- Pharmaceuticals

- Gynaecological Cancer Drugs Market

Gynaecological Cancer Drugs Market Size, Share, and Growth Forecast, 2026 - 2033

Gynaecological Cancer Drugs Market by Indication (Cervical Cancer, Uterine Cancer, Ovarian Cancer, Vaginal & Vulvar Cancer), Therapeutic Modality (Chemotherapy, Targeted Therapy, Hormonal Therapy), and Regional Analysis for 2026 - 2033

Gynaecological Cancer Drugs Market Size and Trends Analysis

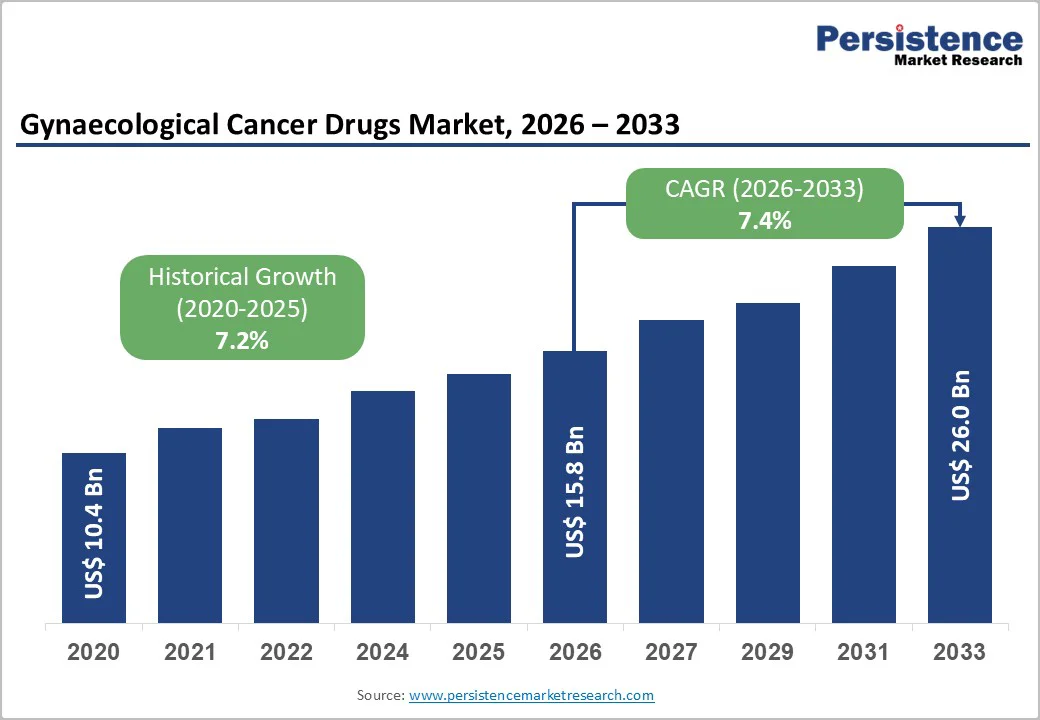

The global gynaecological cancer drugs market size is likely to be valued at US$15.8 billion in 2026, and is expected to reach US$26.0 billion by 2033, growing at a CAGR of 7.4% during the forecast period from 2026 to 2033, driven by the increasing prevalence of ovarian and cervical cancers, rising adoption of targeted therapies, and advancements in immunotherapy.

Rising demand for effective treatments for hormone-sensitive and uterine cancers is driving gynaecological cancer drug adoption, supported by advances in chemotherapy and hormonal therapies. Growing emphasis on personalized, less toxic options and early intervention, especially in North America, is fueling market growth.

Key Industry Highlights:

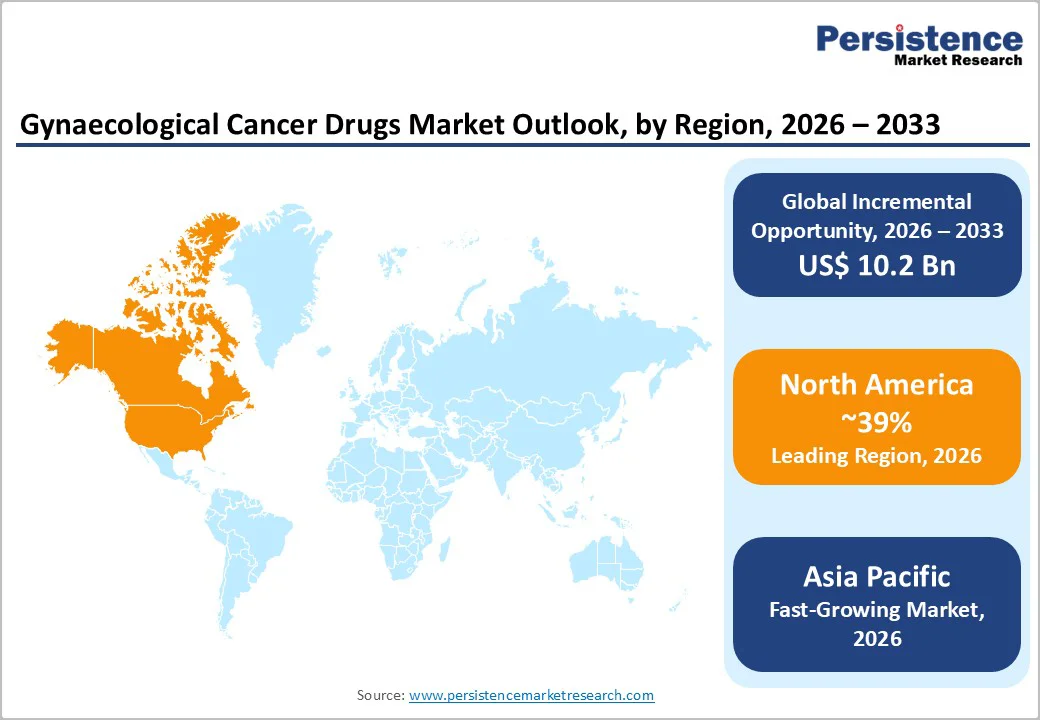

- Leading Region: North America, to command a 39% market share in 2026, driven by advanced oncology infrastructure, high prevalence of ovarian cancer, and strong R&D activities in the U.S.

- Fastest-growing Region: Asia Pacific, fueled by increasing healthcare access, rising awareness of women's cancers, and growing investments in pharma in China and India.

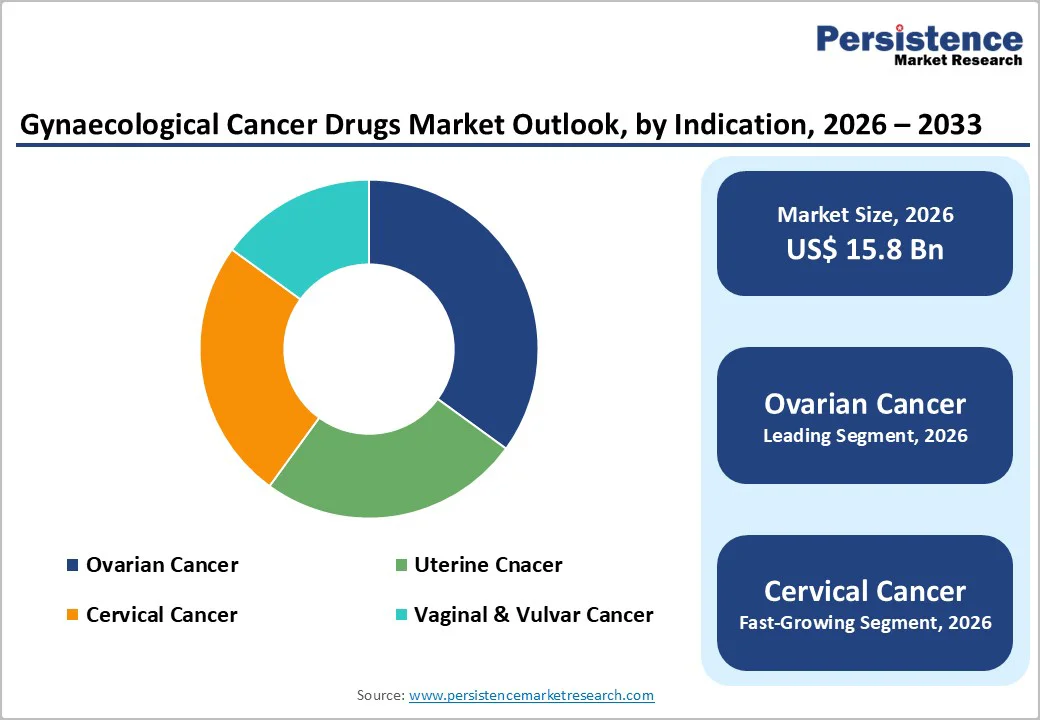

- Dominant Indication: Ovarian cancer, holding approximately 35% of the market share, is driven by complexity, late diagnosis, and treatment intensity.

- Leading Therapeutic Modality: Targeted therapy accounts for over 40% of market revenue, driven by its high precision in targeting specific cancer mutations and the improved availability of biomarker testing.

| Key Insights | Details |

|---|---|

|

Gynaecological Cancer Drugs Market Size (2026E) |

US$15.8 Bn |

|

Market Value Forecast (2033F) |

US$26.0 Bn |

|

Projected Growth (CAGR 2026 to 2033) |

7.4% |

|

Historical Market Growth (CAGR 2020 to 2025) |

7.2% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Rising Prevalence of Ovarian and Cervical Cancers and Demand for Targeted Therapies

The rising prevalence of ovarian and cervical cancers is significantly shaping the growth trajectory of the gynaecological cancer drugs market, driving stronger demand for advanced and targeted treatment approaches. Increasing lifestyle changes, delayed pregnancies, genetic predispositions, and limited early screening in many regions contribute to higher incidence rates, particularly in developing countries. Cervical cancer, strongly linked to persistent HPV infection, continues to rise in areas where vaccination and screening programs remain inadequate. According to the World Health Organization (WHO), in 2022, there were an estimated 660,000 new cases of cervical cancer globally, with around 350,000 deaths, highlighting its substantial and ongoing global burden. Ovarian cancer, often detected at later stages due to subtle symptoms, requires more specialized and effective treatment options, further increasing the need for innovative therapies.

As disease burden grows, the demand for targeted therapies is escalating rapidly. These treatments offer high precision by targeting specific genetic mutations or molecular pathways, resulting in fewer side effects and improved outcomes compared to traditional chemotherapy. PARP inhibitors, VEGF inhibitors, and other biomarker-driven therapies are becoming essential components of treatment regimens, especially for recurrent or resistant cases. Healthcare systems are increasingly adopting targeted approaches to enhance survival rates and personalize care.

High Development and Access Costs

The high costs associated with development and patient access to gynaecological cancer drugs pose a significant restraint on market growth. Developing advanced therapies such as immunotherapies, targeted drugs, and combination regimens requires extensive research, multi-phase clinical trials, sophisticated technology platforms, and regulatory compliance. These processes often span several years and involve high financial risk, as only a small fraction of candidate drugs successfully reach commercialization. As a result, companies price successful therapies at a premium to recover R&D investments, leading to exceptionally high treatment costs for patients and healthcare systems.

Access disparities further widen when newer therapies are introduced. In many developing regions, limited reimbursement frameworks, inadequate insurance coverage, and gaps in oncology infrastructure restrict availability. Even in developed markets, high out-of-pocket costs and formulary limitations can delay or prevent treatment initiation. Logistics such as cold-chain requirements, specialized administration, and trained personnel also add to the overall cost burden.

Advancements in Immunotherapy and Gene-Targeted Therapies

Advancements in immunotherapy and gene-targeted therapies are transforming the landscape of gynaecological cancer treatment by offering far more precise, durable, and personalized outcomes than traditional approaches. Immunotherapy has evolved from basic checkpoint inhibitors to advanced platforms, including personalized cancer vaccines, T-cell engineering, and combination regimens that strengthen immune activation against tumor cells. These innovations not only improve survival rates but also benefit patients with recurrent or resistant cancers, where conventional treatments often fail. According to a review covering gynecologic malignancies, immune-checkpoint inhibitors such as pembrolizumab have shown promise in cervical, endometrial, and ovarian cancers, with single-agent or combination immunotherapy currently under active clinical investigation.

Gene-targeted therapies are reshaping care by directly addressing the molecular drivers of cancer. Technologies such as PARP inhibitors, mutation-specific kinase inhibitors, and RNA-guided mechanisms enable clinicians to tailor treatment to genetic profiles, including BRCA, HRD, and PIK3CA mutations. This precision ensures stronger response rates with fewer side effects, making therapy more tolerable and effective. The integration of genomic testing into routine diagnostics further accelerates adoption, enabling early identification of actionable mutations.

Category-wise Analysis

Indication Insights

Ovarian cancer is anticipated to dominate the market, accounting for 35% of the market share in 2026. Its dominance is driven by complexity, late diagnosis, and treatment intensity. Ovarian cancer therapies, particularly PARP inhibitors, are widely adopted because they improve progression-free survival in patients with BRCA mutations. A well-known example is Lynparza (Olaparib) by AstraZeneca and Merck, a validated PARP inhibitor approved for frontline and maintenance treatment in ovarian cancer. Its strong clinical efficacy, expanding indications, and ongoing R&D advancements make ovarian cancer a primary focus area for pharmaceutical innovation and market investment.

Cervical cancer is likely to be the fastest-growing segment, driven by gaps in HPV vaccination coverage and rising adoption of advanced therapies in emerging markets. Its strong synergy between prevention and treatment makes it a key area for immunotherapy expansion. For example, there is Keytruda (pembrolizumab) by Merck, which received expanded approvals for persistent, recurrent, or metastatic cervical cancer, including use in combination with chemotherapy. This immunotherapy has shown significant survival benefits and is increasingly adopted in countries such as Brazil, Mexico, India, and Southeast Asia, aligning directly with the rising uptake of advanced treatments in these regions.

Therapeutic Modality Insights

Targeted therapy is anticipated to lead the market, holding over 40% of the market share in 2026, due to its high precision in targeting specific cancer mutations and the improved availability of biomarker testing. Its strong efficacy, fewer systemic side effects, and expanding use across ovarian, cervical, and endometrial cancers drive dominance. Rising demand for mutation-focused treatments and continuous drug approvals further strengthen its leadership. For example, Lynparza (Olaparib), a PARP inhibitor approved for BRCA-mutated ovarian, metastatic breast, and certain endometrial cancer settings. Its effectiveness in patients with defined genetic alterations and expanded indication approvals showcases how targeted therapies drive significant growth in gynecological cancer treatment.

Hormonal therapy is estimated to be the fastest-growing segment, due to its strong effectiveness in managing estrogen receptor (ER)-positive gynaecological cancers, especially rising uterine cancer cases. Its convenient oral administration, fewer side effects compared to chemotherapy, and suitability for long-term treatment are accelerating uptake. Increasing clinical adoption, expanding drug approvals, and patient preference for non-invasive therapies further fuel rapid growth. For example, Letrozole (Femara), a widely used aromatase inhibitor, is increasingly prescribed for ER-positive endometrial cancer, especially in recurrent and metastatic cases. Clinical studies have shown meaningful response rates in hormone-sensitive patients, supporting its expanding use in gynecological oncology and validating the strong momentum behind hormonal therapy.

Regional Insights

North America Gynaecological Cancer Drugs Market Trends

North America is projected to be the dominant region in the market, accounting for 39% of the share in 2026, supported by advanced healthcare infrastructure, strong R&D capabilities, and early adoption of innovative oncology therapies. The U.S. leads the regional market due to its high cancer awareness, well-developed diagnostic systems, and significant investment in clinical research for ovarian, cervical, and endometrial cancers. According to the CDC, every year in the U.S., about 13,000 new cases of cervical cancer are diagnosed, and around 4,000 women die from it, underscoring the strong need for improved early detection and advanced therapeutic options.

Large pharmaceutical companies actively conduct Phase II and Phase III trials across major cancer centers, accelerating the introduction of novel targeted and immunotherapy drugs. The rapid uptake of precision oncology, including biomarker-based treatments, PARP inhibitors, and checkpoint inhibitors, is driven by growing physician preference for personalized regimens. The availability of genetic testing and advanced diagnostics supports early identification of high-risk patients, improving treatment outcomes. North America is also fostering collaborations between academic institutions, biotech firms, and major pharmaceutical companies to advance drug discovery in rare gynaecological cancers.

Europe Gynaecological Cancer Drugs Market Trends

Strong healthcare systems, early adoption of advanced therapies, and increasing emphasis on precision oncology shape market growth in Europe. The region benefits from robust screening programs and early diagnosis initiatives, especially for cervical and endometrial cancers, which drive the need for effective and specialized treatments. Countries such as Germany, the U.K., France, and Italy remain central to innovation due to their mature clinical research infrastructure and strong support for oncology trials.

A major trend in Europe is the growing uptake of targeted therapies and immunotherapies, including PARP inhibitors, checkpoint inhibitors, and personalized treatment regimens. These advancements align with Europe’s focus on individualized care and biomarker-driven decision-making. The European Medicines Agency (EMA) continues to accelerate approvals for breakthrough therapies, enabling faster patient access to cutting-edge drugs. Collaboration is also increasing across academia, biotech companies, and large pharmaceutical firms to advance research in ovarian, cervical, and rare gynaecological cancers. Initiatives supporting the collection of real-world evidence and digital health integration are improving treatment outcomes.

Asia Pacific Gynaecological Cancer Drugs Market Trends

Asia Pacific is likely to be the fastest-growing market for gynaecological cancer drugs, driven by rising cancer incidence, expanding healthcare access, and increasing adoption of advanced treatment options. Countries such as China, India, Japan, and South Korea are witnessing a steady rise in ovarian, cervical, and endometrial cancer cases due to changing lifestyles, aging populations, and improved diagnostic capabilities. This growing patient base is prompting governments and healthcare providers to strengthen cancer care infrastructure, boosting demand for effective pharmaceutical therapies.

The rising shift toward targeted therapies and immuno-oncology. As awareness increases and treatment guidelines evolve, more patients are gaining access to biologics, including checkpoint inhibitors and precision-targeted regimens. Pharmaceutical companies are expanding clinical trials in the region to tap into large, diverse patient populations, accelerating drug development and regulatory approvals. Affordability remains important, which is why generic manufacturers, particularly in India and China, play a crucial role in improving treatment accessibility. Partnerships between global innovators and regional firms are expanding distribution networks and supporting technology transfer.

Competitive Landscape

The global gynecological cancer drugs market is highly competitive, dominated by major pharmaceutical companies such as F. Hoffmann-La Roche and Bristol-Myers Squibb in North America and Europe, which leverage strong oncology pipelines, clinical trial programs, and immunotherapy research. In the Asia Pacific, companies such as TEVA are gaining ground by offering affordable therapies and expanding access in emerging markets.

Growth is fueled by rising cancer incidence, improved healthcare infrastructure, and increased adoption of targeted and personalized treatments. Advances in immuno-oncology, including checkpoint inhibitors, along with strategic partnerships and acquisitions, are accelerating the development of novel therapies, reshaping treatment strategies worldwide.

Key Industry Developments

- In October 2025, Merck, known as MSD outside the U.S. and Canada, announced that over 100 abstracts covering more than 20 cancer types and various treatment settings from its diverse portfolio and pipeline will be presented at the European Society for Medical Oncology (ESMO) Congress 2025 in Berlin, Germany, from October 17–21. These findings highlight Merck’s dedication to advancing research across multiple tumor types to improve patient outcomes at all stages of cancer.

- In August 2025, GSK India re-entered the oncology market by launching two precision therapies, Jemperli (dostarlimab) and Zejula (niraparib), targeting gynecological cancers, as part of its strategy to expand its specialty medicines portfolio. This move marks GSK’s return to cancer care nearly a decade after selling its oncology portfolio to Novartis.

Companies Covered in Gynaecological Cancer Drugs Market

- F. Hoffmann-La Roche Ltd

- Bristol Myers Squibb

- Teva Pharmaceuticals

- AstraZeneca plc

- Novartis AG

- Eli Lilly and Company

- Pfizer Inc.

- Merck & Co., Inc.

- GlaxoSmithKline

- Apotex Inc.

Frequently Asked Questions

The global gynaecological cancer drugs market is projected to reach US$15.8 billion in 2026.

The rising prevalence of ovarian and cervical cancers and demand for targeted therapies are the key drivers.

The gynaecological cancer drugs market is poised to witness a CAGR of 7.4% from 2026 to 2033.

Advancements in immunotherapy and gene-targeted therapies are the key opportunities.

F. Hoffmann-La Roche Ltd, Bristol Myers Squibb, Teva Pharmaceuticals, AstraZeneca plc, and Novartis AG are the key players.