- Biotechnology

- Neuroscience Market

Neuroscience Market Size, Share, and Growth Forecast, 2025 - 2032

Neuroscience Market by Technology (Brain Imaging, Neuro-microscopy, Others), Component (Instruments & Consumables, Software, Services), End-user (Hospitals, Diagnostic Laboratories, Academic & Research Institutions, Others), and Regional Analysis for 2025 - 2032

Neuroscience Market Share and Trends Analysis

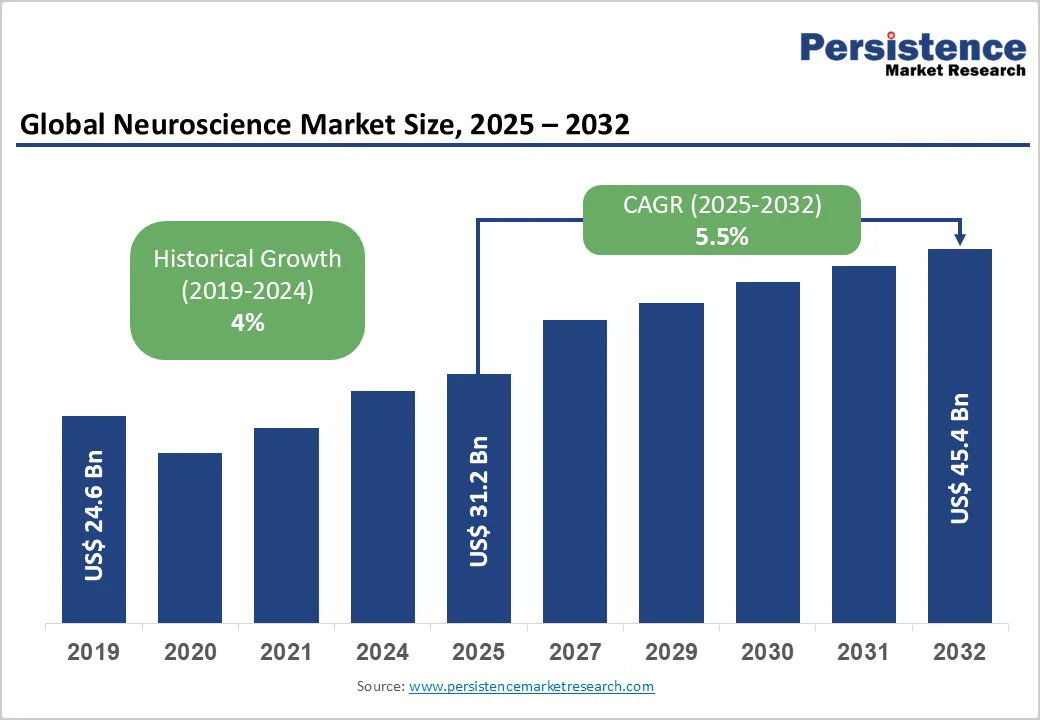

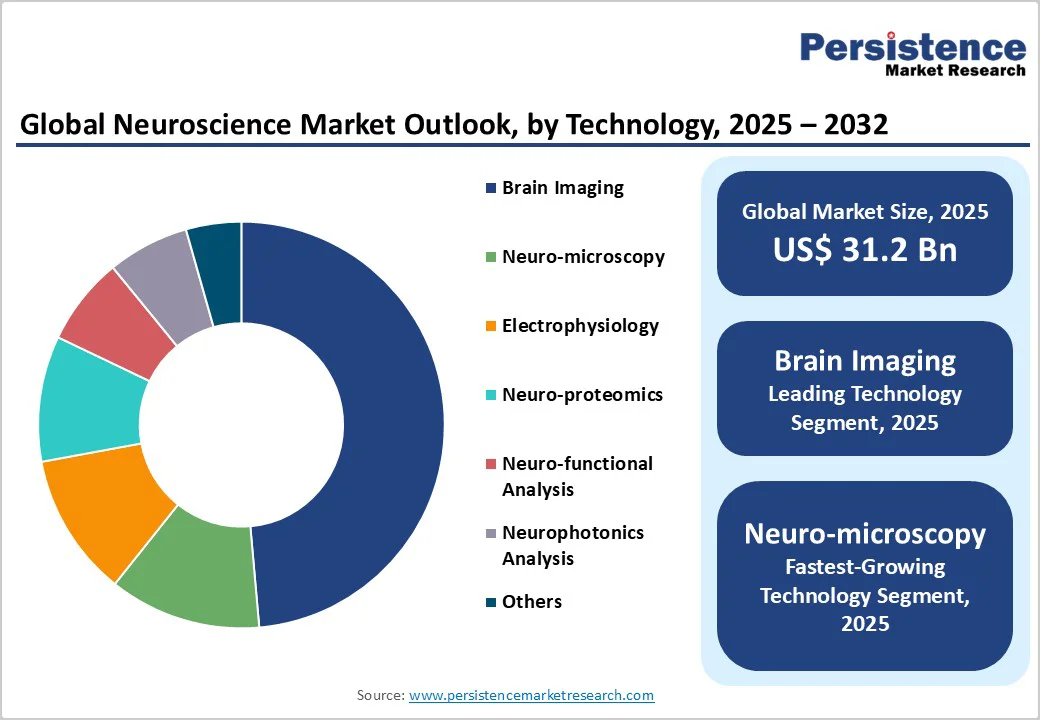

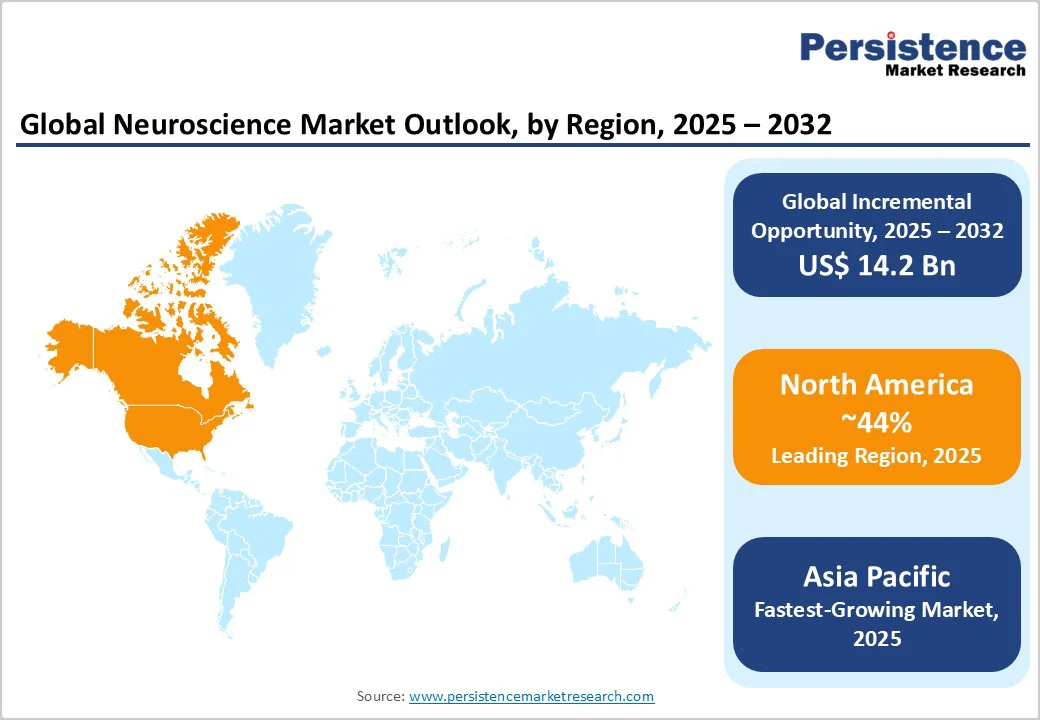

The global neuroscience market size is likely to be valued at US$31.2 Billion in 2025, and is estimated to reach US$45.4 Billion by 2032, growing at a CAGR of 5.5% during the forecast period from 2025 to 2032, driven by the rising prevalence of neurological diseases worldwide, increased investments in neuroimaging and AI-integrated diagnostics, and expanded utilization of brain imaging equipment in primary research and clinical settings.

Brain imaging and neuroinformatics see strong demand, led by hospitals and research centers; North America dominates through funding and regulation, while Asia Pacific grows fastest with expanding healthcare infrastructure and patient access.

Key Industry Highlights

- Leading Technology: Brain imaging is set to lead with an estimated 48.6% market share in 2025, driven by applications in research and clinical diagnosis.

- Fastest-growing Technology: Neuro-microscopy is projected to expand at the highest CAGR between 2025 and 2032, as single-cell and optogenetic methods gain traction.

- Leading Component: The instruments and consumables segment is likely to claim approximately 57.3% of the market revenue in 2025, underpinned by expanding hospital and laboratory usage.

- Fastest-growing Component: Software and SaaS models are opening new recurring revenue streams, forecast to grow the fastest through 2032.

- Regional Dominance: North America solidifies its leadership with around 43.8% market share in 2025 and remains a hub for R&D, regulatory innovation, and healthcare investment.

- Fastest-growing Regional Market: Asia Pacific is expected to be the fastest-growing regional market, advancing at a forecast CAGR of about 6.2% during 2025 - 2032 due to major investments in infrastructure and rising neurological disease incidence.

- Industry Trends: AI-powered MRI launches, major M&A in neuroinformatics, and collaborative innovation partnerships in neuroimaging and therapeutics have come to define the competitive landscape of the market.

- September 2025: Researchers at the University of Southern California (USC) developed a novel brain imaging method that reveals previously undetectable vascular changes linked to aging through enhanced visualization of small cerebral blood vessels and microvascular health, providing critical insights into brain aging and neurodegenerative diseases.

| Key Insights | Details |

|---|---|

| Neuroscience Market Size (2025E) | US$31.2 Bn |

| Market Value Forecast (2032F) | US$45.4 Bn |

| Projected Growth (CAGR 2025 to 2032) | 5.5% |

| Historical Market Growth (CAGR 2019 to 2024) | 4% |

Market Factors: Growth, Barriers, and Opportunity Analysis

AI-Driven Brain Mapping and Precision Diagnostics

Machine learning (ML) and AI are significantly reshaping advanced brain imaging and diagnostics, making early detection of neurological diseases both more accurate and scalable.

For example, U.S. and EU government initiatives such as the NIH Brain Research through Advancing Innovative Neurotechnologies (BRAIN) Initiative have injected over US$2.3 Billion in research funding since 2019, while collaborative innovation between tech giants and research institutes has led to breakthroughs in automating magnetic resonance imaging (MRI) and positron emission tomography (PET) scan interpretation.

Both regulatory agencies and payer systems increasingly recognize the clinical utility of AI-assisted imaging for diseases such as Alzheimer's, stroke, and brain tumors, expediting reimbursement pathways and driving global adoption.

This shift is reducing false-negative rates significantly in some studies and enabling actionable early interventions. Consequently, investments from both private and governmental sectors are expected to rise, cementing the digital-precision paradigm as a core long-term growth driver for neuroscience.

High Capital Expenditure and Operational Complexity in Advanced Imaging

Stalling the neuroscience market growth is the high initial capital required for installing and maintaining advanced imaging devices, such as 7-Tesla MRI or hybrid PET/MRI systems.

Hospitals and smaller diagnostic centers, particularly in Latin America and parts of Asia, face barriers as equipment costs typically exceed US$1.5-2 Million per unit, with associated annual service contracts and software upgrades adding an extra US$300,000 to US$500,000 in recurring expenses.

Integrating these devices into the digital workflow mandates a robust IT infrastructure and staff retraining, which can delay ROI and create operational inertia. This results in market fragmentation, reduces penetration in price-sensitive regions, and places pressure on device manufacturers to develop scalable, lower-cost alternatives without compromising performance, an ongoing structural risk for market expansion.

Demand Surge for Connectomics and Comprehensive Brain Mapping Solutions

The convergence of high-throughput neuroimaging, cloud-based analytics, and bioinformatics is catalyzing a fast-growing market for connectomics, which is the comprehensive mapping of neural circuit connectivity, particularly for large-scale academic and pharmaceutical research.

Global investments in connectomics have been increasing, according to the NIH, and are projected to rise steadily through 2032 as large population studies, such as the Human Connectome Project, gain momentum.

Opportunities are especially robust in mid-tier research institutes, biopharma R&D partnerships, and new contract research organizations (CROs) looking to capture value in functional brain circuit mapping for psychiatric and neurodegenerative disorders.

With the growing intersection between cutting-edge technologies and neuroscience research, cloud-based analytics vendors and imaging device makers can offer integrated workflow solutions, particularly as data privacy rules and open-science initiatives support scalable, multicenter collaboration.

Category-wise Analysis

Technology Insights

In 2025, brain imaging technologies, including MRI, PET, and functional MRI (fMRI), will continue to dominate the market, with an estimated 48.6% of the neuroscience market revenue share. This is due to their unparalleled capability to provide structural and functional insights critical for early diagnosis, disease monitoring, and research.

The integration of AI and deep learning into these systems is transforming clinical workflows by reducing scan times and improving diagnostic accuracy, which further incentivizes hospital and research institution spending.

The rapid evolution of high-field MRI systems and hybrid PET/MRI machines is enabling nuanced exploration of neurodegenerative and psychiatric conditions, extending their applications beyond traditional diagnostics to personalized medicine and targeted therapies.

From 2025 to 2032, neuroinformatics and brain network analysis are projected to grow at a CAGR of approximately 8.2%, driven by the rising need for comprehensive neural connectivity mapping, especially in psychiatric and neurodegenerative disorders.

Developments in ML algorithms and cloud-based platforms facilitate large-scale data integration, enabling researchers and clinicians to extract meaningful insights from complex brain datasets. The convergence of edge computing, AI, and neurobiological data architectures is creating opportunities for innovative diagnostic tools and personalized neurotherapies, positioning neuroinformatics as a pivotal driver of future market growth.

Component Insights

Instruments such as MRI, CT, EEG, and neurostimulation devices are likely to account for roughly 57.3% of the total revenue in the component category. The high durability, technological sophistication, and critical clinical decision-making roles of these devices sustain their market dominance.

Innovations such as portable EEG units, improved neurostimulators, and AI-enabled imaging processors are expanding applications, especially in outpatient settings and low-resource markets. As governments and healthcare providers prioritize neurological disease diagnosis, the instrumentation segment will continue to experience consistent growth, supported by ongoing R&D investments.

Software solutions, which encompass AI-driven analytics, neuroinformatics platforms, and remote monitoring applications, are forecasted to grow at a CAGR of approximately 8.1% during 2025 - 2032. The shift to cloud-based data management, combined with increasing adoption of tele-neurology and AI-powered diagnostic tools, is boosting software revenues.

Vendors offering modular, scalable, and secure data analytics solutions are well-positioned to enlarge their market share. This shift is driven by the need to manage vast neurodata efficiently, especially with the rising deployment of high-throughput imaging systems and neurostimulation devices.

End-user Insights

Hospitals, including academic medical centers and specialty clinics, are set to dominate with an estimated market share of 38.5% in 2025. This is due to their role in routine neurological diagnostics, neurosurgery, and integration of advanced neuroimaging systems.

The demand for high-fidelity imaging and neuromodulation therapies in treatment protocols significantly contributes to this dominance. The increasing prevalence of neurological disorders, such as Alzheimer’s and stroke, further amplifies hospital utilization, especially in the developed economies of North America and Europe.

Academics and research institutions are projected to grow at the highest CAGR from 2025 to 2032. This growth is driven by increased government grants, international research collaborations, and private sector investments in neuroscience R&D.

These centers are adopting cutting-edge neurotechnologies such as connectomics, brain-computer interfaces (BCIs), and optogenetics. The push for translational research is generating opportunities for vendors specializing in neuroinformatics, advanced imaging, and neuromodulation devices. The segment growth is critical for innovation pipelines and early-stage startups aiming to commercialize new neurodiagnostic and therapeutic solutions.

Regional Insights

North America Neuroscience Market Trends

North America is slated to retain a commanding 43.8% of the neuroscience market share in 2025, with the U.S. leading due to high R&D investment, regulatory pathways favorable for innovation, and a well-established clinical ecosystem.

The region’s advanced healthcare infrastructure facilitates the deployment of high-end neurotechnologies, including AI-integrated imaging, gene therapies, and neurostimulation devices. Private investments in neurotech startups are fueling innovation, with strategic alliances between pharmaceutical companies and neurotech startups becoming more common.

Regulatory bodies such as the U.S. Food and Drug Administration (FDA) are streamlining approval processes for neurodiagnostic and neurostimulation devices, further fostering market growth.

The competitive landscape of North America features dominant players such as Siemens and GE Healthcare, with a growing presence of startups specializing in AI-powered neurodiagnostics. Large funding pools, favorable IP protections, and a vibrant innovation ecosystem create a fertile environment for sustained growth and technological breakthroughs.

Europe Neuroscience Market Trends

Europe is predicted to hold an estimated 27.1% the market share in 2025, with key hubs in Germany, the U.K., and France. Projected CAGR ranges around 5.1% through 2032, with steady expansion fostered by regulatory harmonization, increased public funding, and collaborative research programs such as Horizon Europe across the European Union (EU).

The European Medical Devices Regulation (MDR) has increased compliance standards but also incentivized high-quality device manufacturing, creating opportunities for premium-priced innovative solutions. The region’s strength lies in its combination of academic research excellence, robust healthcare policies, and strategic investment in translational research, particularly in neurodegenerative diseases.

Expanding budgetary allocations from national ministries of health for medical research and dedicated neuroscience institutes support a pipeline of new diagnostics and therapeutics. The competitive landscape features significant contributions from Siemens, Philips, and emerging biotech startups focused on neuromodulation and neuroinformatics.

Challenges such as bureaucratic complexities and fragmented funding streams are being addressed through cross-border projects and EU grants, laying the groundwork for sustained market growth.

Asia Pacific Neuroscience Market Trends

Asia Pacific is expected to command around 19.7% of the global market share in 2025, with an impressive CAGR extending through 2032. The market rests on China, Japan, and India, where government-led initiatives such as China’s Brain Project and substantial healthcare infrastructure investments are energizing research into neuroscience and neurology.

Cost-competitive manufacturing, especially in high-end neuroimaging hardware, allows international and local companies to supply scalable neurodiagnostic solutions. The region's large, aging population and increasing incidence of neurological diseases such as stroke and Alzheimer’s create a substantial unmet clinical need, prompting massive investments in neurotechnologies.

Regulatory reforms are gradually aligning to facilitate faster approval processes, enabling quicker adoption. Strategic alliances between Western industry leaders and local firms are expanding market reach, while innovative startups focus on low-cost diagnostic solutions, neurostimulation, and digital health integrations.

The thriving research ecosystem and growing venture capital investments position Asia Pacific as a manufacturing and innovation hub for neurotechnologies, underpinning rapid growth.

Competitive Landscape

The global neuroscience market structure is moderately fragmented, with the top dozen players collectively dominating approximately 40% of the total revenue. The industry features a core group of multinational corporations (MNCs), including Siemens, GE Healthcare, Philips, and Medtronic, whose extensive portfolios span advanced imaging, neurostimulation, and neurodiagnostic software.

These incumbents leverage their global footprint to penetrate emerging markets, maintain dominance in R&D, and forge strategic alliances with academic and clinical institutions. A significant portion of the market comprises niche and mid-tier players focusing on specialized segments such as neuroinformatics, drug delivery devices, and AI-enabled diagnostics.

The ongoing vertical integration trend, which entails merging hardware, software, and clinical services, has led to more comprehensive, end-to-end solutions. Industry consolidation is driven by strategic acquisitions and alliances, aimed at expanding technological capabilities and geographic reach. As neurodigitalization accelerates, new entrants with innovative AI algorithms, low-cost sensors, and cloud-based analytics are gaining traction, marking an evolving competitive landscape.

Key Industry Developments

- In September 2025, the University of Sydney partnered with Siemens Healthineers in a US$9 Million deal to launch the Cima.X 3T MRI, enhancing brain mapping, supporting MRI-guided procedures, and accelerating neuroscience research, early disease detection, and innovative treatments.

- In September 2025, GE HealthCare announced plans to acquire icometrix, integrating its AI-powered icobrain platform with GE’s MRI systems to enhance neurological care. The move aims to improve diagnosis, support personalized treatment, and expand access to icobrain aria for monitoring amyloid-related imaging abnormalities across MRI vendors.

- In July 2025, NIH-supported researchers developed the Connectome 2.0 MRI, an ultra-high-resolution scanner that images microscopic brain structures noninvasively. Offering near single-micron precision, it maps brain fibers and cellular architecture in real time. Its compact, multi-channel design advances the BRAIN Initiative, enabling precision neuroscience and tailored brain stimulation therapies for neurological disorders.

Companies Covered in Neuroscience Market

- Siemens Healthineers AG

- GE Healthcare Technologies Inc.

- Koninklijke Philips N.V.

- Medtronic plc

- Nihon Kohden Corporation

- Natus Medical Incorporated

- NeuroPace Inc.

- Plexon Inc.

- Blackrock Neurotech

- Compumedics Ltd.

- Fujifilm Holdings Corporation

- Canon Medical Systems Corporation

- Bruker Corporation

- Boston Scientific Corporation

- Abbott Laboratories

Frequently Asked Questions

The neuroscience market is projected to reach US$31.2 Billion in 2025.

The rising prevalence of neurological diseases worldwide and increased investments in neuroimaging and AI-integrated diagnostics are driving the neuroscience market.

The neuroscience market is poised to witness a CAGR of 5.5% from 2025 to 2032.

Expanded utilization of brain imaging equipment in primary research and clinical settings, development of advanced neuroinformatics, and growing collaborations between hospitals, academic research institutes, and healthcare technology companies are key market opportunities.

Siemens Healthineers AG, GE Healthcare Technologies Inc., and Koninklijke Philips N.V. are a few of the key market players.