- Medical Devices

- Actigraphy Device Market

Actigraphy Device Market Size, Share, and Growth Forecast 2026 - 2033

Actigraphy Device Market by Product (Wearable, Handheld), by Application (Sleep Disorders, Physical Activity Monitoring, Chronic Disease Management), End-user (Healthcare Providers, Research Institutions, Homecare Settings, Fitness and Sports Centers), and Regional Analysis, 2026-2033

Actigraphy Device Market Size and Trend Analysis

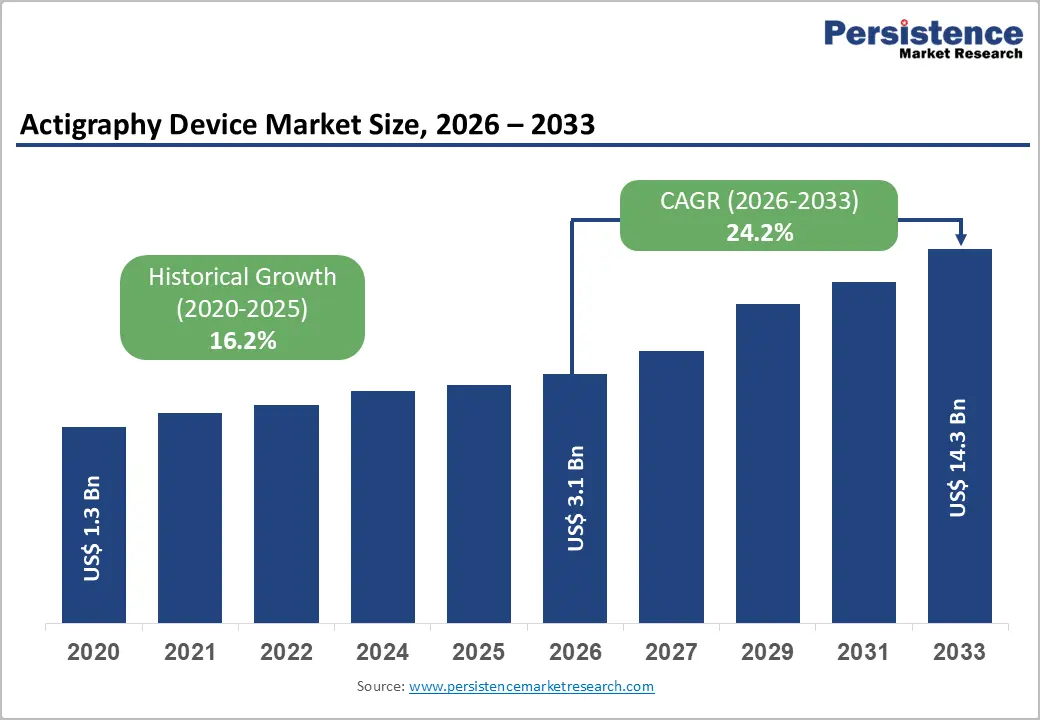

The global actigraphy device market size is expected to be valued at US$ 3.1 billion in 2026 and projected to reach US$ 14.3 billion by 2033, growing at a CAGR of 24.2% between 2026 and 2033. The rise in the number of people suffering from sleep disorders and the growing use of wearable health monitoring devices.

Actigraphy devices are mainly used to track sleep patterns, physical activity, and rest cycles through wrist-worn monitors. These devices help doctors diagnose sleep problems and improve patient care. The American Academy of Sleep Medicine (AASM) recognizes actigraphy as an important tool for sleep-wake cycle assessment. Growing awareness of sleep health, better reimbursement for remote patient monitoring in North America, and the use of AI-based data analysis are further supporting market growth.

Key Industry Highlights

- Leading Region - North America will likely lead in terms of revenue in 2026, backed by the increasing prevalence of mental health issues and sleep disorders.

- Fastest Growing Region - Asia-Pacific is the fastest-growing region, driven by China’s strong market share, India’s high undiagnosed OSA burden, and expanding digital health infrastructure.

- Dominant Segment - Wearable actigraphy devices are highly preferred due to their lightweight, wrist-worn design that ensures user comfort during long-term monitoring.

- Fast-Growing Segment - Chronic Disease Management is the fastest-growing segment, driven by CMS reimbursement expansion, rising research funding, and growing use in disease progression monitoring.

- Key Opportunity - Increasing use in pediatric and geriatric research is expected to open new segments for device manufacturers.

Market Dynamics

Drivers - Surging Global Prevalence of Sleep Disorders Driving Clinical Actigraphy Adoption

Sleep disorders represent one of the most underdiagnosed public health challenges globally. The American Academy of Sleep Medicine (AASM) estimates that over 70 million Americans suffer from chronic sleep disorders, while the World Sleep Society classifies sleep deprivation as a global epidemic affecting over 45% of the world's population. Actigraphy devices validated by AASM's Clinical Practice Guidelines as appropriate tools for assessing circadian rhythm disorders, insomnia, and hypersomnia are experiencing rapidly growing deployment as cost-effective ambulatory alternatives to in-laboratory polysomnography (PSG).

The National Institutes of Health (NIH) has funded multiple large-scale cohort studies utilizing actigraphy for sleep phenotyping. Actigraphy's ability to provide objective, longitudinal sleep-wake data across multiple weeks from home settings makes it clinically superior to single-night PSG for characterizing circadian rhythm disorders, driving adoption across sleep medicine clinics and academic medical centers globally.

Remote Patient Monitoring Integration and Digital Health Ecosystem Expansion

The accelerating adoption of remote patient monitoring (RPM) programs is a powerful structural demand driver for actigraphy devices. U.S. Centers for Medicare & Medicaid Services (CMS) reimbursement for remote physiologic monitoring under CPT codes 99453, 99454, and 99457 has created a financially sustainable model for deploying actigraphy in home and ambulatory settings.

A landmark study published in JAMA Internal Medicine demonstrated that wrist actigraphy correlated strongly with polysomnography in detecting sleep disorders across multiple patient populations. Furthermore, integration of actigraphy devices with electronic health record (EHR) systems, including Epic and Cerner and AI analytics platforms is enabling clinicians to incorporate objective activity and sleep data into longitudinal patient care plans, expanding actigraphy from a research tool into a mainstream clinical monitoring modality.

Restraints - Dependence on Movement-Based Tracking Limits Clinical Reliability

The demand for actigraphy tools in the sleep aid devices market is poised to hamper to a certain extent due to limitations in their ability to capture the full spectrum of sleep stages. Actigraphy primarily measures movement to infer sleep and wake states, lacking the ability to distinguish between different sleep stages such as non-REM and REM sleep. This issue arises as the devices do not record physiological signals, including muscle activity, eye movements, or brain activity, which are required for accurate sleep staging.

Actigraphy further tends to overestimate total sleep time and sleep efficiency while underestimating wakefulness, specifically in individuals with disturbed sleep patterns. This discrepancy is due to the device's reliance on movement. Hence, periods of immobility, even when awake, are often misclassified as sleep. Such inaccuracies are challenging in populations with fragmented sleep. It is evident among those with insomnia or sleep apnea, where precise measurement of wakefulness is important.

Opportunities - Actigraphy Devices Gain Traction in Fitness Centers to Optimize Recovery

Fitness and sports centers are increasingly integrating actigraphy devices to improve recovery monitoring, injury prevention, and athletic performance. These are further creating lucrative opportunities for actigraphy device manufacturers. Philips' Motion Biosensors exemplify this trend by offering trainers and athletes reliable feedback on sleep quality and energy use across multiple activities, including injury recovery, travel, and training. Such devices help enhance training and rehabilitation schedules by evaluating the ideal balance of sleep, activity, and rest required to maximize performance.

Wearable technology is also playing a significant role in recovery monitoring and injury prevention. By enabling real-time performance tracking, these devices enable athletes and coaches to access data on calories burned, heart rate, distance covered, and speed. These insights facilitate immediate adjustments to training programs, thereby improving performance and lowering the risk of overtraining. The ability of wearable sensors to analyze body movements to detect injury-prone patterns and support timely corrections is also projected to drive adoption.

Category-wise Analysis

Product Insights

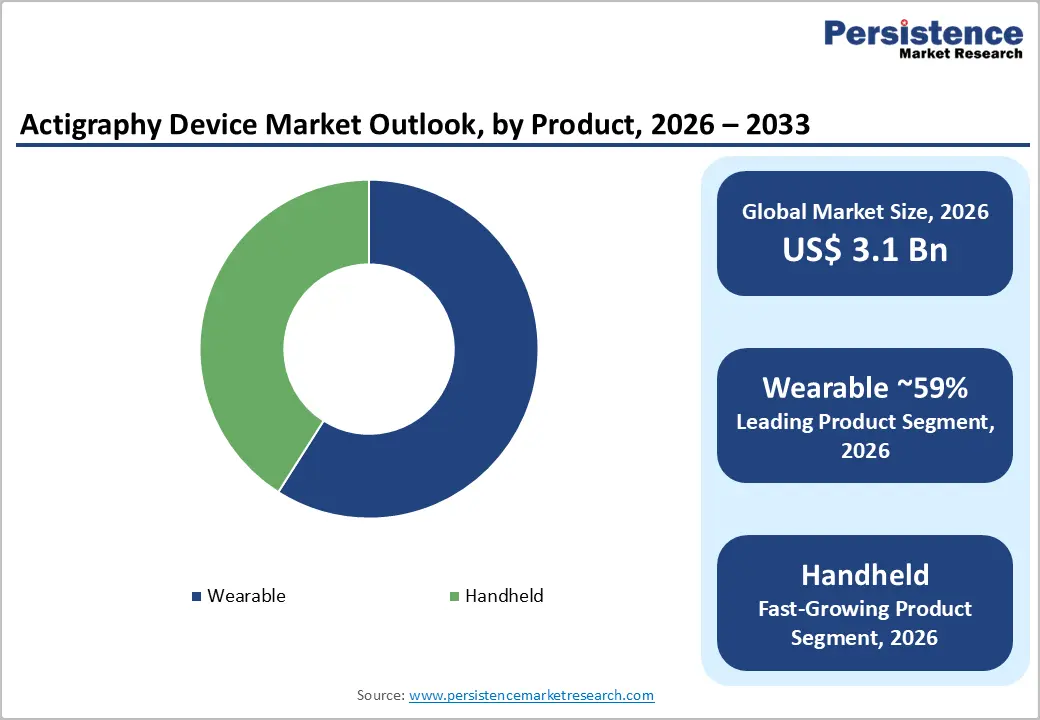

The wearable segment leads the actigraphy device market by product type, accounting for ~59% of total market share in 2025. Wearable actigraphy devices, primarily wrist-worn accelerometer-based monitors, dominate due to their non-invasive design, patient comfort for multi-day continuous wear, and proven clinical validation in sleep medicine and physical activity research. The AASM's Clinical Practice Guidelines specifically recommend wrist actigraphy for evaluating circadian rhythm sleep-wake disorders and insomnia in adults and pediatric populations, cementing wearable devices' clinical legitimacy. Leading platforms, including ActiGraph's GT9X Link and CamNtech's Actiwatch Spectrum Pro set the research-grade clinical standard. Handheld devices are the fastest-growing product segment, driven by clinical point-of-care applications in hospital inpatient settings and pediatric populations where wrist-worn formats are impractical.

Application Insights

Sleep disorders lead the actigraphy device market, accounting for ~47% of total share in 2026. Sleep medicine represents actigraphy's most established, clinically validated, and reimbursed application domain. The International Classification of Sleep Disorders (ICSD-3) published by the AASM specifies actigraphy as a recommended diagnostic tool for circadian rhythm sleep-wake disorders, insomnia disorder evaluation, and treatment response monitoring.

The National Sleep Foundation estimates that ~50-70 million U.S. adults have ongoing sleep disorders, providing a vast clinical population. Physical Activity Monitoring is the fastest-growing application, fueled by CMS RPM reimbursement expansion and chronic disease prevention programs integrating objective activity measurement into population health management strategies.

End-user Insights

Healthcare providers represent the leading end-use segment in the actigraphy device market, commanding ~44% of total revenue in 2026. Hospitals, sleep disorder clinics, neurology departments, and academic medical centers drive this leadership through structured clinical actigraphy protocols and integration of actigraphy data into EHR-linked patient care pathways.

The American College of Chest Physicians (ACCP) and AASM clinical guidelines recommend actigraphy deployment in accredited sleep centers, creating institutional procurement mandates. Research Institutions represent the second-largest segment, driven by NIH-funded cohort studies. Homecare settings are the fastest-growing end-use category, driven by CMS RPM reimbursement enabling actigraphy deployment in home-based chronic disease management programs across cardiology, oncology, and geriatric care applications.

Regional Insights

North America Actigraphy Device Market Trends and Insights

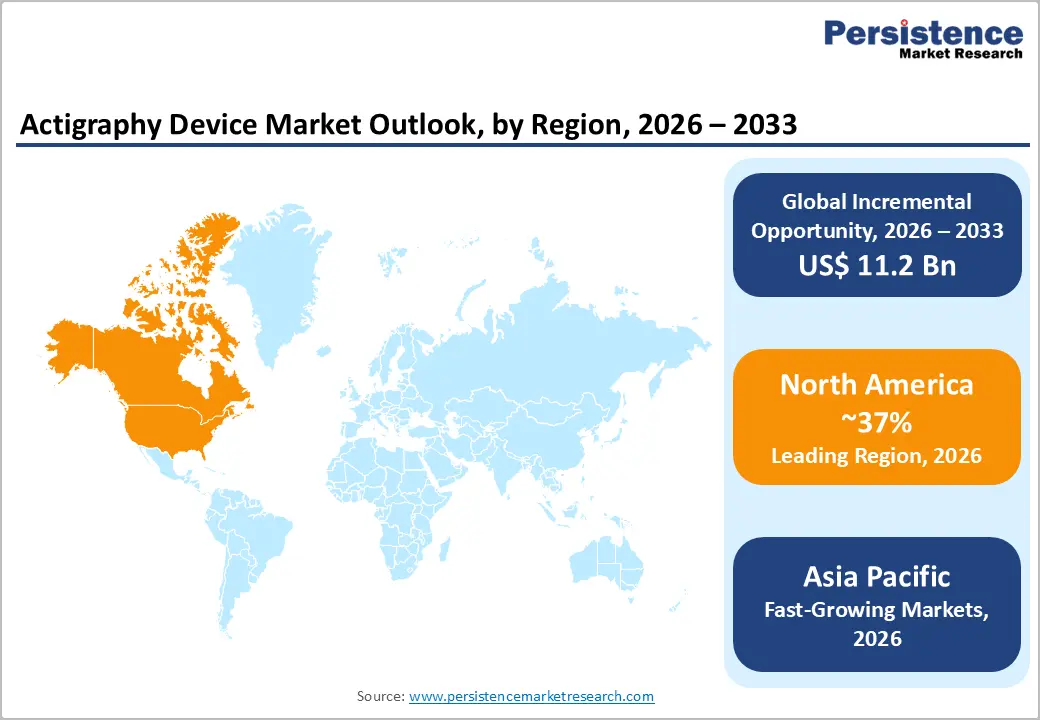

North America is anticipated to account for around 37% of the actigraphy device market share in 2026 due to a significant shift toward decentralized clinical trials and remote patient monitoring. Organizations such as the National Institutes of Health (NIH) and sleep research institutes are increasingly relying on actigraphy to collect longitudinal sleep data in non-clinical environments. Florida-based ActiGraph, for example, has witnessed a surge in partnerships with pharmaceutical companies, providing FDA-registered devices.

U.S. Actigraphy Device Market Size

The U.S. accounts for ~87% of North America's actigraphy device revenue, anchored by over 2,500 AASM-accredited sleep centers, broad CMS RPM reimbursement enabling home actigraphy deployment, and active NIH-funded clinical research programs utilizing ActiGraph and Philips Actiwatch platforms as validated study instruments.

Europe Actigraphy Device Market Trends and Insights

In Europe, the deployment of smart sleep tracking devices such as actigraphy in occupational health research is predicted to drive the market, especially in Germany and Scandinavia. A recent study funded by Sweden’s Karolinska Institute, for example, used actigraphy to examine sleep irregularities among shift workers in the transportation sector. It used CE-marked devices connected to cloud-based dashboards to analyze circadian misalignment. This further influenced labor policy discussions around night shifts and health.

The European Union’s Medical Device Regulation (MDR), which was fully implemented in 2021, has also resulted in a consolidation of vendors. Under this norm, only companies with CE-certified devices can participate in hospital tenders and public procurement. Hence, firms such as CamNtech in the UK and SOMNOmedics in Germany have strengthened their positions by updating their actigraphy devices to comply with these norms.

Germany Actigraphy Device Market Size

Germany holds ~24% of European actigraphy device revenue, supported by its dense hospital and sleep medicine center network, Deutsche Gesellschaft fur Schlafforschung und Schlafmedizin (DGSM) clinical guidelines recommending actigraphy use, and Germany's strong university research sector deploying actigraphy in longitudinal health studies funded by the Deutsche Forschungsgemeinschaft (DFG).

UK Actigraphy Device Market Size

The UK contributes ~19% of European actigraphy device revenues. NHS England's growing recognition of sleep medicine as a clinical priority, combined with NICE (National Institute for Health and Care Excellence) guidance supporting actigraphy in selected patient populations, drives institutional procurement across NHS sleep and neurology departments and Medical Research Council (MRC)-funded research programs.

Asia Pacific Actigraphy Device Market Trends and Insights

Asia-Pacific is the fastest-growing regional market for actigraphy devices, driven by a massive and underdiagnosed sleep disorder burden, rapidly expanding digital health infrastructure, and universal health coverage expansion in China, Japan, India, and Southeast Asia. China represents ~34% of Asia-Pacific market revenue, with the Chinese Sleep Research Society (CSRS) promoting standardized sleep disorder diagnostic protocols incorporating actigraphy in tier-1 and tier-2 hospital settings.

India Actigraphy Device Market Size

India contributes ~10% of Asia-Pacific actigraphy device revenues and is one of the region's fastest-growing markets. The Indian Sleep Disorders Association (ISDA) estimates that over 93 million Indians suffer from moderate to severe obstructive sleep apnea, representing a vast underdiagnosed population. Government healthcare digitalization under Ayushman Bharat Digital Mission is driving medical device adoption, including wearable monitoring across tier-2 hospital networks.

Japan Actigraphy Device Market Size

Japan holds ~21% of Asia-Pacific actigraphy device revenues, reflecting its advanced healthcare infrastructure and significant investment in aging population care. Japan's high prevalence of sleep disorders in its 65+ demographic, with the Ministry of Health, Labour and Welfare (MHLW) reporting widespread insomnia and circadian rhythm disruption, drives institutional actigraphy adoption in geriatric care and hospital sleep medicine departments.

Competitive Landscape

The global actigraphy device market is moderately fragmented, with specialized medical device companies including ActiGraph, LLC, CamNtech Ltd., ActivInsights Ltd., SOMNOmedics AG, and Nox Medical competing alongside large, diversified healthcare companies such as Koninklijke Philips N.V. and consumer wearable leaders including Fitbit.

Key competitive differentiators include clinical validation depth, regulatory clearance portfolio breadth, data analytics software capabilities, EHR integration, and research institution partnerships. Strategic trends include AI analytics platform development, cloud-based data management services, consumer-to-clinical device convergence strategies, and geographic expansion into Asia-Pacific emerging markets through local distributor partnerships and regulatory pathway navigation.

Key Developments:

- In June 2025, Empatica launched EmbraceMini, the world’s smallest wrist-worn actigraphy device for clinical trials, offering 7-day continuous monitoring and tracking over 200 digital sleep and activity measures.

- In November 2023, ActiGraph launched its next-generation multisensor wearable called the ActiGraph LEAP. It provides researchers with the ability to collect continuous digital measures of mobility, sleep, physical activity, and additional vital signs in a single fit-for-purpose device.

- In October 2023, the American Academy of Sleep Medicine unveiled the Act on Actigraphy campaign to highlight the significance of actigraphy testing for sleep disorders. It also urged payers to reimburse healthcare professionals for this evidence-based medical service.

Global Actigraphy Device Market - Key Insights

| Key Insights | Details |

|---|---|

|

Historical Market Value (2020) |

US$ 1.3 Billion |

|

Current Market Value (2026) |

US$ 3.1 Billion |

|

Projected Market Value (2033) |

US$ 14.3 Billion |

|

CAGR (2026-2033) |

24.2% |

|

Leading Region |

North America, 37% share (2026) |

|

Dominant Product |

Wearable, ~59% market share (2026) |

|

Top-ranking Application |

Sleep Disorders, ~47% market share (2026) |

|

Incremental Opportunity |

US$ 11.2 Billion (2026-2033) |

Companies Covered in Actigraphy Device Market

- ActiGraph, LLC

- ActivInsights Ltd.

- Koninklijke Philips N.V.

- Fibion Inc.

- neurocare group AG

- Empatica Inc.

- CamNtech Ltd.

- Cleveland Medical Devices

- SOMNOmedics AG

- Nox Medical

- Fitbit

- CIDELEC

- Others

Frequently Asked Questions

The global market is projected to reach US$ 3.1 billion in 2026.

Key demand drivers include rising sleep disorders, CMS reimbursement for remote monitoring, AASM guideline support, and AI integration improving clinical decision-making.

North America leads the global market with 37% of market share in 2025.

Major opportunities lie in chronic disease management applications and the integration of consumer wearables with clinical actigraphy platforms supported by SaMD regulations.

Key players include ActiGraph LLC, Koninklijke Philips N.V., CamNtech Ltd., Empatica Inc., Garmin Ltd., and other companies focusing on wearable monitoring and sleep diagnostics.