- Pharmaceuticals

- Anti-venom Market

Anti-venom Market Size, Share, and Growth Forecast, 2025 - 2032

Anti-venom Market By Species (Snake, Scorpion, Spider), Product Type (Polyvalent, Monovalent), Mode of Action (Cytotoxic, Neurotoxic, Hemotoxic), End-user (Hospitals, Clinics, Ambulatory Surgical Centers), and Regional Analysis for 2025 - 2032

Anti-venom Market Size and Trends Analysis

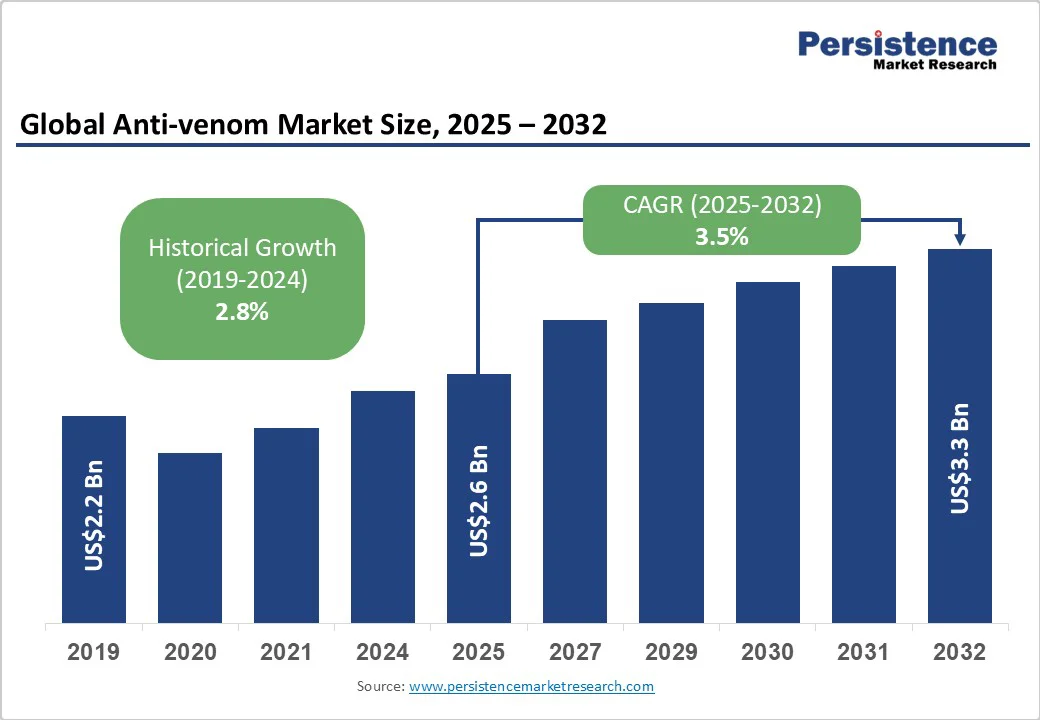

The global anti-venom market size is likely to be valued at US$2.6 Billion in 2025 and is estimated to reach US$3.3 Billion in 2032, growing at a CAGR of 3.5% during the forecast period 2025 - 2032, driven by the high incidence of venomous bites worldwide, particularly in rural and tropical regions. Increasing awareness, rising healthcare access, biotechnological innovations, and supportive global health initiatives are also fueling growth.

Growing demand for multi-species coverage, product development tailored to regional venom profiles, and supportive government policies enhancing treatment availability are all contributing to the market’s strong growth outlook.

Key Industry Highlights

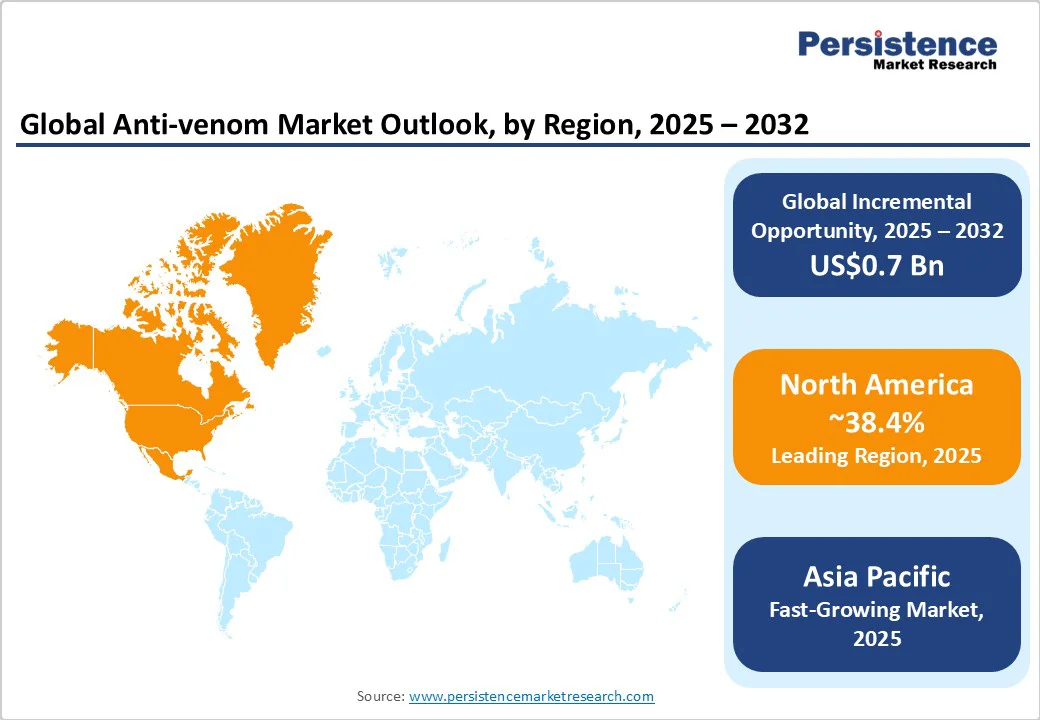

- Leading Region: North America, with about 38.4% share in 2025, with increased investments in biotech research and adoption of novel recombinant therapies.

- Fastest-growing Region: Asia Pacific is poised to record around 9.4% CAGR through 2032, due to the high incidence of venomous snakebites and increasing government support.

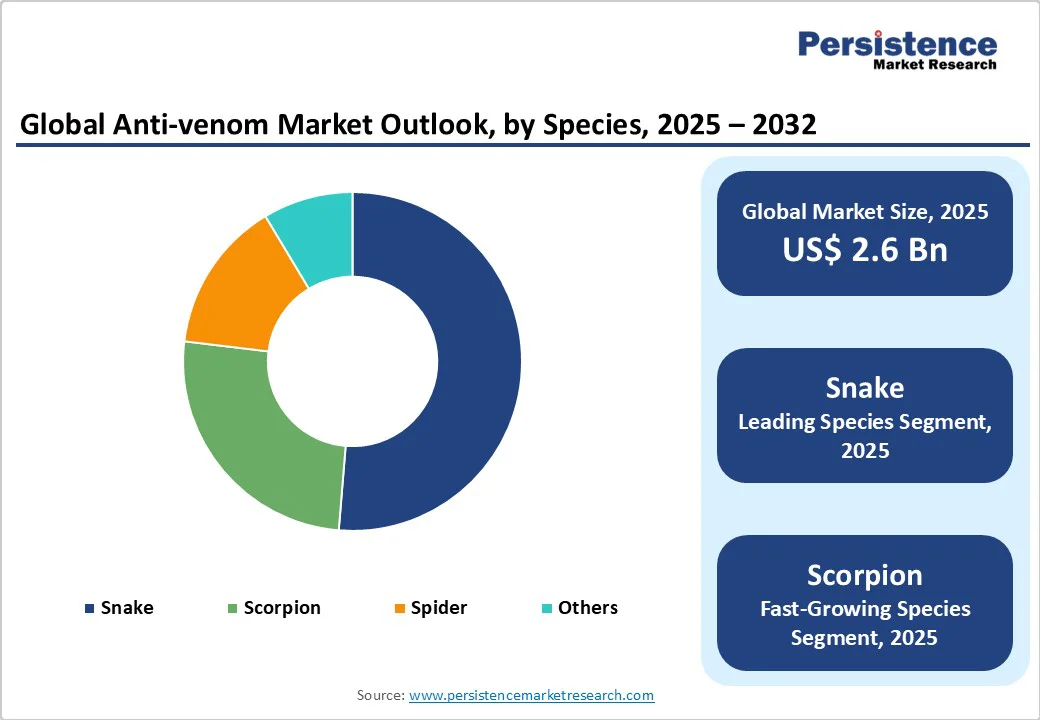

- Leading Species: Snakes hold nearly 51.3% share in 2025, as snakebites remain the primary source of envenomation worldwide, creating high demand for targeted anti-venom therapies.

- Dominant Product Type: Polyvalent anti-venoms, approximately 68.5% of the anti-venom market share in 2025, as they provide broad-spectrum coverage against multiple snake species, reducing the risk of misidentification.

- Key Mode of Action: Neurotoxic anti-venoms recorded about 33.7% share in 2025, due to their ability to neutralize venom efficiently, preventing life-threatening paralysis and organ failure.

- Local Production Plan: Speakers at the 2nd Scientific Conference and General Meeting of the Toxinological Society of Nigeria emphasized the need to strengthen local production of anti-venom. They mentioned that such initiatives would significantly reduce costs and improve access to affordable, life-saving treatment for snakebite victims.

| Key Insights | Details |

|---|---|

| Anti-venom Market Size (2025E) | US$2.6 Bn |

| Market Value Forecast (2032F) | US$3.3 Bn |

| Projected Growth (CAGR 2025 to 2032) | 3.5% |

| Historical Market Growth (CAGR 2019 to 2024) | 2.8% |

Market Factors - Growth, Barriers, and Opportunity Analysis

High Incidence of Snakebites and Venomous Bites

Globally, approximately 4.5 to 5.4 million people suffer snakebites each year, with 1.8 to 2.7 million showing clinical envenoming and an estimated 81,000 to 138,000 fatalities annually. This burden is high in tropical and subtropical regions such as South Asia, Africa, and Latin America.

In these regions, rural communities face high exposure and limited emergency care facilities. Government initiatives, including India’s sub-regional anti-snake venom units, improve access and underline the urgent medical need, resulting in reliably superior product demand.

Ongoing Developments in Biotechnology

Recent biotechnological progress, including synthetic monoclonal antibodies and recombinant anti-venoms, improves therapeutic safety, specificity, and efficacy. For example, Columbia University’s collaboration in 2025 led to a broad-spectrum anti-venom counteracting neurotoxins from 19 deadly snake species.

It helped in significantly improving universal treatment options and safety profiles in clinical applications. These innovations drive sustained growth, enabling increased market penetration into high-burden regions.

Government and Global Health Initiatives

The World Health Organization (WHO) and national governments continue to prioritize antivenom supply as a public health imperative, directing policy and funding to ensure wide availability, especially for rural, low-income populations. International collaborations with local manufacturers and research bodies target endemic regions with custom, affordable therapies and improved product delivery.

Governments in regions with high snakebite incidence, including South Asia and sub-Saharan Africa, are partnering with NGOs and private stakeholders to improve anti-venom distribution networks. Programs are focusing on training rural healthcare workers in the safe administration of anti-venoms, coupled with awareness campaigns to encourage early medical intervention.

High Cost of Treatment and Production

Anti-venom production is costly due to biological extraction processes, regulatory compliance, and low-volume manufacturing in developed countries. For example, a single vial in Nepal, can cost up to US$150, which is prohibitive for many victims in need.

Nearly one-third of sufferers in South Asia cannot afford life-saving anti-venom therapy, creating accessibility gaps. High prices limit adoption in regions with the highest clinical burden.

Supply Chain and Infrastructure Constraints

Distribution is especially challenging in rural and low-resource settings due to supply chain weaknesses, inconsistent funding, and inadequate healthcare infrastructure. Several patients remain untreated or receive suboptimal care, exacerbating preventable morbidity and mortality rates. Structural gaps hinder market penetration and expansion.

Cold-chain dependency and limited local production further strain distribution, as various anti-venoms require controlled storage and rapid transportation to maintain efficacy. In regions where road connectivity is poor and healthcare facilities are sparsely located, even available stock often fails to reach patients on time.

Emergence of Recombinant Anti-venoms and Novel Therapies

Increased research and development into recombinant and humanized therapies provides broad-spectrum effectiveness, better safety, and more reliable supply chains. For instance, monoclonal antibody formulations under development could decrease dependence on animals, reduce allergenicity, and expand reach, promising a market potential of at least US$500 Mn globally in new product lines by 2032.

Several biotech companies and academic institutions are collaborating to fast-track clinical trials of recombinant anti-venoms. Early studies show improved neutralization across multiple snake species compared to traditional serums. These next-generation therapies aim to address regional variability in venom composition, delivering a universal solution that would help simplify production and distribution.

Heat-stable and Easy-to-administer Formulations

A key opportunity lies in creating anti-venoms that are thermostable and require minimal clinical expertise for administration. Heat-stable formulations would overcome cold-chain dependencies, ensuring access in remote and tropical regions where electricity and storage facilities are limited.

At the same time, simplified delivery methods such as pre-filled syringes, oral formulations under research, or auto-injectors could empower frontline workers and even trained community volunteers to respond quickly to snakebite incidents. These developments not only reduce mortality in underserved areas but also broaden the potential customer base by making treatment more practical.

Integration with Advanced Diagnostics

Introducing point-of-care diagnostics for venom identification is enabling the precision use of monovalent anti-venoms, reducing adverse reactions and boosting outcomes. Healthcare facilities providing rapid species identification and immediate targeted therapy are seeing improved success rates, supporting expanded market application.

Emerging portable diagnostic kits based on molecular and immunoassay technologies are being developed for use in low-resource settings. These are allowing frontline workers to quickly match the venom type with the most effective treatment. Integration with digital health platforms further strengthens this approach. This is due to the ability to transmit diagnostic data in real time to centralized databases, enabling more informed clinical decisions and efficient stock management.

Category-wise Analysis

Species Insights

Snake anti-venoms hold approximately 51.3% of the market share in 2025, driven by the high incidence of snakebites and their severe health consequences, especially in India, Africa, and Latin America. Broad indication and strong product pipeline safeguard market dominance.

The scorpion segment will likely see steady growth due to increased stings in the Middle East, North Africa, and South Asia. Additionally, improved diagnostic coverage and rising urbanization encroaching on natural habitats are predicted to drive growth. Regional initiatives continue to support local product launches and ramp supply.

Product Type Insights

Polyvalent anti-venoms account for nearly 68.5% of the market share in 2025, favored for emergency use and multi-species efficacy, especially where snake identification is not feasible. This versatility drives large-scale government procurement and public hospital uptake.

Monovalent anti-venoms, made for specific species, are expanding considerably through technological development and improved venom profiling. Growth is supported by investments in molecular diagnostics and clinical precision, mainly in semi-urban healthcare facilities.

Mode of Action Insights

Neurotoxic anti-venoms hold about 33.7% of the market share in 2025, targeting life-threatening envenomation agents such as cobras and kraits that cause neuro-respiratory paralysis. The urgency of clinical requirements and focus on Asia Pacific and Africa underpins sustained demand.

Cytotoxic anti-venoms are increasingly adopted to treat Russell’s viper and puff adder cases, with accelerated segmental growth driven by awareness and formulation developments. Market CAGR for cytotoxic products nears double digits in developing countries.

Regional Insights

North America Anti-venom Market Trends

North America is projected to account for approximately 38.4% of the global anti-venom market share in 2025, led by a well-established pharmaceutical industry and novel healthcare delivery systems. The U.S. alone is forecast to reach US$0.8 Billion by 2032, propelled by government investments, ongoing research and development inflows, and sophisticated emergency infrastructure.

Key drivers include regulatory support, quick innovation cycles, and superior partnerships between biotech firms and academic research institutions. North America’s competitive landscape features high market concentration, with leading multinationals and emerging start-ups accelerating next-generation therapies. Ongoing investment in product development and geographical expansion exhibits continued leadership, and high health insurance coverage reduces financial barriers for treatment.

Asia Pacific Anti-venom Market Trends

Asia Pacific is the market’s fastest-growing region, with an expected CAGR of 9.4% through 2032, propelled by high incidences of venomous bites across India, China, ASEAN, and Japan. Rural and semi-urban demand remains high, with governments and NGOs investing in diagnostic capacity, local manufacturing, and new anti-venom product launches such as India’s collaboration with the Indian Institute of Science (IISc).

Competitive parity is achieved via partnerships with global leaders, rapid clinical trials, and local technology transfer, further reinforced by favorable regulatory frameworks. Investment has focused on infrastructure expansion, regional market entry, and public procurement programs. Asia Pacific is speculated to dominate in terms of volume growth by the end of the forecast period.

Europe Anti-venom Market Trends

Europe’s steady growth is being fueled by regulatory harmonization under the European Medicines Agency, facilitating uniform standards for anti-venom safety, efficacy, and distribution. Southern countries such as France, Italy, Spain, Greece, and Portugal record the highest incident rates. National health systems often respond with improved funding, public health campaigns, and collaborative product development.

Competitive market structures balance large pharmaceutical operators and small-scale regional firms. The majority are focusing on rapid innovation and affordable supply. Key investments target diagnostic integration, region-specific production, and cross-border distribution networks.

Competitive Landscape

The global anti-venom market is moderately fragmented, with regional and national producers competing alongside global giants. Dominant players collectively control over 60% of sales, but significant volumes are also supplied by government-run and local ventures.

Competitive positioning is influenced by geographic reach, research and development pipelines, and regulatory compliance. A few companies are now differentiating through technology development, targeted therapies, and affordability initiatives.

Key Industry Developments

- In July 2025, Kerala announced plans to begin local production of snake antivenom in partnership with the Health Department. The initiative came in response to long-standing concerns over the effectiveness of anti-venom currently sourced from Tamil Nadu, which may not be fully effective in targeting bites from snakes found in Kerala.

- In January 2025, the Punjab Government launched an anti-snake venom treatment in all the district and tehsil level veterinary hospitals across the state. Punjab Animal Husbandry, Dairy Development, and Fisheries Minister stated that polyvalent anti-snake venom medicine has been made available.

Business Strategies

The market’s dominant strategies center on development, geographic expansion, and cost leadership. High research and development spend, partnerships for regional adaptation, and expandable manufacturing are key elements, with new distribution models targeting underserved and remote areas.

Companies Covered in Anti-venom Market

- CSL Limited

- Pfizer Inc.

- Merck & Co., Inc.

- Bharat Serums & Vaccines Ltd.

- VINS Bioproducts Limited

- Rare Disease Therapeutics Inc.

- Instituto Bioclon

- MicroPharm Ltd.

- Haffkine Bio-Pharmaceutical Corp.

- Sanofi Pasteur

- Incepta Pharmaceuticals Ltd.

- Laboratorios Silanes S.A.

- BTG plc

- Vacsera

- Indian Immunologicals Limited

Frequently Asked Questions

The anti-venom market is projected to reach US$2.6 Billion in 2025.

The rising incidence of snakebites and WHO-backed initiatives are the key market drivers.

The anti-venom market is poised to witness a CAGR of 3.5% from 2025 to 2032.

Integration of point-of-care diagnostics and launch of monoclonal antibody-based anti-venoms are the key market opportunities.

CSL Limited, Pfizer Inc., and Merck & Co., Inc. are a few key market players.