- Processed Food

- Beet Pulp Market

Beet Pulp Market Size, Share, and Growth Forecast 2026 - 2033

Beet Pulp Market by Pulp Type (Wet beet pulp, Dried beet pulp, Beet pulp pellets), by Category (Molassed beet pulp, Non-molassed beet pulp), Application (Animal feed, Pet food, Bioenergy & others), and Regional Analysis, 2026 - 2033

Beet Pulp Market Share and Trends Analysis

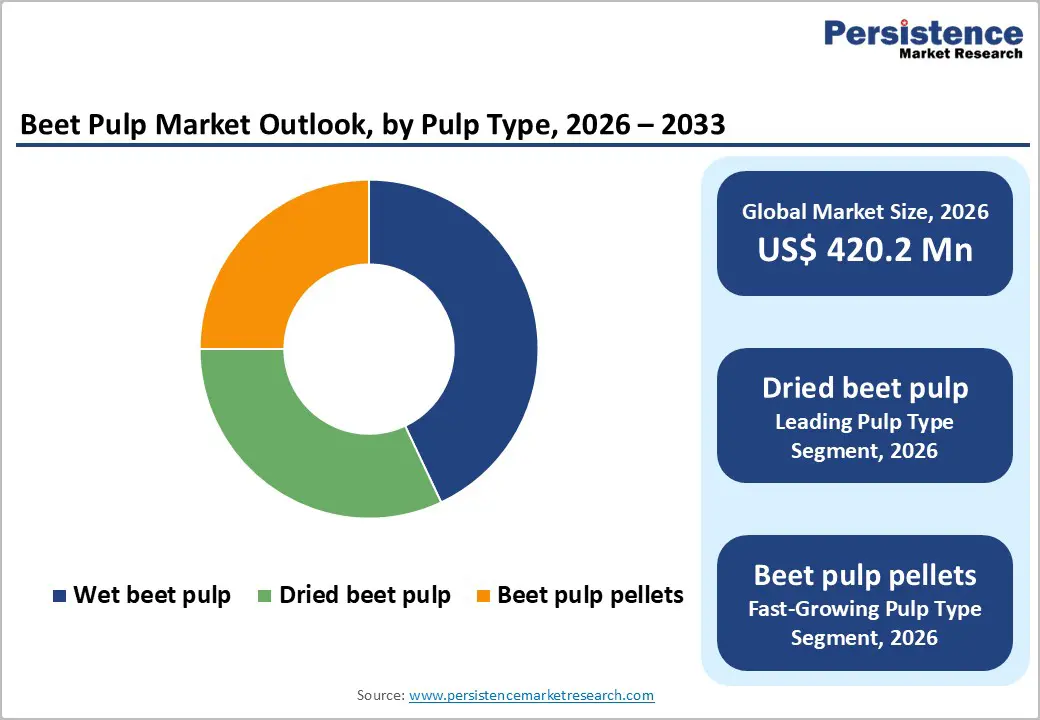

The global beet pulp market size is expected to be valued at US$ 420.2 million in 2026 and projected to reach US$ 712.4 million by 2033, growing at a CAGR of 7.8% between 2026 and 2033.

Growth in the beet pulp market is primarily driven by the intensification of the global livestock sector and rising demand for high-fiber, cost-effective feed ingredients in dairy, beef, and equine nutrition. As per FAO assessments, global meat production has increased steadily over the last decade, while world milk output is projected to continue expanding, requiring consistent supplies of fibrous co-products to balance rations and support rumen health.

Beet pulp, a co-product of sugar beet processing, is valued for its highly digestible fiber, moderate energy, and low starch profile, which improves feed efficiency and animal performance compared with many traditional forages. In parallel, sugar beet cultivation areas in Europe and North America remain extensive and well-organized through cooperatives and large processors, ensuring stable raw material availability and enabling long-term beet pulp supply integration into compound feed and pet food value chains.

Key Industry Highlights:

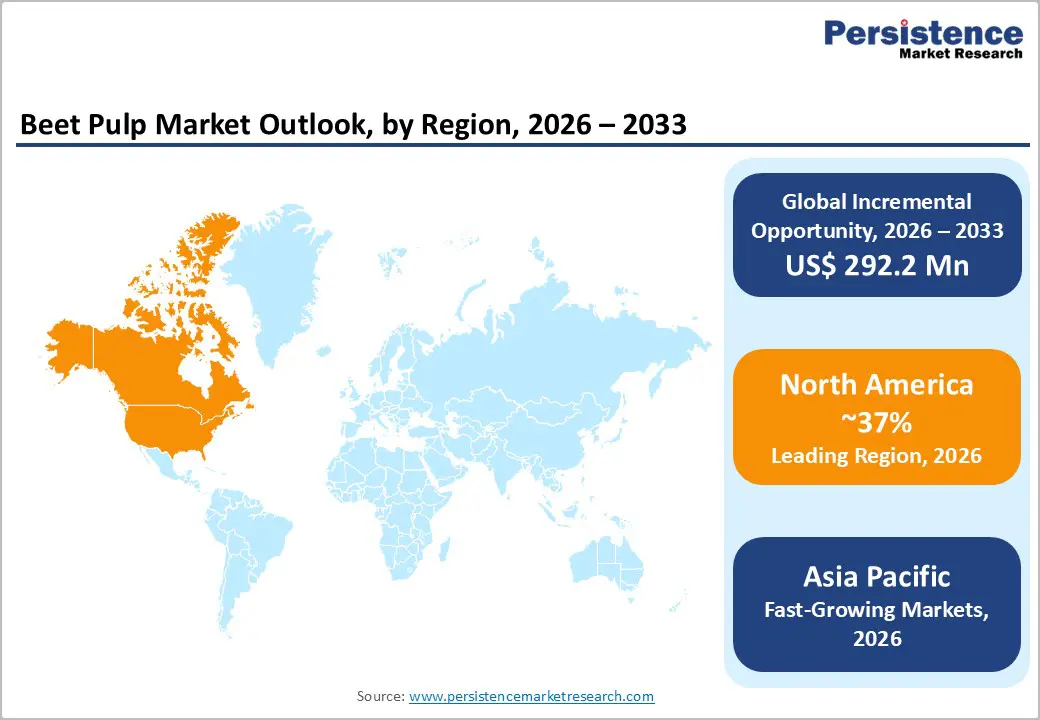

- Leading Region: North America commands around 37% share of the beet pulp market in 2025, supported by substantial sugar beet cultivation, integrated processing by companies such as American Crystal Sugar Company and Amalgamated Sugar, strong dairy and beef sectors, and robust feed and pet food industries.

- Fastest-growing Region: Asia Pacific is the fastest-growing market, driven by dairy and meat sector expansion in China, India, and ASEAN regions, rising demand for imported fiber-rich feed ingredients, and rapid growth in premium pet food consumption as incomes and urbanization increase.

- Dominant Product Segment: Dried beet pulp leads the pulp type category with approximately 43% share in 2025, owing to its long shelf life, ease of storage and transport, suitability for pelleting, and high acceptance among compound feed manufacturers globally.

- Fastest-Growing Product Segment: Beet pulp pellets are the fastest-growing pulp type segment, benefiting from higher bulk density, reduced transport costs, and strong adoption in international feed trade, particularly for supplying dairy and beef operations in regions without local sugar beet processing.

- Sustainability and Circular Economy as Key Opportunity: Positioning beet pulp as a circular, low-waste co-product of sugar beet processing with potential roles in both animal feed and bioenergy creates a compelling opportunity for processors and traders to align with corporate sustainability goals and differentiate against alternative feed ingredients.

| Key Insights | Details |

|---|---|

| Beet Pulp Market Size (2026E) | US$ 420.2 million |

| Market Value Forecast (2033F) | US$ 712.4 million |

| Projected Growth CAGR (2026 - 2033) | 7.8% |

| Historical Market Growth (2020 -2025) | 7.6% |

Market Dynamics

Drivers - Rising Global Livestock Production and Demand for Functional Fiber-Rich Feeds

Expansion of the global livestock and dairy industries is a fundamental growth driver for the beet pulp market, as producers increasingly rely on functional fiber sources to optimize productivity. According to FAO data, world milk production has surpassed 900 million tonnes and is forecast to continue growing as demand for dairy products rises in developing regions. Beet pulp, with its high level of fermentable fiber and relatively low lignin content, supports rumen function, improves milk fat percentage, and reduces the risk of acidosis when replacing part of cereal grains in dairy rations. In intensive beef and sheep operations, beet pulp is used to enhance diet digestibility and maintain gut health, particularly in high-concentrate feeding systems. Additionally, increasing awareness of animal welfare and the role of fiber in digestive health is encouraging feed formulators to use ingredients such as beet pulp in balanced rations for cattle, small ruminants, and horses, thereby contributing to sustained demand from the feed industry.

Growing Use of Beet Pulp in Pet Food and Specialty Animal Nutrition

The rapid premiumization of pet food and the shift towards fiber-balanced, digestive-health-focused formulations have opened new demand pockets for beet pulp. Pet food manufacturers frequently use beet pulp as a moderately fermentable fiber source that supports beneficial gut microbiota, improves stool quality, and moderates glycemic response, which is important in managing obesity and digestive sensitivities in dogs and cats. Industry associations and veterinary nutrition bodies recognize the value of controlled fermentable fiber in complete pet diets, and beet pulp has become a standard component in many mid- to high-range dry pet foods. With global pet ownership rising-particularly in North America, Europe, and emerging markets in Asia Pacific-and with pet owners increasingly viewing pets as family members, spending on premium, functional pet food is growing steadily, thereby strengthening the structural demand for beet pulp as an established, science-backed fiber ingredient in this segment.

Restraints - Dependence on Sugar Beet Processing Volumes and Crop Volatility

A key restraint for the beet pulp market is its intrinsic dependence on sugar beet processing volumes, which are influenced by agricultural, climatic, and policy-related factors. Fluctuations in sugar beet acreage due to crop rotation requirements, price volatility in the global sugar market, and changes in government support schemes in major producing regions such as the European Union and United States can directly impact beet pulp output. Adverse weather conditions-such as droughts or excessive rainfall-can reduce beet yields and sugar recovery, consequently limiting the volume of pulp generated as a co-product. In years of tight supply, beet pulp prices may rise, making it less competitive versus alternative fibrous feeds like soy hulls or citrus pulp, which can restrain its usage in cost-sensitive feed formulations.

Competition from Alternative Co-Products and Regional Logistics Constraints

The beet pulp market also faces competition from other agro-industrial co-products and logistical challenges that can limit its penetration in certain regions. Ingredients such as soy hulls, corn gluten feed, wheat bran, and citrus pulp provide comparable fiber and energy values and may be more readily available or economical in areas without sugar beet processing capacity. Moreover, the bulky nature of wet beet pulp and the cost of drying or pelleting increase the importance of transport economics; markets located far from sugar beet factories may find imported fibrous co-products cheaper or more practical than beet pulp. Storage stability and moisture management are additional concerns for wet pulp, necessitating appropriate infrastructure and handling practices at the farm and feed mill level. These logistical and competitive factors can limit market growth in regions with limited or no sugar beet industry presence.

Opportunity - Expansion of Beet Pulp Pellets and Value-Added Formats in Global Trade

Rising demand for stable, easy-to-handle feed ingredients in export markets creates a significant opportunity for beet pulp pellets and other dried formats. Pelleting improves bulk density, reduces transport costs per unit of digestible fiber, and enhances shelf life, making beet pulp more attractive for long-distance shipping and year-round use by compound feed producers. As international trade in feed ingredients grows, particularly towards Asia Pacific and Middle East & Africa where livestock sectors are expanding but local fiber co-products are limited, dried beet pulp and pellets can gain share in import flows. Technological improvements in drying and pelleting processes at large beet processors in Europe and North America support higher throughput and consistent quality, while adherence to international feed safety standards (such as GMP+ and FAMI-QS) enhances customer confidence. This positions beet pulp pellets as the fastest-growing pulp type segment, supported by both logistical advantages and strong integration into global dairy and beef feed supply chains.

Leveraging Beet Pulp in Bioenergy, Circular Economy, and Sustainability Narratives

The move towards circular bioeconomy models and sustainable feedstock utilization offers another opportunity for beet pulp market participants. Sugar beet processing already exemplifies high resource efficiency, with beets converted into sugar, molasses, bioethanol, and animal feed; promoting beet pulp as a low-waste, low-carbon co-product aligns with national and corporate sustainability goals in agriculture and food systems. In some regions, beet pulp and other sugar factory by-products are being evaluated or used in biogas production and bioenergy applications, providing additional outlets and strengthening the overall business case for beet-based value chains. Feed buyers and retailers increasingly demand transparency and sustainable sourcing; highlighting beet pulp’s origin as a co-product from established sugar industries, often backed by certification schemes and environmental reporting from companies such as Tereos Group, Südzucker AG, and Nordzucker AG, can differentiate it from alternative feed ingredients with higher land-use or carbon footprints. Over time, this sustainability positioning could support premiumization or preferential inclusion of beet pulp in procurement strategies of large integrated dairy and meat companies.

Category-wise Analysis

Pulp Type Insights

Dried beet pulp is the leading pulp type segment, accounting for about 43% of global market share in 2025, supported by its superior storage stability, tradeability, and compatibility with industrial feed manufacturing. Drying reduces moisture content substantially, lowering the risk of spoilage and enabling longer storage periods compared with wet pulp. This is particularly important for large dairy and beef operations and feed mills that require predictable year-round supplies and cannot rely solely on the sugar beet processing season. Dried pulp can be used as shreds or further processed into beet pulp pellets; both forms are easily incorporated into compound feeds and total mixed rations. Industry analyses indicate that dried and pelleted pulp formats account for the majority of beet pulp exports from key producing regions such as Europe and North America, underscoring their central role in international feed trade. The combination of stable quality, global logistical suitability, and the ability to blend seamlessly into commercial feed formulations explains the sustained leadership of dried beet pulp in the product mix.

Category Insights

Molassed beet pulp is the leading category segment and can reasonably be estimated to hold around 60% share in 2025, given its widespread use and functional benefits in ruminant and equine diets. The addition of sugar beet molasses increases the energy density of the pulp and substantially improves palatability, encouraging consistent feed intake in dairy cows, beef cattle, and horses. Molassed formats provide a balanced combination of digestible fiber and readily fermentable carbohydrates, which helps stabilize rumen fermentation and performance, particularly when forage quality is variable or when diets include high proportions of low-sugar forages. Dairy producers commonly rely on molassed beet pulp for its positive effect on milk yield and milk fat percentage, while equine nutrition programs use it as a safer energy source compared with high-starch cereals. The functional and sensory advantages, combined with the convenience of receiving a single co-product containing both fiber and sugar, justify the dominant position of molassed beet pulp within the overall category mix. Non-molassed beet pulp remains important where lower sugar levels are required or where molasses is added separately at the feed mill.

Application Insights

Animal feed is the leading end-use application and can be considered to account for roughly 70% of total beet pulp utilization in 2025, reflecting its core role in ruminant and equine feeding. Beet pulp is particularly valued in dairy cow rations, where it supports rumen function, improves fiber digestibility, and can enhance milk fat and overall production when used as part of balanced diets. Beef cattle, sheep, and goat producers also use beet pulp as a partial forage or grain replacer, especially in intensive and semi-intensive systems. Pet food is the fastest-growing application segment, supported by the expansion of premium, health-oriented formulas that use beet pulp as a controlled, moderately fermentable fiber source to support gastrointestinal health and stool quality in companion animals. As global pet ownership rises and owners increasingly demand science-based, functional nutrition, the inclusion of beet pulp in dry dog and cat foods continues to expand. Bioenergy and other uses, including biogas production and specialized industrial applications, represent smaller but emerging outlets that can add incremental demand and support a more diversified utilization profile for beet pulp over the long term.

Regional Insights

North America Beet Pulp Market Trends and Insights

North America holds a leading share of around 37% in the global beet pulp market in 2025, anchored by its large sugar beet processing industry and intensive livestock sector. The United States is among the world’s major sugar beet producers, with significant cultivation in states such as Minnesota, North Dakota, Michigan, and Idaho, supplying factories operated by companies such as American Crystal Sugar Company, Amalgamated Sugar, and Michigan Sugar Company. These processors generate substantial volumes of beet pulp, much of which is dried or pelleted and marketed as feed ingredients for dairy and beef operations, particularly in the Upper Midwest and Western regions where cattle densities are high. Robust infrastructure, strong cooperative structures, and established feed distribution networks help ensure that beet pulp is firmly integrated into regional feed markets.

Regulatory frameworks in North America, including feed safety oversight by agencies such as the U.S. Food and Drug Administration (FDA) and compliance with standards from the Association of American Feed Control Officials (AAFCO), support high-quality and traceable feed ingredient supply chains, enhancing buyer confidence. Innovation in ruminant nutrition, driven by universities and industry research, continues to validate the role of beet pulp in ration formulation for production efficiency and animal welfare. In addition, growing pet ownership and the mature pet food manufacturing base in the United States and Canada underpin rising demand for beet pulp in companion animal diets. Taken together, these factors ensure that North America remains a structurally important production and consumption hub for beet pulp, with stable domestic demand and export potential.

Asia Pacific Beet Pulp Market Trends and Insights

Asia Pacific is the fastest-growing regional segment of the beet pulp market, supported by rapid expansion of livestock and pet populations, rising incomes, and strengthening feed manufacturing capacity. Countries such as China and India are experiencing sustained growth in dairy and meat production, with national policies aimed at improving productivity per animal and modernizing feed practices. While sugar beet cultivation in the Asia Pacific is more concentrated and smaller in scale compared with Europe or North America, domestic production in countries such as China and Japan contributes to regional supply, and imports of dried beet pulp and pellets from Europe and North America are increasing as compound feed manufacturers seek reliable fiber sources. The development of organized dairy value chains, particularly in India and China, is creating greater awareness of the nutritional and economic benefits of incorporating beet pulp into ruminant rations.

Additionally, the region’s fast-growing pet food market, especially in China, Japan, and urban centers across ASEAN, is driving demand for high-quality functional ingredients such as beet pulp, which support digestive health claims in premium pet food brands. Manufacturing cost advantages in certain Asia Pacific countries also open opportunities for local processors and international companies to establish blending, packaging, or distribution operations targeting regional customers. Nonetheless, growth is influenced by trade policies, currency fluctuations, and competition from locally available co-products. As logistics and cold-chain infrastructure improve and industry consolidation progresses, Asia Pacific’s share of global beet pulp consumption is expected to rise steadily over the forecast period, making it a critical growth engine for market participants.

Competitive Landscape

The beet pulp market shows a moderately consolidated competitive landscape, shaped by strong integration with the sugar processing industry. Competition is primarily based on product quality, consistency, pricing, and supply reliability. Players focus on optimizing drying and pelleting processes to improve shelf life, ease of transportation, and nutritional value. Pelletized and dried formats dominate due to better handling and export suitability. Sustainability initiatives, including waste valorization and energy-efficient processing, are increasingly influencing competitive positioning. Market participants also compete through long-term supply contracts with feed manufacturers, regional distribution strength, and customized formulations for different livestock applications, while international trade dynamics and raw material availability continue to shape competition.

Key Developments

- In June 2024, Tereos Group announced investments to modernize and expand beet processing and drying capacity at selected European plants, improving energy efficiency and increasing availability of high-quality dried beet pulp and pellets for export and regional feed customers.

Companies Covered in Beet Pulp Market

- Tereos Group

- Südzucker AG

- Nordzucker AG

- American Crystal Sugar Company

- Amalgamated Sugar, Michigan Sugar Company

- British Sugar plc, Cosun Beet Company

- Pfeifer & Langen GmbH & Co. KG

- Cargill, Inc.

- Louis Dreyfus Company

- Associated British Foods plc

- Midwest Agri-Commodities

- Ontario Dehy Inc.

- Nippon Beet Sugar Manufacturing Co., Ltd.

Frequently Asked Questions

The global beet pulp market is expected to reach about US$ 420.2 million in 2026, supported by robust demand from dairy, beef, and equine feed sectors and expanding use in pet food and export-oriented pellet formats.

Key demand drivers include growth in global livestock and dairy production, the need for digestible fiber sources that support rumen health and feed efficiency, and increasing use of beet pulp in pet food formulations focused on digestive health and stool quality.

North America leads the market, benefiting from substantial sugar beet cultivation, strong processing capacity, high livestock densities, and mature feed and pet food industries that incorporate beet pulp as a standard ingredient in ruminant and companion animal nutrition.

Expanding value-added dried and pelleted beet pulp formats for international trade, leveraging sustainability and circular economy narratives, and targeting fast-growing livestock and pet food markets in Asia Pacific and Middle East & Africa.

Key players include sugar beet processors and agribusiness companies such as Tereos Group, Südzucker AG, Nordzucker AG, American Crystal Sugar Company, Amalgamated Sugar, Michigan Sugar Company, British Sugar plc, Cosun Beet Company, Pfeifer & Langen GmbH & Co. KG, Cargill, Inc., Louis Dreyfus Company, and Associated British Foods plc, among others.