- Biotechnology

- Treponema Pallidum Tests Market

Treponema Pallidum Tests Market Size, Share, Growth, and Regional Forecast, 2026 to 2033

Treponema Pallidum Tests Market by Test Type (Treponemal Serology and Non-Treponemal Serology), End-user (Hospitals, Specialty Clinics, Diagnostic Laboratories, Academic & Research Institutes), and Regional Analysis from 2026 to 2033

Treponema Pallidum Tests Market Share and Trends Analysis

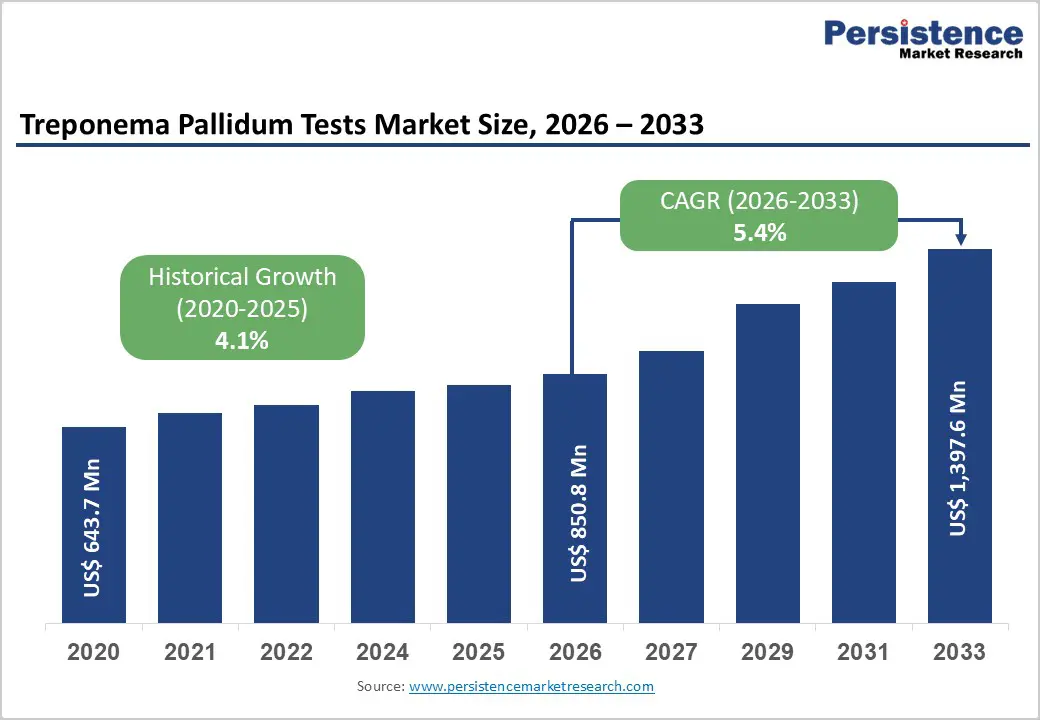

The global Treponema pallidum tests market size is estimated to grow from US$ 850.8 million in 2026 to US$ 1,397.6 million by 2033, growing at a CAGR of 5.4% during the forecast period from 2026 to 2033.

Global demand for Treponema pallidum tests is rising rapidly, driven by increasing syphilis prevalence, expanding antenatal screening programs, and growing awareness of the importance of early and accurate STI diagnosis. Hospitals and specialty centers prefer both treponemal and non-treponemal assays to support routine screening, confirmatory testing, and management of congenital and latent infections.

Rise in investments in infectious-disease surveillance, expanding laboratory automation capacity, and growing public-health testing initiatives are accelerating global adoption. Continuous advancements in CLIA/EIA platforms, rapid lateral-flow diagnostics, automated RPR/VDRL systems, and AI-enabled laboratory workflow technologies are significantly improving diagnostic accuracy, turnaround time, and scalability. Additionally, growing acceptance of reverse-sequence screening algorithms, increasing global syphilis burden, and expanding clinical evidence supporting dual HIV/syphilis testing are further propelling global market growth.

Key Industry Highlights:

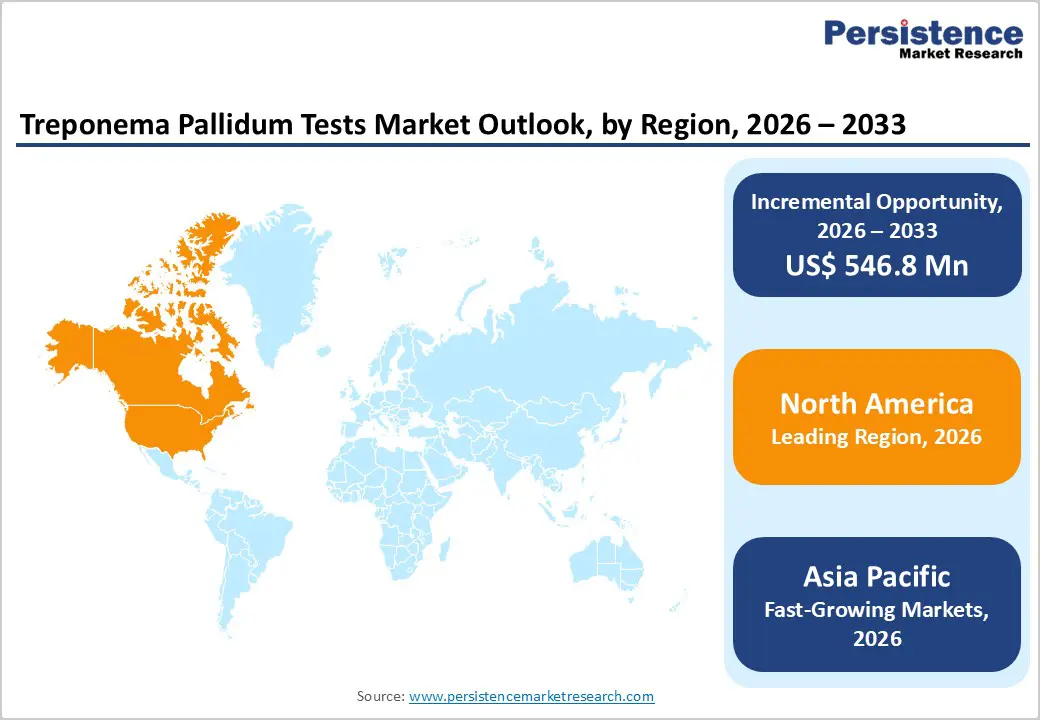

- Leading Region: North America holds the largest share at 47.3%, supported by advanced diagnostic infrastructure, strong adoption of automated immunoassay platforms, high healthcare expenditure, and early access to FDA-approved syphilis testing technologies.

- Fastest-Growing Region: Asia Pacific is expanding the fastest due to a large patient pool, rapid laboratory modernization, growing medical tourism, and increasing investments in infectious-disease testing capacity.

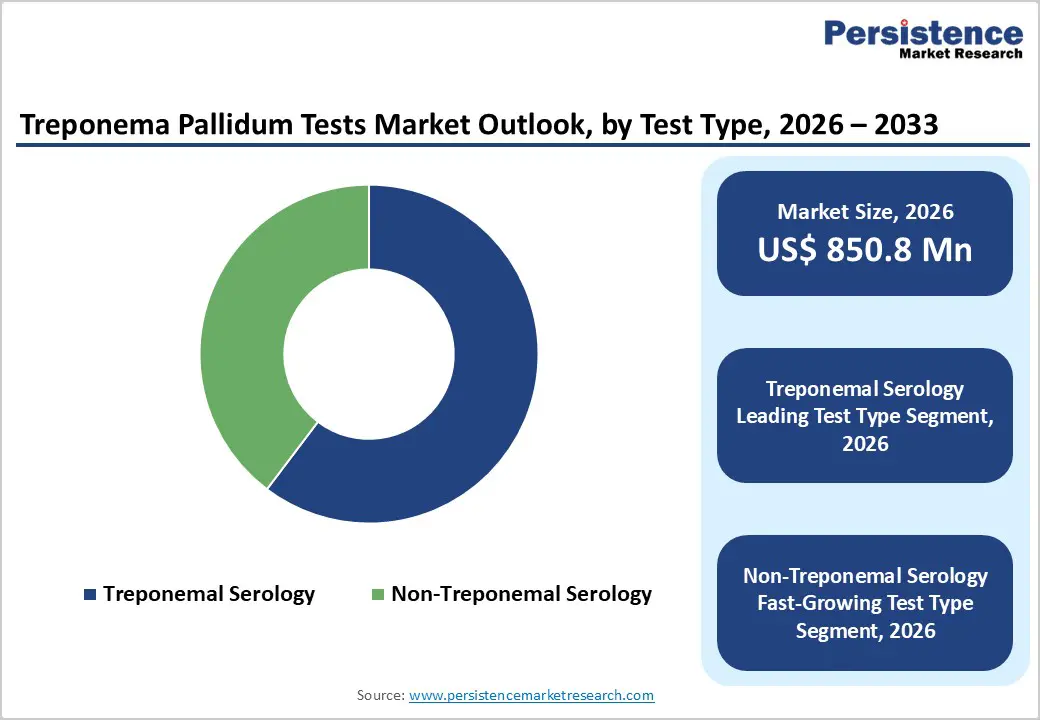

- Leading Test Type Segment: Treponemal serology dominates the market due to its extensive use in screening and confirmatory algorithms, offering high specificity and long-term serological sensitivity.

- Fastest-Growing Test Type Segment: Non-treponemal serology grows rapidly as rising syphilis incidence supports broader use of RPR/VDRL tests for screening, disease staging, and treatment monitoring.

- Leading End-user Segment: Hospitals remain the top application, driven by high diagnostic volumes, availability of automated platforms, and central roles in maternal health and infectious-disease management.

- Fastest-Growing End-user Segment: Diagnostic laboratories are scaling quickly as demand increases for high-throughput testing, digital lab integration, and expanded population-based surveillance programs.

| Key Insights | Details |

|---|---|

| Treponema Pallidum Tests Market Size (2026E) | US$ 850.8 Mn |

| Market Value Forecast (2033F) | US$ 1,397.6 Mn |

| Projected Growth (CAGR 2026 to 2033) | 5.4% |

| Historical Market Growth (CAGR 2020 to 2025) | 4.1% |

Market Dynamics

Driver - Rising Syphilis Burden and Expanding Diagnostic Screening Programs

The global burden of syphilis continues to rise, with rising case notifications across the U.S., Europe, and Asia driving healthcare systems to strengthen their surveillance infrastructure. For instance, in 2023, the U.S. Centers for Disease Control and Prevention (CDC) reported a national congenital syphilis rate of 105.8 cases per 100,000 live births, a 3.0% increase from 2022. Increasing transmission rates among sexually active adults, congenital syphilis cases linked to untreated maternal infections, and urban clusters of high-risk populations are compelling governments to prioritize routine screening.

Many countries are expanding mandatory testing protocols for pregnant women, blood donors, and individuals attending STI clinics. These initiatives are not only increasing testing volumes but also accelerating early detection and treatment, which helps reduce transmission and lowers the incidence of severe complications such as neurosyphilis and congenital infections. As awareness campaigns and public health budgets expand, the need for reliable, scalable, and cost-effective diagnostic solutions is becoming paramount.

Technological advancements in treponemal and non-treponemal testing are reshaping the diagnostic landscape. Automated chemiluminescence immunoassays (CLIA), next-generation ELISAs, and molecular assays such as PCR have significantly enhanced sensitivity and specificity, ensuring more accurate clinical decisions. Laboratories increasingly rely on automated platforms that streamline workflows, support high-throughput screening, and reduce human error. These innovations enable faster turnaround times, improve patient management, and support large-scale government-led screening drives. Collectively, rising disease prevalence, expanding screening mandates, and rapid technological evolution are creating a strong foundation for sustained market growth.

Restraints - Low Awareness, Limited Diagnostic Infrastructure, and False-Positive

The global Treponema pallidum testing market faces persistent limitations stemming from low awareness, social stigma, and inadequate diagnostic infrastructure in developing regions. In many low- and middle-income countries, public understanding of sexually transmitted infections (STIs) remains limited, leading to underutilization of routine screening services. Cultural barriers and misconceptions further discourage individuals from seeking timely testing, contributing to delayed diagnoses and continued disease transmission. These challenges are compounded by resource constraints that limit community-level outreach, education programs, and early screening initiatives essential for controlling syphilis spread.

Additionally, restricted access to high-quality diagnostic technologies poses a significant restraint on market expansion. Many regions lack automated immunoassay platforms, rapid treponemal analyzers, or RT-PCR systems required for sensitive and confirmatory detection of Treponema pallidum. This technological gap is further exacerbated by false-positive and cross-reactive results from serological tests, which can complicate clinical interpretation, especially among populations with autoimmune conditions or co-infections. These diagnostic challenges not only delay appropriate treatment but also reduce clinicians' confidence in test reliability, limiting broader adoption. Ensuring consistent reagent quality, improving test specificity, and expanding infrastructure remain critical steps to overcoming these barriers globally.

Opportunity - Smartphone-Enabled POC Testing, Multiplex STI Panels, High-Throughput Automation, and Global Public-Private Partnerships in Treponema pallidum Diagnostics

The global Treponema pallidum testing market is poised for accelerated growth, driven by rapid innovation in point-of-care (POC) diagnostics and multitarget screening technologies. Smartphone-enabled POC platforms equipped with AI-based lateral-flow readers are transforming early detection in remote and underserved regions by providing real-time result interpretation and improved analytical sensitivity. These advancements significantly strengthen community-level screening and decentralize diagnostic access. At the same time, the integration of Treponema pallidum testing into multiplex STI panels, capable of simultaneously detecting infections such as HIV, HBV, and chlamydia, is driving adoption among diagnostic laboratories. Such consolidated testing systems enhance workflow efficiency, reduce reagent costs, and streamline patient management across diverse clinical settings.

Furthermore, the growing demand for automated high-throughput analyzers presents a major opportunity for manufacturers as hospitals and reference laboratories continue to expand their screening capacity. These systems minimize manual workload, reduce operational errors, and enable faster turnaround times essential for large-scale STI surveillance. Parallel to technological progress, increasing public-private partnerships involving the WHO, CDC, and global health organizations are creating strong potential for market penetration by funding affordable test kits, supporting procurement programs, and strengthening national STI control strategies. These collaborations are expected to enhance testing coverage, improve early diagnosis, and accelerate the global rollout of next-generation diagnostic solutions for Treponema pallidum.

Category-wise Analysis

By Test Type Insights

The treponemal serology segment is projected to dominate the global Treponema pallidum tests market in 2026, accounting for 60.3% of total revenue. This dominance is driven by the increasing adoption of treponemal assays, including TP-PA, FTA-ABS, ELISA, and CLIA tests, which offer higher specificity for detecting Treponema pallidum antibodies and are widely recommended in confirmatory and reverse-sequence screening algorithms. Their ability to detect both early and latent infections, provide long-term serological memory, and support high-throughput automated testing platforms further strengthens adoption. Growing preference for rapid treponemal tests in point-of-care settings, combined with advances in assay sensitivity, reagent stability, and automated analyzer integration, is accelerating global adoption in public health programs, antenatal screening, and routine STI diagnostics.

By End-user Insights

The hospitals segment is projected to dominate the global Treponema pallidum tests market in 2026, capturing a 53.7% revenue share. Hospitals, particularly tertiary-care centers, infectious-disease units, and academic medical institutions, serve as primary hubs for syphilis diagnosis due to their ability to manage complex cases, maintain robust laboratory operations, and integrate confirmatory testing workflows. High patient inflow, availability of automated immunoassay analyzers, and access to specialized infectious-disease clinicians support strong hospital-based demand for both treponemal and non-treponemal assays. Additionally, hospitals play a central role in outbreak surveillance, antenatal screening programs, and clinical research initiatives evaluating new diagnostic technologies, reinforcing their position as the leading end-user segment globally.

Regional Insights

North America Treponema Pallidum Tests Market Trends

North America is expected to maintain global dominance in the Treponema pallidum tests market with a market share value of 47.3%, supported by its advanced healthcare infrastructure, strong infectious disease surveillance systems, and widespread adoption of high-performance diagnostic platforms. The U.S. leads the region due to frequent FDA approvals of new serology and rapid diagnostic assays, a strong presence of leading diagnostic manufacturers, and extensive collaborations among hospitals, public health laboratories, and academic research centers. Major reference labs and academic institutions continuously validate new treponemal and non-treponemal assay technologies, accelerating clinical implementation. Rising demand for early syphilis detection, antenatal screening, and decentralized point-of-care testing continues to drive investments from large healthcare networks.

The region also benefits from strong reimbursement frameworks for laboratory testing, high clinician preference for automated immunoassay systems, and growing adoption of rapid dual HIV/syphilis tests in community health programs. Increasing investments in high-throughput analyzers, digital laboratory workflow integration, and AI-supported diagnostic platforms are expanding testing capacity. Additionally, rising public awareness of sexually transmitted infections and the growing number of infectious disease research hubs strengthen North America’s long-term leadership in the global market.

Europe Treponema Pallidum Tests Market Trends

Europe shows steady and mature adoption of Treponema pallidum testing, supported by strong public-health screening programs, well-established laboratory networks, and stringent diagnostic accuracy standards. Countries such as Germany, the U.K., France, Italy, Switzerland, and the Nordic region lead deployment, backed by robust epidemiological surveillance systems and consistent clinical validation of new serological and molecular assays. For instance, in 2023, the European Centre for Disease Prevention and Control (ECDC) reported 41,051 confirmed syphilis cases across 29 EU/EEA Member States, corresponding to a crude notification rate of 9.9 cases per 100,000 population, marking a 13% increase compared to 2022. The region is characterized by active integration of automated immunoassays, rapid treponemal tests, and confirmatory TP-PA/FTA-ABS assays in routine diagnostics, driven by the need for improved accuracy, early detection, and reduced congenital syphilis incidence.

Europe’s favorable regulatory environment, emphasis on quality assurance, and strong involvement of academic research centers create a supportive foundation for evaluating next-generation diagnostic technologies. Growing demand for high-sensitivity screening tests, automated workflows, and integrated lab platforms further strengthens adoption. Regional diagnostic manufacturers continue to innovate in assay sensitivity, reagent stability, and scalable GMP-compliant production. Government initiatives supporting STI prevention, digital health integration, and migrant-population screening continue to boost Europe’s overall market growth.

Asia Pacific Treponema Pallidum Tests Market Trends

Asia Pacific is projected to be the fastest-growing region for treponema pallidum tests with a CAGR of 7.3%, driven by rising healthcare expenditure, expanded infectious-disease programs, and rapid modernization of diagnostic laboratory infrastructure. Countries such as China, Japan, South Korea, Singapore, and India are accelerating the adoption of treponemal and non-treponemal diagnostic assays across hospitals, STI clinics, and public-health screening initiatives. Increasing availability of cost-effective rapid tests and automated serology kits, combined with strong participation from regional diagnostic manufacturers, is improving affordability and expanding access across mid-sized hospitals and community clinics.

Furthermore, government-supported screening programs, investments in laboratory modernization, and collaborations with global diagnostic companies for technology transfer are fueling adoption. The growing need for early detection, antenatal syphilis screening, and point-of-care testing in rural and underserved populations continues to drive strong clinical uptake. Clinicians across the Asia Pacific are increasingly participating in global STD research networks, adopting advanced diagnostic platforms to enhance accuracy and reduce diagnostic delays. Strengthening private healthcare networks, expanding medical tourism, and the rise of infectious-disease research institutes continue to support robust market growth across the region.

Competitive Landscape

The global Treponema pallidum tests market is highly competitive, with strong participation from leading diagnostics companies such as Abbott, F. Hoffmann-La Roche Ltd, Bio-Rad Laboratories, Inc., Thermo Fisher Scientific Inc., and BD. These companies leverage advanced immunoassay platforms, high-throughput analyzers, rapid lateral-flow technologies, and expanding global distribution networks to strengthen their presence across clinical laboratories and point-of-care settings. Rising demand for early syphilis detection, antenatal screening, and decentralized testing is accelerating the adoption of treponemal and non-treponemal assays across hospitals, public-health programs, and diagnostic centers worldwide.

Manufacturers are increasingly focusing on next-generation CLIA/EIA platforms, automated RPR/VDRL systems, dual HIV/syphilis rapid tests, and molecular/NAAT solutions designed for improved sensitivity, faster turnaround time, and scalable deployment in low-resource regions. Strategic priorities include expanding assay menus, enhancing reagent production capacity, securing regulatory approvals, and partnering with government agencies and global health organizations to support large-scale screening initiatives, strengthen disease surveillance, and drive market growth.

Key Industry Developments:

- In August 2025, Altona Diagnostics introduced the AltoStar® Treponema pallidum PCR Kit 1.5 RUO, a real-time PCR-based reagent system for qualitative detection of Treponema pallidum DNA. Designed for research use only, the kit expands the AltoStar® STI panel and strengthens the platform’s molecular testing capabilities by adding syphilis detection to its portfolio.

- In August 2024, the U.S. Food and Drug Administration (FDA) granted marketing authorization to NOWDiagnostics for the first to know syphilis test, the first over-the-counter at-home test capable of detecting Treponema pallidum antibodies in human blood. While this test enables convenient preliminary screening, results alone are not sufficient for a definitive syphilis diagnosis and must be confirmed through follow-up testing by a healthcare professional.

- In December 2022, the National Institute of Allergy and Infectious Diseases (NIAID) awarded Arlene Seña, MD, MPH, professor of infectious diseases and member of the Institute for Global Health & Infectious Diseases, $1.9 million to conduct a 16-month longitudinal clinical study to advance syphilis diagnostic product development. The project has the potential for additional funding over three more years, supporting continued innovation in Treponema pallidum detection.

Companies Covered in Treponema Pallidum Tests Market

- Abbott

- F. Hoffmann-La Roche Ltd

- Bio-Rad Laboratories, Inc.

- Thermo Fisher Scientific Inc.

- BD

- Hologic, Inc.

- Danaher Corporation.

- DiaSorin S.p.A.

- QuidelOrtho Corporation.

- Creative Diagnostics

- Meridian Bioscience, Inc.

- Biosynex SA

- SEKISUI Diagnostics

- Fujirebio

- Alpine Biomedicals Pvt Ltd.

- Others

Frequently Asked Questions

The global treponema pallidum tests market is projected to be valued at US$ 850.8 Mn in 2026.

Rising syphilis prevalence, expanding antenatal and public-health screening programs, and growing adoption of rapid treponemal and automated immunoassay platforms drive the global treponema pallidum tests market.

The global treponema pallidum tests market is poised to witness a CAGR of 5.4% between 2026 and 2033.

High-growth opportunities lie in scaling dual HIV/syphilis rapid tests, deploying molecular/NAAT diagnostics for early detection, and expanding affordable POC solutions in resource-limited regions.

Abbott, F. Hoffmann-La Roche Ltd, Bio-Rad Laboratories, Inc., Thermo Fisher Scientific Inc., and BD are some of the key players in the treponema pallidum tests market.