- Pharmaceuticals

- Anti-Obesity Prescription Market

Anti-Obesity Prescription Market Size, Share, Trends, Growth, and Forecasts for 2025 - 2032

Anti-Obesity Prescription Market by Product Type (Approved, Off Label), Mechanism (Peripherally Acting Drugs, Centrally Acting Drugs), Distribution Channel (Retail Pharmacies, Hospital Pharmacies, Others), and Regional Analysis for 2025 - 2032

Anti-Obesity Prescription Market Size and Trends

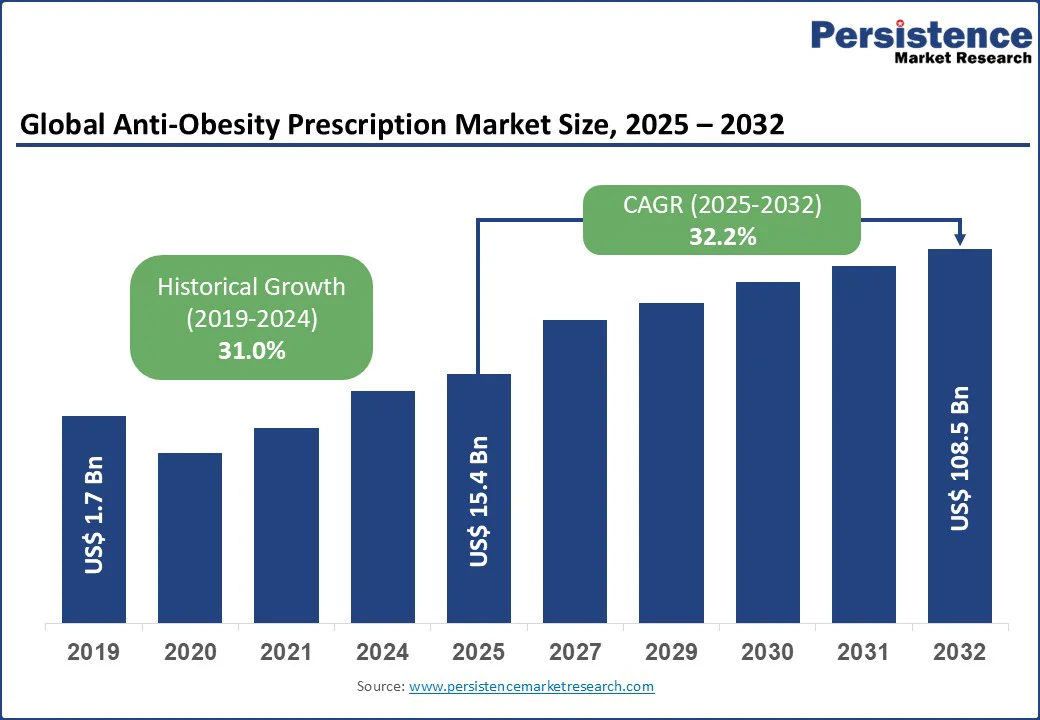

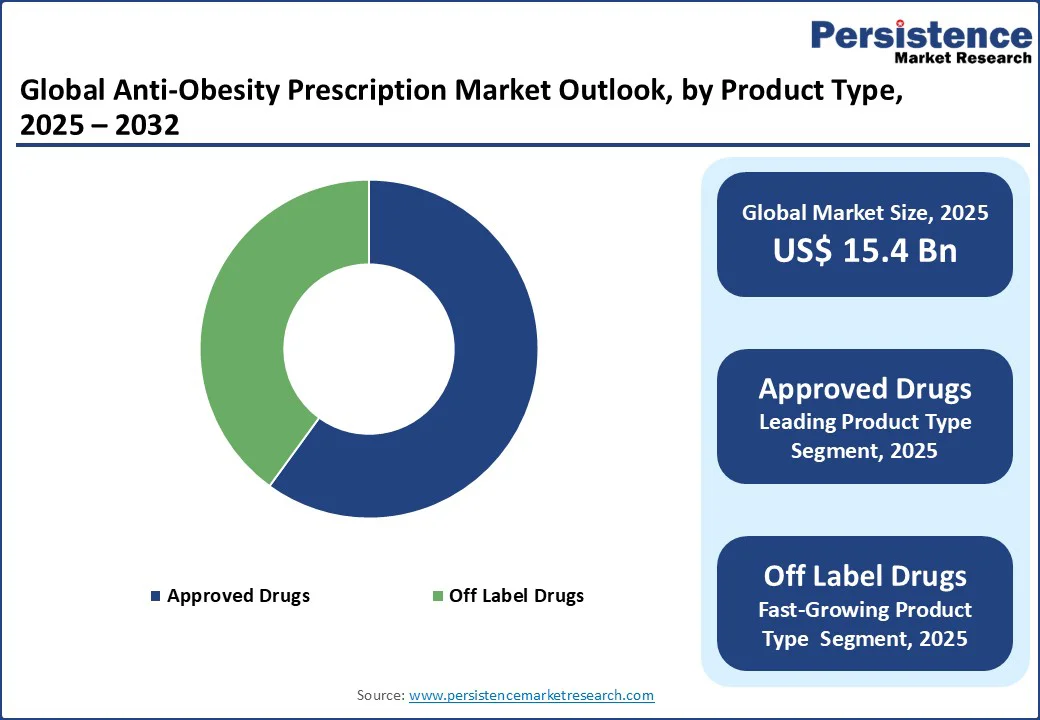

The global anti-obesity prescription market size is likely to be valued at US$15.4 Bn in 2025 and projected to reach US$108.5 Bn by 2032, growing at a CAGR of 32.2% during the forecast period 2025 - 2032. The growth is fueled by the increasing global prevalence of obesity, advancements in obesity treatment drugs, and growing awareness of health risks associated with obesity, such as diabetes and cardiovascular diseases.

Key Industry Highlights:

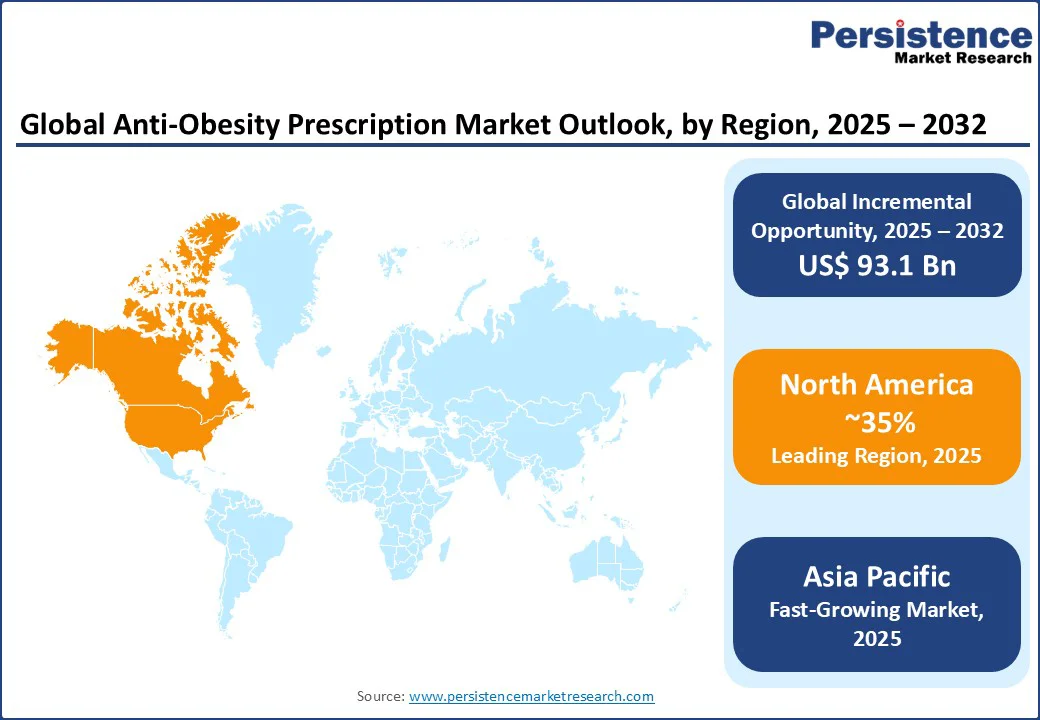

- Leading Region: North America holds a 40% market share in 2025, driven by its high obesity prevalence, advanced healthcare infrastructure, and supportive regulatory environment.

- Fastest-growing Region: Asia Pacific holds a leading share in 2025 and is the fastest-growing region, driven by sedentary lifestyles and processed food consumption, which fuels demand for prescription weight loss medications such as orlistat and liraglutide.

- Dominant Product Type: Approved drugs market share accounts for 65% in 2025, led by GLP-1 receptor agonists.

- Leading Mechanism: Peripherally acting drugs contribute 60% of revenue, due to their efficacy and safety.

- Fastest-Growing Distribution Channel: Retail pharmacies register a 50% share, focusing on online pharmacy services.

|

Global Market Attribute |

Key Insights |

|

Anti-Obesity Prescription Market Size (2025E) |

US$15.4 Bn |

|

Market Value Forecast (2032F) |

US$108.5 Bn |

|

Projected Growth (CAGR 2025 to 2032) |

32.2% |

|

Historical Market Growth (CAGR 2019 to 2024) |

31.0% |

Market Dynamics

Drivers: Rising Prevalence of Obesity in the Population

The global rise in obesity is a primary driver for the anti-obesity prescription market, as increasing numbers of individuals face health challenges linked to excess body weight, such as type 2 diabetes, hypertension, and cardiovascular diseases. The World Health Organization (WHO) reports that obesity rates have nearly tripled since 1975, with significant implications for healthcare systems worldwide. This surge is particularly pronounced in urban areas, where sedentary lifestyles, high-calorie diets, and limited physical activity contribute to rising Body Mass Index (BMI) levels.

Prescription weight loss medications such as GLP-1 receptor agonists (e.g., semaglutide, liraglutide) and appetite suppressants (e.g., phentermine-topiramate) are increasingly prescribed to address these conditions, offering targeted solutions for patients unable to achieve weight loss through lifestyle changes alone. The growing recognition of obesity as a chronic disease has shifted healthcare approaches, with physicians emphasizing obesity treatment drugs as part of comprehensive weight management programs. In developed regions, robust healthcare infrastructure and insurance coverage facilitate access to anti-obesity medication drugs, while in emerging markets, rising disposable incomes and healthcare awareness are driving demand.

Restraints: High Costs and Limited Reimbursement

The high cost of anti-obesity prescription drugs, particularly advanced therapies such as GLP-1 receptor agonists and combination medications, poses a significant restraint to market growth. These drugs often involve complex manufacturing processes and extensive clinical trials, resulting in elevated prices that can be prohibitive for patients without adequate insurance or government support. For instance, semaglutide (Wegovy) and tirzepatide (Zepbound) require ongoing treatment, increasing long-term expenses for patients and healthcare systems. In developing regions, limited healthcare budgets and a lack of reimbursement for obesity treatment drugs restrict access, forcing patients to rely on cheaper, less effective alternatives or lifestyle interventions.

Even in developed markets, insurance coverage for prescription weight loss medications varies, with some plans excluding obesity treatments due to their classification as non-essential or cosmetic. This financial barrier limits market penetration, particularly among low-income populations, and slows the adoption of innovative anti-obesity medication drugs, hindering overall market expansion.

Opportunities: Advancements in Personalized Medicine

The shift toward personalized medicine presents a transformative opportunity for the Anti-Obesity Prescription Market, as genetic and metabolic profiling enables the development of tailored obesity treatment drugs. Advances in pharmacogenomics allow healthcare providers to identify patients most likely to benefit from specific prescription weight loss medications, such as GLP-1 receptor agonists or appetite suppressants, based on their genetic makeup and metabolic pathways. This approach enhances treatment efficacy and minimizes side effects, improving patient outcomes and adherence. Companies such as Novo Nordisk A/S and Rhythm Pharmaceuticals are investing in R&D to develop targeted therapies, such as setmelanotide for rare genetic obesity disorders, which address specific patient profiles.

The integration of digital health tools, such as AI-driven diagnostics and telehealth platforms, further supports personalized treatment plans by monitoring patient progress and optimizing drug regimens. Emerging markets, with growing healthcare infrastructure and increasing awareness of obesity-related health risks, offer significant potential for these innovations.

Category-wise Analysis

Product Type Insights

Approved drugs dominate with a 65% share in 2025, driven by their regulatory approval, proven efficacy, and widespread adoption. Drugs such as semaglutide (Wegovy), liraglutide (Saxenda), and tirzepatide (Zepbound) lead this segment due to their effectiveness in promoting significant weight loss and managing obesity-related comorbidities. These prescription weight loss medications are backed by extensive clinical trials and FDA approvals, ensuring trust among healthcare providers and patients.

Off-label drugs are the fastest-growing, driven by their increasing use in weight management for patients with specific needs. Drugs such as semaglutide (Ozempic) and liraglutide (Victoza), originally approved for diabetes, are prescribed off-label for obesity due to their weight-loss benefits. The flexibility of off-label drugs allows physicians to tailor treatments to individual patients, particularly those with comorbidities such as type 2 diabetes.

Mechanism Insights

Peripherally acting drugs hold a 60% market share in 2025, driven by their efficacy and favorable safety profiles. Drugs such as orlistat (Xenical) and GLP-1 receptor agonists (e.g., semaglutide, liraglutide) work by inhibiting fat absorption or regulating appetite and glucose metabolism without directly affecting the central nervous system. These obesity treatment drugs are preferred for their reduced risk of neurological side effects, making them suitable for a wide range of patients, including those with comorbidities.

Centrally acting drugs are the fastest-growing segment, driven by innovations in appetite suppressants such as phentermine-topiramate (Qsymia) and bupropion-naltrexone (Contrave). These drugs target the central nervous system to reduce hunger and promote satiety, offering effective weight loss for patients with high BMI. The segment’s growth is fueled by increasing demand for combination therapies that enhance efficacy while minimizing side effects.

Distribution Channel Insights

Retail pharmacies dominate with a 50% share in 2025, driven by their accessibility and the growing popularity of prescription weight loss medications among consumers. The rise of e-commerce platforms and online pharmacies within this segment enhances convenience, allowing patients to access anti-obesity prescription drugs such as semaglutide and liraglutide with ease. Retail pharmacies benefit from strong supply chains and partnerships with pharmaceutical companies, ensuring a steady supply of obesity treatment drugs.

Online pharmacies are the fastest-growing segment, with a CAGR of 35%, driven by the increasing adoption of digital health platforms and telehealth services. The convenience of online purchasing, coupled with home delivery and subscription models, is transforming the distribution of anti-obesity medication. Online pharmacies offer competitive pricing and access to both approved drugs and off-label drugs, appealing to tech-savvy consumers in urban areas.

Regional Insights

North America Anti-Obesity Prescription Market Trends

North America is likely to hold 40% market share in 2025, with the United States as the primary contributor, driven by its high obesity prevalence, advanced healthcare infrastructure, and supportive regulatory environment. The U.S. market is propelled by the Centers for Disease Control and Prevention (CDC) reporting that over 40% of adults are obese, fueling demand for prescription weight loss medications such as semaglutide (Wegovy) and tirzepatide (Zepbound). The FDA’s approval of innovative obesity treatment drugs, such as semaglutide in 2025 for chronic weight management, has accelerated market growth.

The U.S. benefits from robust healthcare spending and insurance coverage, making anti-obesity medication drugs more accessible through retail pharmacies and hospital pharmacies. The growing adoption of telehealth and online pharmacies further enhances access, particularly for patients in rural areas. The focus on personalized medicine, driven by companies such as Novo Nordisk A/S and Rhythm Pharmaceuticals, is shaping the market, with tailored therapies addressing specific patient needs.

Asia Pacific Anti-Obesity Prescription Market Trends

APAC is expected to lead with a positive share in 2025 and is the fastest-growing region, led by China, India, and Japan. China’s rapid urbanization and rising obesity rates, driven by sedentary lifestyles and processed food consumption, fuel demand for prescription weight loss medications such as orlistat and liraglutide. Government healthcare reforms, such as the Healthy China 2030 initiative, promote access to obesity treatment drugs through hospital pharmacies and retail pharmacies.

India’s growing middle class and increasing obesity prevalence, particularly in urban areas, drive demand for affordable anti-obesity medication drugs. The Ayushman Bharat program enhances healthcare access, boosting the adoption of approved drugs and off-label drugs in online pharmacies. Japan’s market is expanding due to rising awareness of obesity-related health risks and the adoption of GLP-1 receptor agonists such as semaglutide. The country’s advanced healthcare infrastructure and focus on preventive care support the growth of hospital pharmacies as key distribution channels.

Europe Anti-Obesity Prescription Market Trends

Europe is poised to register a steady growth in 2025, with Germany, France, and the United Kingdom as leading contributors. Germany’s advanced healthcare system and high obesity rates drive demand for prescription weight loss medications such as liraglutide and orlistat, supported by government reimbursement programs. The country’s focus on preventive healthcare and chronic disease management promotes the adoption of GLP-1 receptor agonists in hospital pharmacies and retail pharmacies.

France’s universal healthcare system facilitates access to anti-obesity medication drugs, with stair lifts and obesity treatment drugs integrated into obesity management programs. The French government’s initiatives to address obesity-related comorbidities, such as diabetes, boost demand for approved drugs such as semaglutide. The UK’s National Health Service (NHS) drives market growth through public health campaigns and pilot programs, such as the £40 Mn initiative to expand access to obesity treatment drugs outside hospitals.

Competitive Landscape

The global anti-obesity prescription market is highly competitive, with key players focusing on innovation, strategic partnerships, and market expansion. Leading companies leverage advanced R&D to develop prescription weight loss medications with improved efficacy and safety profiles, while also targeting emerging markets to capture growing demand.

Key Developments

- In 2025, Rhythm Pharmaceuticals presented real-world data on setmelanotide's effectiveness in patients with hypothalamic obesity at a joint congress, indicating expansion of the drug's potential to a broader patient group beyond its established use in rare genetic obesity disorders like Bardet-Biedl Syndrome (BBS) and Pro-opiomelanocortin (POMC) deficiencies

- In 2023, Eli Lilly's Zepbound (tirzepatide) injection, the first GIP and GLP-1 hormone receptor activator for obesity, receives FDA approval based on phase 3 trial results, offering significant weight loss potential with gastrointestinal side effects.

Companies Covered in Anti-Obesity Prescription Market

- Novo Nordisk A/S

- GlaxoSmithKline plc

- Novartis AG

- VIVUS LLC

- Currax Pharmaceuticals

- Kintai Therapeutics

- Boehringer Ingelheim International GmbH

- Rhythm Pharmaceuticals, Inc.

- Gelesis

- Others

Frequently Asked Questions

The anti-obesity prescription market is projected to reach US$15.4 Bn in 2025, driven by rising obesity rates and demand for prescription weight loss medications.

The rising prevalence of obesity globally fuels demand for anti-obesity medication drugs such as GLP-1 receptor agonists and appetite suppressants.

The anti-obesity prescription market is expected to grow at a CAGR of 32.2% from 2025 to 2032, driven by innovations in obesity treatment drugs.

Advancements in personalized medicine and digital health platforms offer significant growth potential for tailored prescription weight loss medications.

Leading players include Novo Nordisk A/S, GlaxoSmithKline plc, Currax Pharmaceuticals, VIVUS LLC, and Rhythm Pharmaceuticals.