- Smart Packaging

- ASEAN Cling Film Market

ASEAN Cling Film Market Size, Share, and Growth Forecast, 2026 - 2033

ASEAN Cling Film Market By Material (Polyethylene (PE), Polyvinyl Chloride (PVC), Others), Thickness (Up to 9 microns, 9 to 12 microns, Others), End-user, and Country Analysis for 2026 - 2033

ASEAN Cling Film Market Size and Trends Analysis

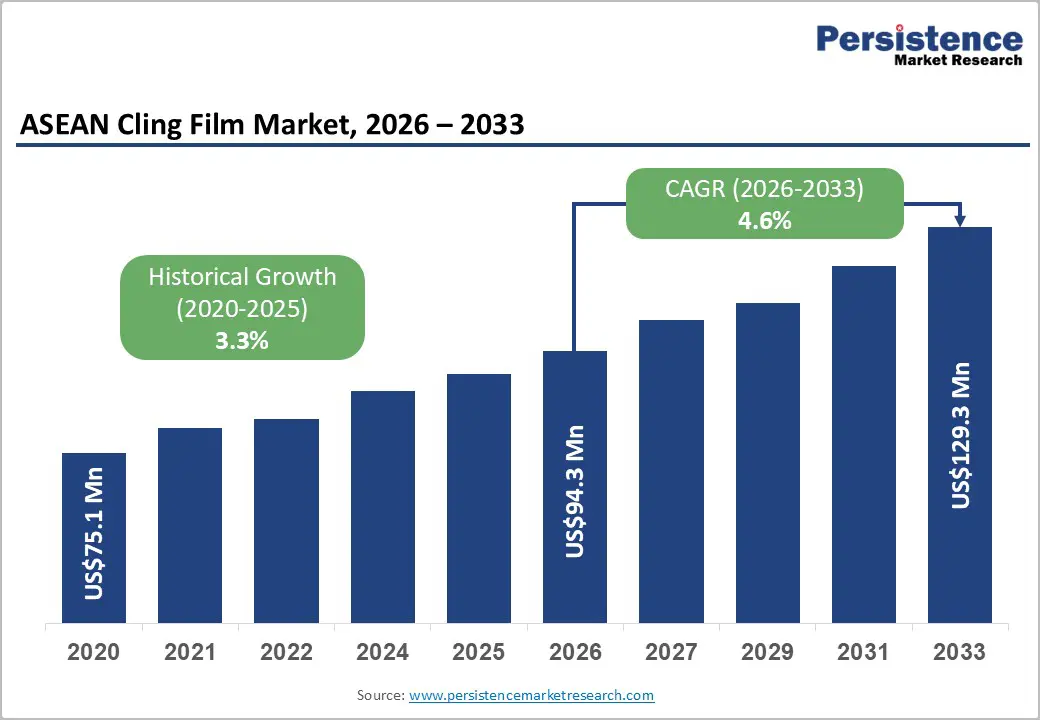

The ASEAN cling film market size is likely to be valued at approximately US$94.2 million in 2026 and is expected to reach around US$129.8 million by 2033, growing at a CAGR of 4.6% during the forecast period from 2026 to 2033, driven by rising demand for food freshness preservation packaging in tropical climates and the rapid expansion of modern retail and online grocery channels, the market supports a wide range of food, beverage, and household packaging applications.

Cling films play a critical role in maintaining hygiene, reducing spoilage, and enhancing shelf presentation, particularly in warm and humid conditions prevalent across Southeast Asia. The market is shaped by growing consumption of packaged and ready-to-eat foods, alongside increasing reliance on ultra-thin polyethylene films that balance performance with material efficiency.

Key Industry Highlights

- Leading Region: Indonesia is projected to account for 30.6% of market share, supported by its large food-processing base, high fresh-food consumption, and strong penetration of modern retail and household food-storage applications.

- Investment Plans: Leading regional converters are actively investing in ultra-thin polyethylene cling film production lines and high-clarity food-grade films, with capacity expansions focused on Indonesia, Vietnam, and Thailand to support modern retail, foodservice, and e-commerce packaging demand.

- Dominant Material: Polyethylene (PE) remains the leading material segment, projected to hold 67.2% market share, owing to its flexibility, food safety compatibility, and strong performance in humid tropical conditions.

- Leading End-user: The food industry segment is expected to account for 53.6% of market share, supported by high consumption of fresh produce, ready-to-eat meals, and retail food packaging requiring consistent freshness retention and hygiene control.

| Key Insights | Details |

|---|---|

| ASEAN Cling Film Market Size (2026E) | US$94.3 Mn |

| Market Value Forecast (2033F) | US$129.3 Mn |

| Projected Growth (CAGR 2026 to 2033) | 4.6% |

| Historical Market Growth (CAGR 2020 to 2025) | 3.3% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Demand for High-Performance Cling Film in Humid ASEAN Climates to Preserve Food Freshness

The persistent risk of food spoilage in tropical ASEAN climates continues to drive demand for high-performance cling film solutions. Elevated temperature and humidity levels across Southeast Asia accelerate moisture loss and microbial activity in fresh produce, meat, and ready-to-cook foods, increasing reliance on food freshness preservation packaging, high-barrier cling film for humid environments, and ultra-thin polyethylene cling films below 9 microns. These films deliver tighter seal integrity and oxygen control while reducing material consumption, aligning with cost-sensitive retail operations. In wet markets and semi-organized grocery formats, cling film remains a primary tool for minimizing shrinkage and extending shelf visibility. For instance, fresh produce retailers in Thailand increasingly use micron-optimized PE cling films to reduce daily spoilage losses in open refrigerated displays.

Modern retail expansion and the penetration of packaged food are reshaping cling film performance requirements across ASEAN. Rapid growth in organized supermarket chains, online grocery fulfillment, and ready-to-eat meal packaging has accelerated the adoption of high-clarity, recyclable polyethylene cling films that meet hygiene, transparency, and sustainability benchmarks. Food processors and retailers now favor films that balance recyclable food contact compliance, visual appeal, and consistent wrapping efficiency at scale. This shift is particularly visible in Indonesia and Vietnam, where private-label fresh and prepared foods rely on advanced PE cling films to maintain product aesthetics during last-mile delivery. As a result, cling film demand is increasingly driven by performance-led specifications rather than price-only procurement.

Volatile Polyethylene Resin Supply and Shifting Food Storage Habits Affect Cling Film Consistency

Volatility in polyethylene resin availability for food-grade cling film production continues to influence supply consistency across ASEAN. Regional converters depend heavily on imported polymer feedstock, making micron-specific cling film manufacturing vulnerable to uneven resin allocation and sudden formulation changes. This instability affects output planning for ultra-thin cling films used in fresh-food packaging, where precise material characteristics are critical to seal performance. Inconsistent resin flow often leads to short production runs and fluctuating film quality, limiting manufacturers' ability to meet rising demand from modern retail and foodservice channels at scale.

Shifts in food storage behavior are also reshaping demand patterns for traditional household cling film applications. Urban consumers and premium food brands increasingly explore reusable food wrapping alternatives, vacuum-sealed packaging solutions, and portion-controlled containers that offer longer preservation without frequent material replacement. These substitutes reduce the frequency of repeat purchases of cling film, particularly in organized retail and online grocery segments, where sustainability narratives influence buying decisions. As a result, growth in cling film usage becomes more application-specific, with slower uptake in the household and premium retail segments compared with institutional foodservice.

Ultra-Thin, High-Transparency Cling Film and E-Commerce Packaging Drive Market Growth in ASEAN

Rising demand for ultra-thin polyethylene cling films below 9 microns opens a strong pathway for product differentiation in the ASEAN cling film market. Food retailers and processors are increasingly seeking high-clarity, low-fog food wrapping films that preserve visual appeal while reducing material usage, particularly for fresh produce and ready-to-eat meals. This creates scope for manufacturers to develop performance-enhanced cling films for humid climates that deliver stronger seal integrity and longer freshness retention. Targeted innovation in anti-condensation and microwave-safe film formats can support premium positioning in modern retail. For example, several ASEAN-based converters have recently expanded their portfolios with thinner, high-transparency PE cling films tailored for supermarket fresh food counters.

The rapid expansion of online grocery platforms and cloud kitchen ecosystems across Southeast Asia presents another growth avenue for e-commerce-ready cling film packaging solutions. Food delivery operators increasingly require durable cling wraps for last-mile transport that maintain hygiene and moisture control during handling and transit. This shift creates an opportunity for specialized foodservice-grade cling films with enhanced tear resistance and wrap consistency, supporting high-volume usage in centralized kitchens. As digital food retail scales across Indonesia, Vietnam, and the Philippines, cling film suppliers that align products with delivery-centric packaging needs can secure long-term supply contracts and recurring demand.

Category-wise Analysis

Material Insights

The polyethylene (PE) segment is expected to be the largest material segment in the ASEAN cling film market and is expected to account for around 67.2% of the market share. Its leadership is driven by a strong balance of flexibility, food safety, and sealing performance, which aligns well with high-volume food packaging needs across the region. PE cling films adapt easily to irregular food shapes, provide reliable moisture retention, and perform consistently in hot and humid climates common across ASEAN countries. These characteristics make PE the preferred choice for fresh produce, cooked foods, and household storage applications. For example, supermarkets across Indonesia and Malaysia widely use PE cling film to wrap fruits, vegetables, and prepared meals due to its dependable cling and ease of handling.

Polyvinyl Chloride (PVC) is projected to be the fastest-growing material segment, supported by its superior durability, stretchability, and visual clarity in food packaging applications. PVC cling films offer a tighter seal and stronger puncture resistance than many alternatives, making them suitable for high-value and moisture-rich foods such as fresh meat, seafood, and deli products. Retailers and food processors value PVC films for their ability to maintain product presentation and extend shelf life under refrigeration. In premium fresh food counters and butcher sections across Thailand and Vietnam, PVC cling films are increasingly used to improve shelf appearance and reduce spoilage, supporting faster adoption despite their smaller overall market share.

End-user Insights

The food industry is expected to be the largest end-user segment, accounting for approximately 53.6% of the ASEAN cling film market. This dominance reflects the essential role cling film plays in food preservation, hygiene control, and freshness retention across retail, foodservice, and household channels. Rising consumption of packaged and ready-to-eat foods, combined with the need to limit food waste in warm climates, continues to reinforce the use of cling film in food applications. Its ability to prevent contamination and moisture loss makes it indispensable for fresh produce, bakery items, and prepared meals. For instance, large supermarket chains in Thailand routinely use cling film to seal cut fruit packs and ready meals, maintaining quality throughout the retail cycle.

The beverages segment is likely to be the fastest-growing end-user category, largely driven by the rapid expansion of online grocery platforms and home delivery services. Ready-to-drink beverages, such as fresh juices, cold brews, and health drinks, increasingly require secondary packaging to prevent leakage and condensation during transit. Cling films designed for secure sealing and moisture resistance are gaining traction in beverage packaging workflows, particularly for short-distance and last-mile delivery. In markets such as Vietnam and the Philippines, beverage retailers use cling film to secure cup lids and bottle packs for delivery orders, supporting faster growth in this segment compared to traditional retail channels.

Country-Wise Insights

Indonesia remains the largest market in ASEAN, accounting for roughly 30.6% of total regional demand. This leadership reflects rapid urbanization, a growing middle class, and extensive food processing activity, all of which boost consumption of cling films for fresh produce, ready meals, and foodservice packaging. Cling film plays an essential role in preserving moisture and preventing spoilage in Indonesia’s tropical climate, especially for wet markets and grocery retail. The country’s large consumer base also supports the penetration of cling film in households and the increasing use of ultra-thin PE wraps for everyday food storage and small-format convenience. With modern retail and e-commerce grocery channels expanding, cling film adoption is extending into logistics and last-mile packaging workflows.

Competitive Landscape

The ASEAN cling film market is shaped by a mix of regional polymer film converters and multinational packaging players competing on product performance, supply reliability, and distribution reach. Leading manufacturers prioritize developing high-clarity polyethylene (PE) and performance-enhanced PVC cling films to meet diverse customer needs across the fresh food retail, foodservice, and e-commerce segments. Competitive differentiation increasingly revolves around material innovation, such as ultra-thin and anti-fog film variants, and strategic partnerships with supermarket chains and quick commerce platforms to secure bulk supply agreements. Regional converters in Indonesia, Thailand, and Vietnam leverage local production capabilities to respond rapidly to market shifts and minimize dependence on imports, while global players bring advanced film technologies and broader supply networks.

Market competition also reflects value-chain integration and service-based positioning, with firms expanding beyond basic film rolls to offer customized packaging solutions and technical support for automated wrapping systems in industrial and retail settings. Companies that can deliver consistent quality, scale production efficiently, and align with sustainability and freshness performance criteria tend to command stronger commercial traction. For example, leading suppliers that collaborate with modern retail groups to co-develop cling films tailored for fresh produce displays or online grocery packaging gain preferential placement and recurring volume commitments.

Key Industry Developments

- In January 2025, Berry Global released a new line of cling films designed for medical and health applications, offering enhanced hygiene, compatibility with sterilization, and improved barrier properties for healthcare packaging, indicating diversification of cling film product portfolios beyond traditional food wrap use.

Companies Covered in ASEAN Cling Film Market

- Berry ASEAN Group, Inc.

- Intertape Polymer Group (IPG)

- Gruppo Fabbri Vignola S.p.A

- Kalan SAS

- Fine Vantage Limited

- Wrapmaster

- Klöckner Pentaplast

- Prowrap Group (Wrapex)

- AEP Industries Inc.

- Anchor Packaging Inc.

- Polyvinyl Films Inc.

Frequently Asked Questions

The ASEAN cling film market size is estimated at US$94.3 million in 2026.

The ASEAN cling film market is expected to reach US$129.3 million by 2033.

Key trends include the adoption of ultra-thin polyethylene (PE) cling films, high-clarity films for fresh produce and ready-to-eat meals, rising demand from e-commerce and online grocery delivery, and growing interest in sustainable and performance-enhanced cling films for foodservice and retail applications.

The polyethylene (PE) material segment is the largest, expected to hold 67.2% share.

The ASEAN cling film market is projected to grow at a CAGR of 4.6% from 2026 to 2033.

Major players include Berry Global Inc., Intertape Polymer Group (IPG), Gruppo Fabbri Vignola S.p.A., Kalan SAS, and Fine Vantage Limited.