- Specialty & Fine Chemicals

- Alkyl Polyglucoside Surfactants Market

Alkyl Polyglucoside Surfactants Market Size, Share, and Growth Forecast 2026 - 2033

Alkyl Polyglucoside Surfactants Market by Application (Personal care & cosmetics, Home Care, Industrial Application, Textile, Others), and Regional Analysis, 2026 - 2033

Alkyl Polyglucoside Surfactants Market Size and Trend Analysis

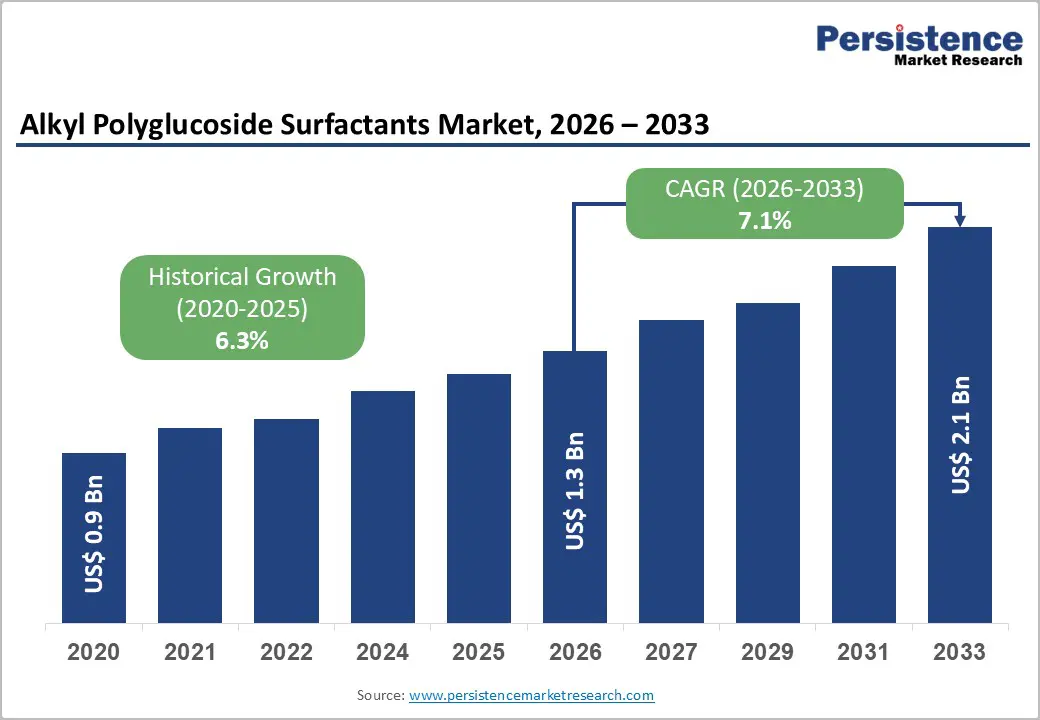

The global Alkyl Polyglucoside (APG) Surfactants market is projected to reach US$ 1.3 billion in 2026 and US$ 2.1 billion by 2033, growing at a CAGR of 7.1% from 2026 to 2033.

This growth is underpinned by tighter environmental regulations, rapid adoption of biodegradable ingredients, and rising consumer demand for greener products. REACH-driven compliance, the expansion of eco-label programs, and advances in bio-based manufacturing are accelerating APG penetration. Increasing disposable incomes, especially across the Asia-Pacific region, are further boosting the use of sulfate-free shampoos, baby care products, and sustainable home-care formulations.

Key Market Highlights

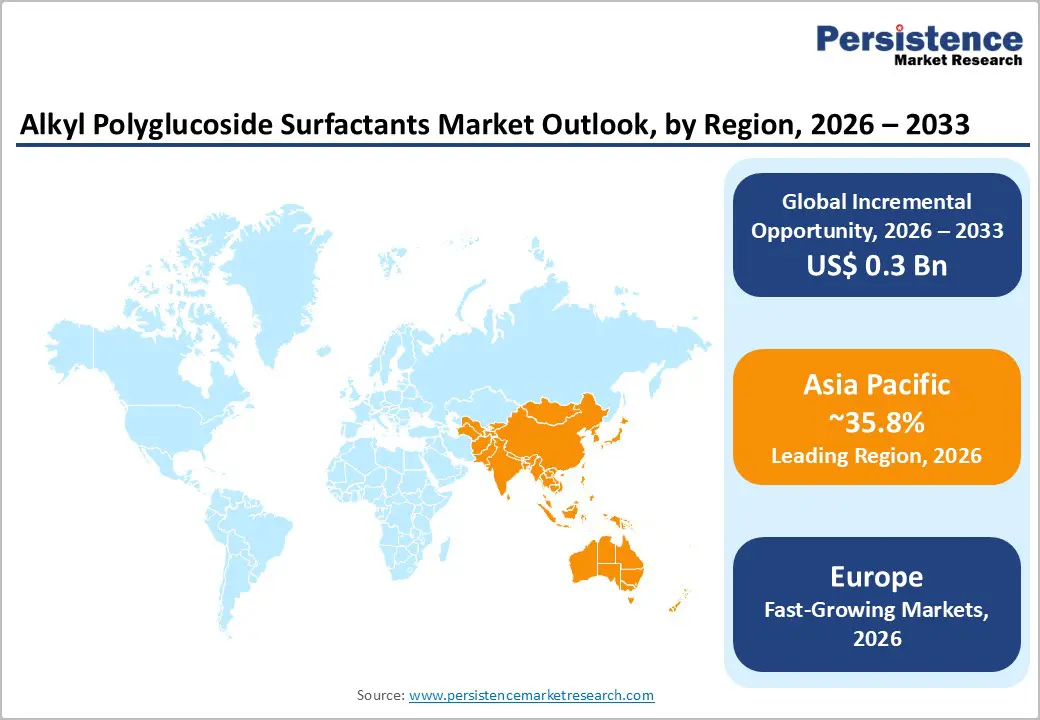

- Leading Region: Asia Pacific holds 35.8% of global market value, supported by urbanization, rising incomes, and strong bio-based policy momentum.

- Fastest Growing Region: Asia Pacific leads growth, with China rising 7.3% annually and India at 6.8%, outpacing developed markets.

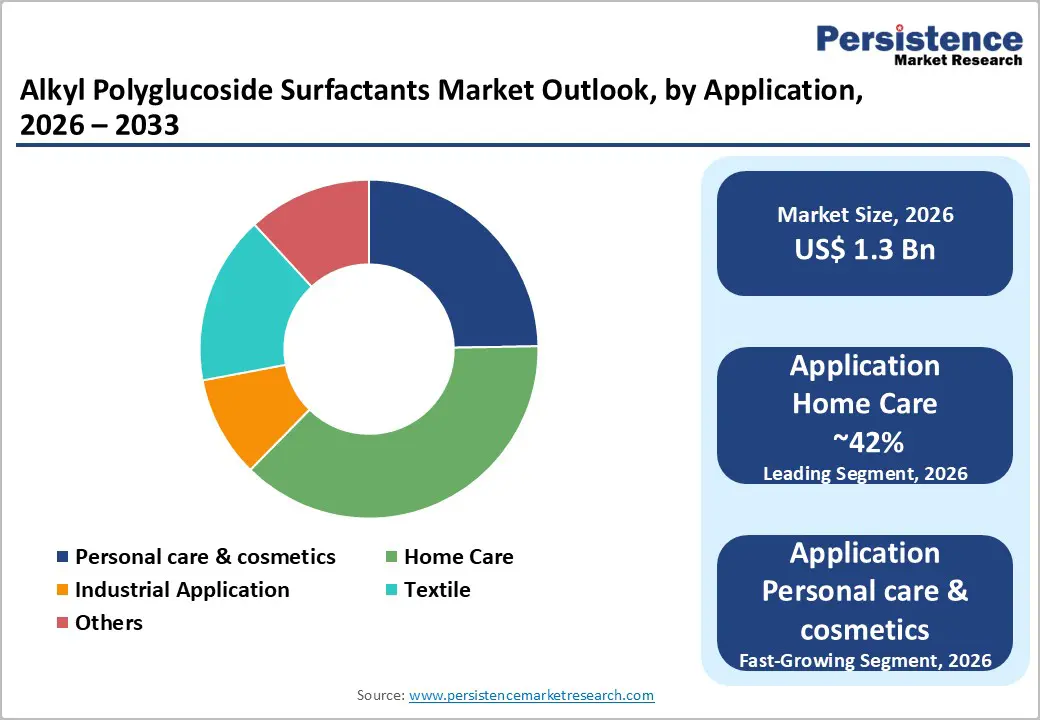

- Dominant Application Segment: Home care accounts for 42% of global value, led by laundry detergents, dishwashing liquids, and surface cleaners.

- Fastest-Growing Application Segment: Personal care & cosmetics grow fastest at ~7.8% annually, capturing 39% through sulfate-free and premium formulations.

- Key Market Opportunity: Industrial uses expand, with ~52% of modern agrochemical formulations integrating APGs, broadening revenue across multiple sectors.

| Key Insights | Details |

|---|---|

|

Alkyl Polyglucoside Surfactants Market Size (2026E) |

US$ 1.3 Billion |

|

Market Value Forecast (2033F) |

US$ 2.1 Billion |

|

Projected Growth CAGR (2026-2033) |

7.1% |

|

Historical Market Growth (2020-2025) |

6.3% |

Market Dynamics

Market Growth Drivers

Escalating Consumer Demand for Biodegradable and Non-Toxic Surfactants

Growing environmental awareness is reshaping consumer choices across personal care and home care categories. APGs, produced from renewable sugars and plant-derived fatty alcohols, are fully biodegradable and leave no toxic residues in aquatic systems. Compared with conventional sulfated surfactants, they offer improved mildness, reduced irritation, and safer performance for sensitive-skin and baby formulations.

Their compatibility with eco-label requirements and natural certifications further accelerates market adoption. Regulatory frameworks encouraging the phase-out of harsh sulfates, alongside brand commitments to sustainability, are strengthening APG's positioning as a preferred alternative. Rising penetration in eco-labeled home care portfolios highlights how environmental compliance combined with consumer trust is driving sustained demand across premium and mass-market product lines.

Expanding Industrial Applications Beyond Traditional Personal Care Markets

Beyond household and cosmetic formulations, APGs are gaining strong traction across regulated industrial environments. In agriculture, they function as efficient adjuvants, improving wetting, spreading, and penetration of active ingredients while helping reduce overall chemical load. Their stability under varied pH conditions and low toxicity profile make them attractive across precision farming and crop protection systems.

In textiles, food processing, and oilfield operations, APGs offer performance advantages, including effective cleaning, controlled foaming, and compatibility with sensitive equipment and wastewater systems. Their biodegradability supports compliance with tightening industrial discharge standards. As more sectors transition toward safer chemistries, diversified APG usage reduces market dependency on consumer cycles and supports resilient, long-term growth.

Market Restraints

Raw Material Cost Volatility and Supply Chain Constraints

APG production remains highly exposed to fluctuations in glucose and plant-derived fatty alcohol prices, which account for the majority of manufacturing inputs. Agricultural cycles, climate impacts, and competing demand from biofuels and food processing amplify price instability, while geographically concentrated coconut and palm kernel oil supplies heighten supply-security risk and periodic scarcity.

Tight margins make APG producers particularly vulnerable to inflation in feedstock costs and logistics disruptions. Limited alternative raw material sources and slow agricultural expansion cycles restrict the industry’s ability to scale production quickly. These dynamics create periodic cost spikes, supply bottlenecks, and restrained profitability, ultimately slowing investment momentum and limiting faster market expansion despite growing demand for bio-based surfactants.

Higher Production Complexity Compared to Conventional Surfactants

APG manufacturing involves more complex chemistry, tighter process control, and rigorous quality monitoring than traditional surfactants. Multi-stage reactions, precise temperature management, and control over the degree of polymerization increase operational difficulty and risk of variability. Maintaining consistent performance characteristics requires advanced analytical capability and disciplined production oversight.

Capital expenditure requirements for APG facilities are higher, creating financial barriers for new entrants and limiting capacity expansion in emerging regions. Skilled technical expertise remains scarce, while compliance with diverse regulatory, toxicology, and eco-labeling standards elevates development costs. Together, these structural challenges keep production costs elevated and slow broader industrial adoption.

Market Opportunities

Surge in Sulfate-Free and Mild Formulation Demand for Premium Personal Care

Premium beauty brands are rapidly transitioning toward sulfate-free and dermatologically safe formulations, opening a strong opportunity for APGs due to their mild cleansing profile and compatibility with natural actives. APGs deliver gentle foaming, improved skin tolerance, and strong performance in formulations positioned for “clean,” “vegan,” and “eco-certified” claims, aligning closely with evolving consumer expectations across global premium segments.

Baby care and sensitive-skin categories are expanding especially fast, with APG-based products earning measurable price premiums as shoppers prioritize safety credentials and sustainability messaging. Premium lines command higher margins despite lower volumes, enabling formulators and suppliers to capture value through differentiated positioning. As brands emphasize efficacy paired with gentleness, APG adoption is expected to rise significantly across dermatology-inspired and high-end personal care portfolios.

Geographic Expansion in Asia Pacific and Emerging Market Agrochemical Applications

Asia Pacific is emerging as a key APG demand hub as rising incomes, rapid urbanization, and sustainability awareness accelerate interest in biodegradable personal and home care products. Localized production expansions by leading manufacturers are improving availability and reducing logistics costs, creating competitive advantages for brands adopting bio-based ingredients in high-growth consumer markets.

Simultaneously, the modernization of agriculture across emerging markets is unlocking opportunities for APG-based adjuvants that improve pesticide spread, penetration, and environmental safety. Supportive policy frameworks promoting green chemistry, combined with limited regional capacity, create space for contract manufacturers and specialty formulators. As supply builds and regulatory incentives strengthen, APGs are positioned to capture sustained, above-average growth across both consumer and industrial applications in the Asia Pacific and beyond.

Category-wise Analysis

Application Insights

The alkyl polyglucoside surfactants market is led by the home care segment, accounting for around 42% of global value. APGs are widely adopted across dishwashing liquids, laundry detergents, and surface cleaners, where they enhance foam stability, reduce irritation, and strengthen biodegradability credentials. Regulatory pressure favoring eco-labeled cleaning solutions and their compatibility with cold-water formulations further reinforces APGs as indispensable surfactants in high-volume household and institutional cleaning products.

The fastest-growing opportunity emerges in personal care and cosmetics, as formulators pivot toward sulfate-free, mild, and plant-derived cleansing systems. APGs deliver gentle yet effective performance in shampoos, body washes, facial cleansers, and baby care lines, aligning with clean-label, dermatologically safe, and sustainability-driven positioning. Expanding roles in premium, anti-aging, and sensitive-skin formulations continue to accelerate adoption across global beauty portfolios.

Regional Insights

North America Alkyl Polyglucoside Surfactants Market Trends

North America represents a mature APG market, accounting for about 30.1% of global value, shaped by strong regulatory oversight and premium consumer positioning. The U.S. leads regional demand as personal care and home care brands emphasize clean-label, biodegradable surfactants. Retail channels clearly differentiate mass-market versus premium categories, enabling APGs to capture higher-margin product opportunities.

Domestic supply strength reinforces adoption, supported by BASF’s capacity additions in Cincinnati and secure trans-Atlantic integration with Europe. Environmental policies mandating biodegradability across states encourage formulators to shift toward APGs as future-proof ingredients. Ongoing partnerships and portfolio consolidation highlight APGs’ strategic importance, particularly in sulfate-free shampoos, sensitive-skin cleansers, and next-generation institutional cleaners.

Europe Alkyl Polyglucoside Surfactants Market Trends

Europe is the global reference market for APGs, driven by advanced sustainability standards, REACH compliance, and strong institutional support for renewable chemistry. Regulatory tightening around toxicity, biodegradability, and animal testing creates natural advantages for APGs, reinforcing their presence in personal care, detergents, and specialty cleaning formulations across key markets, including Germany, France, and the UK.

The region demonstrates steady growth, expanding at a CAGR of around 6.6%, supported by robust domestic production, harmonized regulations, and strong penetration in premium beauty portfolios. ESG disclosure requirements and traceable renewable feedstocks further accelerate adoption, favoring suppliers with transparent value chains and technical documentation. APGs increasingly influence mainstream product reformulation strategies across Europe’s consumer and industrial sectors.

Asia Pacific Alkyl Polyglucoside Surfactants Market Trends

Asia Pacific is the largest and fastest-expanding region, accounting for about 35.8% of global market value, driven by urbanization, growing middle-class consumption, and policy support for bio-based chemicals. China leads with scaling production capacity and rapid premiumization trends in home care and personal care categories, incorporating mild, sustainable surfactants.

India and Japan add complementary growth dynamics. India, through modernization of cleaning products and agrochemical adjuvants, and Japan, through high-end, dermatology-focused formulations. Strategic production expansions, including BASF’s Thailand capacity builds and regional glucose and fatty-alcohol supply integration, improve logistics, pricing resilience, and responsiveness. Strengthening regional ecosystems continues to anchor APGs as core ingredients across diversified downstream industries.

Competitive Landscape

The APG surfactants market is moderately consolidated, characterized by large global producers with integrated production networks, strong distribution capabilities, and deep technical expertise. Competitive advantage is shaped by control over feedstocks, sustainability certifications, and the ability to support formulators with technical documentation and application-specific guidance across personal care, home care, and industrial segments.

Competition is increasingly driven by innovation, including specialized APG grades, blended systems, and performance-enhancing additives aligned with clean-label expectations. New regional entrants are intensifying price pressure through cost-efficient production and proximity-based supply models, while industry leaders focus on partnerships, process optimization, and next-generation bio-based technologies to extend performance and protect margins.

Key Market Developments

- In November 2025, BASF inaugurated expanded Alkyl Polyglucosides production capacity at Bangpakong, Thailand, enhancing regional supply capabilities and enabling faster, more flexible customer service across Asia Pacific markets.

- In November 2025, the European Union approved the new Detergents and Surfactants Regulation, strengthening biodegradability requirements, prohibiting animal testing, and establishing digital product passport requirements, creating favorable competitive dynamics for established APG suppliers with comprehensive safety documentation.

- In November 2025, BASF announced scheduled completion of new APG production line at Cincinnati, Ohio facility in 2026, substantially increasing North American capacity and supporting downstream formulator expansion in U.S. and Canadian markets.

Companies Covered in Alkyl Polyglucoside Surfactants Market

- BASF SE

- Clariant AG

- Croda International Plc

- SEPPIC (Air Liquide)

- Evonik Industries

- Kao Corporation

- Galaxy Surfactants Ltd.

- Shanghai Fine Chemical Co., Ltd.

- Yangzhou Chenhua New Material Co., Ltd.

- Fenchem Biotek

- Stepan Company

- Sasol Limited

- Pilot Chemical Company

- Dow

- Huntsman Corporation

Frequently Asked Questions

The global Alkyl Polyglucoside Surfactants market is projected to reach US$ 2.1 Billion by 2033, up from US$ 1.3 Billion in 2026 at a 7.1% CAGR, driven by demand for biodegradable, sustainable surfactants.

Demand is fueled by biodegradable and non-toxic surfactant preference, strict EU REACH biodegradability rules, growth in agrochemicals and textiles, and rising Asia Pacific incomes.

Home care leads with ~42% of global value, while personal care and cosmetics is the fastest-growing segment at ~7.8% annually.

Asia Pacific leads with ~35.8% of global market value, supported by strong manufacturing bases, sustainability policies, and expanding consumer demand.

Key opportunities span premium personal care and baby care, agrochemical adjuvants, industrial and textile cleaning, and expansion in underpenetrated emerging markets.

Major market players include BASF SE, Croda International Plc, Clariant AG, Kao Corporation, Evonik Industries, SEPPIC.