- Specialty & Fine Chemicals

- Acetophenone Market

Acetophenone Market Size, Share, and Growth Forecast 2026 - 2033

Acetophenone Market by Product Grade (Industrial Grade, Pharmaceutical Grade, Reagent Grade, Cosmetic Grade), Form (Liquid, Solid, Crystalline), Application (Chemical Intermediate, Pharmaceutical Intermediate, Fragrance Ingredient, Flavoring Agent, Solvent), End-user, Regional Analysis, 2026 - 2033

Acetophenone Market Size and Trend Analysis

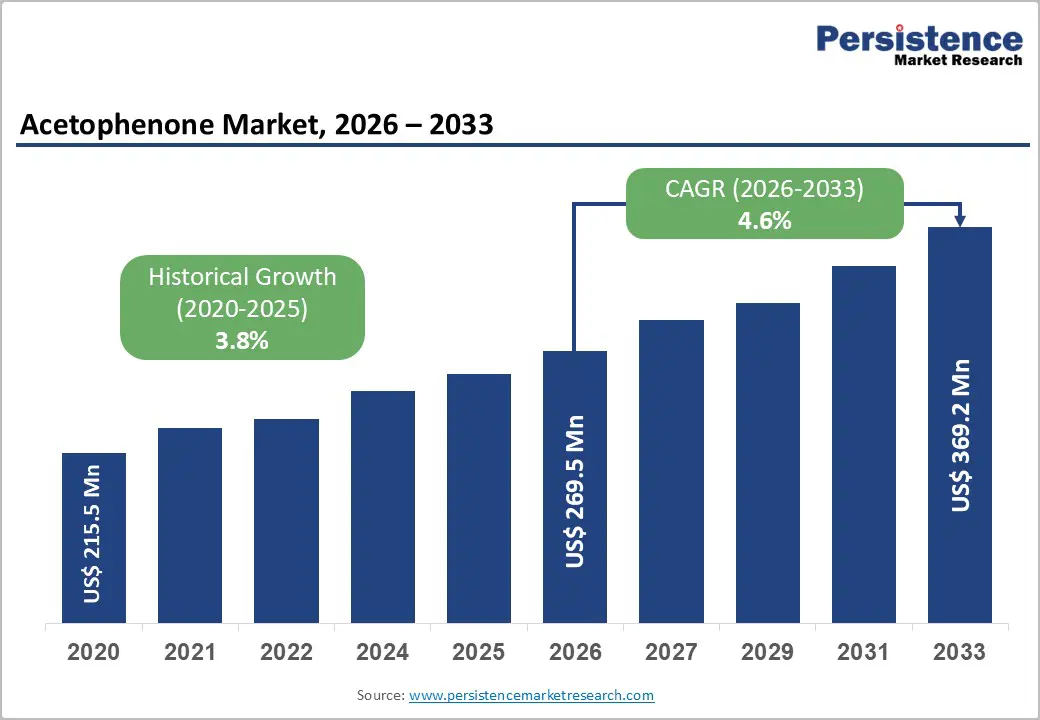

The global acetophenone market is projected to reach US$ 269.5 million in 2026 and US$ 369.2 million by 2033, growing at a CAGR of 4.6% over the forecast period.

Market expansion is fundamentally driven by rising demand for pharmaceutical intermediates, with acetophenone serving as a critical precursor for synthesizing active pharmaceutical ingredients, including anti-inflammatory agents, anesthetics, and sedatives. The global pharmaceutical industry is expanding at 7% annually.

Key Industry Highlights:

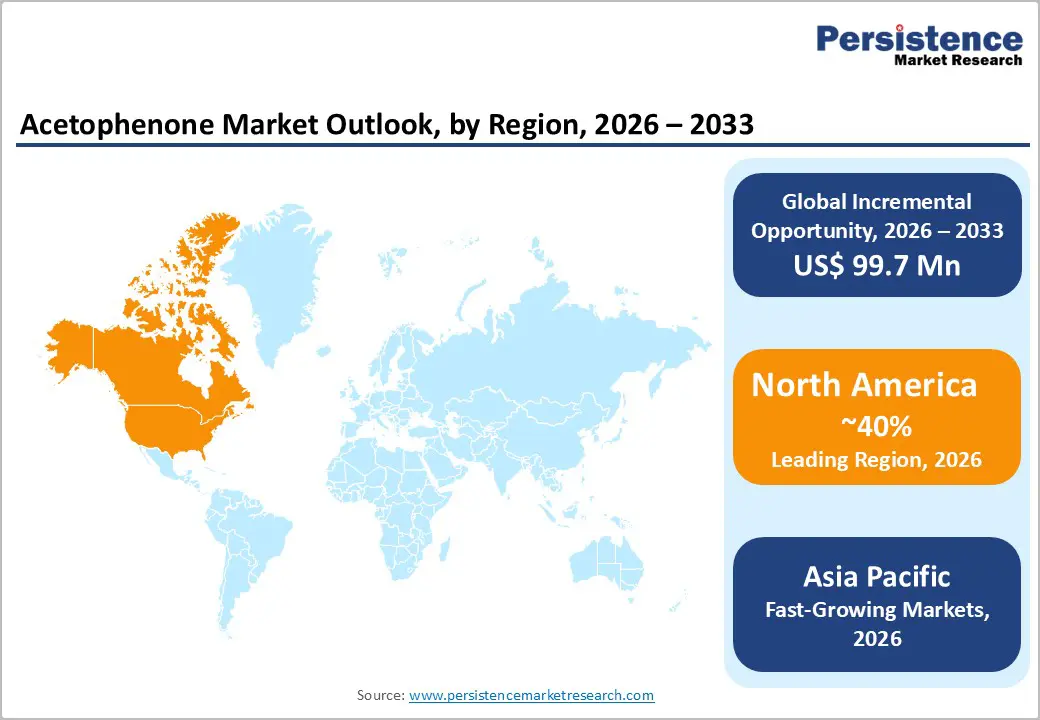

- Leading Region: North America maintains market leadership with established pharmaceutical manufacturing with 40% share, robust research capabilities, and mature supply chains supporting premium acetophenone applications across pharmaceutical synthesis, specialty chemicals, and cosmetic formulations.

- Fastest Growing Region: Asia Pacific accelerates at 5.9% CAGR, anchored by China's 35%+ global capacity and India's pharmaceutical expansion driven by generic drug manufacturing and cosmetics industry growth across rapidly urbanizing populations.

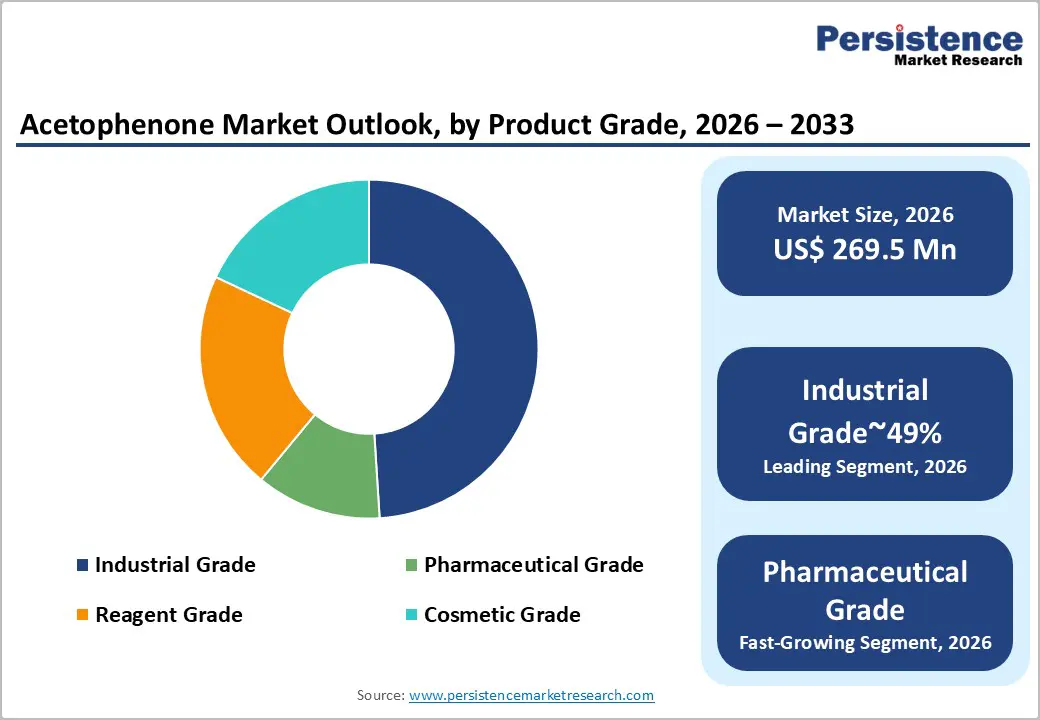

- Dominant Segment: Industrial Grade accounts for 49% of the market, reflecting cost-sensitive applications in chemical intermediate synthesis, resin production, and polymer manufacturing, with an established supply infrastructure and proven performance.

- Fastest Growing Segment: Pharmaceutical-grade acetophenone grows 6.7% CAGR, driven by expanding pharmaceutical intermediates demand, stricter quality requirements for API synthesis, and premium pricing supporting specialty manufacturers.

- Key Market Opportunity: Asia-Pacific specialty chemicals expansion offers substantial growth potential, with rising pharmaceutical manufacturing, cosmetics industry growth, and agrochemical production accounting for 65% of incremental market growth through 2033.

| Key Insights | Details |

|---|---|

| Acetophenone Market Size (2026E) | US$ 269.5 Million |

| Market Value Forecast (2033F) | US$ 369.2 Million |

| Projected Growth CAGR (2026 - 2033) | 4.6% |

| Historical Market Growth (2020 - 2025) | 3.8% |

Market Dynamics

Drivers - Rising global pharmaceutical production and chronic disease prevalence continue driving strong acetophenone demand as a critical API intermediate

Acetophenone is a key intermediate in the production of active pharmaceutical ingredients, significantly supporting market growth. It is widely used in the synthesis of anti-inflammatory drugs, anesthetics, sedatives, and pain management medications. One of the most notable examples is ibuprofen, one of the most commonly consumed medicines worldwide, underscoring acetophenone’s importance in pharmaceutical manufacturing.

Global pharmaceutical market expansion continues to accelerate due to aging populations, rising healthcare spending exceeding US$ 12 trillion annually, and increasing cases of chronic diseases such as arthritis, cardiovascular disorders, and neurological conditions. Pharmaceutical manufacturers prioritize acetophenone because of its chemical stability, consistent reaction performance, and ability to meet high-purity requirements. Its well-established global supply chain supports cGMP-compliant production, ensuring reliability for large-scale drug manufacturing. As pharmaceutical innovation and generic drug production expand globally, demand for acetophenone remains strong and structurally supported.

Growing consumption of perfumes, cosmetics, and flavored products significantly boosts acetophenone usage across the fragrance and personal care industries

The fragrance and flavor segment represents 41.5% of the total acetophenone market revenue and continues to show steady growth. Rising global consumption of perfumes, cosmetics, and personal care products is a major driver supporting this segment. Acetophenone functions as a fragrance intermediate and fixative, helping stabilize scent compositions while offering a pleasant, sweet, heliotrope-like aroma. The global cosmetics and personal care industry, valued at over US$500 billion, increasingly emphasizes premium fragrances and differentiated formulations, thereby directly boosting acetophenone use.

Food and beverage manufacturers use acetophenone as a flavoring agent in processed foods and beverages to enhance aroma consistency. Cosmetic producers incorporate it into lotions, creams, body washes, and hair care products to enhance fragrance stability and product uniformity. Growing consumer preference for branded, scented, and premium personal care products continues to strengthen long-term demand.

Restraints - Strict global chemical safety regulations increase compliance costs and operational complexity for acetophenone manufacturers across major markets

The acetophenone market faces increasing regulatory pressure due to strict chemical safety frameworks across major regions. Regulations such as Europe’s REACH Regulation 1907/2006/EC and U.S. EPA oversight require extensive documentation, toxicity testing, and compliance verification, raising operational costs for manufacturers. Concerns regarding occupational exposure limits, environmental impacts, and reproductive or developmental safety assessments further complicate production and use.

Differences in regulatory standards between regions often lead to approval delays and increased administrative burden for global suppliers. Additionally, manufacturers must invest in advanced safety systems, worker protection equipment, and specialized transportation protocols to meet occupational health requirements. These compliance-related expenses increase capital expenditure and reduce flexibility, particularly for smaller producers. As regulatory expectations continue to tighten, meeting safety and environmental standards remains a major challenge affecting production efficiency and profit margins.

Market saturation and consolidation in North America and Europe limit growth potential despite stable demand from established end-use industries

Developed regions such as North America and Europe show clear signs of market maturity, limiting overall growth potential. North America records a modest CAGR of 2.2%, while major European countries such as Germany and the UK grow at 1.9% and 1.6%, respectively. These markets already have well-established supply chains, stable customer bases, and strong domestic production, leaving limited room for volume expansion.

Intense price competition and long-term supplier contracts further restrict margin growth. Market consolidation among leading players such as Solvay, INEOS Phenol, and Mitsui Chemicals has reduced competitive diversity, making entry difficult for new participants. Although pharmaceutical-grade and specialty applications command higher prices, their growth in volume demand remains limited. As a result, developed markets primarily focus on efficiency improvements rather than significant capacity expansion.

Market Opportunities

Rapid industrialization and expanding pharmaceutical capacity position the Asia Pacific as the primary growth engine for the global acetophenone market

Asia-Pacific presents the strongest growth opportunity for the acetophenone market, driven by rapid industrialization and the expansion of the pharmaceutical and cosmetics industries. China and India are the key growth engines, recording CAGRs of 4.5% and 5.9%, respectively. China accounts for more than 35% of global acetophenone production and consumption, owing to large-scale manufacturing infrastructure and cost advantages.

India’s pharmaceutical industry, ranked among the world’s top three producers of generic drugs, generates substantial demand for acetophenone in API synthesis. Favorable government policies, increasing chemical investments, and lower production costs further strengthen regional competitiveness. Additionally, ASEAN countries such as Vietnam, Thailand, and Indonesia are emerging as attractive markets owing to the growth of consumer-goods manufacturing and rising healthcare demand. Together, these factors position the Asia Pacific as the primary contributor to future global market expansion.

Rising demand for pharmaceutical-grade and specialty acetophenone creates premium pricing opportunities and supports long-term margin expansion

The development of specialty and high-purity acetophenone grades offers attractive premium pricing opportunities for manufacturers. Pharmaceutical-grade and reagent-grade products typically command 20% higher prices than industrial-grade products due to strict purity and compliance requirements. These grades are essential for advanced pharmaceutical synthesis, laboratory research, and fine chemical applications.

Emerging therapeutic areas, including psoriasis, fungal infections, and oncology-related treatments, increasingly require high-purity acetophenone derivatives. In the cosmetics sector, acetophenone is also used to produce UV filter intermediates, such as Avobenzone, thereby supporting the growth of sunscreen and skin-protection products. Rising consumer awareness regarding sun protection continues to expand this application base. Manufacturers investing in cGMP facilities, analytical certification, and specialty product development can strengthen margins while reducing dependence on commodity-grade competition, creating long-term value growth opportunities.

Category-wise Analysis

Product Grade Insights

Industrial-grade acetophenone accounts for approximately 49% of the market, primarily due to its extensive use in cost-sensitive industrial applications. Typically offering 98-99% purity, this grade is widely used in chemical intermediate synthesis, resin production, solvents, polymers, and agrochemical manufacturing. Large-volume end users prioritize affordability and consistent supply over ultra-high purity, thereby supporting industrial-grade dominance.

Cumene-process production accounts for nearly 64.7% of total acetophenone output, providing cost-effective and high-yield manufacturing advantages. This process benefits from the use of integrated benzene and propylene feedstocks, which are commonly available in petrochemical complexes. Major producers such as Solvay, INEOS Phenol, and Mitsui Chemicals focus heavily on industrial-grade capacity to serve global demand. Strong supply reliability, established performance standards, and competitive pricing continue to reinforce this segment’s leadership across multiple industries.

Form Insights

Liquid acetophenone accounts for approximately 65% of the market, making it the most commercially preferred form. Its dominance is driven by easy handling, accurate dosing, and seamless integration into existing manufacturing processes. The liquid form exhibits excellent solubility in organic solvents and compatibility with various reaction systems, thereby improving processing efficiency. Food and beverage manufacturers favor liquid acetophenone for smooth incorporation of flavor, whereas cosmetic producers rely on it for fragrance stabilization in creams, lotions, body washes, and hair products.

Chemical manufacturers also prefer liquid acetophenone for the synthesis of pharmaceutical intermediates due to improved reaction control and faster reaction kinetics. Availability in multiple packaging sizes, from laboratory-scale bottles to 200-liter industrial drums, supports flexible usage across industries. These practical advantages make liquid acetophenone the preferred choice for both large-scale industrial operations and specialty formulation applications.

Application Insights

Chemical intermediate applications account for approximately 47% of total acetophenone revenue, making it the leading usage segment. Acetophenone plays a central role in organic synthesis, supporting the production of fine chemicals, substituted ketones, heterocyclic compounds, and specialty intermediates. Pharmaceutical companies use it extensively as a foundational building block for API manufacturing. Dye producers use acetophenone in the synthesis of organic dyes for textiles, inks, and coatings.

Agrochemical manufacturers also use it in the production of pesticides and herbicides via established Friedel-Crafts acylation reactions. The wide applicability, proven reaction reliability, and extensive technical documentation have made acetophenone a preferred intermediate across industries. Its consistent chemical behavior and scalability further strengthen its role in industrial organic chemistry, ensuring sustained demand across pharmaceutical and specialty chemical manufacturing sectors.

End-user Insights

The pharmaceutical industry represents the largest end-use segment, accounting for nearly 39% of total acetophenone consumption. Pharmaceutical manufacturers rely heavily on acetophenone for the synthesis of ibuprofen, aspirin derivatives, sedatives, anti-inflammatory drugs, and advanced therapeutic compounds. Its chemical structure enables the development of complex molecules required for targeted medical treatments. Growth in global healthcare spending, rising prevalence of chronic diseases, and expansion of generic drug production continue to drive demand.

Pharmaceutical-grade acetophenone must comply with strict cGMP standards and quality control procedures, including impurity profiling and analytical certification. These stringent requirements support premium pricing and long-term supplier relationships. Both multinational pharmaceutical companies and large generic drug manufacturers depend on a reliable supply of acetophenone to maintain uninterrupted production. As healthcare access and medication demand continue rising globally, pharmaceutical end-use remains a stable and high-value consumption segment.

Regional Insights

North America Acetophenone Market Trends

North America maintains a strong market presence due to its advanced pharmaceutical manufacturing ecosystem and mature chemical supply chains. The United States pharmaceutical industry, valued at over US$600 billion, generates significant demand for acetophenone in API synthesis and specialty drug development. The region’s cosmetics and personal care sector, valued at over US$ 90 billion, further supports fragrance and flavor applications.

However, market growth remains moderate, with a CAGR of 2.2%, owing to saturation and intense competition. Strict regulatory oversight from agencies such as the EPA, FDA, and OSHA increases compliance complexity and operational costs. Trade policies and supply chain restructuring also influence sourcing strategies. Despite slower growth, North America continues to lead in innovation, demand for high-purity products, and specialty chemical development, thereby maintaining its importance in the global acetophenone market.

Europe Acetophenone Market Trends

Europe plays a significant role in global acetophenone consumption, owing to its strong chemical and pharmaceutical industries. Germany leads regional demand, with a CAGR of 1.9%, owing to its position as a global chemical manufacturing hub that employs over 450,000 professionals. France and Italy contribute through pharmaceutical production, fragrance manufacturing, and fine chemical specialization. REACH Regulation 1907/2006/EC ensures high-quality standards but also increases regulatory and compliance costs.

The UK focuses largely on specialty and high-value pharmaceutical applications. Although demand remains stable, growth rates between 1.6% and 1.9% reflect market maturity. Increasing emphasis on sustainability and environmental responsibility is influencing production practices, with manufacturers investing in cleaner synthesis methods. While expansion opportunities are limited, Europe remains strategically important for premium-grade acetophenone and regulated chemical applications.

Asia Pacific Acetophenone Market Trends

Asia-Pacific is the fastest-growing regional market, driven by robust industrial expansion and rising pharmaceutical output. China accounts for more than 35% of global acetophenone capacity and records a CAGR of 4.5%, supported by large-scale manufacturing hubs and cost-efficient production. India follows with a higher CAGR of 5.9%, driven by its position as a leading global generic drug manufacturer.

Pharmaceutical, fragrance, and cosmetics companies across the region increasingly utilize acetophenone for API and formulation applications. ASEAN countries such as Vietnam, Thailand, and Indonesia are emerging as new growth centers, driven by expanding consumer-goods industries and improved chemical infrastructure. Favorable investment policies, lower production costs, and growing domestic demand position the Asia-Pacific region to account for nearly 65% of global incremental growth through 2033, making it the primary future growth engine.

Competitive Landscape

The acetophenone market exhibits moderate consolidation, with the top ten producers controlling largest share of global revenue. This structure reflects balanced competition, neither fully fragmented nor dominated by a few players. Solvay leads the market through strong integration with phenol and acetone production using the cumene process, ensuring cost efficiency and supply stability. INEOS Phenol benefits from petrochemical integration, enabling competitive pricing and large-scale output. Mitsui Chemicals differentiates itself through pharmaceutical-grade and reagent-grade offerings that command premium margins.

Key competitive strategies include vertical integration, capacity optimization, and expansion into specialty-grade products. Manufacturers increasingly focus on sustainable production methods, emission reduction, and process efficiency improvements. Emerging producers from China and India compete on cost for industrial-grade supply, while established players protect premium segments through quality, compliance expertise, and long-term customer partnerships.

Key Market Developments

- In April 2022, Solvay announced a major investment to expand its acetophenone and related phenolic compound production capacity to better meet rising global pharmaceutical and specialty chemical demand, strengthening its supply position in key end-use markets.

- In June 2023, INEOS Phenol completed the modernization of its cumene-based acetophenone production facilities by implementing advanced catalytic and process technologies, enhancing production efficiency and environmental compliance at key sites.

- In October 2024, Chinese chemical manufacturers expanded acetophenone output capacity to over 50,000 metric tons annually, leveraging cost-competitive production advantages to serve growing demand in the Asia Pacific and emerging markets.

Companies Covered in Acetophenone Market

- Alfa Aesar

- Rhodia

- INEOS Phenol

- CellMark USA LLC

- Tanfac

- A.B. Enterprises

- Triveni Interchem

- Shenze Xinze Chemical

- Solvay

- Novapex

- Mitsui Chemicals

- Haicheng Liqi Carbon

- SI Group

- Zhongliang

- RÜTGERS Group

- Eni Versalis

- Seqens

- Vinati Organics

- Dow Chemical Company

Frequently Asked Questions

The global Acetophenone market is projected to reach US$ 369.2 Million by 2033 from US$ 269.5 Million in 2026, growing at a CAGR of 4.6% driven by expanding pharmaceutical intermediate demand, fragrance and flavor industry growth, and Asia Pacific industrialization.

Primary drivers include pharmaceutical intermediate expansion for API synthesis including ibuprofen production, fragrance and flavor industry growth representing 41.5% of total demand, Asia Pacific industrial expansion with China and India demonstrating 4.5% and 5.9% CAGR respectively, and rising cosmetics and personal care product consumption globally.

Industrial Grade dominates with 49% market share, driven by cost-sensitive applications in chemical intermediate synthesis, solvent production, resin manufacturing, and polymer processing, supported by cumene-process synthesis achieving 64.7% of total production through established, cost-effective manufacturing.

North America maintains market leadership through advanced pharmaceutical manufacturing, robust chemical supply chains, and established research capabilities, though Asia Pacific emerges as fastest-growing region with China's 35%+ global capacity and India's 5.9% CAGR positioning region for 65% of incremental growth through 2033.

Pharmaceutical-grade and specialty-grade development represents primary opportunity, with pharmaceutical-grade products commanding 25% price premiums over industrial-grade, supported by expanding Asia Pacific pharmaceutical manufacturing, rising API synthesis demand, and emerging applications in specialty chemicals and fine pharmaceutical synthesis.

Leading companies include Solvay, INEOS Phenol, Mitsui Chemicals, Novapex, Haicheng Liqi Carbon, and Eni Versalis, with top 10 producers controlling largest share of global revenue through integrated production capabilities and specialty-grade differentiation.