- Agrochemicals

- Glyphosate Market

Glyphosate Market Size, Share, and Growth Forecast 2026 - 2033

Glyphosate Market by Product Type (Liquid, Granules), Application (Cereals & Grains, Fruits & Vegetables, Pulses, Roots & Tubers, Others), Crop Type (Conventional Crop, GM Crop), by Regional Analysis, 2026 - 2033

Glyphosate Market Size and Trend Analysis

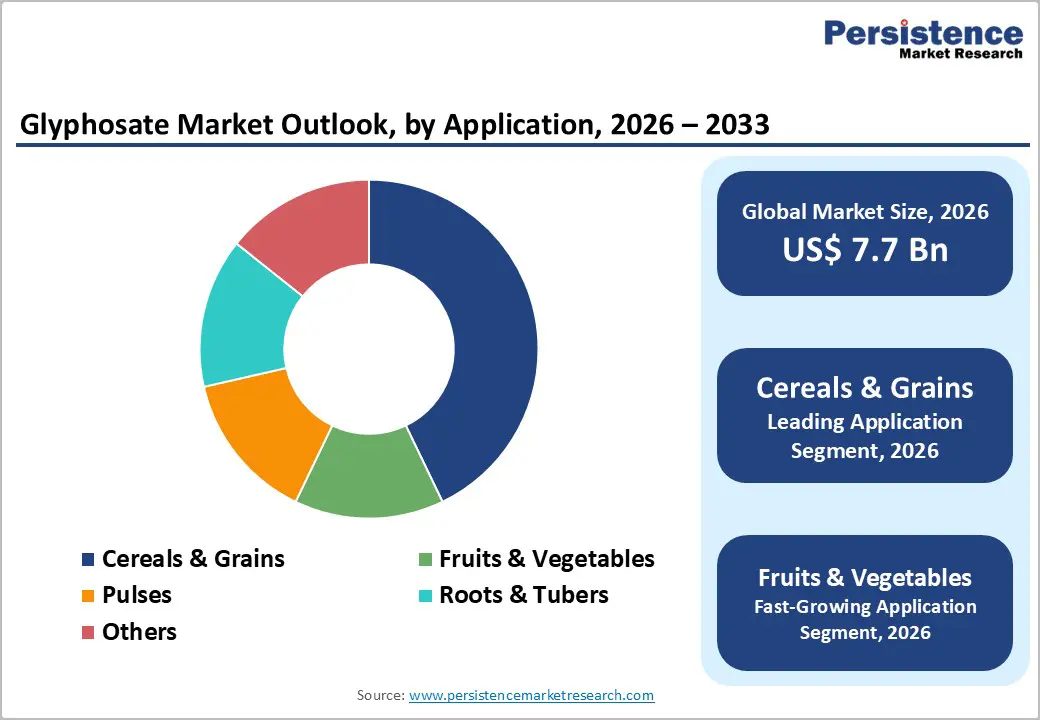

The global glyphosate market size is expected to be valued at US$ 7.7 billion in 2026 and projected to reach US$ 10.4 billion by 2033, growing at a CAGR of 4.4% between 2026 and 2033.

This steady market expansion is primarily driven by increasing global food demand necessitating enhanced agricultural productivity, widespread adoption of genetically modified herbicide-tolerant crops enabling efficient weed management, and glyphosate's cost-effectiveness compared to alternative herbicides making it the preferred choice for farmers worldwide.

Key Industry Highlights

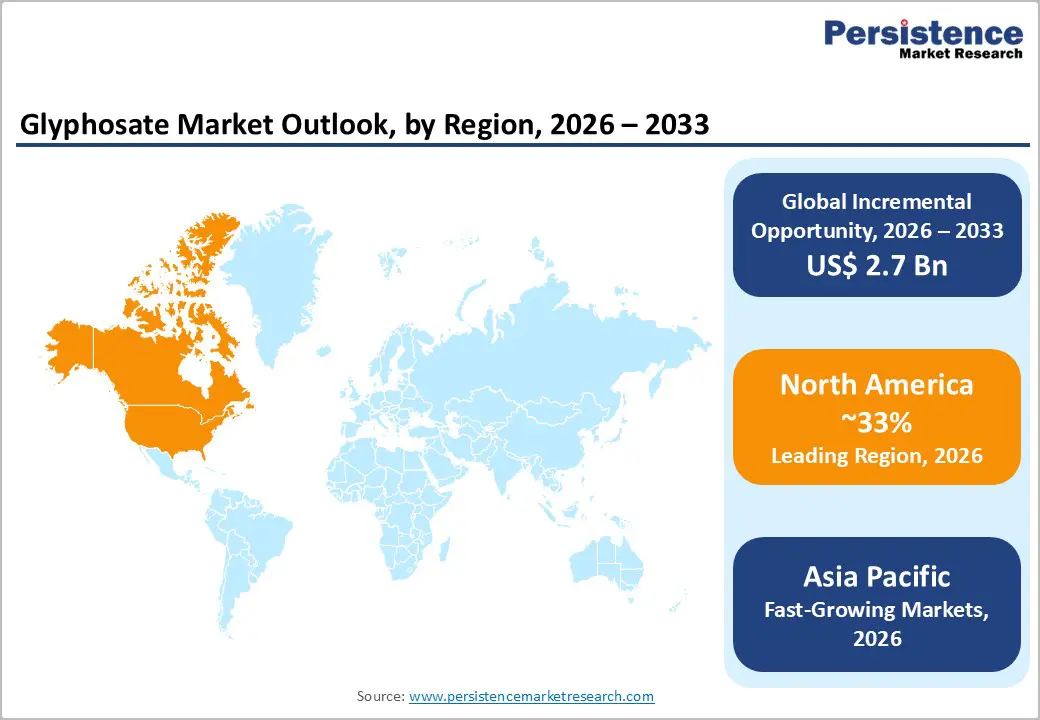

- North America maintains regional market leadership with approximately 33% market share in 2025, driven by extensive cultivation of genetically modified glyphosate-tolerant crops across over 200 million acres of corn, soybeans, and cotton, established herbicide utilization patterns, EPA regulatory approvals, and mechanized large-scale agricultural systems.

- Asia Pacific emerges as the fastest-growing regional market with projected CAGR of 5.2% during 2026 - 2033, propelled by China's dominant manufacturing and agricultural consumption, India's expanding herbicide adoption driven by rising labor costs, agricultural intensification across Southeast Asia, and mechanization trends replacing manual weeding.

- Liquid formulations command dominant market position with approximately 74% market share in 2025, reflecting farmer preference for ease of handling, application flexibility with modern spray equipment, tank-mix compatibility, established distribution infrastructure, and operational advantages including accurate dosing and reduced dust exposure.

- GM Crop applications represent the fastest-growing segment with anticipated CAGR of 5.1% through 2033, driven by continued expansion of herbicide-tolerant crop cultivation in major markets, new generation traits incorporating multiple herbicide resistances, farmer economic benefits averaging US$ 12-15 per acre, and facilitation of conservation tillage practices.

- Significant market opportunities emerge from expansion in developing agricultural economies across Asia, Africa, and Latin America where herbicide adoption remains low but growing, development of integrated weed management systems addressing resistance challenges while maintaining glyphosate as a foundation component, and formulation innovations improving performance and sustainability profiles.

| Key Insights | Details |

|---|---|

| Glyphosate Market Size (2026E) | US$ 7.7 billion |

| Market Value Forecast (2033F) | US$ 10.4 billion |

| Projected Growth CAGR (2026 - 2033) | 4.4% |

| Historical Market Growth (2020 - 2025) | 3.6% |

Market Dynamics

Drivers - Increasing Global Food Demand and Agricultural Intensification

The relentless growth of global population and rising food consumption patterns are fundamentally driving agricultural intensification efforts that depend heavily on effective weed management solutions including glyphosate herbicides. The United Nations Food and Agriculture Organization (FAO) projects that global agricultural production must increase by 70% by 2050 to feed an estimated world population of 9.7 billion people, necessitating maximized crop yields and minimized production losses from weed competition. The U.S. Department of Agriculture (USDA) reports that uncontrolled weeds can reduce crop yields by 30-70% depending on weed pressure, crop type, and environmental conditions, highlighting the critical importance of herbicide applications in maintaining agricultural productivity.

Glyphosate's broad-spectrum activity against annual and perennial weeds, systemic translocation to root systems ensuring complete weed elimination, and post-emergence application flexibility make it indispensable in modern crop production systems. The International Grains Council documents that global grain production reached approximately 2.3 billion tonnes in 2024, with major producing regions including the United States, Brazil, Argentina, and China relying extensively on glyphosate for weed control in soybeans, corn, wheat, and other cereals. The herbicide's effectiveness in controlling problematic weed species that compete with crops for nutrients, water, and sunlight directly contributes to yield protection and food security objectives worldwide.

Widespread Adoption of Genetically Modified Herbicide-Tolerant Crops

The commercialization and rapid global adoption of genetically modified crops engineered for glyphosate tolerance have created substantial structural demand for glyphosate herbicides in major agricultural markets. The International Service for the Acquisition of Agri-biotech Applications (ISAAA) reports that biotech crops were planted on 190.4 million hectares globally in 2019, with herbicide-tolerant varieties representing a significant portion of this acreage. The USDA Economic Research Service documents that in the United States, over 90% of soybeans, 89% of cotton, and 87% of corn planted in 2024 were genetically engineered varieties, with herbicide tolerance being the predominant trait. Glyphosate-tolerant crop systems enable farmers to apply glyphosate over-the-top of growing crops for effective weed control without crop injury, simplifying weed management programs and reducing reliance on multiple herbicide applications or mechanical cultivation.

The Brazilian National Biosafety Technical Commission has approved numerous glyphosate-tolerant crop varieties, supporting Brazil's position as the world's second-largest adopter of biotech crops with over 50 million hectares planted annually. Argentina, another major agricultural exporter, cultivates glyphosate-tolerant soybeans on virtually 100% of its soybean acreage according to government statistics. The agronomic and economic benefits of these cropping systems, including improved weed control efficacy, reduced labor requirements, fuel savings from fewer field passes, and facilitation of conservation tillage practices, ensure sustained glyphosate demand in regions where genetically modified crops are approved for cultivation.

Restraints- Regulatory Restrictions and Glyphosate Bans in Key Markets

Growing regulatory scrutiny and outright bans on glyphosate use in several countries represent significant market constraints, driven by health concerns, environmental considerations, and evolving political landscapes regarding agrochemical use. The European Chemicals Agency (ECHA) classification controversies and the International Agency for Research on Cancer (IARC) classification of glyphosate as "probably carcinogenic to humans" in 2015 have triggered regulatory reviews and restrictions across multiple jurisdictions.

Several European countries including Austria, Germany, and France have implemented or proposed phase-out plans for glyphosate despite the European Commission's approval for continued use. The European Union renewed glyphosate approval until December 2023 but with heightened conditions and ongoing political pressure for restrictions. Various municipalities and regions globally have enacted local bans on glyphosate use in public spaces, parks, and schools. The regulatory uncertainty creates market instability, limits long-term planning for manufacturers and distributors, and drives research into alternative herbicides, potentially constraining future market growth in affected regions.

Litigation Risks and Public Perception Challenges

Extensive litigation alleging health damages from glyphosate exposure has created substantial financial liabilities for manufacturers and negatively influenced public perception, potentially constraining market expansion despite scientific disagreements on causation. Bayer AG, which acquired Monsanto and its glyphosate products in 2018, has faced over 100,000 lawsuits in the United States alleging that glyphosate exposure caused cancer, primarily non-Hodgkin's lymphoma. The company has agreed to settlements exceeding US$ 10 billion to resolve existing and potential future claims, while maintaining that glyphosate is safe when used as directed. These legal challenges have influenced public opinion, with consumer advocacy groups calling for restrictions or bans on glyphosate products.

Retailers in some markets have voluntarily removed glyphosate products from shelves in response to consumer concerns. The negative publicity surrounding litigation, even in cases where scientific regulatory bodies have concluded glyphosate does not pose unreasonable risks when used according to label directions, creates market headwinds by influencing farmer purchasing decisions, encouraging exploration of alternative weed control methods, and supporting political movements advocating for glyphosate restrictions.

Opportunities - Expansion in Emerging Agricultural Markets and Developing Economies

Rapid agricultural development in emerging economies across Asia, Africa, and Latin America presents substantial growth opportunities for glyphosate suppliers as farmers in these regions adopt modern farming practices and seek cost-effective weed management solutions. The Food and Agriculture Organization projects that developing countries will account for the majority of future agricultural production growth to meet rising domestic food demand and export opportunities. India's agricultural sector, supporting over 263 million farmers cultivating 157 million hectares, demonstrates increasing herbicide adoption as labor costs rise and mechanization advances, with the Ministry of Agriculture and Farmers Welfare promoting integrated weed management practices. Southeast Asian countries including Vietnam, Thailand, Indonesia, and Philippines are experiencing agricultural intensification in rice, palm oil, rubber, and other crops where glyphosate provides effective weed control.

Sub-Saharan Africa, with vast agricultural potential and growing populations, represents an emerging market where glyphosate adoption remains relatively low but is expanding as farmers gain access to improved inputs and extension services. The African Development Bank supports agricultural modernization programs that include improved crop protection practices. Glyphosate's affordability compared to newer herbicide chemistries, proven efficacy across diverse crops and climatic conditions, and compatibility with conservation agriculture practices promoted by international development organizations position it favorably for market expansion in developing agricultural economies seeking to enhance productivity and food security.

Development of Glyphosate-Based Integrated Weed Management Systems

The evolution of herbicide resistance in weed populations is creating opportunities for manufacturers to develop and market glyphosate-based integrated weed management systems combining multiple herbicide modes of action, application timing strategies, and agronomic practices. The Weed Science Society of America documents that over 250 weed species globally have evolved resistance to herbicides, with glyphosate resistance documented in 48 species across numerous countries. This resistance challenge is driving demand for tank-mix partners, pre-mixed herbicide formulations, and sequential application programs that incorporate glyphosate with complementary chemistries including dicamba, 2,4-D, and residual herbicides.

The U.S. Environmental Protection Agency has registered new herbicide-tolerant crop traits and corresponding herbicide products designed to address resistance issues while maintaining glyphosate as a foundation component. Research by university weed scientists and industry experts emphasizes that glyphosate remains highly effective against susceptible weed populations and delivers value as part of diversified programs. Agricultural extension services promoted by the USDA and land grant universities advocate for integrated weed management combining herbicide diversity, crop rotation, tillage when appropriate, cover crops, and other cultural practices. Manufacturers investing in farmer education, combination products, and stewardship programs that preserve glyphosate efficacy through responsible use can capture market share while supporting sustainable weed management systems that extend the useful life of glyphosate and other herbicide technologies.

Category-wise Analysis

Product Type Insights

The liquid formulation segment dominates the glyphosate market with around 74% share in 2025, driven by farmers’ preference for ease of handling and application flexibility. Liquid glyphosate products, such as isopropylamine, ammonium, or potassium salts, allow precise dosing, reduced dust exposure, and uniform tank dispersion. Modern spraying equipment, including boom sprayers, aerial systems, and precision agriculture technologies, is optimized for liquid applications, enabling GPS-guided section control and automated boom adjustments for consistent coverage. Liquid formulations also support tank-mixing with herbicides, insecticides, or fertilizers, reducing labor and field passes. Innovations such as high-concentration solutions, improved surfactant systems, and proprietary adjuvants further enhance performance, sustain adoption, and strengthen the segment’s market leadership globally.

Application Insights

Cereals and grains account for the leading application segment with approximately 38% share in 2025, reflecting their extensive global acreage and critical role in food security. Wheat, corn, rice, and barley occupy vast areas requiring effective weed management to protect yields. Glyphosate is applied in multiple stages, preplant, in-crop, and post-harvest, to control weeds and optimize crop establishment, particularly in glyphosate-tolerant varieties. Its use facilitates pre-harvest desiccation in wheat and weed management in rice bunds and irrigation channels. The high economic importance of cereals, combined with favorable cost-benefit ratios and essential yield protection, ensures sustained glyphosate demand in these staple crops across major agricultural regions worldwide.

Crop Type Insights

Genetically modified (GM) crops hold the leading position with roughly 62% share in 2025 and are projected to grow at a CAGR of 5.1% through 2033. Herbicide-tolerant GM varieties, pioneered by Roundup Ready technology, allow post-emergence glyphosate applications without crop injury, transforming weed management practices. Adoption is concentrated in the United States, Brazil, Argentina, Canada, and India, accounting for over 90% of global biotech crop area. Farmers benefit from lower herbicide costs, labor savings, yield protection, and the ability to implement conservation tillage. Emerging multi-trait crops with combined glyphosate and other herbicide tolerances address resistance challenges, supporting ongoing growth of GM crop adoption worldwide.

Regional Insights

North America Glyphosate Market Trends and Insights

North America maintains the leading regional position with approximately 33% market share in 2025, underpinned by extensive cultivation of genetically modified glyphosate-tolerant crops, large-scale mechanized agriculture, and established herbicide utilization patterns. The United States dominates regional consumption, with the U.S. Geological Survey estimating that approximately 125 million kilograms of glyphosate active ingredient are applied annually across agricultural and non-agricultural uses, making it the most widely used herbicide in American agriculture. Corn, soybeans, and cotton production, which collectively occupied over 200 million acres in 2024 according to USDA statistics, drive substantial glyphosate demand through both conventional and genetically modified crop systems.

The regulatory environment significantly influences market dynamics, with the U.S. Environmental Protection Agency maintaining glyphosate registrations following comprehensive scientific reviews concluding the product does not pose unreasonable risks to human health or the environment when used according to label directions. However, ongoing litigation and state-level regulatory actions create market uncertainty. Canada, the second major market in the region, cultivates extensive canola, wheat, and pulse crop acreage with significant glyphosate utilization, with Health Canada's Pest Management Regulatory Agency maintaining product registrations. The emergence of herbicide-resistant weed populations in North America is driving adoption of tank-mix partners and integrated weed management strategies that maintain glyphosate as a core component while incorporating additional modes of action to manage resistance.

Europe Glyphosate Market Trends and Insights

Europe exhibits complex market dynamics characterized by stringent regulatory frameworks, active public debate regarding glyphosate safety, and divergent national policies despite region-wide approval processes. The European Commission renewed glyphosate approval in 2017 for five years following extensive scientific assessment by the European Food Safety Authority (EFSA) and European Chemicals Agency, with another renewal process completed in 2023 extending approval. However, individual member states retain authority to restrict or prohibit glyphosate use within their territories, creating a fragmented regulatory landscape. Germany, historically a significant glyphosate market, has implemented restrictions limiting use to cases where alternative control methods are unavailable or impractical.

France pursued glyphosate phase-out objectives though complete elimination by initial target dates proved challenging due to limited alternatives for certain applications. The United Kingdom, following Brexit, maintains independent regulatory authority with the Health and Safety Executive conducting its own glyphosate assessments while reaching similar safety conclusions as EU authorities. Agricultural use in Europe focuses on cereals including wheat and barley, pre-planting applications in various crops, and non-crop uses including railways and industrial sites. The European Crop Protection Association advocates for science-based regulation while acknowledging public concerns. The regulatory uncertainty and market restrictions are constraining European glyphosate consumption while stimulating research into alternative weed control technologies including non-chemical methods, mechanical cultivation, and alternative herbicide chemistries.

Asia Pacific Glyphosate Market Trends and Insights

Asia Pacific emerges as the fastest-growing regional market with an anticipated CAGR of 5.2% during 2026 - 2033, propelled by agricultural intensification, expanding genetically modified crop cultivation in select countries, and growing herbicide adoption replacing labor-intensive manual weeding. China dominates regional production and consumption, serving as both the world's largest glyphosate manufacturer and a major agricultural market with extensive applications in rice, corn, soybeans, and orchards. The Ministry of Agriculture and Rural Affairs regulates pesticide use with increasing emphasis on food safety and environmental protection, implementing policies to reduce chemical pesticide use while promoting integrated pest management approaches.

India represents a high-growth opportunity market driven by rising agricultural labor costs, mechanization trends, and government initiatives promoting agricultural productivity. The Central Insecticides Board and Registration Committee regulates glyphosate registration and use, with applications expanding in tea plantations, non-agricultural areas, and increasingly in field crops as farmers seek alternatives to manual weeding. Australia, though smaller in population, cultivates vast acreages of wheat, barley, and canola with extensive glyphosate utilization, with the Australian Pesticides and Veterinary Medicines Authority maintaining product approvals. Southeast Asian countries including Vietnam, Thailand, and Indonesia demonstrate growing herbicide adoption in rice, palm oil, rubber, and other plantation crops as economic development increases labor costs and farmers seek efficiency improvements. The region's diverse agricultural systems, varying regulatory frameworks, and different stages of agricultural development create complex market dynamics with substantial long-term growth potential.

Competitive Landscape

The global glyphosate market is moderately consolidated, with a few key players commanding significant market share through extensive product portfolios, well-established distribution networks, and strong brand recognition. Market competition is shaped by strategic initiatives such as product differentiation, formulation innovation, and geographic expansion. Given glyphosate’s off-patent status, cost leadership and manufacturing efficiency are critical, particularly with low-cost producers supplying global demand.

Companies increasingly focus on proprietary formulations and branded products to maintain premium positioning and deliver value-added services, including agronomic guidance and optimized application support. Innovation also targets combination products to manage herbicide resistance and improve operational efficiency for end-users. Sustainability and stewardship programs form another pillar of strategy, ensuring responsible use, regulatory compliance, and long-term market acceptance. Additionally, diversification into alternative herbicide chemistries and biological solutions is gaining traction, enabling companies to adapt to evolving environmental regulations, customer preferences, and competitive pressures while sustaining growth in a mature market landscape.

Key Developments:

- January 2023 - Waters Corporation launched Glyphosate-V, the world’s first lateral-flow quantitative test strip for on-site detection of glyphosate in grains and water, providing rapid results in under 15 minutes to support quality and compliance decisions.

- May 2023 - Ancient Organics Bioscience announced the commercial launch of its PaleoPower™ product, a microbial soil probiotic designed to organically break down glyphosate contamination and restore soil microbiome health.

- January 2026 - Two Brothers Organic Farms expanded glyphosate-free certification beyond its ghee product to include everyday staples like atta, jaggery, and amlaprash, verified by a third-party residue testing agency.

Companies Covered in Glyphosate Market

- Nufarm

- BASF SE

- UPL Ltd

- HELM AG

- Bayer AG

- Rolfes Agri

- Wynca Group

- ADAMA Ltd

- Albaugh LLC

- GOOD HARVEST

- ENVIRO Bio-Chem

- Drexel Chemical

- ECOGAURD

- Bharat Group

- Crystal Crop Protection Limited

- Syngenta Group

- FMC Corporation

- Corteva Agriscience

- Zhejiang Xinan Chemical Industrial Group

- Hubei Sanonda

Frequently Asked Questions

The global glyphosate market is expected to reach US$ 7.7 billion in 2026.

Demand is driven by rising food needs, adoption of herbicide-tolerant crops, broad-spectrum efficacy, and cost-effectiveness.

North America leads with around 33% market share in 2025.

Opportunities lie in developing markets, integrated weed management, and formulation innovations.

Leading manufacturers include Bayer AG, BASF SE, UPL Ltd, ADAMA Ltd, Nufarm, Syngenta Group, Corteva Agriscience, FMC Corporation, Wynca Group, etc.