- Medical Devices

- Kidney Dialysis Equipment Market

Kidney Dialysis Equipment Market Size, Share, and Growth Forecast, 2025 - 2032

Kidney Dialysis Equipment Market By Product Type (Hemodialysis Equipment, Peritoneal Equipment), Disease Condition (Chronic, Acute Kidney Disease), End-user (In-center Dialysis Centers, Home Care Settings), and Regional Analysis for 2025 - 2032

Kidney Dialysis Equipment Market Size and Trends Analysis

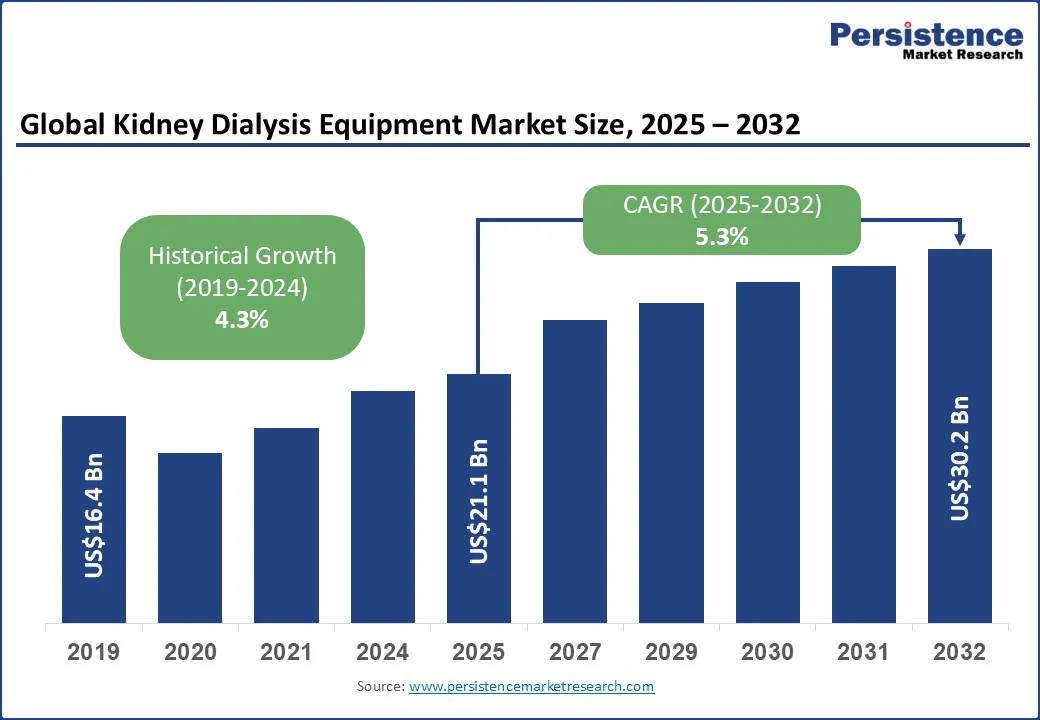

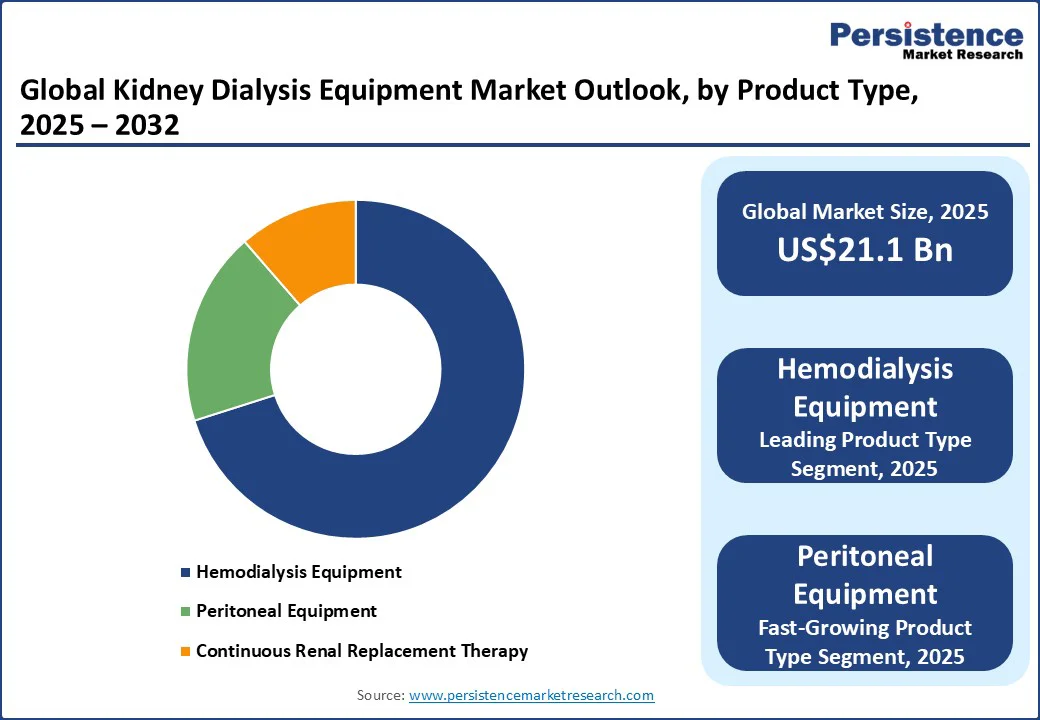

The global kidney dialysis equipment market size is likely to be valued at US$21.1 Bn in 2025 and is estimated to reach US$30.2 Bn in 2032, growing at a CAGR of 5.3% during the forecast period 2025-2032.

The kidney dialysis equipment market growth is driven by the increasing prevalence of chronic and acute kidney diseases, as well as healthcare policies that emphasize home-based care. Key players are investing in novel hemodialysis and peritoneal systems, integrating automation, remote monitoring, and home-use capabilities to differentiate their products. In Asia Pacific, China and India are extending dialysis programs to manage the rising cases of end-stage renal disease (ESRD) population, promoting machines that balance cost-effectiveness with reliability.

Key Industry Highlights:

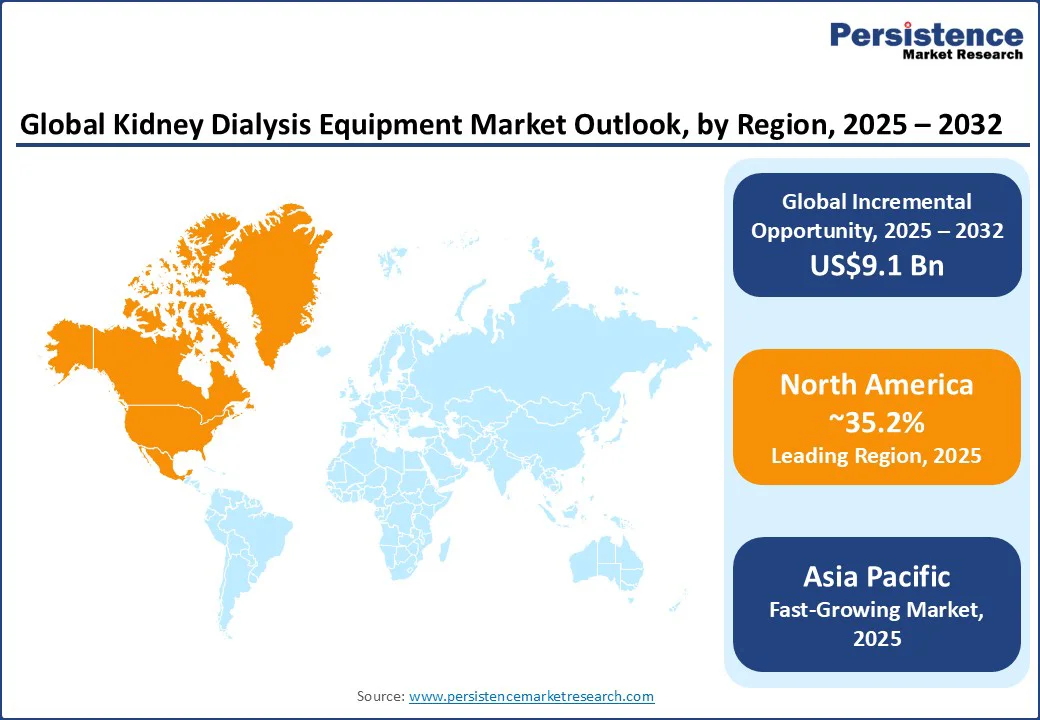

- Leading Region: North America, with around 35.2% share in 2025, due to favorable reimbursement policies and expansion of home dialysis initiatives.

- Fastest-growing Region: Asia Pacific, backed by government-supported dialysis programs and increasing investments in hospital infrastructure.

- Dominant Product Type: Hemodialysis equipment with about 70.1% share in 2025, owing to clinician familiarity and recurring revenue from consumables.

- Leading Disease Condition: Chronic kidney disease records nearly 67.3% of the kidney dialysis equipment market share in 2025, backed by high prevalence and progressive nature.

- New Product Launch: Four Square Medical Center launched the novel Dimi Home Dialysis Machine in January 2025. The new machine is designed to improve dialysis treatment at home, and it operates without the requirement for reverse osmosis.

|

Global Market Attribute |

Key Insights |

|

Kidney Dialysis Equipment Market Size (2025E) |

US$21.1 Bn |

|

Market Value Forecast (2032F) |

US$30.2 Bn |

|

Projected Growth (CAGR 2025 to 2032) |

5.3% |

|

Historical Market Growth (CAGR 2019 to 2024) |

4.3% |

Market Dynamics

Driver - Rising Prevalence of Kidney Diseases Fuel Growth

The surging prevalence of kidney diseases is accelerating demand for kidney dialysis equipment as it creates a continuous patient pool requiring renal replacement therapy. Chronic Kidney Disease (CKD) and Acute Kidney Injury (AKI) are no longer confined to aging population.

Lifestyle-related conditions, including diabetes, hypertension, and obesity, are causing ESRD to appear early. According to a 2023 reportby the Centers for Disease Control and Prevention (CDC), more than one in seven U.S. adults is estimated to have chronic kidney disease (CKD), highlighting a growing demand for hemodialysis and peritoneal therapies.

The increased disease burden is also propelling healthcare strategies. Governments and large dialysis organizations are broadening capacity to manage rising ESRD cases. In China, national volume-based procurement policies are encouraging hospitals to standardize on certain dialysis platforms to manage the growing patient volume effectively. These initiatives make dialysis equipment an essential part of national and regional healthcare infrastructure.

Restraint - Potential Side-effects and Complications Related to Vascular Infections

Adverse effects and patient discomfort are key barriers to the wide adoption of dialysis equipment. Infection risk is one of the most serious concerns, specifically with vascular access in hemodialysis and catheter use in peritoneal dialysis. Patients with compromised immunity or poorly maintained access are prone to bloodstream infections, leading to hospitalization or sepsis. These risks discourage patients from initiating or continuing dialysis, indirectly limiting equipment adoption.

Frequent dialysis sessions also contribute to patient fatigue, discouraging consistent treatment adherence. Hemodialysis typically requires three sessions per week, each lasting several hours, leaving patients physically drained. Even with home dialysis and portable machines, the treatment burden can disrupt daily life.

It further reduces the willingness to adhere to therapy or consider switching modalities. Itchy skin or pruritus is another common complication that affects the quality of life. Uremic toxins and phosphate accumulation in patients contribute to persistent itching, thereby hampering the uptake.

Opportunity - Shift toward Home and Portable Dialysis Solutions Creates Avenues

Developments in portable and home dialysis systems are creating new avenues for manufacturers by shifting dialysis from being a hospital-centric service to one embedded in everyday life. Traditional in-center dialysis has long been tied to rigid schedules and clinical infrastructure. Compact machines now allow patients to manage treatment at home, in assisted living, or during travel. Home-focused developments are further broadening the competitive landscape.

Quanta’s SC+ system, cleared by the FDA for home hemodialysis, provides a compact yet high-dose treatment option that bridges the gap between hospital-grade performance and patient usability. In the U.K., the National Health Service (NHS) has piloted the SC+ across trust as part of its push to expand home therapies.

It shows how government contracts help bolster the adoption of these systems. For manufacturers, this creates an opportunity to sell machines, bundle remote monitoring software, training modules, and consumables made for home patients.

Category-wise Analysis

Product Type Insights

Based on product type, the market is divided into hemodialysis equipment, peritoneal equipment, and continuous renal replacement therapy. Among these, hemodialysis equipment is projected to account for nearly 70.1% of the market share in 2025, owing to clinical comfort.

Nephrologists and nurses are deeply trained in HD protocols. Hence, introducing updated equipment involves marginal learning curves rather than complete retraining. Hospitals facing staffing shortages often choose machines with guided priming, single-use cartridges, and automation layers that reduce human touchpoints.

Peritoneal equipment is gaining momentum as it directly answers the healthcare system’s twin challenges of cost and access. It does not require dedicated water systems or large clinical infrastructure, which makes it convenient to expand coverage in regions with limited hospital capacity. Technology improvements have also changed perceptions of peritoneal dialysis equipment. Modern cyclers now integrate with digital platforms that allow remote patient monitoring and two-way communication between patients and care teams.

Disease Condition Insights

By disease condition, the market is bifurcated into chronic and acute kidney disease. Out of these, Chronic Kidney Disease (CKD) is anticipated to hold around 67.3% of the market share in 2025, as it is progressive, silent in its early stages, and increasingly tied to lifestyle-related illnesses.

Patients with diabetes and hypertension now form the bulk of CKD cases. When kidney function declines to ESRD, dialysis becomes unavoidable unless transplantation is an option. The continuous influx of patients highlights the central role of dialysis equipment in the management of CKD.

Acute kidney disease, commonly referred to as Acute Kidney Injury (AKI), is gaining prominence because hospitals are seeing it as a mortality driver and a long-term cost booster. Unlike chronic kidney disease, which develops slowly, AKI can appear suddenly after surgery, sepsis, or exposure to nephrotoxic drugs. Its rising profile is associated with critical care admissions during and after the COVID-19 pandemic, when ICUs reported surges in AKI cases among ventilated patients.

Regional Insights

North America Kidney Dialysis Equipment Market Trends - Routine ESRD Payment Updates Affect Device-Service Bundles

In 2025, North America is predicted to account for approximately 35.2% share due to the ongoing shift of policy, ownership, and product clearances in the region. In the U.S. kidney dialysis equipment market, the Centers for Medicare & Medicaid Services (CMS) is still nudging providers toward home modalities through its ETC model. However, a new proposal is speculated to wind the program down after December 2025, keeping home-first strategies on the agenda while pushing uncertainty into long-term investments.

Routine payment updates to the ESRD bundle continue, which matters for tenders and device-service bundles that hinge on operating margins. Home hemodialysis is getting fresh hardware options. Quanta’s system bagged U.S. clearance for home use in November 2024, giving clinicians a compact and higher-flow alternative to the incumbent NxStage installed base. Outset Medical, after grappling with a 2023 warning letter, received FDA confirmation in February 2025 that its corrective actions resolved the issues. These events broaden the choice for clinics building home fleets.

Asia Pacific Kidney Dialysis Equipment Market Trends - China’s Volume-based Procurement Influences Unit Pricing

In Asia Pacific, Japan has already made online hemodiafiltration (HDF) the default. As per the Japanese Society for Dialysis Therapy (JSDT), nearly 59.1% of dialysis patients in the country were on HDF at the end of 2023. It encouraged hospitals to buy machines and water systems that can reliably deliver convective volumes and improve nurse steps. This encouraged domestic players to emphasize automation, biofeedback, and compact designs for dense units.

China’s national Volume-Based Procurement (VBP) approach has expanded from drugs into devices and consumables. It has created headwinds on unit pricing but powerful tailwinds on volumes as providers standardize on a few winners.

Multinationals report VBP as supportive for growth in procedures but negative for price. Hence, local guidelines continue to formalize access and adequacy targets that dictate machine features and consumables specs. India’s Pradhan Mantri National Dialysis Program now operates across all states, backing both HD and Peritoneal Dialysis (PD).

Europe Kidney Dialysis Equipment Market Trends - U.K. Home Dialysis Campaign Supports Program Expansion

Europe’s market is defined by mature in-center hemodiafiltration and procurement that rewards whole ecosystem lines rather than standalone machines. Clinical guidance has moved toward online hemodiafiltration after the 2025 EuDial Working Group consensus, comparing it with high-flux HD. This strengthened hemodiafiltration’s advantages in middle-molecule clearance and downstream outcomes. The clinical pull is visible in vendors’ portfolios already common across EU clinics.

Regulation is further influencing product launches and the continuity of supply. The EU extended Medical Device Regulation (MDR) transition deadlines, which eased immediate certificate pressure on legacy devices while still boosting stepwise compliance.

It has helped hospitals avoid abrupt switches while vendors re-certify. The U.K.’s National Kidney Federation also published a Home Dialysis Campaign Manifesto in June 2025 after a parliamentary summit. It gave political cover to trusts expanding home programs.

Competitive Landscape

The global kidney dialysis equipment market is characterized by geography and care delivery models. In the U.S. and parts of Europe, large dialysis organizations, such as DaVita and the provider network owned by Fresenius, play a significant role in influencing procurement decisions.. This helps to create high entry barriers for small-scale manufacturing companies.

Markets in Asia Pacific and Latin America, however, remain more fragmented. They enable companies to expand through localized partnerships and low-cost ranges. Japan is particularly distinctive, where domestic players such as Nikkiso and Toray retain powerful footholds due to regulatory preferences and membrane technology expertise.

Key Industry Developments

- In June 2025, Renalyx Health Systems introduced RENALYX - RxT 21, the world's first fully indigenous, AI, and cloud-enabled smart hemodialysis machine. It features real-time remote monitoring and a clinical connectivity facility.

- In September 2024, Fresenius Medical Care launched the NxStage Versi HD with GuideMe Software. The launch came after the company achieved a growth milestone of more than 14,000 U.S.-based patients using its NxStage systems to perform Home Hemodialysis (HHD) therapy.

Companies Covered in Kidney Dialysis Equipment Market

- Baxter International

- Asahi Kasei Corporation

- Cantel Medical Corporation

- Fresenius Medical Care AG & Co. KGaA

- B. Braun Melsungen AG

- Teleflex Incorporated

- JMS Co. Ltd.

- Rockwell Medical Inc.

- Hemoclean Co., Ltd.

- Outset Medical, Inc.

- Quanta Dialysis Technologies

- Nipro

Frequently Asked Questions

The kidney dialysis equipment market is projected to reach US$21.1 Bn in 2025.

The rising prevalence of kidney diseases and government-backed health programs are the key market drivers.

The kidney dialysis equipment market is poised to witness a CAGR of 5.3% from 2025 to 2032.

The emergence of affordable dialysis solutions and the integration of digital monitoring represent key opportunities in the market.

Baxter International, Asahi Kasei Corporation, and Cantel Medical Corporation are a few key market players.