- Medical Devices

- Biomedical Tester Market

Biomedical Tester Market Size, Share, and Growth Forecast 2026 - 2033

Biomedical Tester Market Size, Share by Test Type (Functionality Testing, Performance Testing, Verification Testing), Device Type (Biomedical Patient Monitor Simulators, Biomedical Infusion Pump Analyzer, Portable Biomedical Oscilloscopes, Biomedical Electrosurgery Analyzer, Biomedical Defibrillator Analyzer, Others Biomedical Tester Devices), End-user, and Regional Analysis, 2026 - 2033

Biomedical Tester Market Size and Trend Analysis

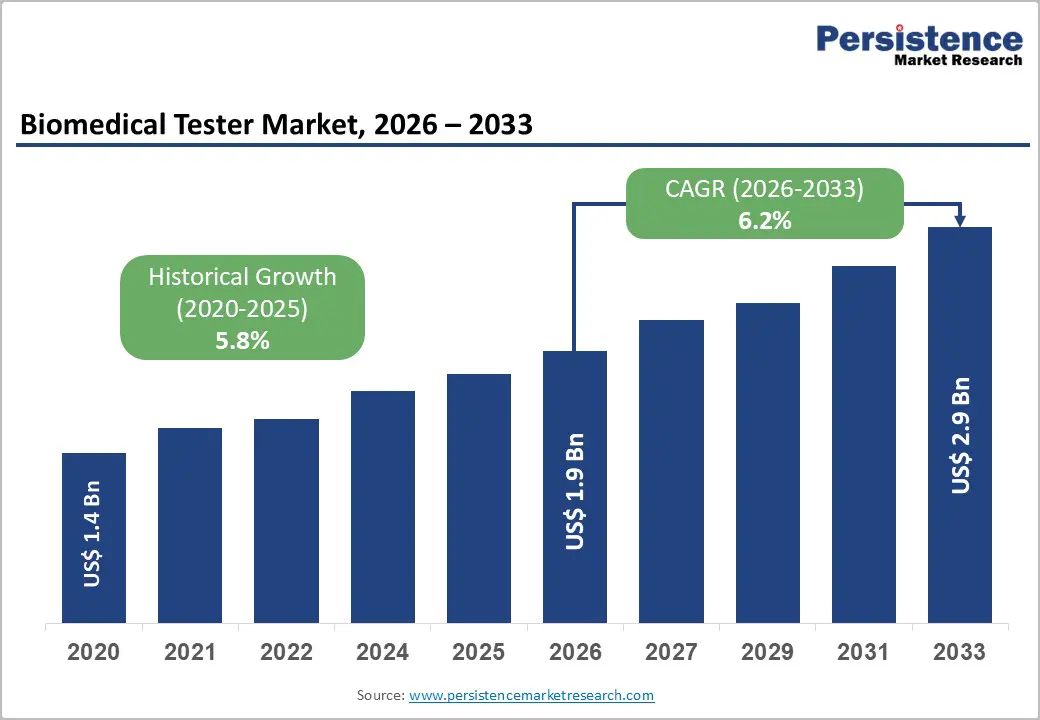

The global biomedical tester market is projected to reach US$ 1.9 billion in 2026 and US$ 2.9 billion by 2033, growing at a CAGR of 6.2% over the forecast period. This steady expansion is driven by rising demand for medical-device safety, regulatory compliance, and preventive maintenance across hospitals, clinics, and medical-device manufacturers.

Key Industry Highlights:

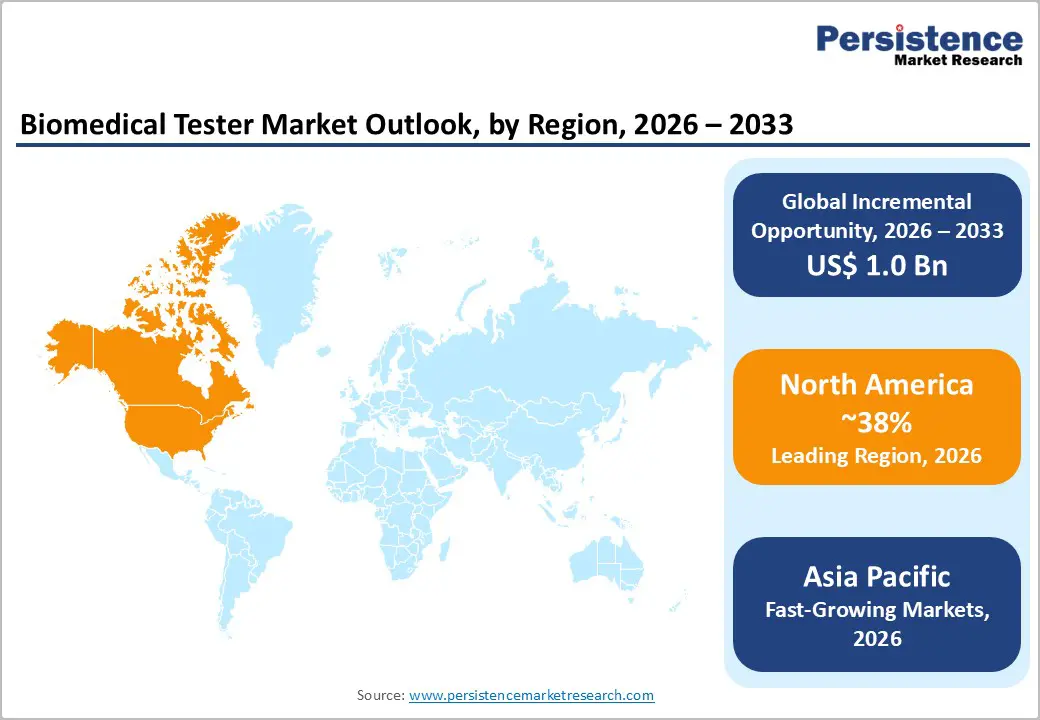

- Leading region: North America leads the biomedical tester market, accounting for 38% of the market, due to mature regulations, high technology adoption, and large-scale healthcare infrastructure and medical facilities.device programs.

- Fastest-growing region: Asia-Pacific is the fastest-growing region, with a CAGR of 8.1%, driven by rapid healthcare infrastructure expansion, medical device adoption, and government-backed modernization initiatives in China, India, and ASEAN countries.

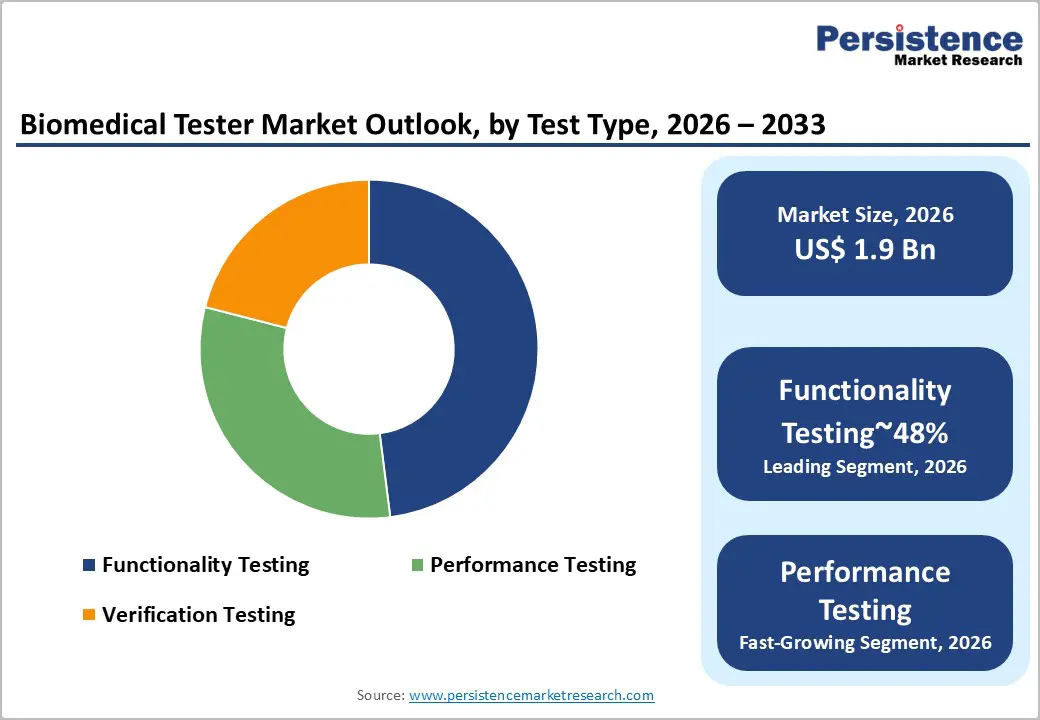

- Dominant Test Type: The functionality testing segment dominates, accounting for approximately 48% of the market, providing essential operational performance and safety compliance verification for medical devices.

- Fastest-growing Device Type: The biomedical patient monitor simulators segment is the fastest-growing, with share expanding toward 40% as patient-monitor testing, training, and calibration drive demand.

- Key market opportunity: The expansion of automated and software-driven biomedical-testing platforms presents a major opportunity, particularly in North America and Europe, where digital health initiatives and value-based-care models favor data-driven maintenance and predictive-testing strategies.

| Key Insights | Details |

|---|---|

|

Biomedical Tester Market Size (2026E) |

US$ 1.9 Billion |

|

Market Value Forecast (2033F) |

US$ 2.9 Billion |

|

Projected Growth CAGR (2026–2033) |

6.2% |

|

Historical Market Growth (2020–2025) |

5.8% |

Market Dynamics

Drivers - Rising Regulatory Pressure Driving Continuous Biomedical Testing Investments for Patient Safety and Compliance

Global regulatory authorities, such as the U.S. Food and Drug Administration (FDA), the European Medicines Agency (EMA), and the International Electrotechnical Commission (IEC), continue to strengthen safety and performance standards for medical devices. These stricter regulations are prompting hospitals and manufacturers to invest regularly in biomedical testing equipment. Standards such as IEC 60601-1 for medical electrical equipment and ISO 13485 for quality management systems require frequent testing of functionality, performance, and verification.

Critical devices, including patient monitors, infusion pumps, and defibrillators, must be tested to ensure compliance with regulatory requirements. In addition, healthcare accreditation organizations such as The Joint Commission (TJC) and Joint Commission International (JCI) mandate routine equipment inspections and documentation. This consistent regulatory oversight significantly increases demand for biomedical patient monitor simulators, infusion pump analyzers, and defibrillator analyzers. As patient safety becomes a global priority, healthcare facilities are increasingly adopting advanced testing solutions to ensure reliable device performance and minimize clinical risks.

Healthcare Infrastructure Expansion Increasing Demand for Medical Devices and Routine Biomedical Testing Services

The global healthcare industry is expanding rapidly, driven by rising patient populations, the prevalence of chronic diseases, and the growth in surgical procedures. Hospitals, diagnostic centers, and ambulatory facilities are continually adding advanced medical devices, including patient monitors, imaging systems, electrosurgical units, and infusion pumps. According to global health organizations, aging populations and growing healthcare access are accelerating the use of electronic medical equipment across regions. This widespread adoption necessitates regular calibration, safety verification, and performance testing.

In North America and Europe, large-scale hospital upgrades and digital health integration projects are boosting demand for preventive maintenance and testing services. Meanwhile, Asia-Pacific and Latin America are experiencing rapid hospital construction and increased medical-device imports. Together, these developments significantly increase the requirement for biomedical testers to ensure equipment reliability, regulatory compliance, and uninterrupted patient care across healthcare systems worldwide.

Restraints - High Cost of Advanced Biomedical Testing Equipment Limiting Adoption among Small and Budget-Constrained Healthcare Facilities

Biomedical testing equipment, particularly advanced patient monitor simulators, infusion pump analyzers, and electrosurgery analyzers, often involves a high upfront investment. Many of these devices cost several thousand dollars, making them difficult for small clinics, rural hospitals, and budget-constrained healthcare providers to afford. In low- and middle-income countries, healthcare budgets are typically focused on treatment equipment rather than preventive maintenance tools. This financial limitation slows the adoption of in-house biomedical testing solutions.

Operating these testers requires trained biomedical engineers and technical professionals, thereby increasing operational costs. Ongoing maintenance, calibration, and software updates also add to total ownership expenses. As a result, many smaller facilities prefer to outsource testing services rather than purchase equipment. These cost barriers continue to restrict widespread market penetration, especially in developing regions where healthcare funding remains constrained.

Legacy Medical Device Systems Creating Integration Challenges for Modern Automated Biomedical Testing Technologies

Many hospitals still operate older medical devices that use proprietary systems, outdated software, and non-standard communication protocols. Integrating modern biomedical testers with these legacy systems can be technically challenging and time-consuming. Several older patient monitors and infusion pumps lack digital connectivity, thereby complicating automated testing, data collection, and report generation. This increases the manual workload and increases the risk of human error during inspections. The need for specialized training to operate complex testing platforms further complicates adoption.

Cybersecurity concerns related to connecting testing equipment with hospital networks and electronic health records add regulatory and technical hurdles. Healthcare providers must ensure data protection and compliance with digital security standards. These integration difficulties often delay the deployment of advanced biomedical testing systems, particularly in hospitals with large legacy device inventories and strict regulatory environments.

Opportunity - Automated Software-Driven Biomedical Testing Platforms Enhancing Compliance Efficiency, Accuracy, and Predictive Maintenance Capabilities

The market is increasingly shifting toward automated, software-enabled biomedical testing solutions that combine hardware devices with cloud-based platforms and intelligent analytics. These advanced systems help healthcare providers reduce manual work, improve accuracy, and standardize testing procedures across multiple facilities. Automated platforms can generate real-time compliance reports, performance trends, and audit-ready documentation, thereby facilitating regulatory inspections. Leading manufacturers such as Fluke Biomedical and Datrend Systems have launched integrated testing solutions that support predictive maintenance and remote monitoring.

These tools allow hospitals to identify potential device issues before failures occur, improving uptime and patient safety. Digital transformation in healthcare, especially in North America and Europe, strongly supports the adoption of these platforms. As healthcare systems increasingly focus on efficiency, data transparency, and cost optimization, automated biomedical testing solutions present a major growth opportunity for technology providers.

Emerging Market Healthcare Modernization Expanding Demand for Biomedical Testing Equipment and Service-Based Maintenance Models

Emerging markets across Asia Pacific, Latin America, and Africa are rapidly modernizing healthcare infrastructure and expanding hospital networks. Governments and international organizations are investing heavily in the procurement of medical equipment and in facility upgrades, often including maintenance and testing programs. Countries such as India, Brazil, and South Africa are establishing dedicated biomedical engineering departments and regional testing centers to improve equipment safety and compliance.

This shift encourages the use of portable biomedical analyzers, including defibrillator, infusion pump, and electrosurgery analyzers. Many healthcare providers in these regions prefer service-based testing models, creating new opportunities for outsourced maintenance providers. As regulatory frameworks continue to strengthen, demand for routine biomedical testing is expected to grow significantly. These developments offer strong market expansion potential for manufacturers and service companies targeting underserved healthcare markets.

Category-wise Analysis

Test Type Insights

The functionality testing segment is projected to lead at 48% of the overall market share in 2026. This dominance reflects its essential role in confirming that medical devices perform correctly under both normal and stress conditions. Functionality testing ensures that patient monitors, infusion pumps, defibrillators, and electrosurgical units respond accurately to alarms, signals, and user controls. These checks are critical for patient safety and regulatory compliance. Hospitals and medical-device manufacturers include functionality testing as a core part of routine quality assurance and preventive maintenance programs. Industry data shows that this testing type is the most frequently performed due to its wide application across multiple device categories. Its ability to quickly identify performance issues before clinical failure makes it indispensable. As healthcare systems prioritize safety and uptime, functional testing remains the foundation of biomedical testing operations.

Device Type Insights

Biomedical patient monitor simulators account for the largest share in the device type segment, at nearly 40% in 2026. These devices are widely used to test, calibrate, and train healthcare professionals on patient monitoring systems. They accurately simulate vital signs, including heart rate, blood pressure, oxygen saturation, and ECG signals. This allows technicians to verify monitor performance without involving real patients.

Hospitals, emergency departments, operating rooms, and intensive care units rely heavily on these simulators for routine inspections and compliance audits. Medical-device manufacturers also use them during product development and validation processes. High usage frequency, strict regulatory requirements, and increased focus on clinical training continue to support strong demand. As patient monitoring becomes more advanced and widespread, the importance of reliable simulation tools further strengthens this segment’s market leadership.

End-user Insights

The healthcare sector is the largest end-user segment, accounting for approximately 45% of total market demand for biomedical testers. Hospitals, clinics, and diagnostic centers depend on these tools to conduct routine safety checks, performance testing, and preventive maintenance of critical medical equipment. Devices such as patient monitors, infusion pumps, defibrillators, and surgical systems require frequent testing to ensure reliable operation and regulatory compliance. Healthcare institutions face increasing pressure from accreditation bodies and regulatory agencies to maintain strict safety standards.

Rising patient volumes, growing surgical procedures, and the widespread use of electronic medical devices further increase testing requirements. Many hospitals are also expanding in-house biomedical engineering teams to improve equipment reliability. As healthcare providers focus on improving patient outcomes and minimizing downtime, demand for biomedical testing solutions continues to grow steadily.

Regional Insights

North America Biomedical Tester Market Trends

North America remains the largest and most technologically advanced market for biomedical testers, led primarily by the United States. The region benefits from strong regulatory frameworks enforced by the FDA, The Joint Commission, and international safety standards. Hospitals and manufacturers are required to conduct routine equipment testing and documentation to maintain compliance and accreditation. Healthcare providers in the U.S. are early adopters of automated and software-driven testing platforms that integrate cloud analytics and predictive maintenance tools.

These systems improve efficiency and reduce operational risks. Major industry players such as Fluke Biomedical, Datrend Systems, and NETECH Corporation are headquartered in the region, driving continuous innovation and product development. High healthcare spending, advanced infrastructure, and strong focus on patient safety continue to support steady market growth across North America.

Europe Biomedical Tester Market Trends

Europe shows strong and consistent demand for biomedical testing solutions aligned with strict regulatory requirements. Countries such as Germany, the United Kingdom, France, and Spain lead adoption due to advanced healthcare infrastructure and regulatory enforcement. The European Union’s Medical Device Regulation (MDR) and In Vitro Diagnostic Regulation (IVDR) require extensive safety and performance testing throughout the device lifecycle. Hospitals across the region are expanding biomedical engineering departments to meet compliance needs.

German and UK healthcare systems are early users of patient monitor simulators and infusion pump analyzers, while Southern European countries are rapidly strengthening testing programs. Harmonized EN ISO standards support cross-border regulatory alignment and consistent testing practices. As regulatory oversight continues to tighten, European healthcare providers increasingly rely on high-quality biomedical testers to ensure safety, operational efficiency, and uninterrupted patient care.

Asia Pacific Biomedical Tester Market Trends

Asia-Pacific is the fastest-growing regional market for biomedical testers, driven by rapid healthcare expansion and rising adoption of medical devices. Countries such as China, India, Japan, and Southeast Asian nations are investing heavily in hospital construction and healthcare modernization programs. Increased imports of advanced medical equipment are driving strong demand for safety testing and calibration tools. China and India are experiencing particularly high growth, driven by expanding healthcare access and government funding initiatives.

Japan is adopting sophisticated testing technologies to support its aging population and advanced clinical systems. ASEAN countries are strengthening biomedical testing services for public healthcare projects and medical tourism development. Cost-efficient manufacturing and improving logistics also support regional market growth. Together, these factors position the Asia Pacific as a major long-term growth engine for biomedical tester manufacturers.

Competitive Landscape

The biomedical tester market is moderately consolidated, featuring a mix of global medical technology leaders, specialized testing equipment manufacturers, and regional service providers. Major players such as Fluke Biomedical, Datrend Systems, Seaward Electronic, NETECH Corporation, Illinois Tool Works, and Pre-sto Group hold strong positions through advanced product portfolios and global distribution networks. These companies focus on integrated hardware-software solutions, automated testing platforms, and compliance-ready reporting tools. Smaller firms compete by offering cost-effective products, localized services, and niche regulatory expertise. Strategic partnerships with hospitals and medical-device manufacturers are increasingly common. The market is also witnessing consolidation through mergers and acquisitions as companies aim to expand capabilities and geographic reach. Overall, innovation, digital integration, and customer-specific solutions continue to shape competitive dynamics and long-term market growth.

Key Developments:

- In October 2025, Fluke Biomedical launched an advanced patient-monitor simulator with AI-driven analytics and cloud-based reporting capabilities that improve testing accuracy, automated data logging, and compliance documentation for hospitals and medical-device manufacturers in North America and Europe.

- In June 2024: Datrend Systems Inc. introduced a portable biomedical oscilloscope featuring wireless connectivity and real-time monitoring to support field technicians in on-site testing of patient-monitoring systems and electrosurgical units, enabling remote diagnostics and predictive maintenance.

- In March 2024, NETECH CORPORATION expanded biomedical-testing services across the Asia Pacific through partnerships with hospitals and device manufacturers in India, China, and ASEAN countries, delivering calibration, safety testing, and performance verification solutions tailored to regulatory compliance needs.

Companies Covered in Biomedical Tester Market

- Fluke Biomedical

- Datrend Systems Inc.

- Seaward Electronic Ltd.

- Southeastern Biomedical

- Dynatech CBET

- Response Biomedical Corp.

- BDC Laboratories

- NETECH CORPORATION

- Illinois Tool Works Inc.

- Presto Group

- Rigel Medical

- Gossen Metrawatt GmbH

- BC Group International

- TSI Incorporated

- iSimulate

Frequently Asked Questions

The biomedical Tester Market is projected to reach US$ 2.9 Billion by 2033, growing at a CAGR of 6.2% from 2026, driven by rising regulatory pressure, patient‑safety requirements, and healthcare‑infrastructure expansion.

Key demand drivers include rising regulatory pressure, patient‑safety requirements, expansion of healthcare infrastructure, and increasing adoption of advanced medical devices, which push hospitals and manufacturers toward routine biomedical‑testing and preventive maintenance.

The Functionality Testing segment dominates, capturing around 48% of the market by providing essential operational‑performance and safety‑compliance verification for medical devices.

North America leads the global Biomedical Tester Market, supported by mature regulations, high technology adoption, and large‑scale healthcare‑infrastructure and medical‑device programs.

A key opportunity lies in automated and software‑driven biomedical‑testing platforms, particularly in North America and Europe, where digital‑health initiatives and value‑based‑care models favor data‑driven maintenance and predictive‑testing strategies.

Major players include Fluke Biomedical, Datrend Systems Inc., Seaward Electronic Ltd., Southeastern Biomedical, Dynatech CBET, Response Biomedical Corp., BDC Laboratories, NETECH CORPORATION, Illinois Tool Works Inc., and Presto Group, among others.