- Pharmaceuticals

- Peptic Ulcer Drugs Market

Peptic Ulcer Drugs Market Size, Share, and Growth Forecast 2026 - 2033

Peptic Ulcer Drugs Market by Product (Proton Pump Inhibitors, Potassium-Competitive Acid Blockers (P-CABs), Antacids, H2-Antagonists, Antibiotics, Ulcer Protective), Indication (Gastritis, Gastric Ulcers, Duodenal Ulcers, Gastroesophageal Reflux Disease (GERD)), Distribution Channel (Hospital Pharmacies, Private Clinics, Drug Stores, Retail Pharmacies, E-Commerce), and Regional Analysis, 2026 - 2033

Peptic Ulcer Drugs Market Size and Trend Analysis

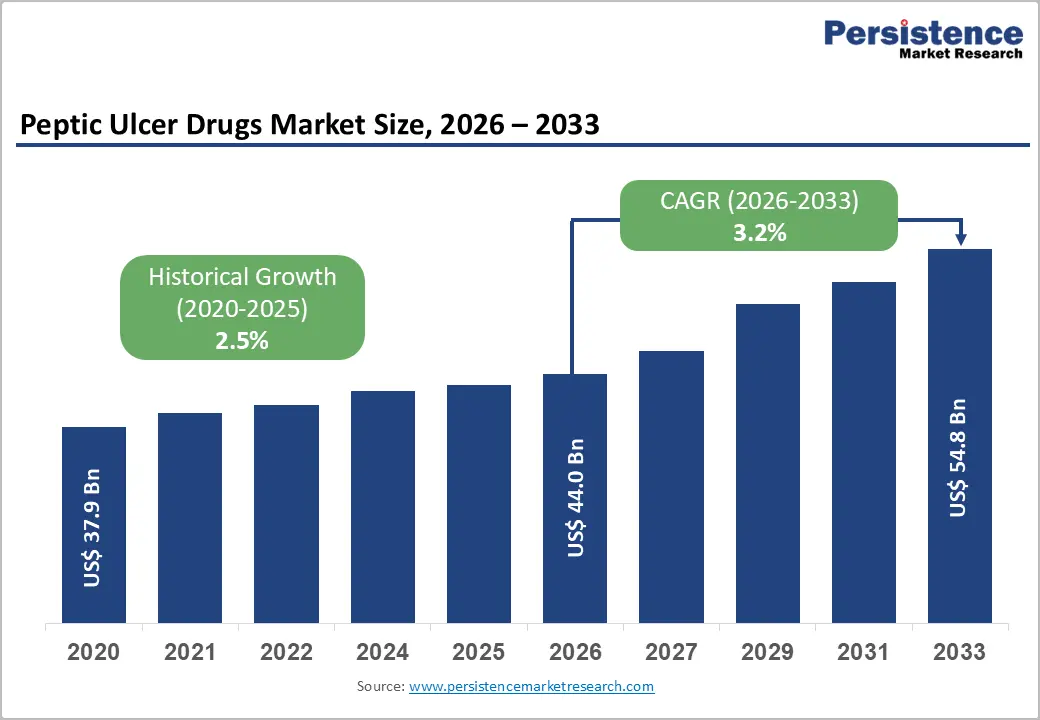

The global peptic ulcer drugs market size is expected to be valued at US$ 44.0 billion in 2026 and projected to reach US$ 54.8 billion by 2033, growing at a CAGR of 3.2% between 2026 and 2033, growing at a steady pace, underpinned by the sustained global burden of Helicobacter pylori infection estimated to affect over 44% of the world's population according to the World Gastroenterology Organisation (WGO). Additionally, the rising GERD prevalence is linked to obesity and sedentary lifestyles, and the pipeline entry of next-generation Potassium-Competitive Acid Blockers (P-CABs) offering clinical differentiation over incumbent proton pump inhibitors.

Generic drug proliferation in the PPI segment, increasing self-medication trends, and expanding pharmaceutical infrastructure in Asia-Pacific are collectively reinforcing the market's long-term revenue trajectory.

Key Industry Highlights:

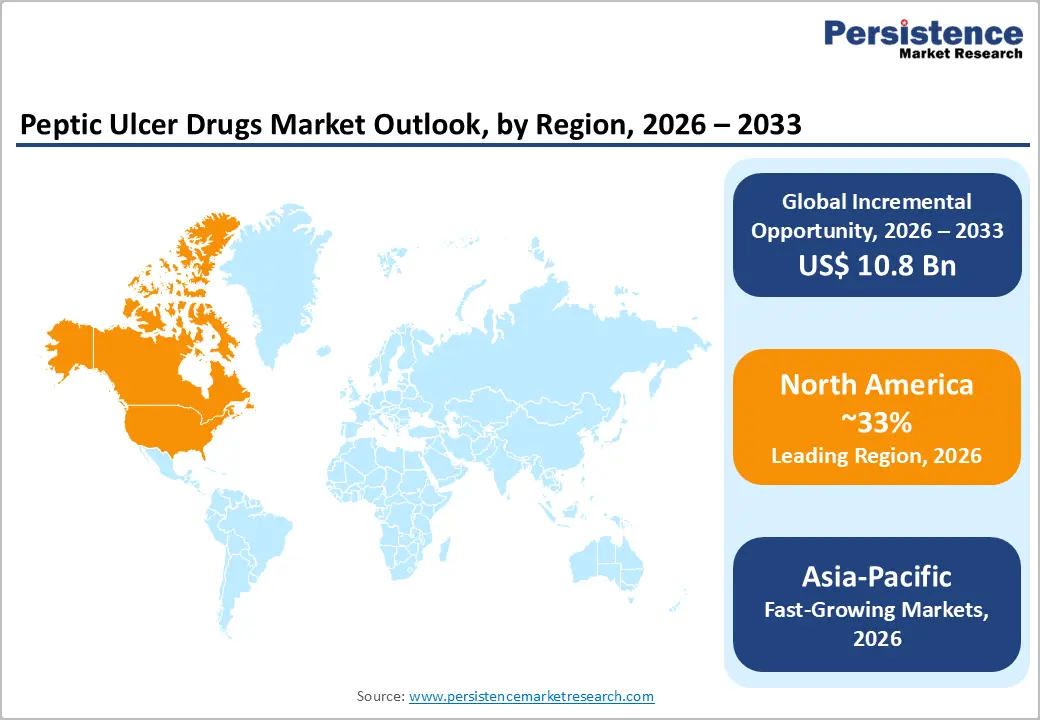

- Regional Leadership: North America leads the global peptic ulcer drugs market with approximately 33% share in 2025, driven by high GERD prevalence affecting 20% of adults per ACG data, comprehensive insurance coverage, and Phathom Pharma's U.S. P-CAB launch setting a premium innovation benchmark.

- Fast-growing Market: Asia Pacific is the fastest-growing region for peptic ulcer drugs, with H. pylori infection exceeding 50–60% prevalence in India and China per WGO data, Japan's pioneering P-CAB adoption, and rapidly expanding pharmaceutical infrastructure across ASEAN markets driving above-average growth.

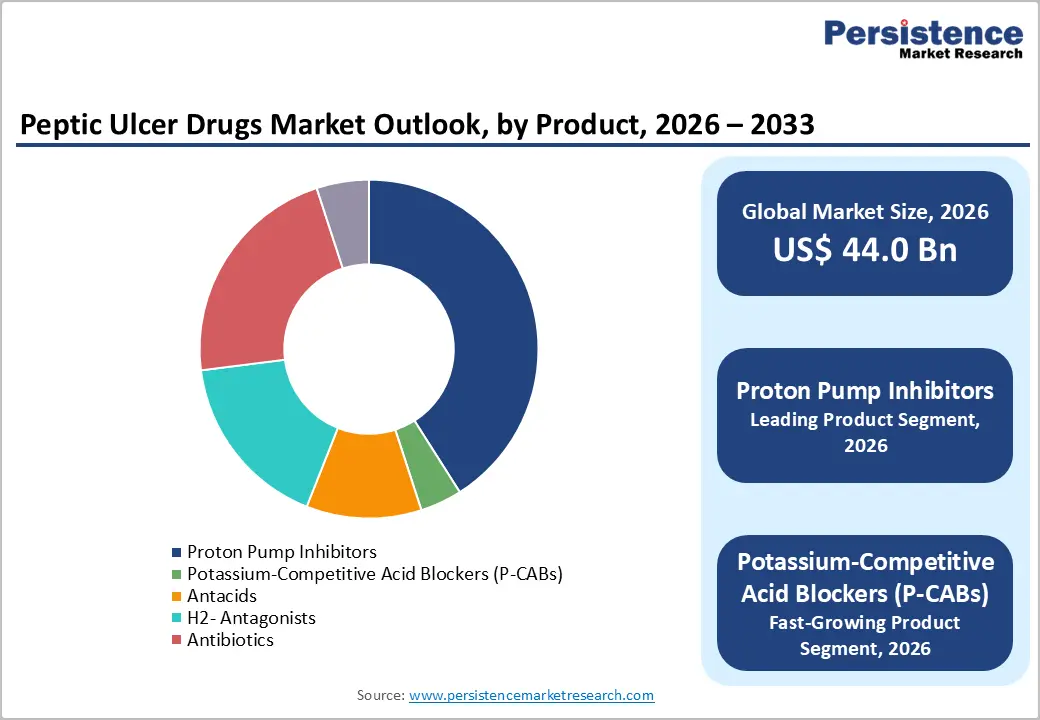

- Leading Product: Proton Pump Inhibitors (PPIs) dominate the product segment with approximately 41% share in 2025, endorsed by ACG and EHMSG guidelines as first-line H. pylori eradication and GERD treatment, with generic availability ensuring widespread prescriber and patient adoption globally.

- Fast-growing Product: Potassium-Competitive Acid Blockers (P-CABs) are the fastest-growing product segment, with vonoprazan demonstrating H. pylori eradication rates exceeding 84% versus ~70% for PPI regimens, earning FDA approval and rapid Asia-Pacific adoption through Takeda's Takecab market leadership.

- Opportunity: The key opportunity lies in P-CAB commercial expansion and antibiotic-resistant H. pylori eradication protocol development addressing a global treatment-refractory population where WGO identifies H. pylori infecting over 3.5 billion people, with growing clarithromycin resistance limiting conventional PPI-based therapy effectiveness.

Market Dynamics

Drivers - High Global Prevalence of H. pylori Infection and Peptic Ulcer Disease

The persistent global burden of Helicobacter pylori (H. pylori) infection remains the single most significant driver of peptic ulcer drug demand. The World Gastroenterology Organisation (WGO) estimates that H. pylori infects over 44% of the global population, approximately 3.5 billion people with prevalence reaching 70–90% in many developing regions of Asia, Africa, and Latin America. H. pylori is the causative agent for the majority of gastric and duodenal ulcers and is classified as a Group 1 carcinogen by the International Agency for Research on Cancer (IARC). The American College of Gastroenterology (ACG) guidelines mandate antibiotic-based eradication therapy, creating consistent demand across multiple drug classes, including PPIs, antibiotics, and bismuth-containing compounds.

Restraints - Patent Expiry of Major PPIs and Intensifying Generic Competition

The widespread patent expiration of blockbuster proton pump inhibitors, including omeprazole, esomeprazole, lansoprazole, and pantoprazole has substantially eroded branded PPI revenue over the past decade. The U.S. Food and Drug Administration (FDA) has approved numerous generic PPI formulations, with market research data confirming generic substitution rates exceeding 80% for most PPI molecules in the United States and major European markets. This intense generic competition has driven per-unit pricing down dramatically, significantly compressing overall market value growth despite stable or growing prescription volumes across the PPI drug class.

Opportunities - Potassium-Competitive Acid Blockers (P-CABs) Disrupting the Acid Suppression Market

The emergence of Potassium-Competitive Acid Blockers (P-CABs) as clinically superior alternatives to conventional PPIs represents the most transformative commercial opportunity in the peptic ulcer drugs market. P-CABs including vonoprazan (marketed as Voquezna by Phathom Pharma in the U.S., and as Takecab by Takeda Pharmaceutical Company Limited in Japan and Asia) offer faster onset of action, sustained acid suppression irrespective of meal timing, and improved H. pylori eradication rates versus standard PPI-based regimens. The FDA approved vonoprazan-based regimens in 2022 for H. pylori treatment, with clinical trials demonstrating eradication rates exceeding 84% compared to approximately 70% for clarithromycin-based PPI regimens, positioning P-CABs for rapid share capture from established PPI prescribing.

Category-wise Analysis

Product Insights

Proton Pump Inhibitors (PPIs) dominate the peptic ulcer drugs market by product, commanding approximately 41% of total product-based market share in 2025. PPIs, including omeprazole, esomeprazole (Nexium), pantoprazole, lansoprazole, and rabeprazole, are the globally recognized first-line pharmacotherapy for GERD, peptic ulcer disease, and H. pylori eradication regimens, entrenched through decades of clinical evidence, guideline endorsement, and physician familiarity. The American College of Gastroenterology (ACG) and the European Helicobacter and Microbiota Study Group (EHMSG) continue to recommend PPI-based triple or quadruple therapy as foundational H. pylori eradication protocols. While P-CABs are gaining momentum, PPIs' near-universal generic availability and extremely competitive price points sustain their dominant prescription share, particularly in generic-favorable healthcare markets across Asia, Latin America, and Eastern Europe.

Indication Insights

Gastroesophageal Reflux Disease (GERD) represents the leading indication segment in the peptic ulcer drugs market, capturing approximately 38% of total indication-based market share in 2025. GERD's dominance reflects its significantly higher prevalence versus discrete peptic ulcer disease affecting approximately 20% of adults in North America and Europe per American College of Gastroenterology (ACG) epidemiological data and its chronic, relapsing nature requiring long-duration pharmacological acid suppression. The World Gastroenterology Organisation (WGO) identifies GERD as the most common upper GI disorder managed in both primary and specialist care globally. Chronic GERD management drives consistently high PPI prescription volumes through maintenance therapy protocols, sustaining the indication's leading revenue contribution and supporting the growing P-CAB segment's targeted entry into treatment-refractory GERD patient cohorts.

Regional Insights

North America Peptic Ulcer Drugs Market Trends and Insights

North America dominates due to high diagnosis rates, strong drug access, and a large GERD patient pool. The U.S. alone reports ~4.6 million peptic ulcer cases annually, with ~10% population experiencing ulcers at some point. Additionally, GERD prevalence is 27%, driving long-term acid suppression therapy demand. High NSAID usage and an aging population further sustain drug consumption. Advanced healthcare infrastructure ensures early detection and consistent prescription use, supporting market dominance despite declining ulcer incidence.

U.S. Peptic Ulcer Drugs Market Trends and Insights

The U.S. leads the regional market and is expected to reach ~US$ 19 billion by 2026. High disease awareness and widespread use of PPIs drive demand. Around 4.6 million people are affected annually, while H. pylori accounts for up to 90% of duodenal ulcers. Strong insurance coverage and OTC availability further increase drug penetration. Aging population and chronic NSAID use continue to sustain demand, making the U.S. the dominant contributor globally.

Canada Peptic Ulcer Drugs Market Trends and Insights

Canada is expected to reach ~4.2% CAGR, driven by rising GERD burden and aging demographics. Increasing healthcare spending and improved diagnostic rates are expanding treated patient pools. GERD prevalence trends mirror North America (~20%), supporting long-term therapy demand. Government-backed healthcare access ensures steady prescription uptake, while increasing awareness and lifestyle-related disorders continue to drive moderate but consistent growth in the ulcer drug segment.

Europe Peptic Ulcer Drugs Market Trends and Insights

Europe holds a significant share due to high NSAID consumption, an aging population, and stable healthcare systems. The region shows high ulcer prevalence in Eastern Europe (~157 per 100,000 population), among the highest globally. Although H. pylori rates are declining, chronic diseases and medication-induced ulcers maintain demand. Strong reimbursement systems and widespread access to gastroenterology treatments support consistent drug usage across major European economies.

Germany Peptic Ulcer Drugs Market Trends and Insights

Germany leads the European market and is expected to reach ~US$ 6–7 Bn by 2026. The country has strong healthcare infrastructure and high NSAID consumption, contributing to ulcer incidence. Aging population significantly increases risk of gastric ulcers and complications. High diagnosis rates and insurance-backed drug access ensure consistent treatment uptake. Germany’s pharmaceutical market maturity and clinical adherence to guidelines make it the largest contributor in Europe.

United Kingdom Peptic Ulcer Drugs Market Trends and Insights

UK is poised to reach at ~4% CAGR, supported by increasing GERD prevalence and aging population. Public healthcare access through NHS ensures widespread treatment coverage. Rising lifestyle-related disorders and obesity are increasing acid-related conditions. Additionally, awareness campaigns and improved diagnostics are expanding the treated population, supporting steady market growth.

Asia Pacific Peptic Ulcer Drugs Market Trends and Insights

Asia Pacific is one of the fastest-growing markets due to a high infection burden and expanding healthcare access. Countries in this region report H. pylori prevalence exceeding 50%, significantly higher than Western regions. South Asia shows one of the highest ulcer prevalence rates globally (~156 per 100,000). Rapid urbanization, increasing NSAID use, and rising GERD incidence are further driving demand. Improving healthcare infrastructure and a large, untreated population base are accelerating market expansion.

China Peptic Ulcer Drugs Market Trends and Insights

China dominates the region and is expected to be valued at ~US$ 13 billion in 2026. High H. pylori infection burden (often >50%) drives strong demand for antibiotics and acid suppressants. Large population base and increasing healthcare access significantly expand treatment volume. Government healthcare reforms and rising awareness are improving diagnosis rates, making China the largest contributor in the Asia Pacific.

India Peptic Ulcer Drugs Market Trends and Insights

India is expected to achieve a growth of ~6.5% CAGR, driven by high infection prevalence and expanding healthcare access. South Asia has one of the highest ulcer burdens globally. Increasing OTC drug usage, improving diagnostics, and rising GERD cases due to lifestyle changes are key drivers. Government initiatives and private healthcare expansion are bringing more patients into treatment, making India the fastest-growing market in the region.

Competitive Landscape

The global peptic ulcer drugs market is moderately fragmented, with a dual-tier structure comprising innovator pharmaceutical companies pursuing P-CAB and combination therapy innovation led by Takeda Pharmaceutical Company Limited, Phathom Pharma, and Eisai Co. Ltd. and a highly competitive generic PPI tier dominated by manufacturers in India, China, and Eastern Europe. Key competitive strategies include P-CAB lifecycle expansion, H. pylori eradication combination drug development, and digital patient adherence programs. RedHill Biopharma is advancing novel H. pylori eradication regimens designed to address antibiotic resistance. Market differentiation increasingly centers on eradication efficacy data and adherence-supporting convenience formulations.

Key Developments:

- February 2026: Researchers reported that extracts from the Launaea herb demonstrated promising anti-ulcer activity in preclinical studies, suggesting a potential new avenue for treating peptic ulcers. The study found that the plant exhibited gastroprotective effects by reducing gastric acid secretion, enhancing mucosal defense, and showing antioxidant properties.

- September 2024: Lupin Limited announced that it had entered into a non-exclusive patent licensing agreement with Takeda Pharmaceutical Company Limited to commercialize vonoprazan in India. Vonoprazan, a novel potassium-competitive acid blocker (P-CAB), had been developed by Takeda for the treatment of acid-related disorders, including peptic ulcers and gastroesophageal reflux disease.

Global Peptic Ulcer Drugs Market – Key Insights & Details

| Key Insights | Details |

|---|---|

|

Historical Market Value (2020) |

US$ 37.9 Billion |

|

Projected Market Value (2026) |

US$ 44.0 Billion |

|

Projected Market Value (2033) |

US$ 54.8 Billion |

|

CAGR (2026-2033) |

3.2% |

|

Leading Region |

North America, 33% share |

|

Dominant Product |

Proton Pump Inhibitors, 41% share |

|

Top-ranking Indication |

Gastroesophageal Reflux Disease (GERD), 42% share |

|

Incremental Opportunity |

US$ 10.8 Billion |

Companies Covered in Peptic Ulcer Drugs Market

- Takeda Pharmaceutical Company Limited

- Pfizer Inc.

- Abbott Laboratories

- AstraZeneca plc.

- Cadila Healthcare Ltd.

- Boehringer Ingelheim GmbH

- Eisai Co. Ltd.

- Yuhan Corporation

- GlaxoSmithKline plc.

- RedHill Biopharma

- Phathom Pharma

- Others

Frequently Asked Questions

The market is set to reach US$ 42.6 Bn in 2025.

Daewoong Pharmaceutical Co., Ltd., Takeda Pharmaceutical Company Limited, Pfizer Inc. are a few leading players.

The industry is estimated to rise at a CAGR of 3.2% through 2032.

North America is projected to hold the largest share of the industry in 2025.

The market for is anticipated to reach a valuation of US$ 54.8 billion by 2032.