- Food Ingredients & Additives

- Fresh Yeast Market

Fresh Yeast Market Size, Share, Growth, and Regional Forecast, 2026 to 2033

Fresh Yeast Market by Form (Block, Crumbled, Liquid), End-user (Food & Beverages, Animal Feed / Nutrition, Biofuels, Pharmaceuticals, Others), Distribution Channel (B2B, B2C), and Regional Analysis from 2026 to 2033

Fresh Yeast Market Share and Trends Analysis

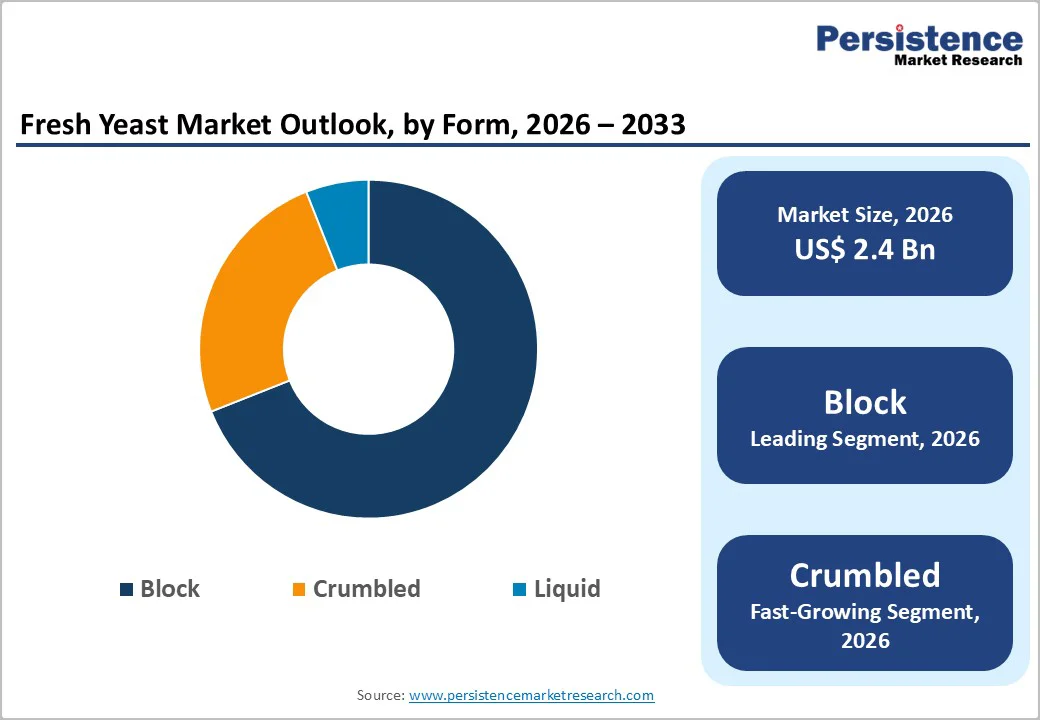

The global fresh yeast market size is estimated to grow from US$ 2.4 billion in 2026 to US$ 3.9 billion by 2033. The market is projected to record a CAGR of 7.3% during the forecast period from 2026 to 2033.

The global market is moving into a phase of scale-driven innovation, regional diversification, and technology-led upgrades, creating a competitive landscape that rewards capability, consistency, and strategic expansion.

Key Industry Highlights:

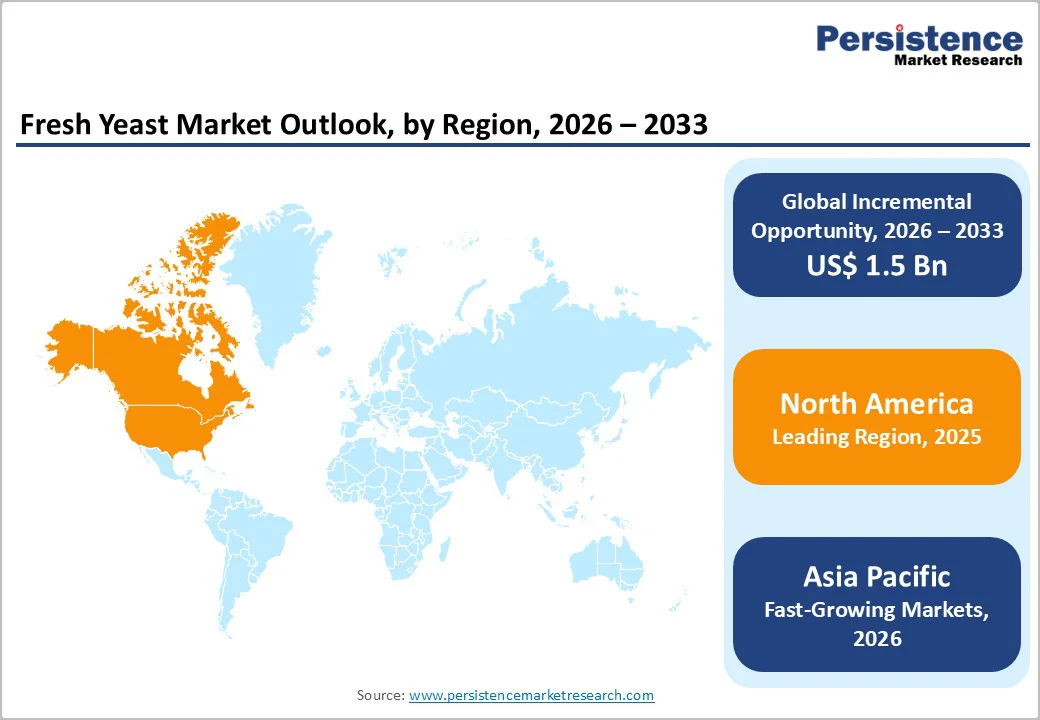

- Leading Region: North America, strengthened by its 39% share, supported by the rise of artisanal baking, clean-label fermentation preferences, and strong adoption of premium fresh yeast strains across commercial bakeries.

- Fastest-Growing Region: Asia Pacific, propelled by the rapid expansion of bakery chains, café culture growth, and the increasing localization of yeast production to meet daily supply needs in urban markets.

- Fastest-Growing Form Segment: Crumbled yeast, gaining momentum due to its efficient dispersion, shorter mixing times, and suitability for automated, high-output bakery environments.

- Market Driver: Growth in craft and specialty bakery formats is pushing demand for high-performance yeast strains that deliver superior fermentation control, richer flavor development, and enhanced dough tolerance.

- Opportunities: Expanding bakery chains in the Asia Pacific are opening avenues for new plants, capacity expansion, localized strain development, and closer technical partnerships with high-volume bakery operators.

- Key Developments: In November 2025, Angel Yeast began trial production at its new specialty yeast facility in Baiyang Biotechnology Park, scaling toward an 8,500-ton annual capacity. In July 2025, Lallemand Bio-Ingredients advanced its fermentation capabilities through the acquisition of Solyve, reinforcing its position in next-generation microbial ingredient solutions.

| Key Insights | Insights |

|---|---|

| Global Fresh Yeast Market Size (2026E) | US$ 2.4 Bn |

| Market Value Forecast (2033F) | US$ 3.9 Bn |

| Projected Growth (CAGR 2026 to 2033) | 7.3% |

| Historical Market Growth (CAGR 2020 to 2025) | 6.2% |

Market Dynamics

Driver - Growth in Craft and Specialty Bakery Segments Fuels Adoption of Premium, High-Performance Yeast Strains

A noticeable push from the craft and specialty bakery world is rapidly reshaping momentum in the global fresh yeast market. Artisan bakers are demanding yeast strains that deliver superior fermentation control, enhanced aroma development, and consistent oven spring to differentiate their breads, pastries, and regional specialties.

As consumer preferences tilt toward artisanal textures, longer fermentation profiles, and richer flavor notes, bakeries are shifting to high-performance fresh yeast that supports this premium positioning. Small and mid-scale bakeries are experimenting with slow-rise doughs, stone-baked formats, and clean-label recipes, raising the requirement for yeast with strong tolerance and stability.

This renewed focus on craftsmanship is directly boosting the adoption of advanced yeast strains designed for quality-driven, specialty bakery applications.

Restraints - Temperature-sensitive Handling Increases Logistics Complexity

A critical challenge shaping the fresh yeast landscape is its sensitivity to temperature fluctuations across transport and storage. Fresh yeast requires tightly controlled cold-chain conditions to maintain viability, fermentation strength, and shelf stability, making logistics far more demanding compared to dry or instant alternatives.

Any deviation during warehousing, transport routes, or last-mile delivery can reduce activity levels, forcing producers and distributors to invest in robust refrigeration infrastructure and continuous monitoring systems. This adds operational cost, complicates long-distance shipments, and limits penetration in warm-climate regions where cold-chain reliability remains inconsistent.

For emerging markets and smaller bakeries, these handling constraints create barriers to adoption, slowing broader market expansion despite rising demand.

Opportunity - Expanding Bakery Chains in the Asia Pacific Present Strong Opportunities For Capacity Expansion

Rapid expansion of bakery chains across the Asia Pacific is creating a compelling opportunity for fresh yeast producers seeking scale, localization, and long-term demand stability. Rising urbanization and café culture growth in countries such as China, India, Indonesia, and Vietnam are driving a surge in demand for consistent, high-performing yeast suited for daily production cycles.

Large-format bakeries and QSR-linked bakery concepts increasingly prefer local supply to secure timely deliveries and reduce dependence on imports. This shift encourages yeast manufacturers to establish regional plants, upgrade fermentation capacity, and tailor strains to local flour types and climatic conditions.

As bakery menus diversify toward artisanal breads and premium pastries, suppliers positioned within Asian markets, they capture expanding volumes with improved responsiveness and cost efficiency.

Category-wise Analysis

By Form Insights

Yeast blocks hold approx. 64% market share as of 2024, underscoring the format’s strong alignment with commercial and industrial baking requirements. Bakers favor block yeast for its high cell density, reliable fermentation strength, and ability to deliver stable performance in large-scale dough processing. Its compact structure supports efficient hydration, consistent rising behavior, and predictable tolerance across diverse bakery applications.

Granular and liquid formats continue finding niche adoption, yet block yeast remains the trusted choice for high-volume bread, rolls, and pastry manufacturing. Dessert-focused bakeries often explore alternative forms for specialized textures, but the dominance of blocks persists due to cost efficiency, established handling familiarity, and compatibility with automated mixing systems. As bakery production modernizes, block yeast retains its central role.

Crumbled yeast is expected to show promising growth during the forecast period

Crumbled yeast is projected to grow at a CAGR of 8.3% during the forecast period, reflecting a decisive shift toward formats that support faster blending, higher fermentation efficiency, and streamlined industrial processing. Its loose, granular structure enables more consistent dispersion in dough systems, making it attractive for high-output bakeries aiming to cut mixing times and improve batch uniformity.

Demand is strengthening in regions where automated dough handling and continuous baking lines are expanding, as crumbled yeast aligns well with precision-driven production. Interest in liquid fresh yeast remains steady, particularly among large industrial manufacturers seeking pumpable, fully automated dosing solutions.

As bakeries scale and optimize operations, crumbled yeast emerges as a practical, performance-oriented choice for modern production environments.

Region-wise Insights

North America Fresh Yeast Market Trends

North America holds approximately 39% market share in the global fresh yeast market, and the region’s trajectory is being reshaped by a resurgence in artisanal baking and clean-label fermentation trends. In the US, bakeries and foodservice operators are increasingly adopting fresh yeast varieties known for consistent rise, improved crumb structure, and enriched flavor performance.

Canada is witnessing greater use of premium strains in specialty bread formats, fueled by rising consumer interest in locally crafted baked goods. Leading brands such as Lesaffre, Lallemand, Red Star, and Fleischmann’s are strengthening their foothold through product upgrades, improved fermentation technologies, and closer partnerships with commercial bakers.

Across the region, innovation in freshness, stability, and baking efficiency continues to influence purchasing decisions.

Europe Fresh Yeast Market Trends

Europe remains a highly mature and innovation-driven market, characterized by strong bakery traditions and deep regional specialization. Germany is witnessing heightened interest in long-fermentation breads and rye-based formulations, boosting demand for robust, performance-stable fresh yeast. The UK is shifting toward artisanal buns, pastries, and premium brioche, prompting bakers to seek yeast variants that offer improved dough tolerance.

Spain continues to expand fresh bakery offerings in hypermarkets, supporting consistent demand for versatile yeast blocks. Italy’s focus on pizza, ciabatta, and regional specialty breads is encouraging mills and bakeries to adopt yeast optimized for high hydration and extended proofing. Across Europe, clean-label fermentation inputs, cold-chain efficiency, and localized strain development remain core trends shaping purchasing behavior.

Competitive Landscape

The fresh yeast market presents a moderately consolidated structure where global leaders and agile regional producers compete through scale, technical expertise, and rapid product development. Major companies are strengthening processing technologies to improve fermentation efficiency, enhance cell vitality, and deliver strains tailored for artisanal and industrial baking.

Startups are entering with specialized cultures, clean-label positioning, and innovative bioprocessing methods shaped around sustainability. Certifications related to food safety and organic compliance are becoming essential tools for building trust, especially in premium bakery applications.

Strategic collaborations with milling companies, foodservice chains, and ingredient innovators are increasing, while investments in capacity expansion, automation upgrades, and selective mergers and acquisitions signal a strong push toward long-term industry consolidation.

Key Industry Developments:

- In November 2025, Angel Yeast initiated trial production at its new specialty yeast facility in Baiyang Biotechnology Park, marking a major scale-up in its advanced fermentation capabilities. The plant, which began material feeding on August 31, is set to reach an annual output of 8,500 tons once fully operational.

- In July 2025, Lallemand Bio-Ingredients strengthened its position in microbial solutions with the acquisition of Solyve, a subsidiary of the InVivo group. The move expands its capabilities in delivering advanced fermentation-driven ingredients for the global food and beverage sector.

- In February 2025, Lesaffre inaugurated its new yeast production facility in Malang, East Java, built across 9.8 hectares to strengthen its presence in Asia Pacific. The plant marks a major step in bringing advanced yeast solutions closer to regional customers.

Companies Covered in Fresh Yeast Market

- Lesaffre

- Lallemand Inc.

- Angel Yeast Co., Ltd.

- Novonesis Group

- Associated British Foods

- DSM-Firmenich

- Kerry Group plc

- Alltech, Inc.

- Pakmaya

- Oriental Yeast Co., ltd

- Laffort SA

- Kothari Fermentation and Biochem Ltd

- Others

Frequently Asked Questions

The global fresh yeast market is projected to be valued at US$ 2.4 Bn in 2026.

Growth in craft and specialty bakery segments is driving the global fresh yeast market.

The global fresh yeast market is poised to witness a CAGR of 7.3% between 2026 and 2033.

Expanding bakery chains across the Asia Pacific are opening significant avenues for scaling production capacity.

Major players in the global Fresh Yeast market include Lesaffre, Lallemand Inc., Angel Yeast Co., Ltd., Novonesis Group, Associated British Foods, Kerry Group plc, Alltech, Inc., and others.