- Media & Entertainment

- Animation and VFX Market

Animation and VFX Market Size, Share, and Growth Forecast, 2025 - 2032

Animation and VFX Market By Animation Platform (Television and OTT, Film, Advertising), Component (Software Solutions, Hardware Equipment, Services), Animation Technique (2D, 3D), by End-user, and Regional Analysis for 2025 - 2032

Animation and VFX Market Size and Trends Analysis

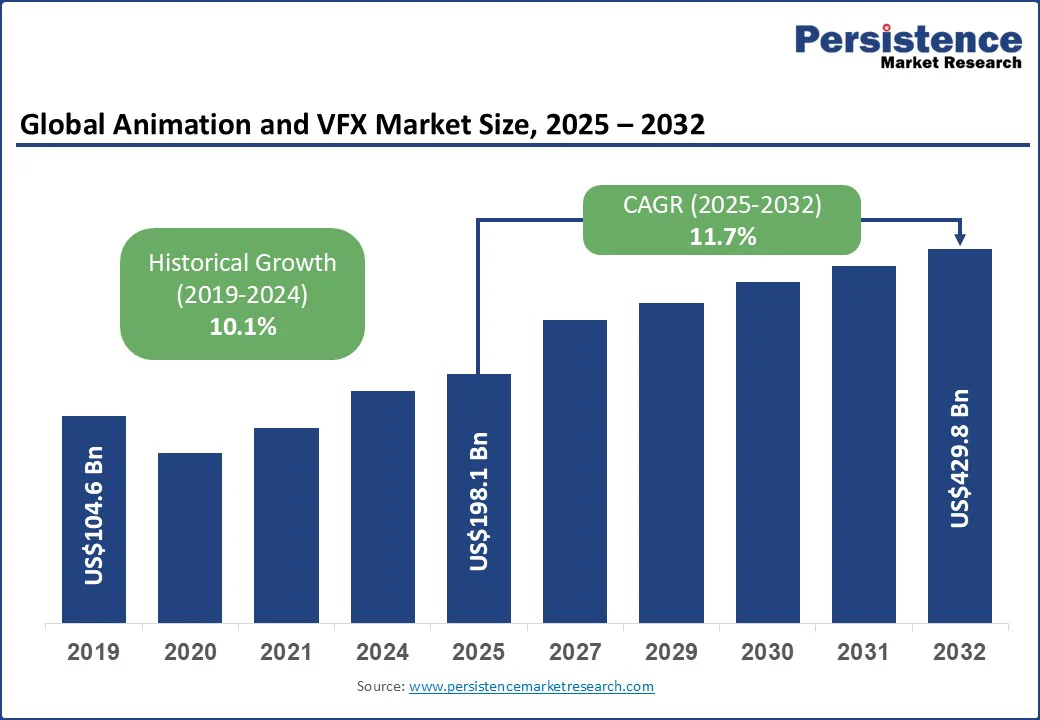

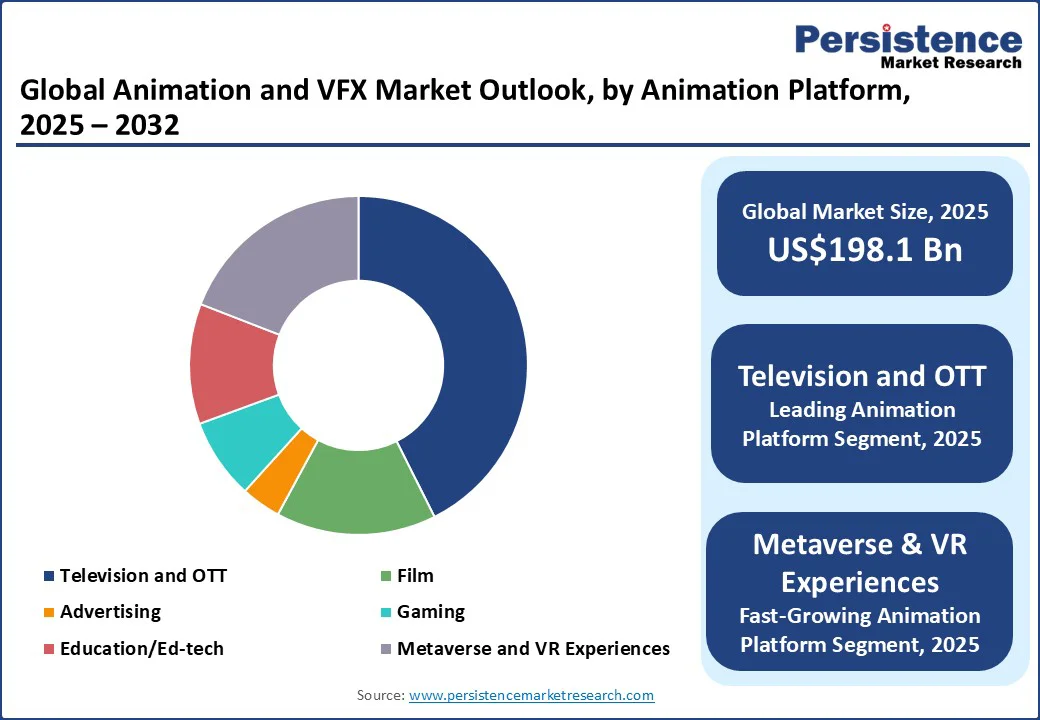

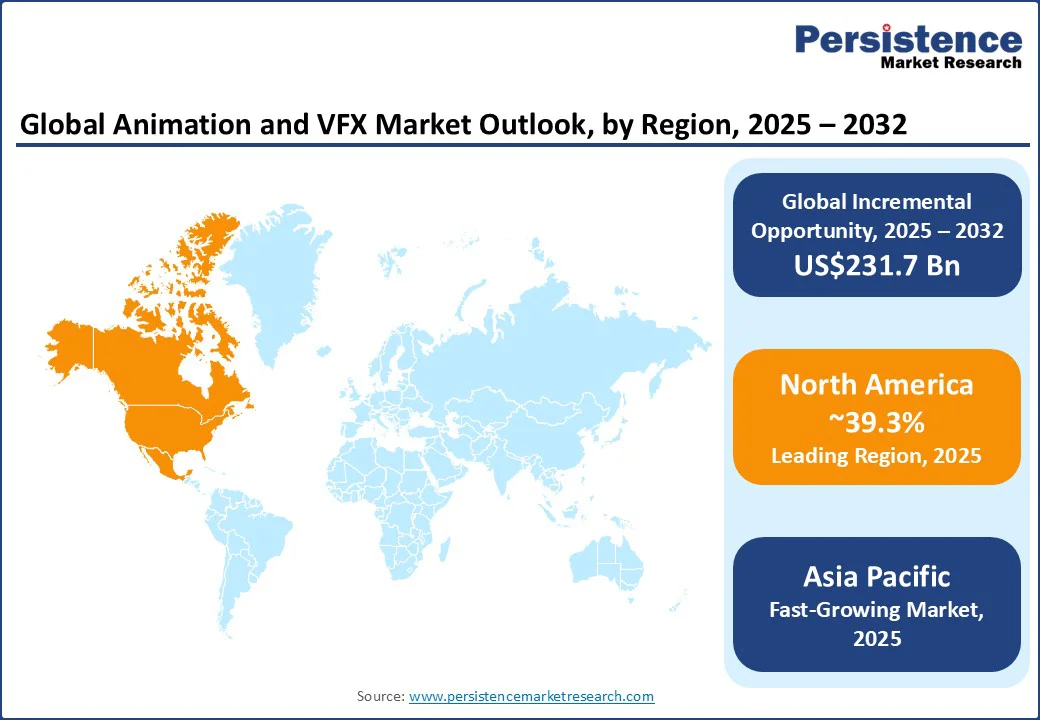

The global animation and VFX market size is likely to be valued at US$ 198.1 Bn in 2025 and is estimated to reach US$ 429.8 Bn in 2032, growing at a CAGR of 11.7% during the forecast period 2025 - 2032, spurred by the rapid expansion of digital streaming platforms, rising investments in AAA gaming and immersive experiences, and sustained global demand for high-quality animated content across various industries.

Key Industry Highlights:

- New Studio Launch: Former Assembly leaders Dave Zeevalk and Luiz Garrido founded a new VFX facility, Mosaic Studios, in January 2025. It is a fully operational, cloud-based VFX facility with a focus on high-end visual effects.

- Leading Region: North America, with about 39.3% share in 2025, backed by superior studio ecosystems, heavy streaming investments, and adoption of novel production technologies.

- Fastest-growing Region: Asia Pacific, owing to rising internet penetration, local content creation, and government incentives.

- Leading Animation Platform: Television and OTT, holding nearly 42.6% share in 2025, driven by surging global demand for original series and diverse regional content libraries.

- Dominant Component: Software solutions, approximately 49.4% of the animation and VFX market share in 2025, as AI-driven tools and real-time rendering help improve efficiency across production pipelines.

- Key Animation Technique: 3D animation recorded about 45.2% share in 2025, because gaming, films, and immersive experiences demand lifelike visuals and interactive storytelling.

| Key Insights | Details |

|---|---|

| Animation and VFX Market Size (2025E) | US$198.1 Bn |

| Market Value Forecast (2032F) | US$429.8 Bn |

| Projected Growth (CAGR 2025 to 2032) | 11.7% |

| Historical Market Growth (CAGR 2019 to 2024) | 10.1% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Growth Analysis - Rapid Growth in Streaming Platforms

Major subscription services are allocating unprecedented budgets for originals, with Disney and Netflix dedicating US$24 Bn and US$18 Bn, respectively, in 2025 to animated and VFX-rich content production.

These investments directly increase demand for novel animation, sophisticated simulations, and high-frame-count productions, raising the technical and creative standards across the industry. Supported by government incentives and a robust research and development ecosystem, especially in North America and Asia Pacific, this trend is expected to contribute a 2.1% uplift in CAGR over the next four years.

Technological Developments in Production

Real-time virtual-production techniques, adoption of 3D-enabled consumer devices such as AR/VR headsets, and cloud rendering platforms are driving operational transformation. Epic Games’ Unreal Engine and Autodesk’s suite of tools have streamlined content creation, cutting post-production cycles and lowering location costs.

With the cloud-native workflows enabling elastic compute and offsetting GPU shortages, the component sector expects a 14.42% CAGR for cloud rendering platforms between 2025 and 2032. Regulatory bodies such as ISO and national agencies are formalizing protocols around immersive content devices, bolstering enterprise and educational adoption.

Government Incentives and Expanding Studios

Countries including China, India, South Korea, and Japan have embraced lower production costs, tax incentive frameworks, and domestic IP development to become global animation and VFX outsourcing hubs. Asia Pacific is projected to rise at nearly 14.11% CAGR through 2032, surpassing all other regions.

Incentivization of local studios and increasing consumption of streaming and theatrical content drive expansion. China and India are mainly attracting international investment for art, tech, and story development.

Barrier Analysis- Talent Shortage and Skills Gap

A global shortage of senior VFX professionals, most acute in North America and Europe, threatens to constrain delivery capacity. Despite estimations of 2 million new Animation, Visual Effects, Gaming, and Comics (AVGC) jobs by 2032, current training and upskilling programs lag technological adoption, potentially reducing market CAGR by 1.4% in the near term. Unions and advocacy groups are pushing for improved work conditions, further impacting cost structures and time-to-market.

High Initial Investments and Operational Costs

Launching and expanding a competitive animation/VFX studio requires multimillion-dollar investments in hardware infrastructure, including high-end workstations and rendering farms, software licenses, and top-tier artistic talent.

Industry consolidation and difficulty accessing capital present high entry barriers, concentrating the market among a handful of transnational players. Competitive threats from vertically integrated hardware/software companies such as NVIDIA and Apple, as well as persistent supply chain volatility in GPU chips, further challenge new entrants.

Opportunity Analysis - Emerging Markets and Localized Content Creation

Regions in Asia Pacific and Latin America present key untapped potential, especially in local language animated features, ed-tech content, and niche gaming platforms. The regional animation/VFX market is forecast to exceed US$100 Bn by 2032 with accelerated new studio formation and IP development. Government policies focused on skills development and tax benefits are predicted to unlock additional value.

Global and regional OTT providers are constantly investing in exclusive animated series and VFX-heavy productions to differentiate their content libraries. This shift is fueling opportunities for independent studios to pitch original IPs and secure long-term licensing deals across multiple geographies.

Technological Convergence in AR/VR and Metaverse

The metaverse, VR experiences, and spatial-computing device adoption represent the fastest-growing segment, with a projected 15.7% CAGR to 2032. Studios that are agile in repurposing character rigs and environments across interactive endpoints are positioned to dominate new monetization channels. The deployment of AI in animation and VFX pipelines is streamlining processes such as rotoscoping, motion capture cleanup, and facial rigging.

It not only reduces turnaround times but also lowers production costs, allowing studios to allocate more resources toward creative innovation and storytelling. Demand for region-specific animated series and films is increasing. Advanced dubbing, subtitling, and culturally adaptive animation techniques are creating new growth avenues for studios targeting local audiences while maintaining global appeal.

Digital Advertising and Social Media Integration

Election cycles and the expansion of influencer-led campaigns on platforms with 4+ billion users propel unprecedented demand for animation/VFX in short-form content and digital advertisements. As brands increase online ad spending, which is surging at 18% YoY globally as per UNESCO, animation studios can develop unique promotional assets, expanding both reach and revenue.

Strategic partnerships with cloud providers, AI developers, and hardware manufacturers are transforming the production ecosystem. Studios integrating GPU-accelerated rendering, motion capture, and AI-based editing tools can expand projects faster while maintaining cinematic quality, positioning themselves as preferred partners for global content creators.

Category-wise Analysis

Animation Platform Insights

The television and OTT segment is anticipated to remain market leaders, capturing nearly 42.6% of global share in 2025. This dominance is fueled by the on-demand consumption of animated series and movies on streaming platforms and ongoing investments in exclusive content libraries such as Netflix Originals and Disney+.

Metaverse and VR experiences are projected to witness steady growth through 2032. The proliferation of spatial-computing devices and immersive technology in gaming, virtual events, and education creates new opportunities for asset reuse and cross-platform revenue. The adoption of real-time rendering and LED volume stages is transforming how films and series are produced.

Component Insights

Software solutions are expected to account for approximately 49.4% of the market share in 2025. Subscription-based licensing models (Autodesk, Adobe, Unity) and the integration of AI-based automation (rotoscoping, matte extraction) have pushed recurring revenue and workflow efficiencies. Cloud migration and the rise of plug-ins for asset orchestration are further consolidating software leadership.

Cloud rendering platforms are predicted to expand at nearly 14.4% CAGR in the forecast period, delivering elastic computing capacity and reducing CAPEX for studios, especially in hardware-constrained markets. Developments in GPU technology and real-time rendering engines are enabling near-instant previews of complex visual sequences. This accelerates decision-making for directors and producers, while also lowering iteration costs and improving collaboration between geographically dispersed teams.

Animation Technique Insights

3D animation is predicted to hold around 45.2% of the market share in 2025. Its widespread adoption in films, AAA games, VR, and healthcare visualization has ensured sectoral dominance. Innovations in neural rendering and AI-based tools are augmenting production output and creative complexity.

Interactive motion graphics and stylized techniques for advertising and streaming portals contribute to portfolio diversification, boosted by improved pipeline efficiency. Companies are embracing dynamic motion graphics to deliver personalized campaigns across social media and OTT platforms. Adaptive templates and data-driven visuals allow studios to expand content production while maintaining audience relevance.

Regional Insights

North America Animation and VFX Market Trends

North America is poised to account for approximately 39.3% of the market share in 2025, benefiting from studio concentration such as Disney, Pixar, and Industrial Light & Magic. In addition, unionized talent pools and robust incentives, including California’s US$750 Mn fund, are pushing the regional market. Growth is further attributed to continuous technological innovation, strong regulatory support for IP protection, and mature vendor ecosystems close to decision-making hubs.

Increased sports animation, advertising, and healthcare visualization bolster diversification. Investment trends favor real-time virtual staging and cloud migration, with capital flowing into proprietary IP and AI partnerships.

Asia Pacific Animation and VFX Market Trends

Asia Pacific is the fastest-growing region, led by China, Japan, India, and ASEAN. Manufacturing advantages, lower costs, and superior training pipelines attract outsourcing contracts and international IP investment.

Government incentives, including India’s VFX tax breaks, and regulatory frameworks for local content ensure rising domestic production. Streaming and theatrical content consumption surge as cultural exports fuel global interest in domestic studios. Investment trends prioritize studio expansions, proprietary rigs, and AI-enabled render farms.

Europe Animation and VFX Market Trends

Europe sustains growth via cultural funding frameworks, co-production treaties, and competitive rebates. The U.K.’s 39% VFX rebate and France’s TRIP program are creating new growth prospects. Germany, the U.K., France, and Spain lead production volumes, while Eastern European hubs absorb overspill via multilingual crews and currency advantages.

Regulatory harmonization and public policy support through the EU Digital Content directives ensure steady cross-border project flows. Investment focuses on high-end television, arthouse ventures, and pan-European distribution, with technology adoption improving efficiency.

Competitive Landscape

The global animation and VFX market is fragmented but consolidating, with some 80% of global output concentrated among 10 leading multinational studios. While legacy titans such as Industrial Light & Magic, Weta FX, and DNEG command marquee projects, asset acquisitions and buyouts are changing scale and capability. Independent studios remain competitive due to developments in AI, cloud migration, and labor cost arbitrage.

Business Strategies

Market leaders pursue innovation, cost optimization, and geographic expansion as core themes. AI-enabled automation, proprietary IP, and transparent workforce management are key differentiators. Emerging business models include usage-based cloud economics, subscription licensing, and cross-industry pipelines such as media, healthcare, and advertising.

Key Industry Developments

- In May 2025, Union Minister of Information and Broadcasting Ashwini Vaishnaw announced the launch of the Indian Institute of Creative Technology (IICT) in Mumbai. This launch aims to boost animation, gaming, and digital arts in India.

- In February 2024, the Walt Disney Company announced an investment of US$1.5 Bn to acquire an equity stake in Fortnite maker Epic Games. As part of the investment, the two companies will collaborate on the creation of what they describe as a new persistent universe.

Companies Covered in Animation and VFX Market

- Disney Animation/Pixar

- Sony Pictures Imageworks

- Netflix Animation

- Industrial Light & Magic

- Weta FX

- DNEG

- Framestore

- Moving Picture Company

- Technicolor Creative

- Blue Bolt

- 3D Matchmovers

- Rocket Science VFX

- Adobe Inc.

- Autodesk

- Method Studios

- Rhythm & Hues

Frequently Asked Questions

The animation and VFX market is projected to reach US$198.1 Bn in 2025.

Increasing demand for animated content across OTT platforms and rising adoption of VFX in advertising are the key market drivers.

The animation and VFX market is poised to witness a CAGR of 11.7% from 2025 to 2032.

Expansion of virtual production techniques in filmmaking and the high popularity of 3D animation in education are the key market opportunities.

Disney Animation/Pixar, Sony Pictures Imageworks, and Netflix Animation are a few key market players.