- Media & Entertainment

- Anime Merchandising Market

Anime Merchandising Market Size, Share, and Growth Forecast, 2026 - 2033

Anime Merchandising Market by Product (Apparel and Accessories, Toys and Figurines, Stationery, Electronic Accessories, Video Games and DVDs, Others), Distribution Channel (Online, Offline) and Regional Analysis for 2026 - 2033

Anime Merchandising Market Size and Trends Analysis

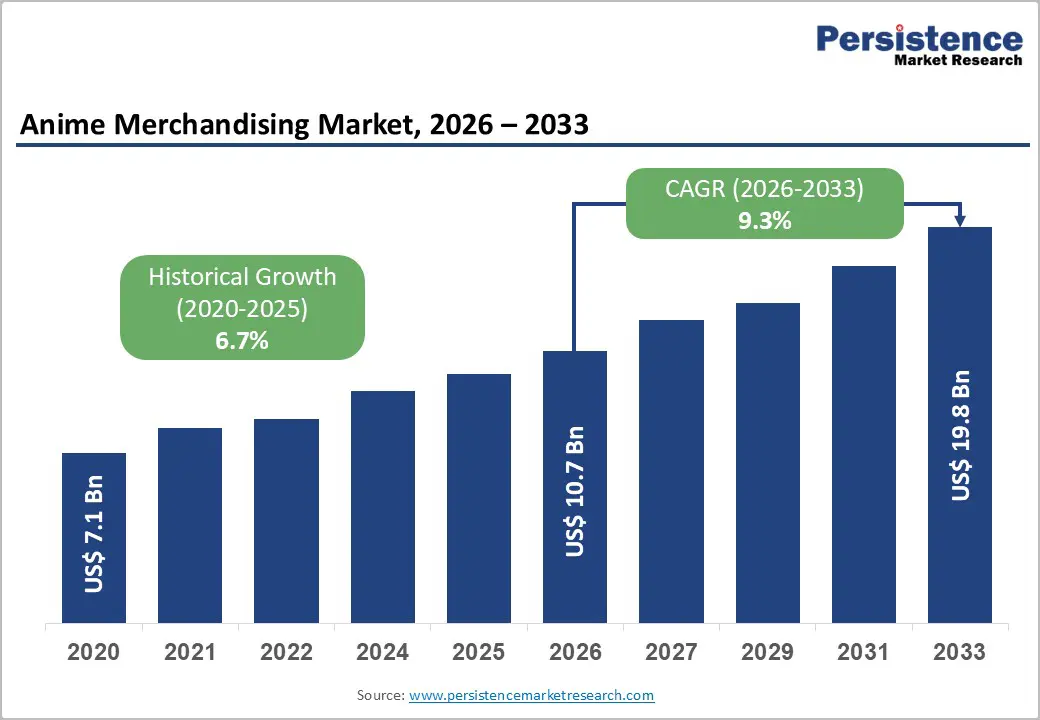

The global anime merchandising market is projected to grow from US$10.7 billion in 2026 to US$19.8 billion by 2033, at a CAGR of 9.3% from 2026 to 2033.

This expansion reflects the rapid globalization of anime culture, supported by streaming platforms, growing international fan bases, and digital-first consumption habits. Strategic IP licensing between Japanese studios and global entertainment companies has enabled anime characters to penetrate diverse merchandise categories. Demand remains strong for limited-edition products, brand collaborations, and character-themed daily-use items. Anime conventions, pop-up stores, and fan events further boost sales by creating immersive direct-to-consumer experiences.

Key Industry Highlights:

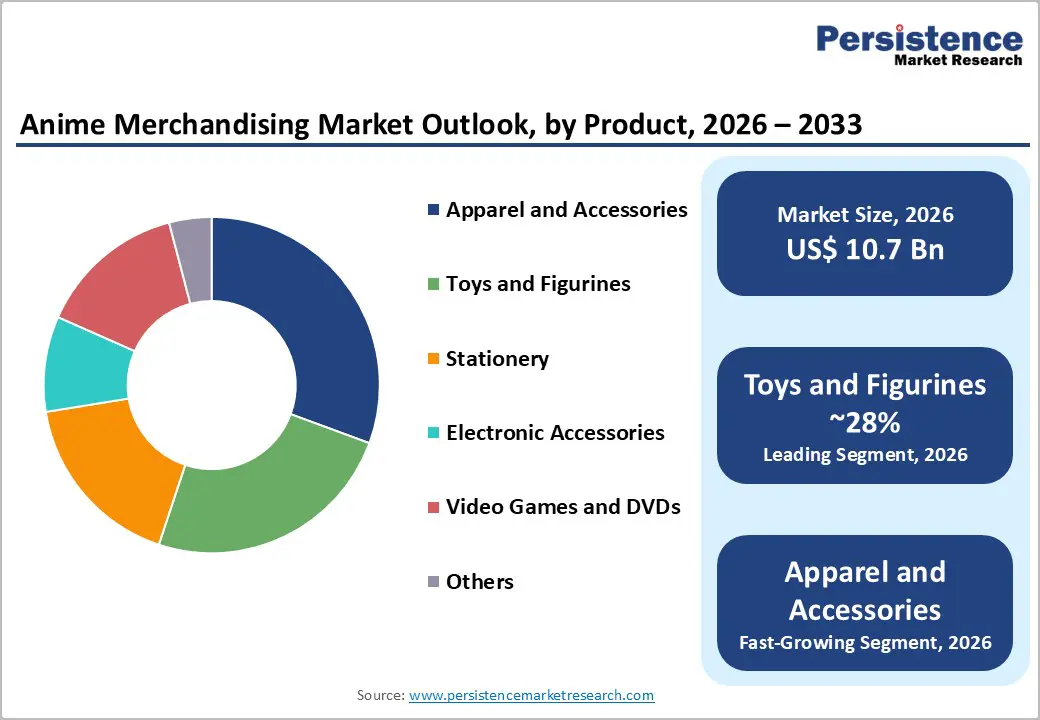

- Leading Product Segment: Toys and figurines lead with over 28% global share and valuations exceeding US$ 3.0 Bn in 2026, driven by collector demand and artistic appeal. Apparel and accessories are the fastest-growing segment with a CAGR of 13.9%, projected to reach US$ 5.9 Bn by 2033, fueled by fashion collaborations and fan identity expression.

- Leading Distribution Channel: Online channels dominate with over 53% market share and valuations over US$ 5.7 Bn in 2026, projected to grow at a CAGR of 14.6%, supported by direct-to-consumer sites and marketplaces like Amazon and AliExpress. Offline channels hold over 40% market share by 2033, with specialty retail stores capturing approximately 49% of offline sales.

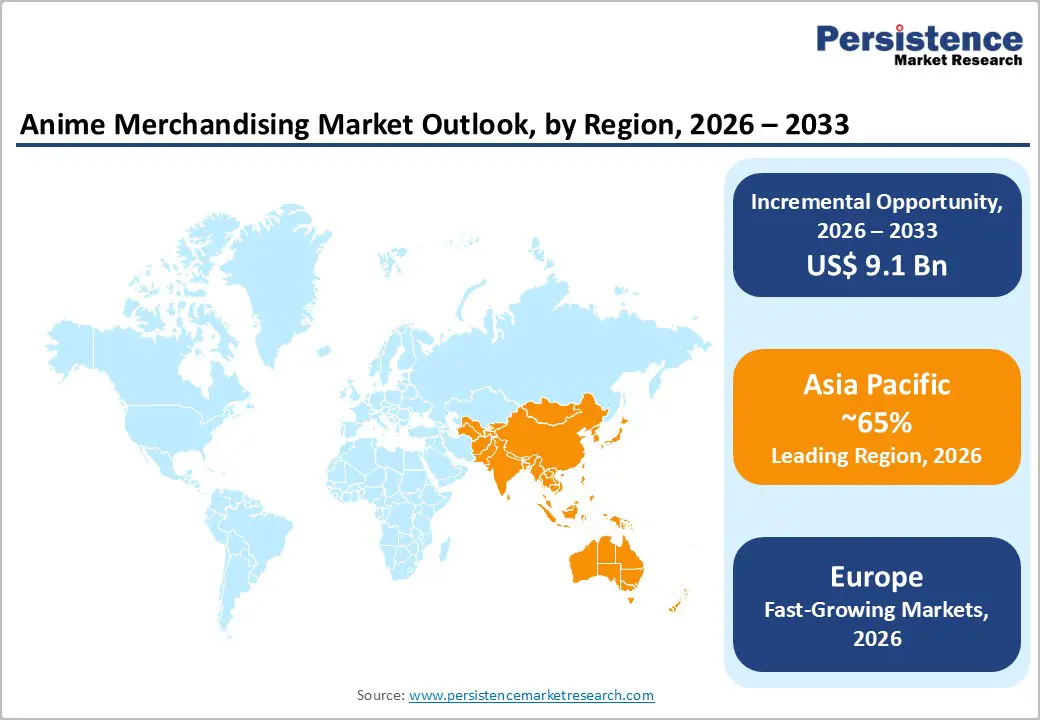

- Leading Region: Asia Pacific commands over 65% global market share with valuations of US$ 7.0 Bn in 2026, led by Japan, which holds around 49% of the global share with valuations exceeding US$ 5.2 Bn. China is expected to exceed US$ 1.2 Bn market valuation by 2033.

- Fastest-Growing Region: North America shows rapid growth projected to reach more than US$ 3.2 Bn by 2033, with the U.S. market expected to exceed US$ 2.4 Bn by 2033, while India grows at a CAGR of 15.2%, driven by fandom expansion and streaming penetration. Europe grows at 10.8% CAGR, projected to cross US$ 1.9 Bn by 2033.

- Market Dynamics: Rising popularity of anime, conventions, and international licensing and co-production models are driving the market. Subscription boxes, print-on-demand merchandise, limited-edition drops, and immersive experiences in VR, AR, and gaming are creating significant opportunities.

| Key Insights | Details |

|---|---|

| Anime Merchandising Market Size (2026E) | US$10.7 Bn |

| Market Value Forecast (2033F) | US$19.8 Bn |

| Projected Growth (CAGR 2026 to 2033) | 9.3% |

| Historical Market Growth (CAGR 2020 to 2025) | 6.7% |

Market Dynamics

Driver - Rising Popularity of Anime Series, Cultural Festivals, and Conventions

The global rise of popular anime series fuels broad merchandise demand across age groups, from toys and school supplies to premium collectibles and apparel, with limited-edition drops driving urgency and high resale value. New content launches such as Demon Slayer, consistently spike related product sales, while cosplay and fan art bolster demand for costumes, wigs, and official licensed goods. Large conventions like Anime Expo 2025 drew a record ~410,000+ attendees from over 65 countries, serving as major merchandising hubs with exclusive items and direct fan engagement. Supported by global streaming reach on platforms like Netflix and Crunchyroll that expand the fan base, these events sustain long-term merchandise demand and cultural engagement.

International Licensing Partnerships and Co-Production Models

International licensing partnerships and co-production models are major growth factors, enabling global IP monetization. For instance, in July 2025 strategic alliance between Bandai Namco Holdings and Sony Group, involving equity investment, highlights this shift toward jointly developing and expanding anime and manga IP worldwide. Such collaborations synchronize content releases with merchandise launches across streaming, gaming, theatrical, and physical retail channels, enhancing IP value extraction. Co-production structures provide Japanese studios with capital for scale, while Western partners gain direct IP access, merchandising rights, and localization flexibility, accelerating penetration in non-traditional anime markets.

Restraint - Impact of Counterfeiting and Piracy on the Anime Merchandising

Counterfeiting and piracy erode consumer trust and divert revenues from licensed players, as fans often unknowingly buy low-quality fake merchandise that damages brand perception. The 2024 USTR Notorious Markets Report highlighted 38 online and 33 physical markets, including China-based platforms such as Taobao, DHGate, and Pinduoduo, as major channels for counterfeit anime apparel, figures, and collectibles. Piracy further weakens the ecosystem by reducing funds available for new content and merchandise development; the Authorized Books of Japan (ABJ) estimate that unauthorized global manga access resulted in around ¥8.5 trillion (~US $51-55 billion) in lost revenue annually in 2025, from 2.8 billion visits to 913 piracy sites across 123 countries, diluting legitimate consumer spending and merchandising opportunity, brand exclusivity is diluted, negatively impacting long-term market growth and sustainability.

Regulatory Complexity and Geographic IP Fragmentation

Anime merchandising faces regulatory complexity due to fragmented IP regimes across regions. Japan, the US, and the EU now largely follow 70-year post-mortem copyright protection, yet differences persist in enforcement, moral rights (EU), and licensing practices. While the Berne Convention sets minimum standards, the lack of harmonized enforcement creates challenges in cross-border licensing. Divergent DRM rules, content regulations, and territorial restrictions force region-specific product designs and distribution models, e.g., region-locked digital merchandise. These factors raise legal and transaction costs, favoring large incumbents with advanced IP management over smaller entrants.

Opportunity - Subscription Boxes and Print-on-Demand (POD) Customization

Subscription boxes and mystery packs are reshaping anime merchandising by driving recurring revenue and fan loyalty through curated, limited-edition collectibles, as seen with Crunchyroll Boxes and Loot Anime, which feature IPs like Demon Slayer and Jujutsu Kaisen. These models enhance engagement while providing valuable consumer trend insights. Simultaneously, print-on-demand enables low-risk market entry for small sellers, with platforms like Etsy hosting 30,000+ anime-focused POD shops offering customized merchandise. This flexibility supports rapid response to fan trends and fuels demand in convention- and e-commerce-driven markets such as North America.

Surge in Limited-Edition Drops and Immersive Anime Experiences

Limited-edition drops are a major growth lever in anime merchandising, using scarcity, fan loyalty, and otaku culture to drive premium demand for collectibles, apparel, and collaborations. High-profile launches such as the DIM MAK × One Piece Spring/Summer 2025 collection, unveiled at New York Fashion Week, show how anime-fashion crossovers attract both core fans and mainstream consumers. At the same time, immersive experiences across gaming, VR, and AR are expanding engagement beyond traditional media. Projects like the Gundam VR film for Meta Quest 2023 demonstrate how digital immersion strengthens emotional attachment and boosts demand for physical merchandise as commemorative items.

Category-wise Analysis

By Product Insights - Toys and Figurines Lead Owing to Strong Collector Demand and Artistic Appeal

The toys and figurines are expected to hold over 28% global market share with valuations exceeding US$ 3.0 bn in 2026, driven by fans' desire for tangible, high-quality collectibles of their favorite characters. Collectible figures ranging from affordable gashapon to high-end statues allow fans to bring iconic characters into their everyday lives. The appeal is not limited to children; adult collectors, often driven by nostalgia or artistic appreciation, make up a growing part of this market. These figurines usually feature intricate designs, high-quality finishes, and detailed craftsmanship, making them prized items among enthusiasts globally.

Apparel and accessories will grow at the fastest rate with a CAGR of 13.9%, projected to exceed US$ 5.9 Bn by 2033 due to their strong integration with fashion, pop culture, and personal identity. Anime-themed clothing such as t-shirts, hoodies, jackets, and caps, allows fans to visibly express their fandom in everyday life, blurring the lines between fashion and fandom. The rise of streetwear collaborations with major anime has propelled anime-inspired designs into mainstream fashion, particularly among Gen Z and millennial consumers who view anime as a core part of their cultural identity.

By Distribution Channel Insights - Online Channel Gains Traction Driven by Accessibility and Innovation

Online distribution channel dominates the market with over 53% market share and valuations exceeding US$ 5.7 Bn in 2026, with projected growth at a CAGR of 14.6%, due to their extensive reach and convenience. Company-operated direct-to-consumer websites and third-party marketplace integration provide global accessibility with reduced geographic friction. General e-commerce platforms including Amazon, eBay, and AliExpress command approximately 46% of online distribution channel share in 2026, facilitating consumer discovery and competitive pricing dynamics.

Offline channel is expected to hold over 40% market share by 2033, with specialty retail stores commanding approximately 49% of offline channel share in 2026. Physical retail outlets, pop-up stores, anime conventions, and themed cafes provide fans with a tangible connection to their favorite franchises, allowing them to see, touch, and engage with merchandise firsthand, something online platforms cannot replicate. Offline events often feature exclusive items, meet-and-greet opportunities, and limited-edition drops that drive foot traffic and purchases.

Regional Insights

North America Anime Merchandising Market Trends

The North America anime merchandising market is projected to reach US$ 3.2 Bn by 2033, with United States market valuations anticipated to exceed US$ 2.4 Bn. The region demonstrates rapid growth acceleration, fueled by expanding fanbase demographics, streaming platform availability, and established convention culture infrastructure. Streaming platform market penetration, particularly through Crunchyroll, Netflix, and specialized anime services, has created dedicated consumer segments with elevated merchandise acquisition propensities. In the U.S., celebrities such as rapper Megan Thee Stallion and Zion Williamson have publicly embraced anime, further fueling interest among Gen Z and millennials. Canada, anime has gained traction in educational curricula, libraries, and bookstores, integrating into youth culture and academic exploration. Events such as Anime North in Toronto frequently sell out, featuring hundreds of vendors and large fan gatherings.

Asia Pacific Anime Merchandising Market Trends

Asia Pacific dominates the global market, commanding over 65% market share by 2026 and reaching market valuations of US$ 7.0 Bn. Japan maintains exceptional market concentration, accounting for over 49% of global market share by 2026 with valuations exceeding US$ 5.2 Bn. Japan's position reflects historical IP creation advantage, established manufacturing infrastructure, and cultural institutionalization of anime consumption. Government support through the Cool Japan initiative, alongside trends like oshikatsu (personal fandom), which involved 14 million fans contributing ¥3.5 trillion (~ US$23 billion) in 2025, around 2.1% of total retail sales, demonstrates the cultural and economic depth of anime merchandise consumption.

China's cross-border e-commerce exports rose by 16.9% in 2024, noted by Ministry of Commerce, enabling easier access to Japanese merchandise, with China expected to exceed US$ 1.2 Bn market valuation by 2033. Korea’s vibrant youth culture, driven by cosplay and conventions, mirrors the popularity seen in K-pop. India’s is expected to grow at a CAGR of 15.2% due to the growing fandom that is gradually shifting towards legitimate merchandise purchases, aided by affordable streaming, though piracy challenges persist.

Europe Anime Merchandising Market Trends

Europe anime merchandising market is growing at CAGR of 10.8% and is expected to cross US$ 1.9 Bn by 2033. France and Germany represent dominant markets, with France commanding over 23% regional share and Germany maintaining approximately 20%. U.K. has seen a rapid growth in anime interest via mainstream platforms like BBC iPlayer and Netflix UK, with retail spaces like HMV adapting by adding anime-themed sections and events like MCM Comic Con fueling purchases. Regulatory harmonization through European Union frameworks creates operational efficiency benefits for continent-wide distribution strategies. Major cities, including Paris, Berlin, and London, establish anime convention infrastructure supporting merchandise commerce. Italy’s long-standing connection with anime, supported by early broadcasts on RAI and Mediaset, continues through nostalgia-driven demand for classics such as Sailor Moon and Naruto.

Competitive Landscape

The anime merchandising market is largely fragmented, with numerous small and mid-sized players competing alongside a few dominant global licensors. Companies are focusing on exclusive licensing agreements, collaborations with popular anime studios, and limited-edition product releases to create scarcity and drive demand. Many focus on diversifying product portfolios from apparel and collectibles to tech accessories to capture different fan segments. They often align product launches with anime premieres, movie releases, or fan events to maximize visibility and impact on sales.

Key Industry Developments

- In July 2025, Kyoto Animation revealed new visuals and exclusive merchandise for its 7th Fan Appreciation Event. The World of KyoAni Exhibition, scheduled for October 25-26, 2025. The event celebrates the studio’s creative legacy with limited-edition goods, behind-the-scenes artwork, and a commemorative book for fans.

- In July 2025, ITOCHU Corporation acquired merchandising rights for the popular character Npochamu in Asia (excluding Japan and South Korea) and North America (U.S. and Canada). The move comes as the global anime and character market, driven by social media popularity among Gen Z, is projected to reach $60.3 billion by 2030, growing at 9.8% annually.

- In June 2025, AnimationXpress launched Anime Originals, India’s first officially licensed anime merchandise platform. The initiative aims to provide high-quality, IP-safe products for Indian anime fans, celebrating local fandom with authenticity and passion.

Companies Covered in Anime Merchandising Market

- GOOD SMILE COMPANY

- Production I.G Inc.

- Studio Ghibli Inc.

- Toei Animation Co. Ltd.

- Bones Inc.

- Kyoto Animation Co. Ltd.

- Ufotable Co. Ltd.

- Bandai Namco Group

- JND STUDIOS

- SNAIL SHELL

- FUNKO

- Others

Frequently Asked Questions

The global anime merchandising market is projected to be valued at US$10.7 Bn in 2026.

The rising popularity of anime series, increasing fan engagement is a key market driver.

The anime merchandising market is expected to witness a CAGR of 9.3% from 2026 to 2033.

Print-on-demand services enable fans to personalize anime merchandise based on their favorite characters or moments, allowing brands to cater to niche tastes without holding large inventories present a significant opportunity.

GOOD SMILE COMPANY, Production I.G Inc., Studio Ghibli Inc., Toei Animation Co. Ltd., Bones Inc., Kyoto Animation Co. Ltd. are among the leading key players.