- Media & Entertainment

- Anime Market

Anime Market Size, Share, and Growth Forecast 2026 - 2033

Anime Market by Service Type (T.V. Series, Movie, Internet Distribution, Merchandising, Music, Others), Genre (Action & Adventure, Sci-fi Fantasy, Romance & Drama, Sports, Others), Regional Analysis for 2026 to 2033

Anime Market Size and Trend Analysis

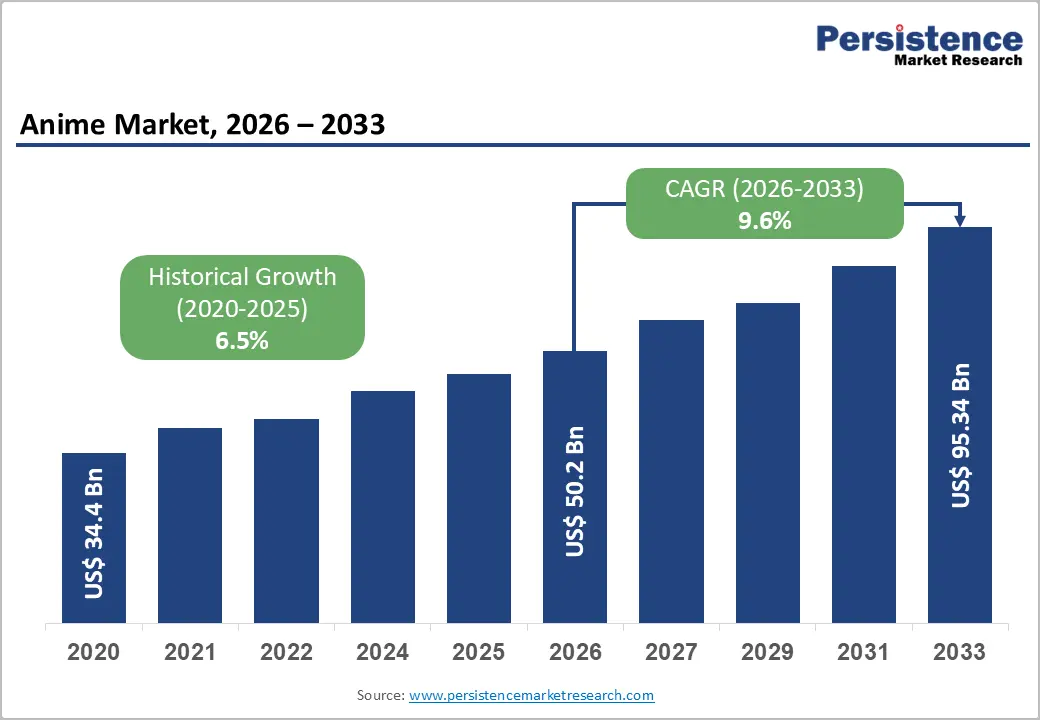

The global anime market size is likely to be valued at US$ 55.0 billion in 2026 and is projected to reach US$ 104.5 billion by 2033, growing at a CAGR of 9.6% between 2026 and 2033.

The market's robust expansion is primarily driven by the proliferation of streaming services and the increasing cultural acceptance of Japanese animation globally. Consumers are increasingly migrating from traditional cable television to on-demand Digital Platforms Market, allowing for simultaneous global releases that diminish the lag between Japanese broadcasts and international availability. Furthermore, the diversification of revenue streams beyond content distribution, into merchandising, live events, and music, creates a sustainable ecosystem where successful intellectual properties (IPs) generate value across multiple verticals. This growth is underpinned by the "conclusion first" principle: accessibility drives consumption, which in turn fuels production investment.

Key Industry Highlights:

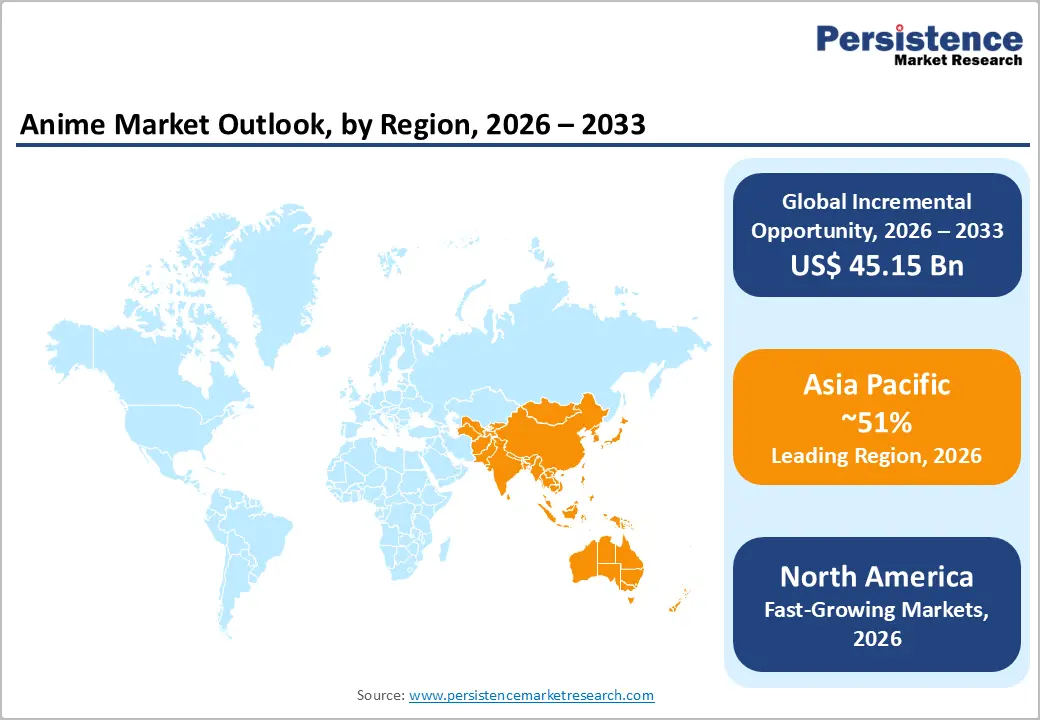

- Leading Region: Asia Pacific dominates the anime market, with 51% market share, due to Japan's production leadership and massive consumption in China.

- Fastest Growing Region: North America accelerates with mainstream streaming adoption and rising merchandise sales.

- Dominant Segment: Action & Adventure genre leads viewership, with 38% share, driving significant licensing and gaming revenue.

- Fastest Growing Segment: Internet Distribution surges as global audiences shift from TV to on-demand platforms.

- Key Market Opportunity: Expansion into Latin America and India offers vast untapped audience potential.

| Key Insights | Details |

|---|---|

| Anime Market Size (2026E) | US$ 55.0 Bn |

| Market Value Forecast (2033F) | US$ 104.5 Bn |

| Projected Growth CAGR (2026 - 2033) | 9.6% |

| Historical Market Growth (2020 - 2025) | 6.5% |

Market Dynamics

Drivers - Expansion of Global Streaming Platforms

The aggressive expansion of global streaming giants such as Netflix, Amazon Prime Video, and Disney+, alongside dedicated platforms like Crunchyroll, acts as a primary catalyst for market growth. These platforms are investing heavily in licensing and co-producing original anime content to differentiate their libraries and retain subscribers. Streaming services such as Netflix reported that anime viewership exceeded 1 billion global views in 2024, with over 50% of its global user base engaging with anime content. Crunchyroll surpassed 15 million monthly paid subscribers in August 2024, demonstrating the substantial international demand for anime series and films.

By localizing content through subtitles and dubbing in multiple languages, these services have dismantled language barriers that historically limited anime's reach. The Digital Platforms Market has fundamentally shifted the consumption model, enabling viewers in North America and Europe to access high-quality content instantly. This ubiquity has transformed anime from a niche subculture into a mainstream entertainment pillar, significantly increasing the total addressable audience and driving subscription revenues for production studios.

Diversification of Revenue Streams via Merchandising

The financial viability of anime production is increasingly supported by the Anime Merchandising Market, which extends the lifecycle of intellectual properties well beyond their broadcast dates. Global demand for anime-themed products, including action figures, apparel, collectibles, and lifestyle merchandise, has surged dramatically as fanbases expand beyond traditional geographic boundaries.

This trend is bolstered by the "media mix" strategy often employed by Japanese production committees, where a single narrative is simultaneously promoted across manga, anime, and merchandise. For instance, franchises like Demon Slayer, Attack on Titan, Jujutsu Kaisen, and One Piece generate substantial portions of their revenue from non-content sources. This diversification stabilizes studio income, mitigating the financial risks associated with high production costs and ensuring that popular series remain profitable even if advertising revenues fluctuate.

Market Restraints

Production Bottlenecks and Animator Labor Shortages

The anime industry faces a critical structural challenge in the form of severe labor shortages and animator burnout. According to Teikoku Databank analysis, anime studio revenues grew 23% to ¥339 billion in 2024, yet only 37% of studios experienced revenue growth, indicating concentrated profitability among major players. Smaller animation studios suffer particularly acute challenges, with only 57% of subcontractor studios achieving profitability compared to 78% of primary contractor studios.

Despite record-breaking revenues, the production pipeline is often bottlenecked by a lack of skilled labor, exacerbated by low entry-level wages and grueling working conditions in Japan. Many studios struggle to meet the insatiable global demand for new content, leading to production delays and quality control issues. This strain forces some studios to outsource work, potentially diluting the unique artistic style that defines the medium. If the industry fails to implement sustainable labor practices, the capacity to produce high-quality animation may plateau, restricting supply during a period of peak demand.

Market Saturation and Genre Fatigue

Genre oversaturation, particularly in the isekai category, which represented 15% of 2024 new anime releases, creates challenges for content differentiation and audience retention. The abundance of similar narrative structures and character archetypes reduces viewer engagement with individual titles, as competitive intensity increases across streaming platforms. Licensing competition intensifies acquisition costs, with platforms competing aggressively for exclusive rights to popular manga adaptations.

Market concentration among major studios, Toei Animation, MAPPA, and Ufotable limits production opportunities for smaller competitors, while animator exploitation concerns and work culture controversies generate reputational risks for the industry.

Opportunities - Integration of Advanced Technologies in Production

The integration of Artificial Intelligence (AI) and Computer-Generated Imagery (CGI) offers a transformative opportunity for the anime industry, closely tied to advancements in content creation tools. By leveraging sophisticated software for background rendering, in-betweening, and visual effects, studios can reduce their reliance on manual labor and optimize production workflows. This technological evolution enables faster delivery of visually compelling content, addressing the growing gap between demand and supply.

Leading studios such as Toei Animation and Studio Orange have successfully adopted 3D CGI alongside traditional 2D styles, expanding creative possibilities while maintaining artistic integrity. Additionally, hybrid monetization models, which combine ad-supported tiers with premium subscriptions, as evidenced by Netflix’s projected $1 billion in U.S. advertising revenue in 2024, unlock price-sensitive segments and enhance overall revenue performance.

Emerging Market Penetration and Regional Expansion

Although North America and Asia currently dominate the anime market, emerging regions such as Latin America, the Middle East, and India present substantial growth opportunities. These markets feature large, youthful populations with high internet penetration and increasing demand for global content. Japan’s Cool Japan initiative invested $827.9 million through fiscal 2022 to promote cultural exports, while the 2024 launch of JLOX+ introduced new subsidies for localization and international marketing.

Regions with advanced 5G connectivity exhibit higher streaming adoption and subscriber retention, with Asia-Pacific already accounting for 42% of global share. Strategic alliances between Japanese studios and regional platforms in ASEAN, India, and Brazil enable localized content and revenue diversification. Rising popularity of anime conventions and community events further signals latent demand, positioning these markets for the next wave of global expansion.

Category-wise Analysis

Service Type Insights

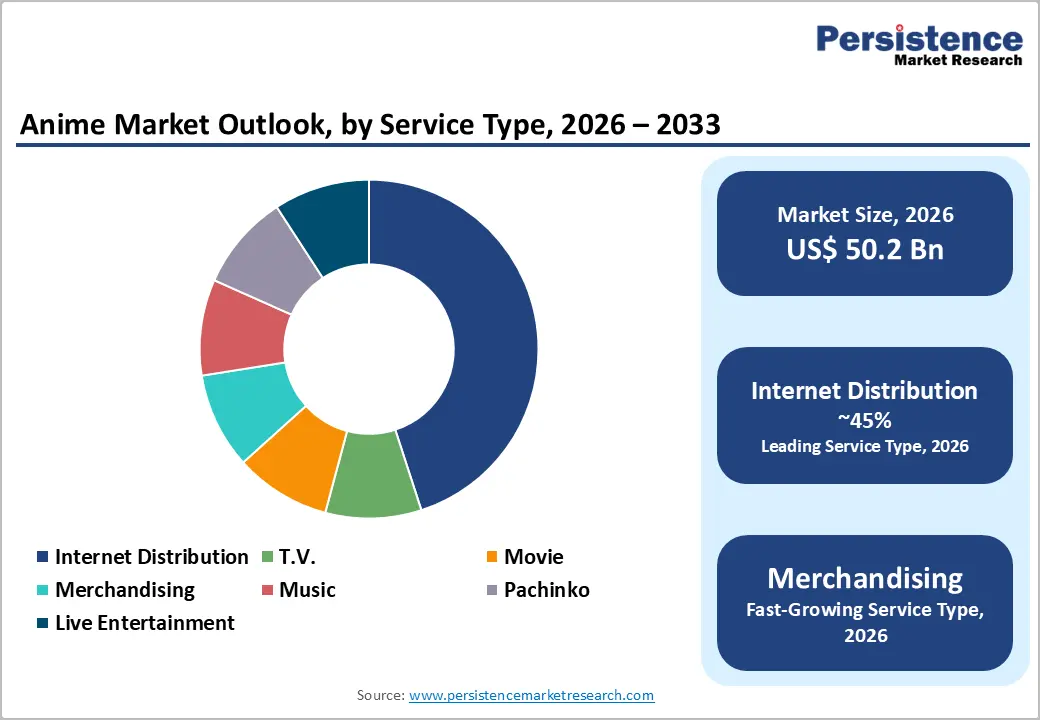

The Internet Distribution segment commands the leading share of the market, accounting for approximately 45% of total revenue. This dominance is justified by the rapid consumer shift away from traditional television broadcasting toward on-demand streaming services. Streaming platforms, including Netflix, Crunchyroll, Amazon Prime Video, and Disney+, have fundamentally reshaped anime consumption, enabling simultaneous global releases, multilingual content delivery, and seamless cross-device accessibility. Netflix contributed $2.07 billion in anime streaming revenue during 2023, representing 38% of global anime streaming revenue, validating platform investment strategies. The convenience of watching anytime, anywhere, combined with sophisticated recommendation algorithms, keeps viewer engagement high. Data from The Association of Japanese Animations (AJA) indicates a consistent year-over-year increase in overseas streaming revenue, validating the segment's supremacy as the primary delivery mechanism for global audiences.

Genre Insights

The Action & Adventure genre remains the undisputed leader, holding a market share of roughly 38%. This segment's preeminence is driven by "Shonen" anime, targeted primarily at young teen males but enjoyed universally, which features compelling hero journeys, high-stakes battles, and themes of friendship and perseverance. Franchises like One Piece, Naruto, Attack on Titan, Jujutsu Kaisen, and Dragon Ball fall under this category and have established multi-generational fanbases. These action-centric properties exhibit strong international appeal, particularly resonating with audiences in North America, Europe, and the Asia-Pacific regions. The visual spectacle inherent in action anime translates exceptionally well to merchandise and video game adaptations, creating a self-reinforcing cycle of popularity. The universal appeal of high-octane storytelling ensures this genre consistently attracts the largest viewership numbers across both domestic and international platforms.

Romance and drama genres maintain secondary significance with approximately 18% combined market share, while the rising isekai category, representing 15% of 2024 releases, demonstrates sustained but plateauing growth trends. Genre diversification, including sports, sci-fi fantasy, and niche categories, addresses specialized audience segments and reduces competitive intensity within dominant action-adventure categories.

Regional Insights

North America Anime Market Trends

North America is experiencing the fastest expansion in the global landscape, characterized by a surging mainstream acceptance of anime culture. The region benefits from a robust Digital Platforms Market ecosystem, with the U.S. serving as a critical export destination for Japanese content. Netflix commands 63% of U.S. anime viewers according to recent Dentsu consumer research spanning 10 countries with 8,600 respondents, validating massive platform investments in anime content libraries. Crunchyroll maintains the largest dedicated anime catalog exceeding 1,800 titles through JustWatch tracking, establishing specialized market positioning complementary to Netflix's broader entertainment portfolio.

High-profile collaborations, such as anime-inspired collections by major apparel brands like Nike and Uniqlo, signal the medium's deep penetration into pop culture. Furthermore, the theatrical success of anime films, with titles from Toei Animation and CoMix Wave Films achieving significant box office numbers, demonstrates a demand that transcends home viewing. The regulatory environment remains favorable for content licensing, fostering a dynamic exchange of intellectual property between Japanese licensors and American distributors.

Europe Anime Market Trends

Europe exhibits steady maturity, driven by historic strongholds in France and Spain, where manga and anime have enjoyed popularity for decades. France, in particular, stands as the second-largest consumer of manga globally after Japan, creating a fertile ground for anime adaptation success. The region is witnessing a trend toward regulatory harmonization regarding digital content, which simplifies cross-border streaming and licensing deals. European audiences exhibit strong engagement with anime streaming platforms, with Disney+ at 32% adoption and Prime Video at 29% according to Dentsu research, indicating diversified platform distribution compared to North American Netflix dominance.

European public broadcasters and cinema chains are increasingly dedicating slots to anime programming, acknowledging its cultural value. The rise of local conventions, such as Japan Expo in Paris, underscores the vibrant community engagement that sustains market momentum across the continent. E-commerce expansion facilitates anime product accessibility, with online retailing representing approximately 48% of merchandise market revenue in 2024, enabling direct-to-consumer sales, bypassing traditional retail limitations.

Asia Pacific Anime Market Trends

Asia Pacific retains the dominant market position, with 51%, anchored by Japan as the production hub and China as a massive consumer base. Japan retains approximately 40% of the global anime market value, maintaining historical production supremacy through major studios including Toei Animation, MAPPA, and Ufotable, which control premium intellectual property portfolios spanning decades. China emerges as the second-largest regional market, with platforms like Bilibili investing heavily in anime licensing and original production, capitalizing on massive youth demographics and improving digital infrastructure.

The region's growth is fueled by deeply ingrained cultural consumption habits and a well-established manufacturing ecosystem for the Anime Merchandising Market. In Japan, the industry is innovating with "2.5D musicals" (stage plays based on anime) and location-based entertainment, creating immersive experiences for domestic fans. Meanwhile, nations like South Korea and India are emerging as significant contributors; South Korea provides high-quality outsourcing studios, while India offers a rapidly growing audience base driven by affordable mobile data and youth demographics. The synergy between regional production capabilities and consumption creates a self-sustaining powerhouse for the industry.

Competitive Landscape

The global anime market structure is moderately fragmented but features a consolidated tier of top-heavy production powerhouses. Key players like Toei Animation and Aniplex (a subsidiary of Sony Group Corporation) wield significant influence due to their vertical integration capabilities, controlling everything from production and music to distribution and licensing. The market is characterized by the "Production Committee" system, where risk is shared among multiple stakeholders. However, a shift is occurring as streaming giants like Netflix fund entire projects directly, disrupting traditional financing models. Competition centers on securing top-tier creative talent and exclusive IP rights. Emerging trends include strategic acquisitions of animation studios by distribution companies to secure content pipelines and the increasing use of the Anime Content Creation Tools Market to differentiate visual styles.

Key Market Developments

- April 2022: Netflix announced a multi-year partnership with Studio Colorido to co-produce three new feature films, reinforcing its commitment to investing in original anime content rather than solely licensing existing titles.

- May 2024: Sony announced the development of its own animation production software named AnimeCanvas in collaboration with its subsidiaries, including Aniplex's A-1 Pictures and CloverWorks, to improve efficiency and quality in anime production.

- May 2025: Toei Animation vaunted its successful ventures and outlined plans, including a scheme to fold AI technology into many facets of its animation production pipeline.

Top Companies in the Anime Market

- Toei Animation (Tokyo, Japan) is a titan of the industry, responsible for legendary franchises like Dragon Ball, One Piece, and Sailor Moon. The company's strength lies in its massive library of legacy IPs, which generate consistent high-margin revenue through global licensing and merchandising. Toei continues to dominate the Action & Adventure genre and has successfully adapted to the digital era by partnering with major global streaming platforms.

- Aniplex (Japan) is a powerhouse in production and distribution, known for high-budget hits like Demon Slayer and Fate/Grand Order. The company operates a vertically integrated business model that encompasses music production, merchandise, and the ownership of A-1 Pictures and CloverWorks. Aniplex's strategic ownership of the streaming service Crunchyroll (via Sony) positions it uniquely to control the entire value chain from creation to consumption.

- Mappa (Japan) has rapidly ascended to the top tier of the industry, earning a reputation for high-quality animation and taking on ambitious projects like Jujutsu Kaisen and the final season of Attack on Titan. Known for its willingness to invest in diverse genres and darker themes, the studio has become a favorite among modern fans. Mappa is increasingly experimenting with direct financing models to retain greater creative control and profit share compared to the traditional committee system.

Companies Covered in Anime Market

- Toei Animation

- Mappa

- Ufotable

- Studio Bones

- Madhouse

- Kyoto Animation

- Production I.G.

- Studio Trigger

- A-1 Pictures

- Netflix

- Aniplex

Frequently Asked Questions

The global anime market is projected to reach a value of US$ 104.5 Bn by the end of 2033, driven by digital streaming and merchandise expansion.

The proliferation of global streaming platforms such as Netflix and Crunchyroll is the main driver, making content instantly accessible worldwide.

The Internet Distribution segment holds the leading market share, fueled by the global shift toward on-demand entertainment consumption.

North America is anticipated to be the fastest-growing region, supported by a booming fanbase and high engagement with digital platforms.

Expanding into emerging markets like Latin America and leveraging Anime Content Creation Tools Market technologies like AI offers significant growth potential.

Key market players include Toei Animation, Aniplex, Mappa, Netflix, and Production I.G., who lead in production and distribution.