% between 2026 and 2033. Biosimulation uses computer-based models to replicate complex biological processes, enabling researchers to anticipate outcomes in drug discovery and development.

As drug development is expensive and late-stage failures lead to significant losses, predictive simulation tools have become essential for minimizing risk and optimizing decision-making.

By predicting the behavior of drug candidates, biosimulation helps in streamlining the R&D, reducing costly trial errors, and improving overall efficiency. Growing healthcare expenditure, continuous advancements in simulation software, and the adoption of sophisticated modelling technologies are further propelling the global biosimulation market.

Key Industry Highlights:

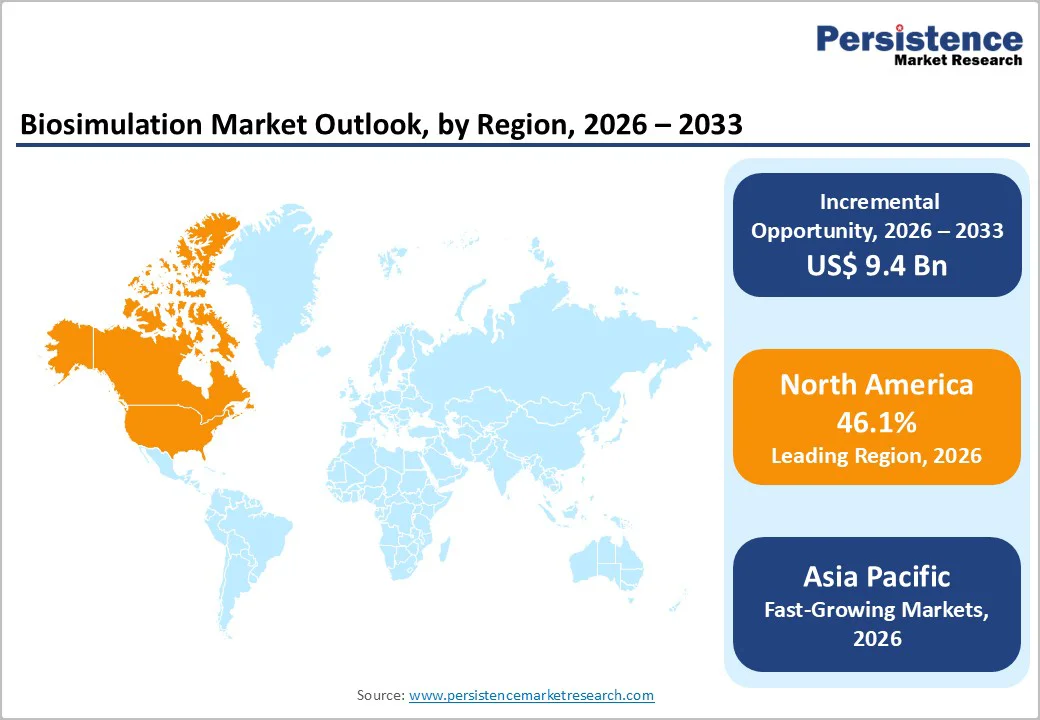

- Leading Region: North America dominates the global market with 46.1%, driven by advanced R&D infrastructure, early adoption of AI and simulation technologies, and strong regulatory support for model-informed drug development.

- Fastest-Growing Region: Asia Pacific market is expected to grow rapidly with a CAGR of 21.5% in forecast period, fueled by rising pharmaceutical R&D investments, government initiatives supporting digital health, and increasing adoption of computational modelling in clinical trials.

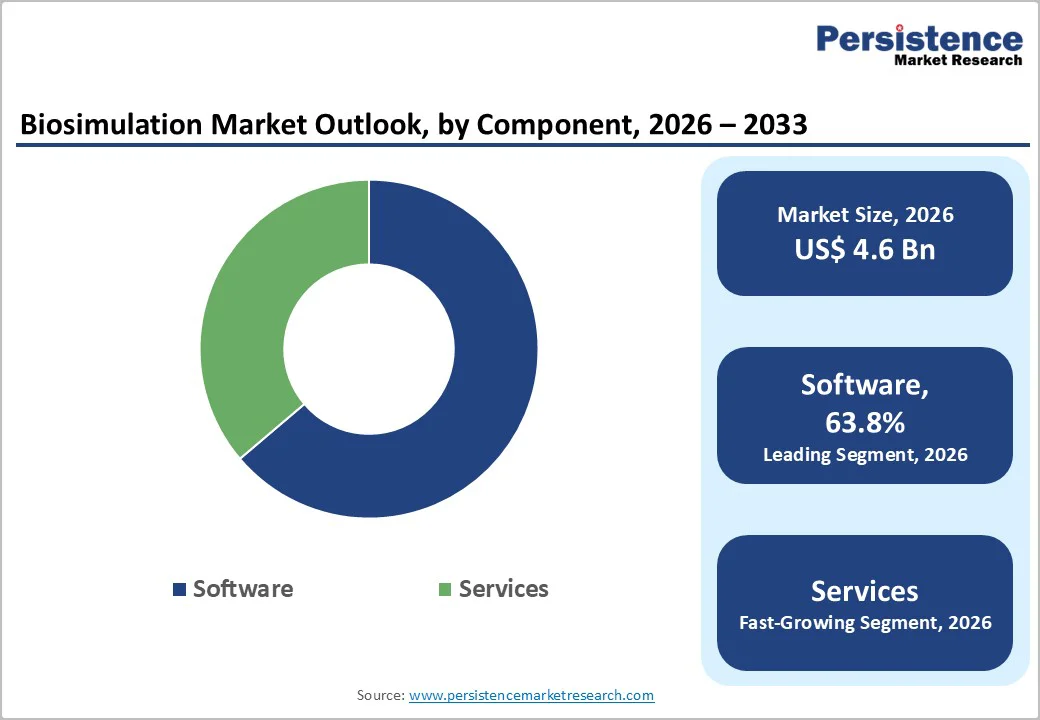

- Leading Component: Software lead with 63.8% share as it enables predictive modeling, virtual trials, and simulation of complex biological processes, which are essential for accelerating drug discovery and reducing trial risks.

- Leading Application: Drug development remains dominant with 59.1%, as biosimulation improves candidate selection, predicts efficacy and toxicity, and minimizes late-stage failures, optimizing overall development costs and timelines.

- Leading Deployment: Cloud-based lead with 41.6% share, due to scalability, remote collaboration, real-time data processing, and seamless integration with AI-driven modeling platforms for faster simulation outputs.

- Leading End User: Pharmaceutical and Biotech Companies with 43.8% share lead adoption because they benefit most from cost-effective predictive tools, accelerated development pipelines, and improved decision-making in complex therapeutics.

- Virtual patient models allow simulation of treatment responses and optimization of dosing, enhancing personalized therapy development.

- Partnerships between research institutes and pharma companies facilitate validation, innovation, and practical application of biosimulation in drug discovery.

| Key Insights | Details |

|---|---|

| Global Biosimulation Market Size (2026E) | US$ 4.6 Billion |

| Market Value Forecast (2033F) | US$ 14.0 Billion |

| Projected Growth (CAGR 2026 to 2033) | 17.1% |

| Historical Market Growth (CAGR 2020 to 2025) | 15.6% |

Market Dynamics

Driver - Growing Reliance on Model-Informed Drug Development to Reduce R&D Costs and Accelerate Clinical Decisions

Growing pressure to accelerate drug development for rare and complex diseases is strengthening global adoption of biosimulation. As traditional trials struggle with limited patient pools, model-informed approaches such as Quantitative Systems Pharmacology (QSP) and Physiologically Based Pharmacokinetic (PBPK) modelling enable researchers to optimize dosing, predict clinical outcomes, and design efficient protocols earlier in development.

Recent advancements-such as Certara’s 2025 launch of Certara IQ, an artificial intelligence (AI)-enabled QSP platform, and the European Medicines Agency’s (EMA) 2025 qualification of the Simcyp Simulator-are building regulatory confidence in biosimulation.

Parallel progress by companies such as Simulations Plus, including its 2023 ADMET (Absorption, Distribution, Metabolism, Excretion, and Toxicity) Predictor® artificial intelligence-driven drug design (AIDD) collaboration and its 2024 acquisition of Pro-ficiency to extend simulation-based training, reinforces the market’s technological momentum.

Growing interest in personalized and precision therapy is also driving demand for in silico disease modeling, synthetic control arms, digital twins, and patient-specific simulations that reduce reliance on large clinical cohorts.

Increasing use of computational biology to revive previously shelved therapeutic candidates, as seen with Cellworks’ 2023 expansion into precision drug development, further supports market growth. Collectively, these trends position biosimulation as a strategic enabler for faster, safer, and more cost-efficient R&D across modalities.

Restraints - Limited Access to High-Quality Data and Skilled Modeling Expertise Restricting Broad Biosimulation Adoption

Despite rapid progress, the adoption of biosimulation faces several practical and structural constraints. High-quality, consistently curated datasets remain difficult to obtain, particularly in rare diseases where patient registries are sparse and heterogeneity is high. Limited availability of standardized experimental datasets restricts the accuracy of PBPK, PK/PD (pharmacokinetic/pharmacodynamic), and disease-progression models.

While regulatory acceptance is improving-illustrated by the EMA’s 2025 qualification of the Simcyp Simulator-many regions still lack clear guidelines for model validation and submission. This introduces uncertainty for sponsors unfamiliar with model-informed regulatory pathways. Integrating artificial intelligence with biosimulation also requires advanced computational infrastructure and specialized expertise, which not all organizations possess.

Smaller biopharma companies often face budget limitations that restrict investment in biosimulation tools or computational biology teams. Data-sharing barriers further limit cross-institutional model refinement. Additionally, model complexity can slow adoption; QSP frameworks require extensive calibration against biological pathways and may take years to mature. These challenges collectively temper industry-wide uptake even as technological capability expands.

Opportunity - Expansion of AI-Integrated Biosimulation Platforms Enabling Personalized Therapies and Faster Regulatory Alignment

Biosimulation is entering a high-opportunity phase as drug developers increasingly turn to in silico strategies to address unmet needs in rare diseases, oncology, neurodegeneration, and complex biologics. The ability to generate synthetic control arms and model disease progression offers major value in indications with limited patient availability.

Collaborations such as the 2023 and 2025 Simulations Plus-IMB PAS artificial intelligence-driven drug design (AIDD) programs demonstrate how biosimulation can rapidly generate and validate ligand candidates for difficult targets.

Momentum is also expanding around digital-twin technologies, highlighted by Aitia’s 2024 and 2025 collaborations with Orion and Servier to simulate disease trajectories and uncover novel therapeutic targets across pancreatic cancer, Parkinson’s disease, glioma, and other conditions.

Regulatory advancements are also opening additional opportunities for model-based submissions in drug-drug interaction (DDI) assessments. The introduction of platforms like Certara IQ strengthens prospects for scaling QSP across discovery and development. As simulation-enabled clinical operations grow, biosimulation is poised to expand into training, commercialization, and lifecycle management, creating multi-stage opportunities for adoption.

Category-wise Analysis

By Component Insights

Software is expected to capture 63.8% of the global biosimulation market by 2026. Its dominance is driven by the ability to simulate complex biological processes, perform pharmacokinetic/pharmacodynamic (PK/PD) modeling, and integrate with AI and machine learning algorithms.

Software enables virtual trials, predictive toxicity assessment, and candidate selection, reducing reliance on costly experimental methods. Continuous upgrades in computational efficiency, real-time visualization, and cloud compatibility further support adoption. As a result, software solutions remain indispensable for pharmaceutical and biotechnology companies seeking faster, cost-effective, and precise drug discovery and development workflows.

By Application Insights

Drug development is projected to hold nearly 59.1% of the global biosimulation market in 2026. Biosimulation tools allow accurate prediction of efficacy, toxicity, and pharmacokinetic properties, minimizing late-stage failures. They support dose optimization, adaptive trial design, and simulation of disease progression, enhancing decision-making.

By reducing time, cost, and resources associated with traditional trials, biosimulation accelerates drug discovery timelines. The application is particularly critical for complex therapeutics, biologics, and rare diseases. Consequently, drug development remains the largest segment, leveraging computational insights to optimize candidate selection and ensure regulatory-compliant, efficient development pathways.

By Deployment: Cloud-Based Lead Owing to Scalability, Real-Time Collaboration, and Seamless Integration

Cloud-based deployment is estimated to account for nearly 41.6% of the global biosimulation market in 2026. It offers scalable infrastructure, enabling high-performance computational modeling without large upfront hardware costs. Cloud platforms facilitate real-time collaboration across geographically dispersed teams, enhance data sharing, and support integration with AI-driven predictive tools.

They also enable secure storage of large omics datasets and simulation outputs. The flexibility, accessibility, and cost-effectiveness of cloud-based solutions make them highly attractive for pharmaceutical and biotech companies seeking to accelerate drug discovery, improve predictive accuracy, and reduce R&D timelines in an increasingly digitalized research environment.

By End User: Pharmaceutical and Biotech Companies Lead Owing to Maximized R&D Efficiency and Predictive Insights

Pharmaceutical and biotech companies, with 43.8% market share, are expected to dominate globally in 2026. These organizations are primary adopters of biosimulation due to its ability to reduce development costs, optimize candidate selection, and enhance trial design. Biosimulation provides predictive insights into drug behavior, efficacy, toxicity, and disease progression, improving strategic decision-making.

Integration with AI, cloud infrastructure, and digital twins allows efficient R&D execution, enabling faster timelines and higher success probabilities. Consequently, pharmaceutical and biotechnology firms remain the largest end users, leveraging biosimulation to streamline complex drug discovery and accelerate market-ready therapeutic development.

Regional Insights

North America Biosimulation Market Trends

North America is projected to capture 46.1% of the global biosimulation market by 2026, due to early regulatory engagement, strong computational infrastructure, and rapid integration of model-informed drug development. The market continues to expand rapidly as life-science companies accelerate adoption of model-based approaches to shorten development timelines and improve regulatory predictability.

The region benefits from a dense ecosystem of pharma innovators, clinical research organizations (CROs), AI-modeling firms, and advanced cloud infrastructure that enables scalable simulation workflows. Growing pressure to reduce clinical trial attrition has also pushed R&D teams toward mechanistic PK/PD modeling, disease progression simulation, and virtual trial design.

Recent technology launches, such as Phoenix™ platform -based initiatives (Certara, 2023) integrating analytics with next-gen modeling engines, have strengthened the region’s leadership by offering faster computation, automated parameter optimization, and real-time visualization capabilities.

Regulatory bodies in the US have increasingly encouraged physiologically based modeling submissions, further validating biosimulation as a mainstream decision-support tool.

Rising investment in oncology, rare diseases, and biologics pipelines is also driving adoption of advanced computational toxicology, immune-response modeling, and digital twinning. With continuous industry-academia collaborations and sustained funding for predictive modeling research, North America remains the anchor region where biosimulation is transforming early discovery, candidate selection, and late-stage development strategies.

Europe Biosimulation Market Trends

Europe is projected to account for 215.6% of the global biosimulation market by 2026, reshaped by regulatory endorsement, academic partnerships, and strong public-funding support for digital innovation.

Europe’s biosimulation market is advancing through strong public-private collaboration, regulatory openness, and increased funding for computational science. The region has seen momentum across ADMET prediction, mechanistic modeling, and population-based simulations as companies seek more evidence-driven decision frameworks.

A key highlight is the July 2025 collaboration between Simulations Plus and the Institute of Medical Biology of the Polish Academy of Sciences, which successfully validated new ADMET prediction capabilities, strengthening Europe’s scientific foundation for early-stage modeling. Additionally, in August 2025, Certara received formal recognition from the European Medicines Agency, reinforcing biosimulation’s role in regulatory submissions and lifecycle management.

Start-ups are also contributing to innovation: Netabolics secured funding from the European Regional Development Fund (Pre-Seed Regione Lazio POR-FESR 2014-2020), enabling advancement of metabolism-focused simulation technologies.

Growth is further supported by Europe’s emphasis on ethical research, reducing animal testing, and digitalising clinical development. Expansion of precision medicine, AI-enhanced modeling platforms, and national investments in computational biology continue to position Europe as a high-value hub where biosimulation drives both scientific and regulatory progress.

Asia Pacific Biosimulation Market Trends

Asia Pacific is rapidly expanding, projected to achieve a CAGR of 21.5% over the forecast period. The market is expanding swiftly as pharmaceutical companies, biotech start-ups, and academic research centers embrace modeling-driven development to shorten time-to-market and lower R&D risks.

Governments across the region are investing heavily in computational biology, digital health infrastructure, and cloud-based simulation platforms, enabling broader adoption of virtual trials, QSP models, and in-silico toxicity prediction. Rising clinical trial activity in oncology, metabolic disorders, and infectious diseases has increased demand for predictive tools that optimize dosing, stratify patient populations, and design adaptive protocols.

Countries such as China, Japan, South Korea, Singapore, and India are building specialized biosimulation clusters supported by talent programs and technology grants. Local companies are integrating AI and machine-learning engines into PBPK frameworks, creating low-cost yet high-precision solutions tailored to regional clinical and genetic diversity.

The shift toward personalized medicine, combined with growing outsourcing to regional CROs, is further accelerating biosimulation uptake. With strong momentum in digital innovation and regulatory modernization, Asia Pacific is positioned to become a powerful contributor to global model-informed drug development.

Market Competitive Landscape

The biosimulation market features a mix of specialized platform providers, AI-driven drug modelling innovators, and integrated R&D solution firms competing to deliver faster, more accurate predictive insights.

Companies differentiate through advanced mechanistic models, regulatory-aligned PBPK/QSP capabilities, disease-specific digital twins, and end-to-end drug development support. Strategic collaborations, technology upgrades, and expanded therapeutic coverage shape the competitive environment.

Key Industry Developments:

- In September 2024, Cellworks reported that its computational biosimulation, combined with personalized tumor microenvironment modelling, accurately predicted immunotherapy responses in NSCLC patients beyond PD-L1 and TMB. Findings were presented at ESMO 2024, demonstrating strong potential for precision IO treatment planning.

- In August 2025, Certara received formal EMA qualification for its Simcyp Simulator, making it the first PBPK platform approved for EU regulatory submissions. The designation streamlines DDI assessments and eliminates the need for repeated platform credibility evaluations.

- In October 2025, Certara launched Certara IQ, an AI-enabled Quantitative Systems Pharmacology platform. The scalable solution integrates biosimulation and machine learning to enhance R&D productivity, improve complex therapy understanding, and reduce development risk across diverse therapeutic areas.

Companies Covered in Biosimulation Market

- Certara

- Simulations Plus

- Dassault Systèmes

- Schrödinger, Inc.

- Orion Corporation

- Cadence Design Systems, Inc.

- bilateralstimulation.io BLS GmbH

- Netabolics

- Cellworks Group Inc.

- Dante Labs Global

Frequently Asked Questions

The global biosimulation market is projected to be valued at US$ 4.6 Billion in 2026.

The need to reduce R&D costs, accelerate drug development, and improve predictive accuracy in complex therapeutics drive market growth.

The global market is poised to witness a CAGR of 17.1% between 2026 and 2033.

AI integration, cloud-based platforms, personalized medicine, rare disease modeling, and regulatory-accepted virtual trials present major growth opportunities.

Major players in the global are Certara, Simulations Plus, Dassault Systèmes, Schrödinger, Inc., Orion Corporation, and others.