- Specialty & Fine Chemicals

- Alkyl Phenol Derivatives Market

Alkyl Phenol Derivatives Market Size, Trends, Share, and Growth Forecast 2025 - 2032

Alkyl Phenol Derivatives Market by Product Type (Para-tert-butyl-phenol (PTBP), 2,4-di-tert-butyl-phenol (2,4 DTBP), 2,6-di-tert-butyl-phenol (2,6 DTBP), Para-octyl phenol (POP)), Application, End-user, and Regional Analysis for 2025 - 2032

Alkyl Phenol Derivatives Market Size and Trend Analysis

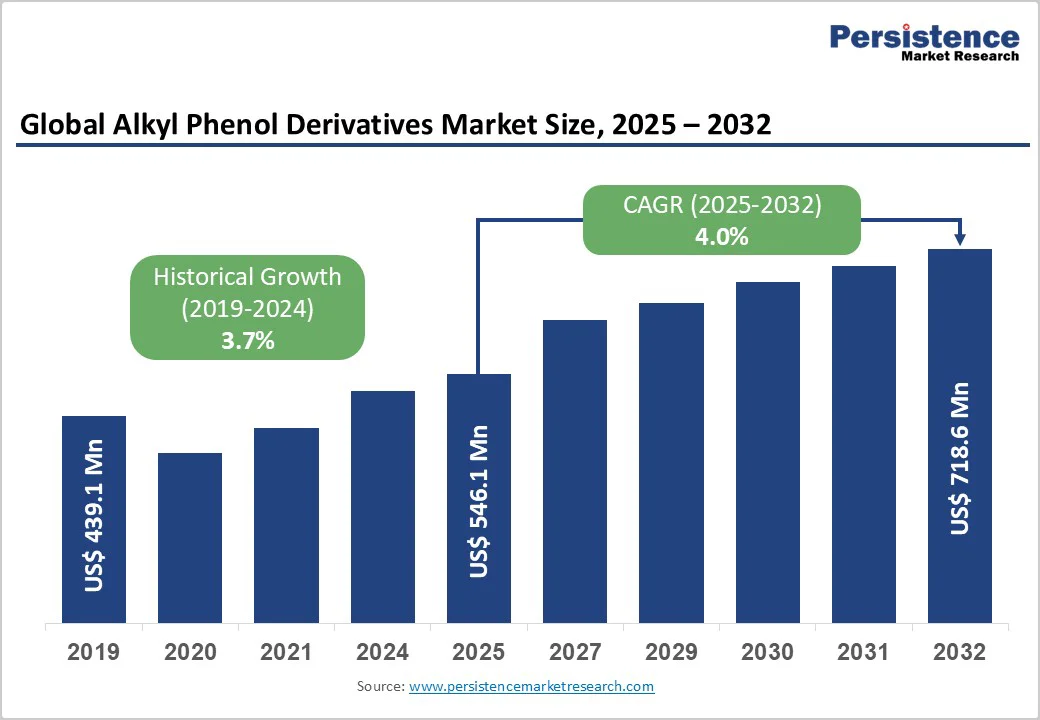

The global alkyl phenol derivatives market size is likely to value at US$ 546.1 million in 2025 and is projected to reach US$ 718.6 million by 2032, growing at a CAGR of 4.0% between 2025 and 2032.

The primary drivers include surging demand from the construction and automotive sectors for high-performance materials such as phenolic resins and coatings, supported by global infrastructure investments exceeding US$ 9 trillion annually.

According to the U.S. Census Bureau, construction spending reached a seasonally adjusted annual rate of $2.13 trillion in August 2024, representing a 4.1% increase from August 2023, which directly stimulates demand for coating formulations incorporating these derivatives.

Key Industry Highlights:

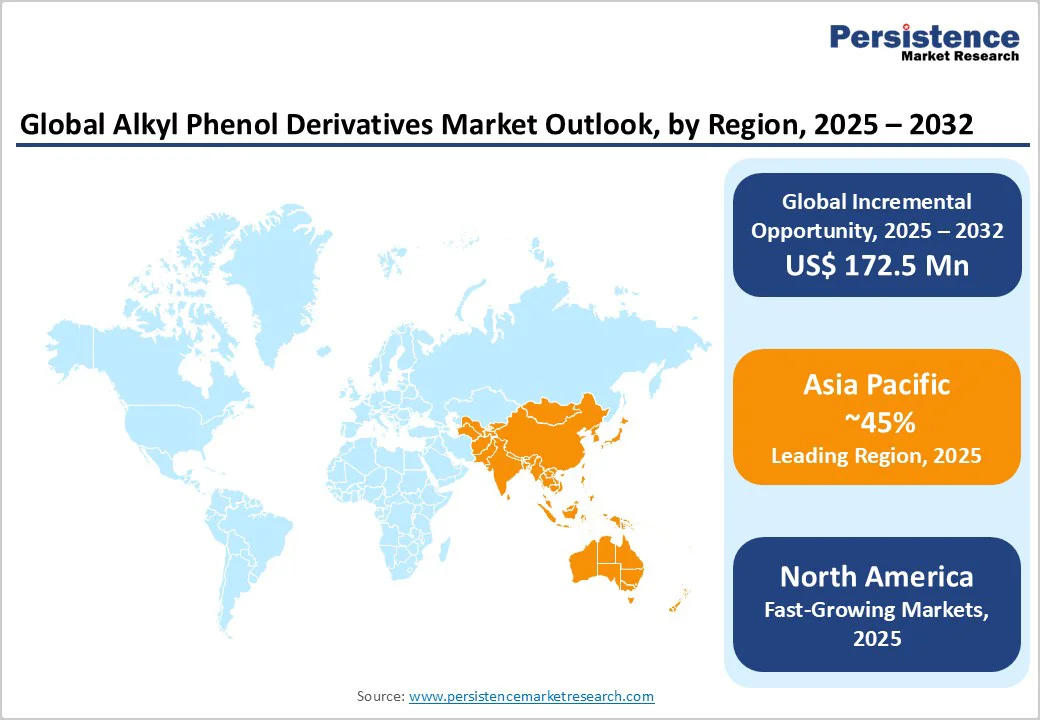

- Regional Leader: Asia Pacific leads the alkyl phenol derivatives market, driven by rapid industrialization and manufacturing hubs in China and India, capturing over 45% global share through phenolic resin demand.

- Fastest Growing Region: North America emerges as the fastest-growing region, propelled by the U.S. innovations in sustainable coatings and EV materials.

- Leading Segment: Para-tert-butyl-phenol (PTBP) dominates the product type category in the alkyl phenol derivatives market, holding approximately 50% market share.

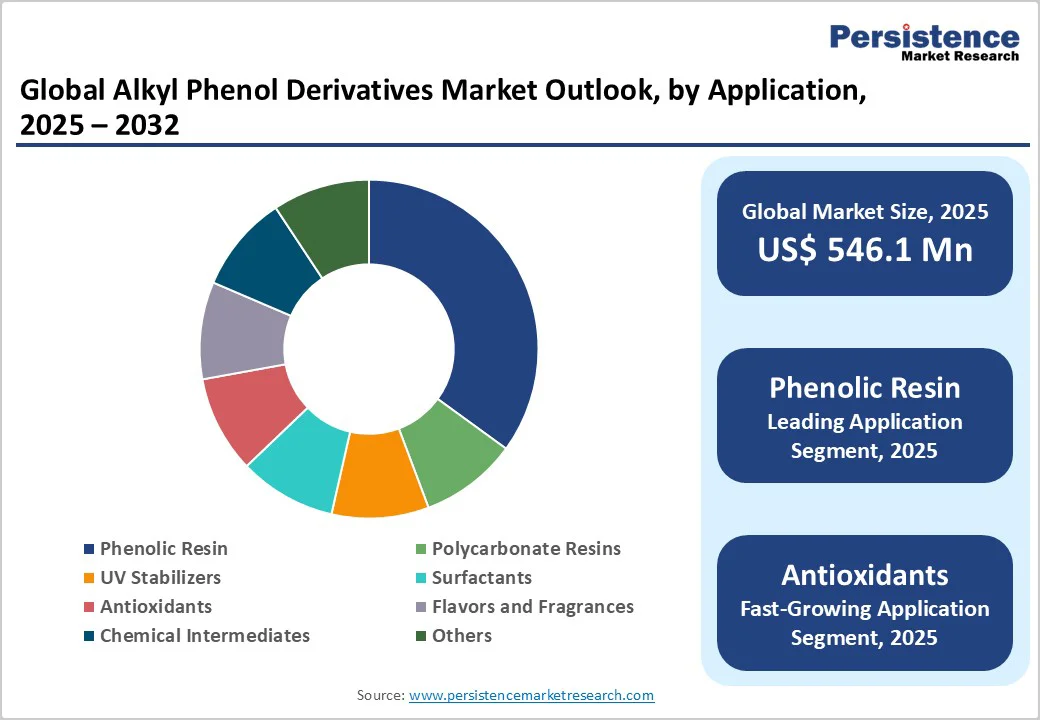

- Fastest Growing Segment: Antioxidants represent the fastest-growing application, expanding at 5% annually from electronic and lubricant needs, enhancing oxidative stability in high-performance polymers.

- Leading Application: Advancements in bio-based formulations offer key opportunities, enabling market players to tap sustainable surfactants amid global green chemistry investments exceeding US$ 10 billion.

| Key Insights | Details |

|---|---|

| Alkyl Phenol Derivatives Market Size (2025E) | US$ 546.1 Mn |

| Market Value Forecast (2032F) | US$ 718.6 Mn |

| Projected Growth CAGR (2025 - 2032) | 4.0% |

| Historical Market Growth (2019-2024) | 3.7% |

Market Dynamics

Driver - Rising Demand in Construction and Automotive Sectors

The growing construction sector is driving the alkyl phenol derivatives market, as these compounds are crucial for producing phenolic resins used in adhesives and coatings that ensure structural integrity.

With global construction spending anticipated to surpass US$ 15 trillion by 2030, driven by urbanization in the Asia Pacific and infrastructure initiatives like China's Belt and Road, demand for durable, heat-resistant materials is intense further driving the growth of alkyl phenol derivatives.

Construction spending data from the U.S. Census Bureau shows that total spending for the first eight months of 2024 reached US$1.42 trillion, reflecting a 7.6% increase from US$1.32 trillion during the same period in 2023, underscoring the sector's robust expansion.

Furthermore, the automotive industry's shift toward electric vehicles (EVs), with sales exceeding 14 million units in 2023, boosts the need for lightweight composites and antioxidants derived from alkyl phenols.

These derivatives stabilize polymers used in interiors and under-hood components, meeting stringent safety standards like those from the International Organization for Standardization (ISO). As EV production grows at 20% annually, alkyl phenol integration in polycarbonate resins ensures enhanced thermal stability, positively impacting market volumes and fostering innovation in high-performance applications.

Expanding Use in Sustainable Formulations

Sustainability initiatives are driving the growth of alkyl phenol derivatives, especially bio-based and low-VOC variants for paints and coatings.

Regulatory pressures from the European Chemicals Agency (ECHA) require manufacturers to adopt environmentally friendly processes, reducing carbon footprints by up to 50%. The shift toward circular economy practices, including recycled feedstocks, supports the demand for eco-friendly surfactants and stabilizers, enhancing non-toxic product lines.

This movement is supported by annual investments exceeding US$ 10 billion in sustainable chemical research and development, ensuring market resilience.

The integration with the P-Tert-Butylphenol Market further accelerates this, as PTBP's solid form facilitates stable, low-emission resins for industrial uses. Enhanced formulations meet consumer demand for environmentally compliant products, evidenced by a 15% increase in bio-based coating sales in Europe, reinforcing growth trajectories for alkyl phenol derivatives.

Restraint - Stringent Environmental Regulations

Stringent environmental regulations pose a significant restraint on the alkyl phenol derivatives market, limiting production due to concerns over toxicity and persistence in ecosystems. Agencies such as the U.S. Environmental Protection Agency (EPA) and REACH in Europe restrict nonylphenol ethoxylates, leading to phased bans that increase compliance costs by 20-30% for manufacturers.

In the United States, the EPA is requiring submission of health and safety studies for 16 chemical substances, including 4-tert-octylphenol, under the Toxic Substances Control Act (TSCA), as these chemicals are candidates for high-priority designation for risk evaluation.

The UK REACH work programme has initiated regulatory management options analysis for substances meeting the definition of phenol alkylation products, investigating risks and recommending approaches to protect human health and the environment.

Raw Material Price Volatility

Fluctuations in crude oil and benzene prices severely restrain the alkyl phenol derivatives market, as these feedstocks constitute over 60% of production costs. The 2020 oil price crash exemplifies this challenge, as phenolic resin producers struggled with supply chain disruptions and demand fluctuations that severely impacted operational stability.

Global oil price swings, influenced by OPEC+ decisions, have caused 15-20% variability in 2024, compelling manufacturers to pass on costs or scale back operations. This instability discourages long-term contracts and innovation, particularly in price-sensitive applications like surfactants, ultimately curbing market growth potential.

Opportunity - Opportunities in Emerging Markets Industrialization

Rapid industrialization in emerging markets offers substantial opportunities for alkyl phenol derivatives, especially in Asia Pacific, where manufacturing output contributes nearly 50% globally.

Countries such as India and ASEAN nations are investing over US$1 trillion in infrastructure by 2030, driving demand for phenolic resins in adhesives and coatings. Developments such as India's Make in India initiative boost local production, creating avenues for suppliers to expand capacity and capture untapped demand in the construction and automotive sectors.

SONGWON Industrial Group, as the largest producer of phenolic antioxidants in Asia with economy-of-scale production units in Korea, demonstrates the strategic importance of backward integration of key raw materials for phenolic antioxidants, ensuring reliability of supply and adding value throughout the production chain.

Advancements in High-Performance Applications

The rise of high-performance applications in electronics and EVs unlocks opportunities for alkyl phenol derivatives in UV stabilizers and antioxidants. With global EV battery production expected to reach 3,000 GWh by 2030, these derivatives enhance material longevity against degradation, meeting standards from the International Electrotechnical Commission (IEC).

Innovations in nanotechnology integration further improve efficacy, as seen in 20% efficiency gains in polymer stabilization, positioning companies to gain market share through R&D investments exceeding US$5 billion annually.

Combining with the Phenolic Antioxidants Market, alkyl phenols serve as key intermediates, with demand surging in rubber and plastics for oxidative resistance. Recent developments in low-toxicity formulations support expansion in food packaging and pharmaceuticals, convincing stakeholders of substantial future revenue potential.

Category-wise Insights

Product Type Analysis

Para-tert-butyl-phenol (PTBP) dominates the product type category in the alkyl phenol derivatives market, holding approximately 50% share. The compound serves critical functions as an intermediate for perfumery ingredients 4-tertiary butyl cyclohexyl acetate (PTBCHA) and 4-tert-butyl cyclohexanol (PTBCH), which are highly valued in fragrance formulations for their distinctive floral, woody, and iris notes.

Data from industry analyses indicate PTBP's consumption exceeds 200,000 tons annually in coatings and adhesives, driven by its role in enhancing polymer durability against chemical exposure. Vinati Organics Limited, the sole producer of PTBP in India with a production capacity of 14,000 TPA, manufactures both Technical Grade and Perfumery Grade variants, demonstrating the commercial significance of this derivative.

Application Analysis

Phenolic Resin leads the application segment in the alkyl phenol derivatives market with about 35% share, owing to its extensive use in high-durability composites for construction and automotive sectors. Authentic statistics show phenolic resins account for over 60% of adhesive formulations in infrastructure projects, bolstered by their thermal stability up to 200°C.

Phenolic resins derived from alkyl phenol compounds, particularly para-tertiary-butylphenol formaldehyde resin (PTBP-FR), exhibit exceptional thermal stability, mechanical strength, chemical resistance, and flame resistance properties that make them indispensable across automotive, construction, and electronics sectors.

The segment's dominance is supported by global resin demand surpassing 5 million tons yearly, where alkyl phenols like DTBP variants improve curing efficiency and mechanical strength, ensuring reliability in demanding environments.

End-user Analysis

Paints & Coatings commands the End-user category in the alkyl phenol derivatives market, capturing roughly 40% share due to its pivotal role in providing corrosion-resistant and weatherproof finishes.

The UV Stabilizers application within coatings represents a particularly dynamic growth area, as automotive coatings face sustained exposure to UV radiation that can lead to degradation of both aesthetic and protective properties, with field measurements showing vehicles in high-sun environments experiencing up to 2,500 hours of direct UV exposure annually and surface temperatures reaching 80°C.

Regional Insights

North America Alkyl Phenol Derivatives Market Trends

North America leads in innovation for alkyl phenol derivatives, with the U.S. dominating through advanced R&D in sustainable formulations. The region's regulatory framework under the Toxic Substances Control Act (TSCA) shapes market dynamics, with the EPA in December 2024 finalizing amendments to regulations governing new chemical reviews to improve efficiency and align with the Frank R. Lautenberg Chemical Safety for the 21st Century Act, ensuring that new persistent, bioaccumulative, and toxic chemicals undergo full safety review processes.

The U.S. construction spending data showing US$1.42 trillion in total expenditure for the first eight months of 2024 reflects infrastructure investment trends supporting coatings and adhesives demand. Innovation ecosystems centered in chemical manufacturing clusters enable rapid commercialization of advanced formulations, with companies such as SI Group and DIC Corporation maintaining significant production and research capabilities in the region to serve automotive, electronics, and industrial customer bases.

Europe Alkyl Phenol Derivatives Market Trends

Europe's alkyl phenol derivatives market thrives on regulatory harmonization under REACH, promoting eco-friendly surfactants in paints and adhesives across Germany, the U.K., France, and Spain. Germany's chemical output, contributing 25% of EU totals, integrates these derivatives in automotive coatings, with BASF's advancements reducing emissions by 40%.

The European Chemicals Agency (ECHA) under the REACH regulation requires companies to identify and manage risks linked to substances they manufacture and market in the EU, with many alkylphenols classified as toxic to the aquatic environment.

The Phenol & Derivatives REACH Consortium facilitates industry coordination on regulatory compliance matters, ensuring manufacturers can navigate complex authorization and restriction requirements. The UK REACH programme's regulatory management options analysis for phenol alkylation products demonstrates the region's proactive approach to chemical safety assessment.

Asia Pacific Alkyl Phenol Derivatives Market Trends

Asia Pacific dominated the market with the most dynamic regional market for alkyl phenol derivatives, with China, Japan, India, and ASEAN countries exhibiting exceptional growth momentum supported by rapid industrialization, urbanization, and manufacturing capacity expansion.

Asia is set to lead global phenol industry capacity additions with a 89% share by 2027, gaining capacities from new-build and expansion projects totaling 2.48 (mtpa), driven by rapid industrialization and urbanization, creating high market demand for phenol and downstream derivatives.

China's phenol production reached 444,000 tons in June 2025 with an operating rate of 79.2%, expected to increase to around 490,000 tons in July 2025 with capacity utilization around 80% as new production facilities come online.

Competitive Landscape

The global alkyl phenol derivatives market exhibits a consolidated structure, growing through integrated supply chains and R&D investments. Companies pursue expansion via capacity upgrades and partnerships, focusing on sustainable technologies to counter regulations.

Major global manufacturers, including SI Group, TASCO Group, Beijing Jiyi Chemical, DIC Corporation, Huntsman, PCC Group, Sasol, and Songwon, command substantial market shares through diversified product portfolios, integrated production capabilities, and established customer relationships across automotive, construction, and electronics sectors.

Key Market Developments:

- September 2024: SI Group announced plans to close its Singapore alkylphenol plant by H2 2025 due to market shifts and costs, shifting production to Europe and the Americas.

- March 2024: DIC Corporation's subsidiary Ideal Chemi Plast commenced operations at a new paint resin plant in Maharashtra, India, enhancing regional phenolic resin capacity.

- October 2023: Sasol Limited launched Carinex and Livinex biosurfactant brands, incorporating alkyl phenol derivatives for sustainable personal and home care applications.

Top Companies in Alkyl Phenol Derivatives Market

- DIC Corporation (Japan) leads with a diverse portfolio in pigments and resins, leading through innovative alkyl phenol applications in coatings. Its global R&D network drives sustainable solutions, strengthening market influence in Asia and Europe.

- SI Group (USA) excels in performance additives, with alkyl phenols central to antioxidants for rubber and fuels, boasting a 4-6% annual growth via strategic acquisitions. Headquarters in The Woodlands supports its worldwide operations.

- Sasol Limited (South Africa) integrates upstream resources for efficient alkyl phenol production, focusing on eco-friendly derivatives. Its maturity in chemicals ensures strong positioning in emerging markets.

Companies Covered in Alkyl Phenol Derivatives Market

- DIC Corporation

- SI Group

- TASCO Group

- Sasol Limited

- United Chemical Products Ltd.

- Maruzen Petrochemical Co., Ltd.

- FabriChem (NutriScience Innovations, LLC)

- HELM AG

- Jiyi Group

- SONGWON Industrial Group

- Qingdao Scienoc Chemical Co., Ltd.

- Red Avenue New Material Group Co., Ltd.

- Prasol Chemicals Pvt. Ltd.

- Vinati Organics Limited

- Novokuibyshevsk Petrochemical Company

- Afton Chemical Corporation

- Dayang Chem Co., Ltd.

Frequently Asked Questions

The global alkyl phenol derivatives market is valued at US$ 546.1 Mn in 2025 and expected to reach US$ 718.6 Mn by 2032.

Key drivers include rising construction and automotive sectors, demanding phenolic resins and coatings, alongside sustainability pushes for bio-based variants amid global infrastructure spending over US$ 15 trillion.

Phenolic Resin leads with 35% share, vital for adhesives and composites in construction, offering thermal stability up to 200°C.

Asia Pacific leads with over 45% share, driven by manufacturing in China and India, supporting phenolic resin demand in infrastructure projects.

Advancements in bio-based surfactants offer opportunities, reducing carbon footprints by 80% through partnerships like Sasol's launches, tapping green chemical demand.

Major players include DIC Corporation, SI Group, and Sasol Limited, leading through innovations in resins and additives with global revenues exceeding US$ 6 billion combined.