- Advanced Materials

- Technical Glass Market

Technical Glass Market Size, Share, and Growth Forecast, 2025 - 2032

Technical Glass Market By Product Type (Borosilicate Glass, Aluminosilicate Glass, Others), Form (Flat Glass, Thin Glass, Others), Application (Optical Devices, Display Glass, Architectural Glass, Others), and Regional Analysis for 2025 - 2032

Technical Glass Market Share and Trends Analysis

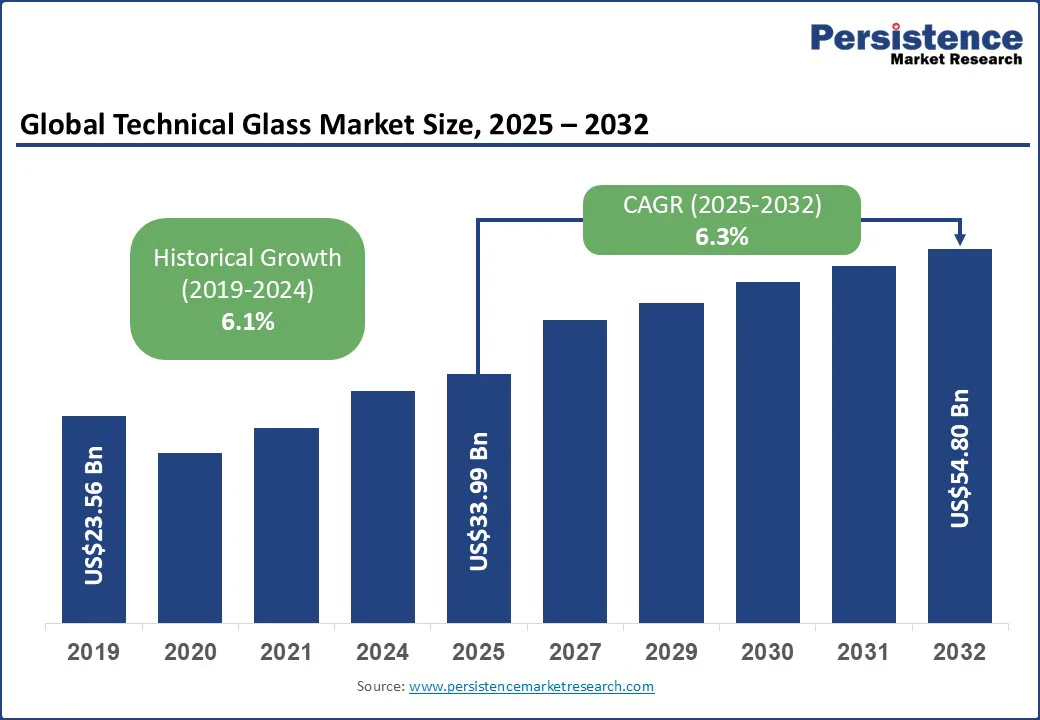

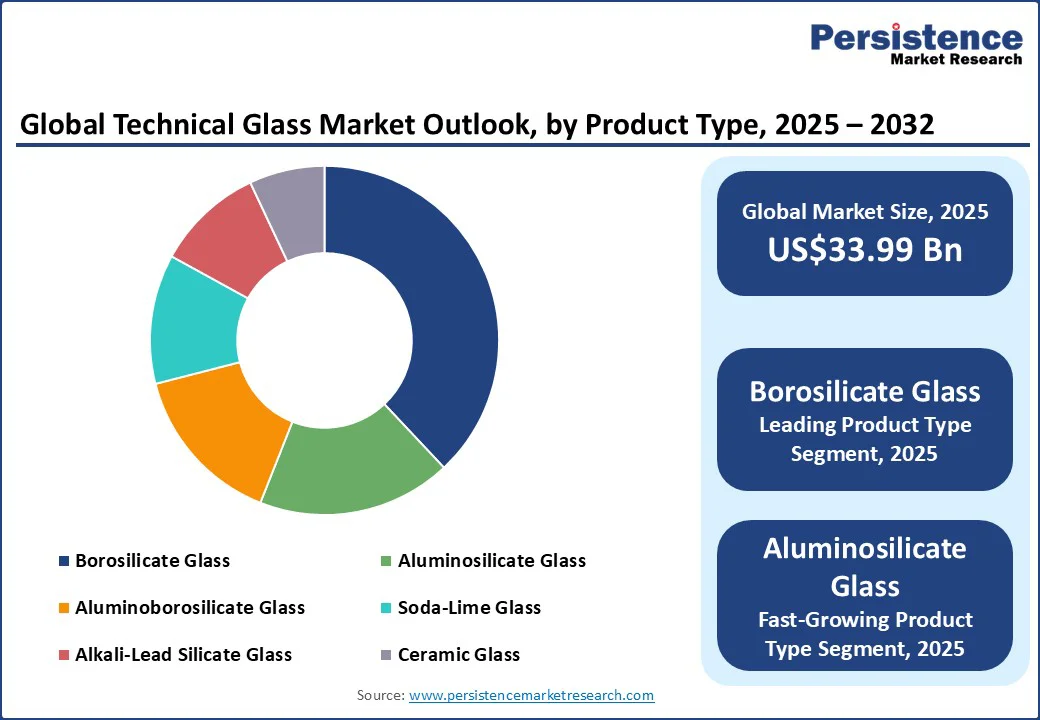

The global technical glass market size is likely to be valued at US$33.99 Bn in 2025, and is estimated to reach US$54.80 Bn by 2032, growing at a CAGR of 6.3% during the forecast period 2025−2032.

Key Industry Highlights:

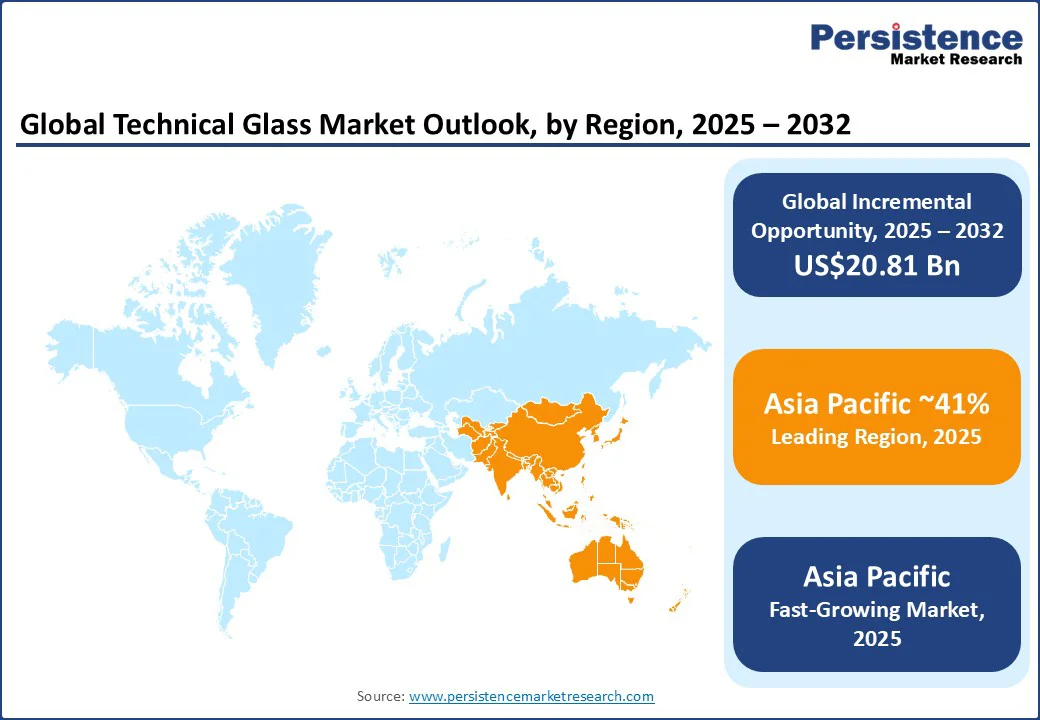

- Dominant Region & Fastest-growing Regional Market: Asia Pacific is set to command the largest regional market share at around 41.0% in 2025, and is also projected to sustain the fastest CAGR through 2032, driven by green infrastructure expansion, renewable energy adoption, and growth of glass manufacturing hubs across China and India.

- Leading Product Type: The borosilicate glass segment is expected to stand out, securing approximately 38.0% revenue share in 2025, owing to its superior thermal resistance and chemical durability.

- Fastest-growing Application Segment: Display glass is anticipated to be the fastest-growing application segment through 2032, with a CAGR hovering around 6.0%, fueled by an escalating demand for flexible, chemically strengthened glass in consumer electronics.

- Key Driver: The market growth is propelled by the rising demand for smart glass technologies, energy-efficient coatings, and multifunctional glass solutions in core sectors such as automotive, construction, and electronics.

- Opportunities Include Advancements in electrochromic and thermochromic glass, which expands sustainable glass applications in EVs, and a huge demand for solar glass in the renewable energy sector, especially in emerging economies.

|

Global Market Attribute |

Key Insights |

|

Technical Glass Market Size (2025E) |

US$33.99 Bn |

|

Market Value Forecast (2032F) |

US$54.80 Bn |

|

Projected Growth (CAGR 2025 to 2032) |

6.3% |

|

Historical Market Growth (CAGR 2019 to 2024) |

6.1% |

The engineering of smart glass technologies, self-healing coatings, and flexible glass displays is transforming market dynamics, opening niche opportunities for manufacturers focused on innovation. Technical glass is a high-performance engineered material characterized by exceptional chemical resistance, thermal stability, optical clarity, and mechanical strength.

Market Factors - Growth, Barrier and Opportunity Analysis

Introduction of Smart and Energy-Efficient Glass Technologies to Act as the Key Market Catalyst

The introduction and deployment of smart glass technologies and energy-efficient glass solutions across diverse industries, particularly construction and automotive sectors, are driving a notable shift toward sustainability and functional innovation. Long-running R&D activities in advanced fenestration solutions have led to the engineering of electrochromic and thermochromic glass, making buildings greener by regulating light and heat.

In July 2025, IIT Indore researchers developed an electrochromic glass using a viologen-based porous organic polymer that swiftly changes color and transparency when an electric current is applied, enabling buildings to block heat and light in summer or let them in during cooler weather, thereby reducing reliance on air conditioning and artificial lighting.

Such innovations hold much significance for rapidly urbanizing economies, especially those located in the tropics, where climates are hot and humid for most of the year. Moreover, breakthroughs in self-healing and flexible glass technologies for displays and solar panels present lucrative growth niches, emphasizing a consumer demand for versatility and functionality.

Tariff Hikes by the U.S. to Trigger Cost Pressures and Disruptions in the Global Glass Supply Chain

The recent implementation of aggressive tariffs by the Trump administration, particularly the hike to a 45% tariff on Chinese imports and a sweeping 25% tariff on goods from Mexico and Canada, is reverberating through the technical glass market, cascading into escalating production costs and disrupting global supply chains. Economic theories and experiences have proven that tariffs increase the cost of a wide range of raw materials, including glass components, which are integral to a wide spectrum of applications such as automotive glazing, smart windows, and solar panels.

While the temporary exemption under the USMCA delayed the tariffs’ impact on imports from Mexico and Canada until April 2025, once the effects of the policy change start to settle in, they will likely impose severe cost burdens on glass fabricators relying heavily on cross-border material flows.

The volatility introduced by these tariff measures will force manufacturers to navigate heightened uncertainty and pricing pressures, which disproportionately strain smaller fabricators with limited supply chain flexibility and capital for innovation in niche areas such as flexible and self-healing glass technologies. Furthermore, the ad valorem nature of the tariffs inflates unit costs, likely driving up prices downstream across construction, renewable energy, and electronics sectors.

Extensive Deployment of Electric Vehicles Worldwide to Boost the Demand for Lightweight Technical Glass

The expanding global electric vehicle (EV) market offers lucrative opportunities for technical glass companies. The International Energy Agency (IEA) predicts that the global EV stock will grow by 23% from 2023 to 2035, with more than one in four vehicles on the road being electric by 2035. EV manufacturers are prioritizing lightweight, energy-efficient, and multifunctional glass components to extend battery range, ensure passenger comfort, and support advanced safety systems, broadening the technical glass market outlook.

Leading automakers such as Tesla, BYD, and Volkswagen are increasingly incorporating advanced glass solutions, including electrochromic smart glass and solar control coatings, that reduce heat absorption and noise, directly enhancing vehicle efficiency and user experience. For example, in June 2025, Xiaomi unveiled its first mid-size electric SUV, the YU7 MAX, equipped with an advanced electrochromic smart dimming sunroof developed by Ambilight, capable of blocking up to 99.85% of sunlight. Furthermore, the integration of advanced driver-assistance systems (ADAS) embedded within laminated and chemically strengthened glass necessitates precision-engineered glass products, spurring the demand for innovation in materials such as alkali-lead silicate and soda lime glass.

Category-wise Analysis

Product Type Insights

Borosilicate glass is expected to dominate the product category, boasting an estimated revenue share of 38.0% in 2025. Owing to its exceptional thermal resistance and chemical stability, this glass is indispensable in high-demand applications such as laboratory equipment, pharmaceutical containers, and energy-efficient architectural solutions.

Furthermore, its superior durability against thermal shock keeps it the front-runner for even more advanced applications such as solar panel covers and high-intensity lighting. Its compatibility with eco-friendly manufacturing processes and recyclability further enhances its market appeal amid stringent environmental regulations. This segment also benefits from the escalating demand for consumer electronics, where robust glass solutions are required for making chemically strengthened screens for smartphones and tablets.

Aluminosilicate glass, on the other hand, is projected to grow at the highest CAGR through 2032, propelled by its unmatched strength-to-weight ratio and scratch resistance that make it ideal for flexible displays, EVs, and aerospace applications. With electric vehicle companies incorporating lightweight, robust glass solutions for windows, windshields, and display covers, the value provided by aluminosilicate glass is likely to increase rapidly in the foreseeable future. Besides the automotive sector, recent developments in the electronics industry show manufacturers focusing on aluminosilicate compositions to meet the rigors of foldable smartphone screens and advanced touch panels, integrating properties such as high thermal tolerance and resistance to chemical corrosion.

Application Insights

With an estimated market revenue share of 37.5%, the architectural glass segment is slated to lead the application category in 2025, mainly due to soaring urbanization and industrialization, particularly in the Asia Pacific, which is increasing the demand for energy-efficient and aesthetically appealing building solutions. The construction industry is singularly focusing on obtaining green building certifications and complying with sustainable infrastructure mandates, which will propel the adoption of high-performance architectural glass variants such as insulated glass units (IGUs), laminated glass, and coated glass to improve thermal insulation and reduce energy consumption. Cutting-edge advancements such as switchable smart glass and nanocoatings are being integrated into commercial and residential buildings to regulate light, enhance privacy, and improve indoor environmental quality.

The display glass segment is anticipated to command the highest CAGR of about 6.0% during 2025-2032, driven by exponential growth in consumer electronics, including smartphones, tablets, wearables, and foldable devices. The demand for chemically strengthened aluminosilicate glass with superior scratch resistance and clarity is surging as manufacturers strive to develop ultra-thin, flexible, and durable display panels. Major innovations include sapphire coatings, durable edge treatments, and integration with touch-sensitive and OLED technologies. The rising penetration of digital devices in emerging economies is another factor fueling the growth of this segment.

Regional Insights

Asia Pacific Technical Glass Market Trends

In 2025, Asia Pacific is anticipated to be the most dominant region, holding approximately 41.0% of the market share and exhibiting the highest CAGR through 2032. Prospects for the market appear bright here on account of rapid industrialization, massive urbanization, and the presence of key glass manufacturing hubs in China, India, Japan, and South Korea.

Government investments in infrastructure, smart cities, and renewable energy projects are expected to fuel the demand for glass technologies for architectural, solar, and automotive purposes, integrating energy efficiency and sustainability mandates. The accelerating adoption of EVs and consumer electronics in the region will also boost the demand for aluminosilicate and specialty glasses. The active commercialization of self-cleaning coatings, smart glass, and flexible glass technologies in the Asia Pacific reflects a strong R&D ecosystem.

North America Technical Glass Market Trends

North America is set to capture about 28.0% market share in 2025, with the market here being characterized by the construction sector's ready adoption of energy-efficient and green building products. The market for technical glass here will also reap benefits from stringent regulatory frameworks such as LEED certification and state-level energy codes demanding a low and laminated safety glass.

High penetration of automotive glass innovations and a significant aftermarket demand are also likely to contribute to the regional market growth. Furthermore, glass companies in North America are also innovating in smart glazing, including electrochromic and thermochromic technologies, often supported by government research funding.

Europe Technical Glass Market Trends

Europe is estimated to account for less than a quarter of the market share in 2025. The market is primarily stimulated by an unrelenting focus on sustainability, energy savings, and innovative materials. The aggressive climate goals and building energy directives set in place by the European Union (EU) have boosted the demand for advanced sustainable solutions, such as low-emissivity glass, triple glazing, and integrated solar glass deployments.

The region is also home to several cutting-edge R&D centers specializing in glass coatings and customized glass composites, reflected in commercial projects such as the renowned Bosco Verticale green towers in Milan, employing high-performance architectural glass.

Competitive Landscape

The global technical glass market is highly competitive with top players ramping up investments in developing sustainable glass technologies, forging strategic partnerships, conducting mergers and acquisitions, and focusing on product differentiation. Companies are navigating the evolving market dynamics by expanding their portfolios through acquisitions and joint ventures that elevate their capabilities in advanced materials such as smart glass, solar glass, and self-cleaning coatings.

Product innovation by companies such as Corning is pushing the boundaries of durability and design flexibility. The competitive dynamics are further shaped by governmental incentives promoting energy-efficient technologies and growing regulatory pressure for environmental compliance, compelling manufacturers to invest heavily in R&D for lightweight, multifunctional, and eco-friendly glass products.

Key Industry Developments

- In August 2025, Ambilight partnered with NIO to equip the all-new flagship NIO ES8 SUV with its advanced electrochromic smart dimming side windows. The solution enables adjustable light transmittance, from near-clear to as low as 0.35%, while blocking up to 99.9% of UV and 97% of infrared rays to enhance cabin comfort, privacy, and thermal control.

- In August 2025, GBA launched the DuraTherm Energy Block, a next-generation architectural glass block offering exceptional strength, over four times that of standard blocks, with high thermal efficiency, a 4″-thick design supporting large openings without structural steel, multiple aesthetic finishes, and full recyclability for green building compliance.

- In July 2025, NorthGlass Coating BU launched a groundbreaking 24-meter ultra-long glass coating processing line, an industry first in China with independent intellectual property. The line is designed to meet the surging demand for high-performance curtain wall glass in super high-rise buildings, overcoming critical challenges such as vacuum stability and service valve reliability, and enabling stable manufacturing of complex coatings.

Companies Covered in Technical Glass Market

- Schott AG

- Nippon Sheet Glass Co., Ltd.

- Saint-Gobain S.A.

- Johnson Matthey Plc

- Elan Technology Co., Ltd.

- Nippon Electric Glass Co., Ltd.

- Guardian Industries Corp.

- Allegion plc

- AGC Inc. (Asahi Glass Company)

- RIOU Glass Co., Ltd.

- Flat Glass Group

- Taiwan Glass Industry Corporation

- Xinyi Energy Holdings Limited

Frequently Asked Questions

The global technical glass market is projected to reach US$33.99 Bn in 2025.

The introduction and deployment of smart glass technologies and energy-efficient glass solutions across diverse industries, particularly construction and automotive sectors, are driving the market.

The technical glass market is poised to witness a CAGR of 6.3% from 2025 to 2032.

The integration of advanced driver-assistance systems (ADAS) embedded within laminated and chemically strengthened glass and a thriving EV market are key market opportunities.

Schott AG, Nippon Sheet Glass Co., Ltd., and Saint-Gobain S.A. are some of the leading players in the technical glass market.