- Industrial Goods & Service

- Rotating Equipment Repair Market

Rotating Equipment Repair Market Size, Trends, Share, and Growth Forecast 2025 - 2032

Rotating Equipment Repair Market By Nature of Service (Condition Monitoring & Reliability Services, Others), Equipment (Pumps, Turbines, Others), Industry, Sales Channel, and Regional Analysis for 2025 - 2032

Rotating Equipment Repair Market Size and Trends Analysis

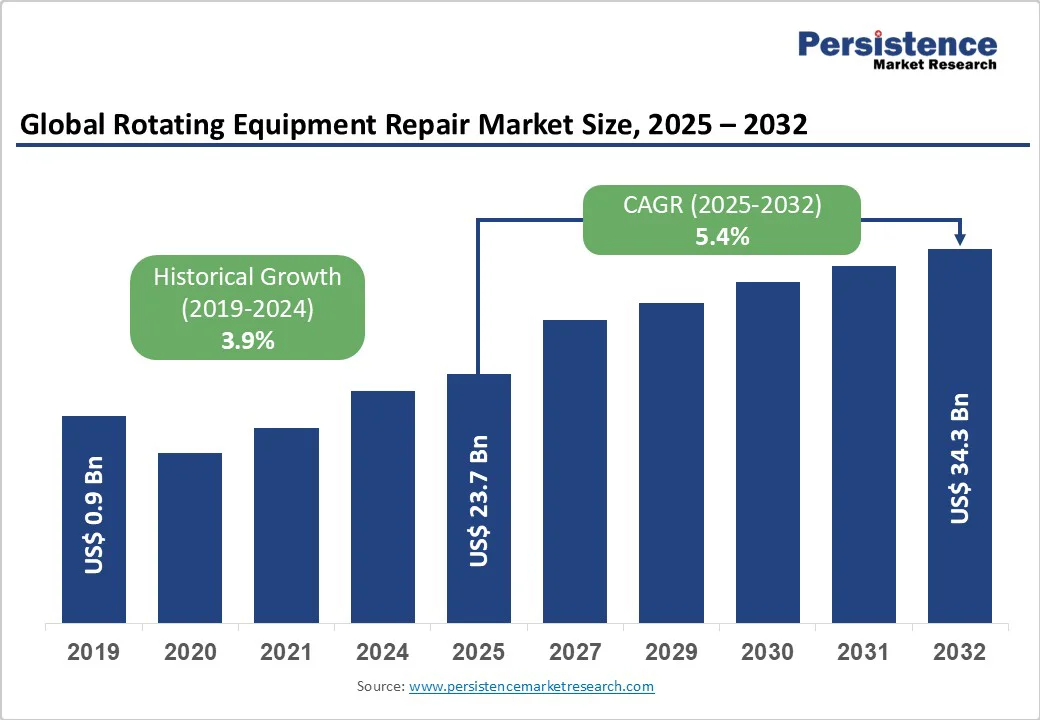

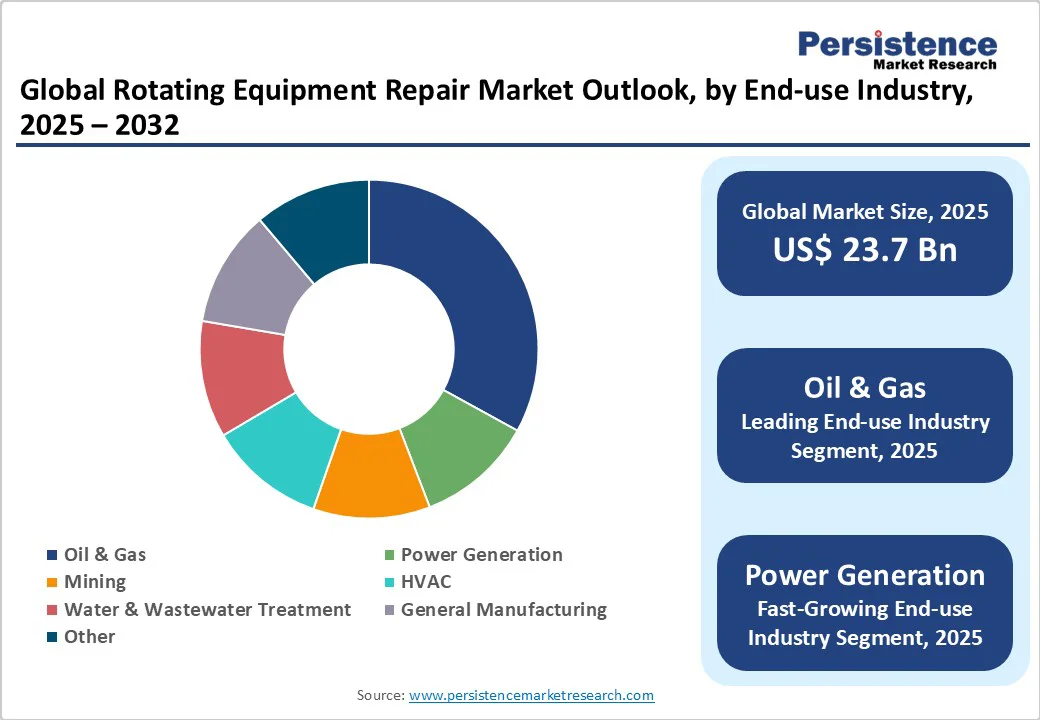

The global rotating equipment repair market size is likely to be valued at US$ 23.7 Billion in 2025 and is expected to reach US$ 34.3 Billion by 2032, growing at a CAGR of 5.4% during the forecast period from 2025 to 2032, driven by rapid industrialization and expanding energy demands, particularly in the oil & gas and power generation sectors, which necessitate reliable maintenance to minimize downtime.

The increasing adoption of IoT-enabled predictive maintenance enhances equipment efficiency, reducing operational costs by up to 50% through real-time monitoring and timely interventions. Global infrastructure developments, such as new power plants and refining capacities, are boosting the need for repair services to extend asset lifespans, ensuring sustained productivity across industries.

Key Industry highlights

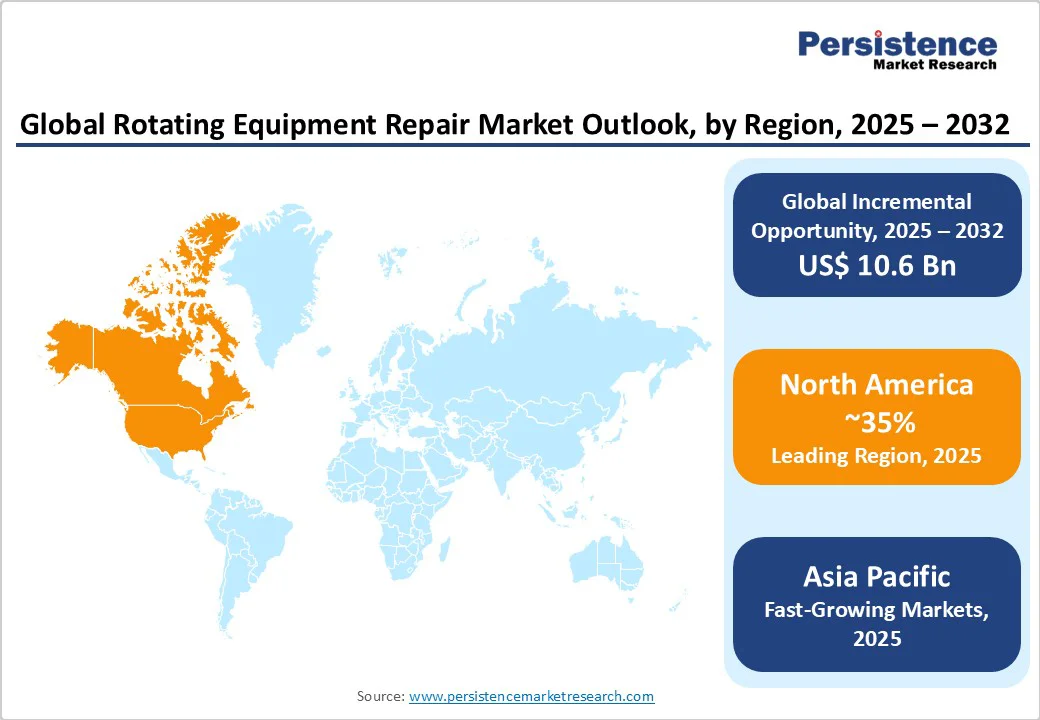

- Regional Leader: North America leads the market with over 35% share in 2025, driven by U.S. shale gas expansions and innovative repair technologies ensuring minimal disruptions in energy infrastructure.

- Fastest Growing Region: Asia Pacific is the fastest-growing region, propelled by India's industrial surge and China's manufacturing demands for efficient turbine and pump maintenance services.

- Leading Segment: Direct OEM-based dominates sales channel segments with 63% share, due to their compatibility with end-to-end solutions, which reduces equipment failures.

- Fastest-Growing Segment: Pumps represent the fastest-growing equipment segment, with a 35% share expansion due to water treatment and refining applications requiring advanced refurbishments.

- Growth Opportunities: The adoption of IoT predictive maintenance offers key opportunities, enabling 40% cost savings and real-time analytics for rotating assets in power and manufacturing sectors.

| Key Insights | Details |

|---|---|

| Rotating Equipment Repair Market Size (2025E) | US$23.7 Bn |

| Market Value Forecast (2032F) | US$34.3 Bn |

| Projected Growth CAGR (2025-2032) | 5.4% |

| Historical Market Growth (2019-2024) | 3.9% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Growth Analysis - Expanding Oil & Gas Sector Demands

The oil & gas industry's growth significantly propels the rotating equipment repair market, as upstream, midstream, and downstream operations rely heavily on pumps, compressors, and turbines that require frequent maintenance due to harsh environments.

According to the International Energy Agency, global oil production reached 103 million barrels per day in 2024, driving investments in equipment upkeep to prevent costly disruptions, with repair services reducing downtime by 30-40%.

This sector's expansion, including shale gas in North America and offshore projects in Asia, underscores the need for specialized repairs, fostering market resilience and efficiency gains for operators. The integration with related areas such as the centrifugal pumps market further amplifies demand, as efficient pump repairs ensure seamless fluid handling in extraction processes.

Adoption of Predictive Maintenance Technologies

Advancements in predictive maintenance, powered by IoT and AI, are accelerating market expansion by enabling proactive repairs for rotating equipment, minimizing unplanned outages in power generation and manufacturing. Industry reports indicate that such technologies can cut maintenance costs by 25% and extend equipment life by 20-50%, as seen in Siemens' implementations where vibration analysis detects anomalies early.

With the International Electrotechnical Commission standards promoting sensor integration, industries are shifting from reactive to data-driven strategies, boosting repair service utilization. This driver not only enhances operational reliability but also aligns with global sustainability goals by optimizing energy use in turbines and mixers.

Barrier Analysis - Skilled Labor Shortage

A critical barrier to the rotating equipment repair market is the shortage of skilled technicians proficient in handling complex rotating machinery, exacerbated by an aging workforce and rapid technological advancements. The U.S. Bureau of Labor Statistics projects a 7% decline in qualified mechanical engineers by 2030, leading to delays in repairs and increased costs, with some industries facing 20-30% higher downtime.

It particularly affects emerging markets, where training infrastructure lags, hindering timely service delivery for critical equipment such as gas turbines. Consequently, it limits market penetration and raises operational risks for end-users in high-stakes sectors.

High Initial Repair Costs

Elevated costs associated with advanced repair technologies and specialized parts pose a significant restraint, deterring smaller manufacturers from investing in comprehensive maintenance programs.

Data from the World Economic Forum highlights that repair expenses can account for 15-20% of total equipment lifecycle costs, straining budgets in volatile markets such as mining and HVAC. Regulatory compliance for safety and emissions further inflates these costs, slowing adoption in regions with economic constraints and reducing overall market accessibility.

Opportunity Analysis - Integration of IoT for Predictive Analytics

The rising integration of IoT in industrial settings presents a major opportunity for repair providers to offer advanced predictive services, targeting fast-growing segments such as power generation, where downtime costs exceed US$50 Billion annually globally.

According to market estimates, IoT adoption in manufacturing will reach 75% by 2025, enabling real-time monitoring of equipment health via sensors for pumps and compressors, potentially increasing service revenues by 40% through subscription models.

Recent developments, such as Siemens' generative AI enhancements in Senseye Predictive Maintenance, demonstrate how conversational AI can streamline diagnostics, appealing to end-users in oil & gas for reduced failures. This opportunity is amplified in renewable energy transitions, where hybrid turbine repairs could capture emerging demand in Asia Pacific.

Expansion in Renewable Energy Infrastructure

Opportunities abound in the renewable sector's growth, particularly for repairing wind and solar-integrated rotating equipment such as turbines, driven by policies, including the EU Green Deal, aiming for 40% renewable capacity by 2030.

The International Renewable Energy Agency reports that global renewable investments hit US$1.8 Trillion in 2024, creating demand for retrofit services to enhance efficiency in aging assets, with potential market gains of 25% in repair volumes.

News from GE Vernova's partnerships, such as blade reinforcements, highlights how providers can leverage this for long-term contracts in power generation. Focusing on Asia's manufacturing hubs, companies can tap into ASEAN's 6-7% annual growth in clean energy projects, positioning repairs as key to sustainable operations.

Category-wise Analysis

Nature of Service Insights

Repair emerges as the leading segment with approximately 30% market share in 2025, driven by its essential role in restoring functionality to critical rotating components such as bearings and seals in high-wear environments. This dominance is justified by industry data from the American Society of Mechanical Engineers, indicating that repair interventions prevent 70% of potential failures in pumps and turbines, ensuring compliance with operational standards.

The segment's prevalence stems from cost-effectiveness compared to full replacements, with sectors such as oil & gas prioritizing quick turnarounds to maintain production flows. The industrial mixer market expansion correlates with repair needs for agitators, as consistent upkeep supports efficient mixing processes in chemical plants.

Industry Insights

The Industry category is led by oil & gas with a 33% market share, attributed to the sector's intensive use of rotating equipment in upstream exploration and downstream refining, where equipment endures extreme pressures and corrosives. Sub-sectors such as midstream pipelines amplify this, with repairs ensuring pipeline integrity and safety under stringent API regulations. This leadership is further supported by the sector's vulnerability to mechanical wear, making repair services indispensable for sustained output.

Equipment Insights

Within the equipment category, pumps account for a 35% share, owing to their ubiquitous application in fluid transfer across industries, where failures can halt entire processes. Authentic data from the Hydraulic Institute reveals that pumps account for 60% of rotating failures in manufacturing, underscoring the need for specialized repairs to maintain flow rates and energy efficiency.

The leadership is reinforced by high installation volumes in water treatment and HVAC, with repairs extending service life by 25-30% via refurbishments. Linking to the centrifugal pumps market, growth in centrifugal variants drives repair demand for handling slurries and chemicals effectively.

Sales Channel Insights

The sales channel category features Direct OEM-based as the front runner with 63% share in 2025, preferred for its assured compatibility and warranty support on proprietary parts for turbines and compressors. This is evidenced by ISO 9001 certifications held by OEMs such as Siemens, ensuring quality repairs that reduce secondary failures by 40%, as per industry benchmarks.

The segment's edge lies in integrated service ecosystems, providing end-to-end solutions from diagnostics to commissioning, vital for complex equipment in power generation. Independent vendors complement but lag due to perceived risks in non-original components.

Regional Insights

North America Rotating Equipment Repair Trends

North America leads the market due to the U.S.'s robust oil & gas infrastructure, with shale production surpassing 13 million barrels per day in 2024, driving repair demands for pumps and turbines.

The Environmental Protection Agency's stringent emissions regulations mandate regular maintenance, fostering an innovative ecosystem where companies such as GE Vernova invest in AI-driven services. Recent developments, such as Duke Energy's turbine deals, highlight how regulatory frameworks support localized repairs, enhancing grid reliability amid rising energy needs.

This region's trends emphasize predictive technologies, with the Department of Energy reporting 20% downtime reductions via IoT in refineries, positioning North America as a hub for advanced refurbishments.

Europe Rotating Equipment Repair Trends

Europe market is shaped by harmonized regulations under the EU Machinery Directive, promoting standardized repairs across Germany, the U.K., France, and Spain, where Germany contributes 4.5% global share through its engineering prowess. In 2024, Germany's Fraunhofer Institute initiatives advanced retrofit services for steam turbines, aligning with net-zero goals and boosting efficiency in chemical plants.

The U.K.'s offshore wind expansions, per Offshore Energies UK, require specialized compressor repairs, while France's nuclear focus drives turbine overhauls. Performance analysis shows Spain's manufacturing resurgence, with 5% annual growth in repair contracts, supported by EU funding for sustainable upgrades, ensuring regional competitiveness.

Asia Pacific Rotating Equipment Repair Trends

The Asia Pacific region is witnessing robust growth, driven by China’s commanding 55.6% share of the East Asia market and India’s strong 8.4% CAGR, supported by rapid industrial expansion and large-scale infrastructure development.

In 2025, Japan's Torishima Pump expansions catered to power generation needs, leveraging cost advantages in component upgrades. ASEAN countries benefit from FDI in oil & gas, with ASEAN Secretariat data showing a 15% rise in repair services for mixers amid electronics surges.

China's aging infrastructure demands, per the National Development and Reform Commission, prioritize predictive maintenance, while India's Make in India initiative spurs local OEM repairs, harnessing manufacturing edges for a 6.3% regional CAGR.

Competitive Landscape

The global rotating equipment repair market is moderately consolidated, with top players such as General Electric Company, Siemens AG, and Flowserve Corporation controlling over 50% share through extensive service networks and technological expertise.

Companies pursue expansion via acquisitions and R&D in predictive analytics, as seen in IoT integrations, reducing costs by 25%. Key differentiators include OEM-backed warranties and AI tools, while emerging models such as performance-based contracts emphasize up-time guarantees. This structure fosters innovation but challenges smaller vendors in fragmented regions.

Key Market Developments

- January 2025: Sulzer AG acquired Davies and Mills Co.W.L.L. in Bahrain to enhance rotating equipment repair capabilities in the Middle East, adding expertise in motors and pumps servicing.

- March 2025: General Electric Company (GE Vernova) and Saudi Electricity Company completed the first locally-led gas turbine outage at Riyadh's 8th power plant, advancing skills in turbine maintenance.

- June 2025: Flowserve Corporation announced a merger with Chart Industries to strengthen industrial process technologies, including repair services for compressors and valves.

Companies Covered in Rotating Equipment Repair Market

- Flowserve Corporation

- General Electric Company

- Siemens AG

- KSB SE & Co. KGaA

- Ebara Corporation

- Sulzer AG

- John Wood Group PLC

- Torishima Pump Mfg. Co., Ltd

- MAN ES

- Stork

- Hydro Inc.

- Triple EEE

- Amaru Giovanni

- The Weir Group PLC

Frequently Asked Questions

The rotating equipment repair market is expected to reach US$34.3 Billion by 2032, reflecting steady growth from US$23.7 Billion in 2025 at a 5.4% CAGR, driven by industrial expansions.

Key drivers include oil & gas sector growth and IoT predictive maintenance adoption, reducing downtime by 30-50% and supporting energy efficiency in global operations.

he oil & gas sector leads with a 33% share due to high equipment wear in extraction and refining, necessitating frequent repairs to maintain production continuity.

North America holds the leading position with over 30% share, bolstered by U.S. shale innovations and regulatory support for advanced maintenance practices.

IoT-enabled predictive maintenance offers significant potential, with 75% adoption projected by 2025, enabling cost savings and extended asset life in renewables.

Leading players include Flowserve Corporation, General Electric Company, and Siemens AG.