- Advanced Materials

- Aramid Fiber Market

Aramid Fiber Market Size, Share, and Growth Forecast, 2026 - 2033

Aramid Fiber Market by Product Type (Para-Aramid Fibers, Meta-Aramid Fibers, Others), Application (Tire Reinforcement, Protective Apparel, Optical Fibers, Electrical Insulation), End-User (Automotive, Aerospace & Defense, Electronics & Communication), and Regional Analysis for 2026-2033

Aramid Fiber Market Share and Trends Analysis

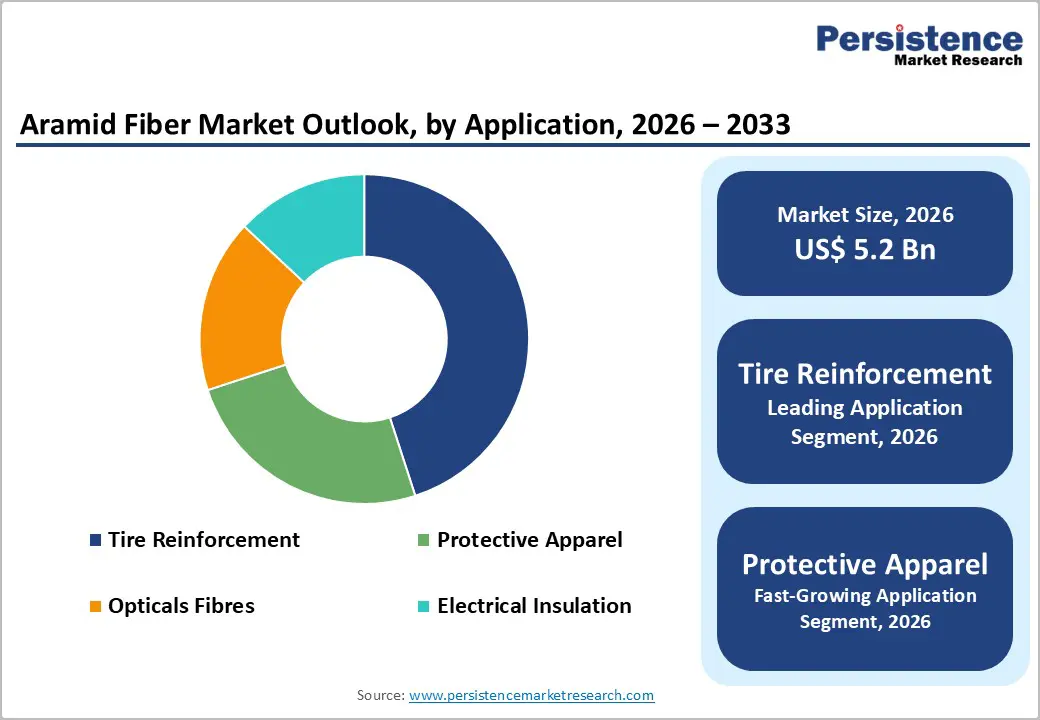

The global aramid fiber market size is likely to be valued at US$ 5.2 billion in 2026, and is projected to reach US$ 10.0 billion by 2033, growing at a CAGR of 8.5% during the forecast period 2026−2033.

This expansion is being supported by sustained demand from aerospace and defense industries, where aramid fibers are valued for their high strength-to-weight ratio and thermal stability. Aircraft manufacturers are incorporating aramid-reinforced composites into structural panels, interior components, and ballistic protection systems to reduce overall weight while maintaining structural integrity. Defense agencies are continuing to procure advanced body armor, helmets, and vehicle protection systems that rely on aramid materials for impact resistance and durability. As global defense budgets remain elevated and commercial aviation production gradually increases, demand for high-performance reinforcement materials is strengthening.

The automotive sector is also contributing significantly to growth, as manufacturers pursue lightweight designs to improve fuel efficiency and extend electric vehicle range. Aramid fibers are being integrated into tire reinforcement, brake pads, transmission belts, and structural composites to enhance durability and reduce mass. At the same time, tightening workplace safety regulations are expanding usage in flame-resistant clothing, protective gloves, and industrial safety equipment. Telecommunications infrastructure development in emerging economies is further driving demand for aramid reinforcement in fiber optic cables, where tensile strength and flexibility are critical for long-distance installations.

Key Industry Highlights

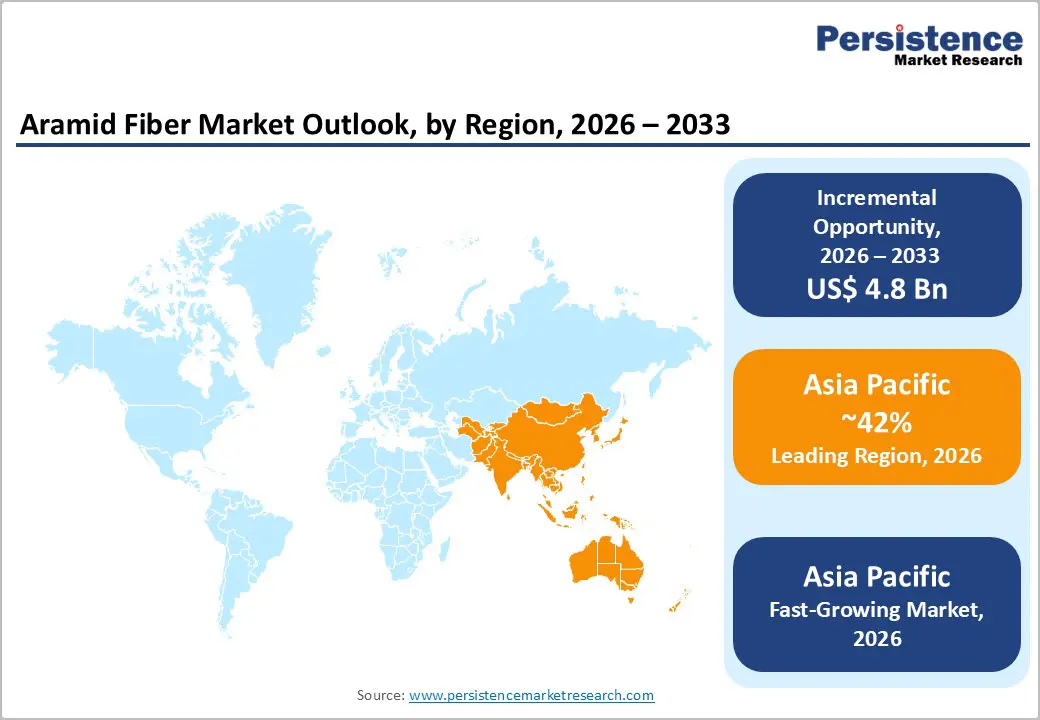

- Regional Dynamics: Asia Pacific is set to dominate by holding approximately 42% of the market share in 2026, propelled by robust industrial expansion across China and India.

- Product Leadership: Para-aramid fibers are slated to lead with an estimated 2026 share of 68%, whereas meta-aramid fibers are likely to be the fastest-growing during the 2026-2033 forecast period.

- Application Dominance: Tire reinforcement is poised to hold an estimated 32% revenue share in 2026, while protective apparel is slated to exhibit the highest 2026-2033 CAGR.

- November 2025: Teijin Aramid launched Twaron Next, a high-strength para-aramid fiber available in two sustainable variants, with one using reclaimed production waste and another made with bio-based feedstock.

| Key Insights | Details |

|---|---|

| Aramid Fiber Market Size (2026E) | US$ 5.2 Bn |

| Market Value Forecast (2033F) | US$ 10.0 Bn |

| Projected Growth (CAGR 2026 to 2033) | 8.5% |

| Historical Market Growth (CAGR 2020 to 2025) | 4% |

Market Factors – Growth, Barriers, and Opportunity Analysis

Aerospace and Defense Modernization Initiatives

Military organizations worldwide ramp up budgets to bolster operational strength and readiness. This expansion directly fuels demand for Aramid Fibers in essential equipment, including ballistic armor, helmets, and aircraft components. The United States (U.S.) Department of Defense pushes forward with modernization initiatives that depend on these advanced materials to deliver superior protection and reliability. Sector leaders gain value by treating this shift as a clear indicator. They should adjust supply chains to match escalating procurement volumes and pursue alliances that lock in enduring agreements. Forward-thinking firms also assess how to integrate next-generation fiber blends for even greater resilience.

Commercial aerospace companies such as Boeing and Airbus elevate composite material adoption in cutting-edge aircraft, such as the 787 Dreamliner and A350. Aramid Fibers reinforce critical areas like fuselage panels, wing assemblies, and cabin structures. The International Air Transport Association (IATA) anticipates robust expansion in passenger volumes and fleet additions through 2030. Producers secure competitive advantages by focusing on fiber advancements that reduce mass and enhance longevity. Decision-makers position themselves for success through targeted investments in high-capacity manufacturing. They further stand out by adopting eco-friendly procurement methods that meet tightening sustainability standards across global markets. Capital Intensity and Fleet Infrastructure Investment.

Environmental Concerns and Sustainability Pressures

Aramid fiber production creates notable environmental challenges through energy-heavy methods and chemical byproducts that demand careful handling. The European Union (EU) enforces strict rules under the Registration, Evaluation, Authorization and Restriction of Chemicals (REACH) framework. These measures target solvents and emissions in manufacturing. Producers face higher operational expenses to meet such standards. End-users benefit from the material's inherent toughness, yet this same quality hinders breakdown at the end of product life. Recycling efforts lag behind other composites, as the European Composites Industry Association notes limited progress in waste recovery systems.

Corporate pledges to sustainability intensify pressure on suppliers across sectors such as automotive and consumer products. Firms pursue circular economy goals that favor reusable materials and reduced waste. Alternative options, including carbon fiber and bio-based composites, encroach on traditional aramid applications. Research centers advance greener fiber solutions to address these gaps. Leaders position their operations for long-term viability by investing early in low-impact production techniques. They also explore hybrid blends that balance performance with recyclability. Strategic partnerships with innovators help manufacturers comply with evolving mandates while capturing emerging market segments.

5G Infrastructure Deployment and Telecommunications Expansion

The global expansion of fifth-generation (5G) networks opens substantial prospects for Aramid Fibers in reinforcing fiber optic cables and building robust telecommunications systems. Operators worldwide invest heavily to deploy these advanced infrastructures. Aramid materials deliver critical tensile support, especially in demanding setups such as submarine links that span continents. Projects such as the Pakistan and East Africa Connecting Europe (PEACE) Cable System highlight this reliance on strengthened designs for reliable connectivity. Network providers secure performance advantages by selecting fibers that endure extreme tension and environmental stresses over long distances.

Emerging economies such as India, Indonesia, and Brazil are accelerating their digital transformations with ambitious infrastructure plans. The International Telecommunication Union (ITU) anticipates rapid growth in mobile broadband access, which fuels needs for extensive cable networks. Suppliers gain a competitive foothold by tailoring aramid solutions to these high-volume deployments. Businesses can advance their strategies through early engagement with regional telecom leaders, and prioritizing scalable production and customized reinforcements that align with local deployment challenges. Firms can also integrate smart monitoring features into fibers to enhance network uptime and future-proof investments against evolving tech demands.

Category-wise Analysis

Product Type Insights

Para-aramid fibers are slated to maintain a dominant position in the market, with an estimated 2026 revenue share exceeding 68%, due to their superior strength-to-weight ratio, positioning them as the preferred material for high-tensile applications. This segment commands the largest market share in both volume and revenue, propelled by expanding adoption in protective gear and ballistic uses. Their exceptional resistance to abrasion and impact proves vital in manufacturing essential products such as bulletproof vests, helmets, and vehicle armor. These attributes ensure reliable performance under extreme stress, meeting stringent safety demands across defense and security sectors.

Meta-aramid fibers are likely to be the fastest-growing segment during the 2026-2033 forecast period. The segment stands out for its superior thermal stability and resistance to chemicals. Manufacturers favor them in thermal protective clothing, filtration systems, and electrical insulation, where they preserve structural integrity amid elevated temperatures. Rising needs for worker safeguards in harsh industrial settings drive this segment's expansion, as personnel face intense heat and corrosive substances. Global workplace safety regulations further accelerate uptake across diverse protective roles, ensuring compliance and reliability in demanding conditions.

Application Insights

Tire reinforcement is anticipated to command an estimated 32% of the aramid fiber market revenue share in 2026, due to its high modulus and minimal thermal shrinkage. These properties suit radial tire belt designs perfectly, where manufacturers seek to lower rolling resistance and cut weight compared to steel cords. Premium and ultra-high-performance tires from companies such as Michelin, Bridgestone, and Continental now feature aramid integration in key product lines, delivering enhanced durability and fuel savings. The shift to electric vehicles (EVs) heightens this trend, as EV tires face accelerated wear from greater mass and torque. Major producers, including Goodyear, Pirelli, and Hankook, prioritize aramid in specialized developments to boost longevity while preserving efficiency for a better range. Asia-Pacific commands the forefront, fueled by robust tire output in China and India's rising automotive sector.

Protective apparel is expected to be the fastest-growing segment during the 2026-2033 forecast period, propelled by tougher workplace safety rules and greater focus on job-related risks. This category covers ballistic vests, cut-resistant gloves, flame-resistant outfits, and gear for first responders. Employers in sectors such as manufacturing, construction, and transportation invest heavily in advanced protective solutions to shield workers from common hazards. Law enforcement and military units drive key demand through procurement for body armor upgrades. Commercial users in oil and gas adopt aramid-based flame-resistant clothing to counter arc flash dangers. Industrial gloves gain traction in automated factories, where human-robot interactions call for top-tier hand safeguards that meet rigorous cut-resistance benchmarks.

End-User Insights

The automotive segment is slated to lead with an approximate 58% of the aramid fiber market share in 2026. Automotive manufacturers harness aramid fibers to craft components that elevate vehicle safety and efficiency. Engineers incorporate these materials into tires, brake pads, and reinforced composites, where they withstand intense stress and heat. As companies prioritize fuel savings and lower emissions, the lightweight properties of aramid fibers deliver key advantages in meeting those targets. The rise of EVs further amplifies this role, with automakers experimenting with innovative designs to trim weight, which directly boosts EV range and performance. Market players can gain strategic leverage by integrating aramid solutions early in development cycles as well as ensuring compliance with evolving standards while positioning brands for competitiveness in a shifting market landscape.

Aerospace & defense is anticipated to be the fastest-growing application area between 2026 and 2033, driven by its resilience in harsh environments and unmatched protective qualities. Engineers deploy these materials in lightweight, durable components that boost fuel economy and operational effectiveness across commercial and military aircraft. Designers create structural elements such as panels and frames that endure extreme stresses without adding bulk. The defense field depends heavily on aramid for personal gear, including helmets and vests, which shield troops in high-risk combat areas. Manufacturers secure a competitive advantage by advancing fiber blends that enhance impact resistance and thermal endurance. Leaders position their firms for growth through targeted R&D investments. They align innovations with procurement priorities to capture expanding defense budgets and fleet modernization programs.

Regional Insights

Asia Pacific Aramid Fiber Market Trends

Asia Pacific is projected to be both the leading and fastest-growing regional market for aramid fiber through 2033, accounting for approximately 42% of the market share, propelled by robust industrial expansion across the key economies of China, India, and the ASEAN bloc. China anchors regional dominance through its vast automotive output, tire manufacturing, and tire cord consumption. Japan bolsters demand via sophisticated production in vehicles, electronics, and machinery. India emerges as the quickest-expanding national player, supported by surging car assembly and defense upgrades. ASEAN economies such as Thailand, Indonesia, and Vietnam gain momentum from factory relocations and telecom buildouts. Regional producers benefit from cost efficiencies tied to integrated petrochemical hubs, which secure affordable inputs and streamlined logistics. Local firms such as Yantai Tayho, Hyosung, and Guangdong Charming scale operations to rival international benchmarks while upholding quality standards.

Strategic investors view Asia Pacific as the prime hub for Aramid Fiber manufacturing, given its unmatched supply chain resilience and innovation potential. China's tire sector fuels tire reinforcement needs, especially for premium and EV models favored by rising consumers. India's self-reliant policies under the Atmanirbhar Bharat initiative spur local sourcing for protective gear in defense applications. Telecom rollouts, notably 5G networks, intensify requirements for strengthened optic cables. Companies such as Hyosung commit major funds to capacity growth in Vietnam, while Chinese players advance nano-enhanced and recycled variants to satisfy multinational sustainability demands.

Europe Aramid Fiber Market Trends

Europe is foreseen to play a central role in advancing the aramid fiber market growth from 2026 to 2033 on account of its advanced automotive production, aerospace capabilities, and rigorous industrial safety protocols. Germany spearheads regional uptake, with the U.K., France, and Spain close behind. These nations drive demand via vehicle manufacturing prowess and aircraft assembly. Automakers integrate aramid materials into tires and brake systems to meet fuel efficiency goals. EU rules, along with other regulations such as Corporate Average Fuel Economy (CAFE) standards of the U.S, push lightweight solutions that cut emissions. Producers can gain an edge by aligning offerings with these mandates, which favor composites over heavier alternatives.

Regulatory alignment under frameworks such as REACH and the Circular Economy Action Plan guides sector evolution. Compliance raises costs yet shields incumbents from new rivals. The European Composites Industry Association underscores aramid's role in reaching carbon neutrality across transport and building sectors. Airbus facilities in France, Germany, and Spain rely on these fibers for key aircraft parts. Teijin Aramid bases its major para-aramid plant in Arnhem, Netherlands. Investments flow to sustainable precursors from firms such as BASF and Covestro. Offshore wind projects expand needs for reinforced turbine blades and housings.

North America Aramid Fiber Market Trends

North America is predicted to occupy a prominent position in the global market for aramid fiber through 2033, fueled by top-tier aerospace output, hefty defense outlays, and firm occupational safety rules from the Occupational Safety and Health Administration (OSHA). The United States steers regional demand through aircraft manufacturing hubs in Washington and South Carolina. Boeing programs such as the 787 Dreamliner and 777X rely on consistent aramid supplies for vital parts. Defense initiatives procure these materials for body armor upgrades and fighter jet production. Executives strengthen their footing by syncing production with U.S. military priorities and commercial aviation cycles.

Regulatory pressures shape the landscape, as the U.S. Environmental Protection Agency (EPA) fuel economy mandates urge automakers to embrace lightweight aramid composites. National Fire Protection Association (NFPA) codes enforce aramid gear in firefighting, power utilities, and heavy industry. DuPont's Richmond facility in Virginia pioneers Kevlar and Nomex fibers, leading advances in nano-enhanced and hybrid blends. Teijin Aramid expands capacity in Conyers, Georgia, to bolster local chains. Mexico's vehicle assembly for the North American Free Trade Agreement (USMCA) markets opens doors for tire cords and parts. Firms can thrive by building resilient domestic networks, targeting near-shoring shifts to cut risks and seize automotive growth in cross-border trade.

Competitive Landscape

The global aramid fiber market structure is likely to remain moderately consolidated, with leading manufacturers dictating nearly 65% of total revenues in 2026. Established producers are maintaining strong positions through continuous investment in research & development (R&D) and expansion of application portfolios. These companies are advancing fiber performance characteristics such as tensile strength, thermal resistance, and chemical stability to address evolving requirements in aerospace, defense, automotive, and industrial safety sectors. Innovation is enabling penetration into emerging areas including electric vehicle components, advanced composites, and high-performance telecommunications infrastructure. Strategic geographic expansion and localized production capabilities are further strengthening supply security and market reach in key growth regions.

Barriers to entry remain substantial due to complex polymerization processes, specialized spinning technologies, and high capital expenditure requirements for manufacturing facilities. Quality control standards and long qualification cycles in sectors such as aerospace and defense further protect incumbent suppliers. As a result, established players continue to retain considerable market influence. Companies are broadening product lines and investing in capacity upgrades to meet rising global demand. Leadership teams benefit from closely monitoring competitor capacity expansions, pricing adjustments, and downstream integration strategies. Strategic partnerships, technology upgrades, and targeted regional investments are enabling firms to capture new opportunities while reinforcing their positions in core application segments.

Key Industry Developments

- In October 2025, researchers at Peking University developed a revolutionary bulletproof fabric by combining carbon nanotubes with aramid polymers, creating a material three times stronger than Kevlar while being only 1.8 mm thick. The aligned nanotubes prevent molecular slippage during high-impact events, enabling three thin layers to stop bullets that would require much thicker Kevlar panels.

- In September 2025, DuPont agreed to sell its iconic aramid fibers business, including the Kevlar and Nomex brands, to chemical manufacturer Arclin for approximately US$ 1.8 billion. This divestiture includes 1,900 employees and five manufacturing plants across the U.S., Europe, and Spain.

- In July 2025, Andhra Pradesh launched a pilot project using Danish Asphalt Reinforcing Fiber technology, a blend of aramid and polyolefin fibers for a two-lane road between Mudigedu and Sanjamala, costing INR 12.58 crore, to create pothole-free asphalt roads that last 50% longer while preventing cracks and rutting.

Companies Covered in Aramid Fiber Market

- DuPont de Nemours, Inc.

- Teijin Limited (Teijin Aramid)

- Hyosung Advanced Materials

- Yantai Tayho Advanced Materials Co., Ltd.

- Kolon Industries, Inc.

- Guangdong Charming Technology Co., Ltd.

- Kermel (Armor Lux Group)

- China National Bluestar (Group) Co., Ltd.

- SRO Aramid (Jiangsu) Co., Ltd.

- Toray Industries, Inc.

- X-FIPER New Material Co., Ltd.

- JSC Kamenskvolokno

- Huvis Corporation

- Sinopec Yizheng Chemical Fiber Company Limited

- Akra Polyester S.A.

Frequently Asked Questions

The global aramid fiber market is projected to reach US$5.2 Bn in 2026.

Rising defense/security spending, automotive lightweighting, aerospace modernization, and 5G/telecom infrastructure expansion are driving the market.

The market is poised to witness a CAGR of 8.5% from 2026 to 2033.

Meta-aramid growth in electrical insulation/EVs, optical fiber cables for 5G deployment, and Asia-Pacific industrial safety/PPE expansion are key market opportunities.

DuPont de Nemours, Inc., Teijin Limited, Hyosung Advanced Materials, Yantai Tayho Advanced Materials Co., Ltd., and Kolon Industries, Inc. are some of the key players in the market.