- Medical Devices

- Fluoroscopy and C - Arms Market

Fluoroscopy and C - Arms Market Size, Share, Growth, and Regional Forecast, 2026 - 2033

Fluoroscopy and C - Arms Market by Product (Mobile C-arm, Mini C-arm, Fixed C-arm), Application (Image-guided biopsy, Discography, Angiography, Others), End-user (Hospitals, Diagnostic centers, Specialty clinics, Others), and Regional Analysis from 2026 - 2033

Fluoroscopy and C-arms Market Share and Trends Analysis

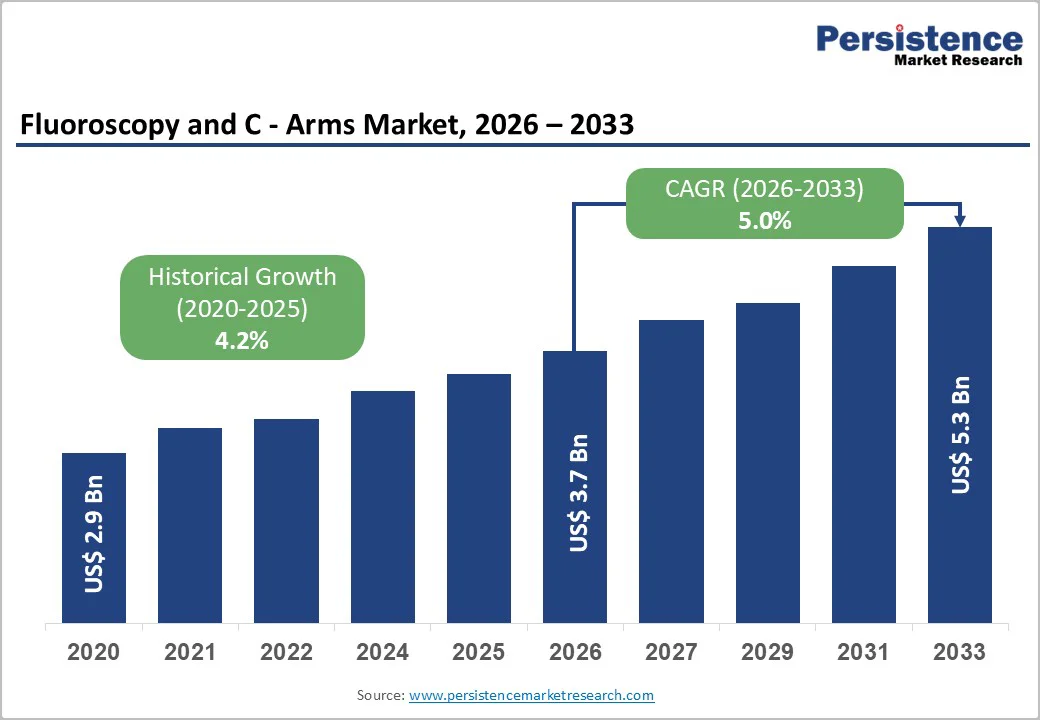

The global fluoroscopy and C - Arms market size is estimated to grow from US$ 3.7 billion in 2026 to US$ 5.3 billion by 2033, growing at a CAGR of 5.0% during the forecast period from 2026 to 2033.

The global market is experiencing a steady expansion, driven by the increase in surgical volumes, growing demand for image-guided procedures, and the shift toward minimally invasive treatments. North America leads due to strong hospital infrastructure and rapid technology adoption, while Asia Pacific is the fastest-growing region, supported by expanding healthcare access, rising investments, and increasing adoption of affordable digital C-arm systems.

Key Industry Highlights:

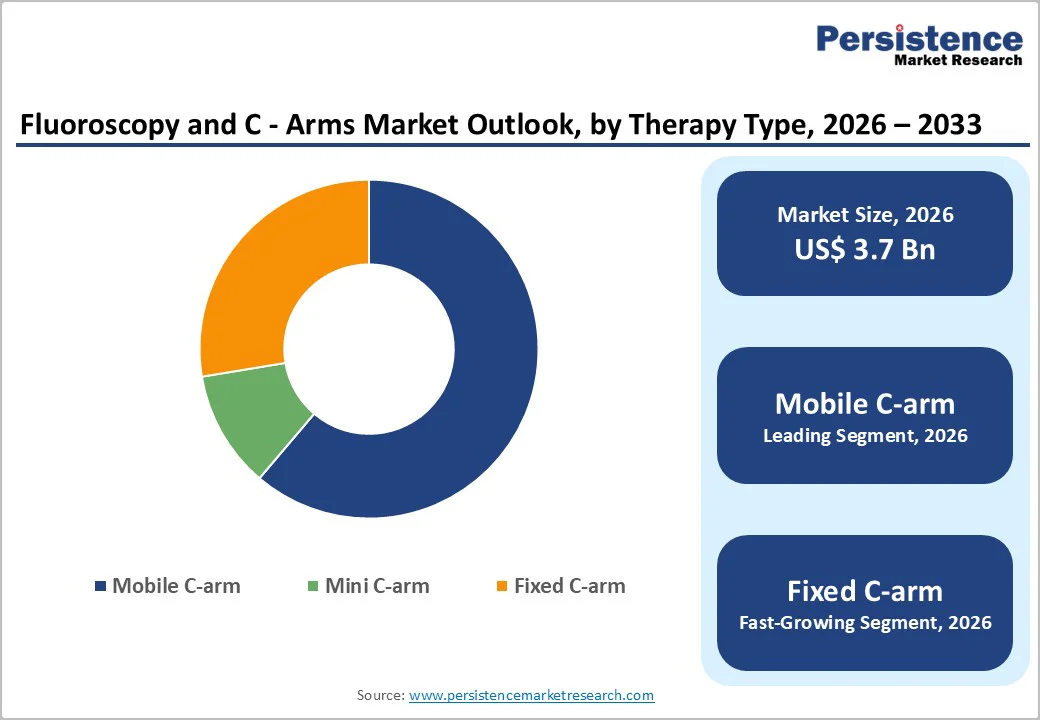

- Dominant Segment: Mobile C-arms dominate the 2025 market with 61.2% share, driven by their flexibility, lower installation costs, rising use in minimally invasive surgeries, and broad adoption across orthopedics, cardiovascular, pain management, and emergency departments. Mini C-arms continue expanding in orthopedics, while fixed C-arms retain demand in high-acuity interventional suites.

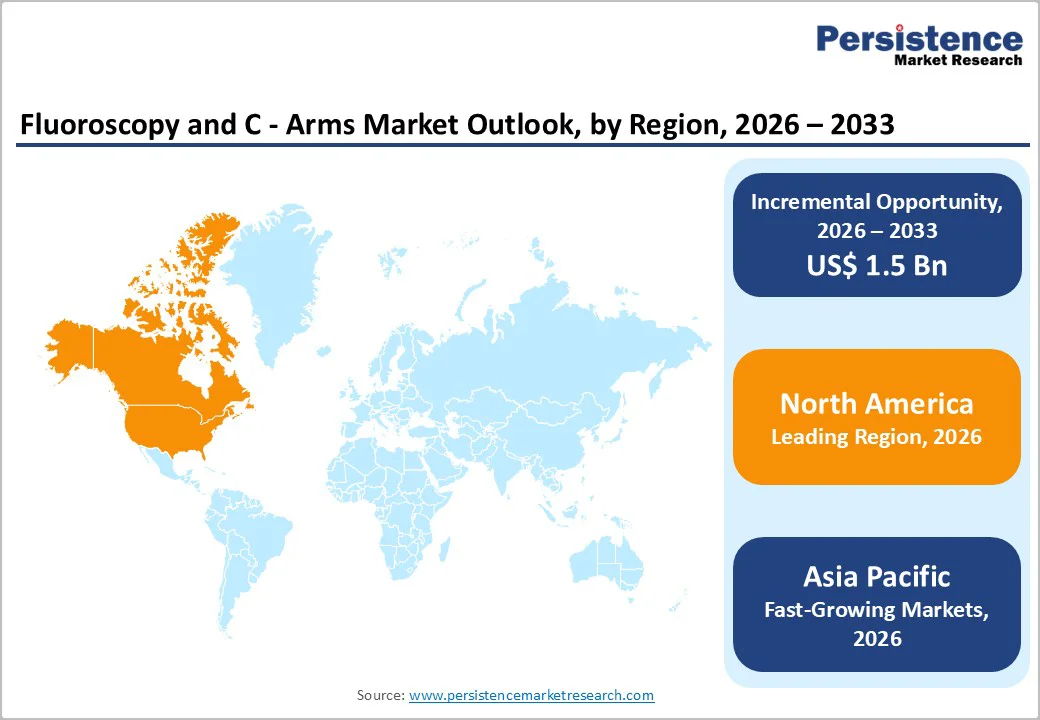

- Dominant Region: North America leads with 38.1% share due to advanced surgical infrastructure, strong adoption of digital and flat-panel C-arms, favorable reimbursement, and continuous hospital upgrades. Europe follows with strong procedural volumes, while Asia Pacific is the fastest-growing region, driven by expanding hospitals, rising trauma cases, and increasing investments in imaging modernization.

- Market Drivers: Growth is fueled by rising minimally invasive surgeries, increasing orthopedic and cardiovascular procedures, technological advancements such as flat-panel detectors, demand for real-time imaging, growing geriatric population, and continuous shifts toward outpatient/ambulatory surgical centers requiring compact and mobile imaging systems.

- Market Opportunity: Key opportunities include expanding digital mobile C-arms, AI-assisted imaging, dose-reduction technologies, value-tier systems for emerging markets, strengthening after-sales service networks, and partnerships with hospitals and surgical centers to penetrate high-growth segments such as orthopedics, pain management, and trauma care.

| Key Insights | Details |

|---|---|

|

Global Fluoroscopy and C - Arms Market Size (2026E) |

US$ 3.7 Bn |

|

Market Value Forecast (2033F) |

US$ 5.3 Bn |

|

Projected Growth (CAGR 2026 to 2033) |

5.0% |

|

Historical Market Growth (CAGR 2020 to 2025) |

4.2% |

Market Dynamics

Driver - Rising volume of Minimally Invasive Surgeries

The global adoption of minimally invasive surgery (MIS) has grown dramatically, with over 86 million procedures performed annually worldwide. Between 2000 and 2018, laparoscopic cases increased by 462%, reflecting a significant shift from open surgeries to minimal-access techniques. MIS is now widely used across orthopedics, cardiology, urology, gastroenterology, and general surgery. These procedures rely heavily on real-time imaging for accurate instrument guidance, implant placement, and intraoperative verification, directly boosting demand for fluoroscopy and C-arm systems. Mobile and mini C-arms are particularly valuable in outpatient and ambulatory surgical centers, while fixed C-arms are essential in high-acuity interventional suites and hybrid operating rooms. The rising number of MIS procedures increases procedural efficiency, reduces patient recovery times, and encourages hospitals to invest in advanced imaging platforms. Consequently, the expanding volume of minimally invasive surgeries serves as a key structural driver, fueling the growth and adoption of fluoroscopy and C-arm technologies across global healthcare facilities.

Restraints - Maintenance and Service Challenges

Maintenance and service challenges pose a significant restraint on the Fluoroscopy and C-Arms market. Studies indicate that 29% of radiology departments experience equipment breakdowns most months, and 14% report weekly malfunctions. Such downtime disrupts clinical workflows, delaying imaging-guided surgeries and forcing rescheduling, which affects hospital efficiency and patient care. Unplanned repairs are costly, as emergency service calls and spare-part replacements often carry premiums well above routine maintenance costs.

High-end C-arm systems require regular calibration, software updates, and preventive servicing, adding to operational expenses. Maintenance agreements alone can account for 5–10% of the total equipment lifecycle cost, making ownership expensive for smaller hospitals and outpatient centers. In regions with limited technical support or slower regulatory oversight, these challenges are exacerbated, reducing adoption rates. Consequently, concerns over recurring maintenance costs, system reliability, and service accessibility act as a key restraint, slowing investment in new C-arm technologies despite the rising demand for advanced imaging solutions.

Opportunity - Hybrid OR and advanced interventional suites

The growth of hybrid operating rooms (hybrid ORs) and advanced interventional suites presents a significant opportunity for the fluoroscopy and C-Arms market. Globally, over 1,500 hybrid ORs were installed as of 2024, with more than 60% of complex procedures relying on real-time fluoroscopy or angiography imaging. In the U.S., over 72% of large hospital systems now operate at least one hybrid ORs. These suites are increasingly used for cardiovascular, vascular, neuro, spine, and trauma procedures, which require precise intraoperative imaging for optimal outcomes.

The integration of advanced C-arm systems in hybrid ORs allows surgeons to perform minimally invasive procedures with enhanced accuracy, reducing patient transfers and improving workflow efficiency. As hospitals invest in upgrading traditional operating rooms to hybrid suites, the demand for fixed and angiography-integrated C-arms is expected to rise sharply. This trend positions hybrid OR expansion as a major driver of market growth and technological adoption worldwide.

Category-wise Analysis

By Product Insights

Mobile C-arm likely accounted for 61.3% share of the global market in 2025, and known for their flexibility, portability, and suitability across diverse clinical settings. In 2024, the global mobile C-arm segment accounted for ~ 82% share. Their compact design lets hospitals avoid dedicated imaging rooms saving space, power-nfrastructure and cost and allows easy movement between ORs, emergency-wards, or ICUs. Because many centers perform a mix of orthopedic, trauma, cardiovascular, and minimally invasive procedures, a mobile system’s versatility and lower overhead make it the preferred choice. As surgical volumes rise globally particularly for trauma, orthopedics and minimally invasive interventions hospitals favor mobile C-arms for their rapid deployment and high utilization across departments, reinforcing their dominant share.

By Application Insights

Angiography dominates the Fluoroscopy and C-Arms market due to the high volume of cardiovascular procedures worldwide. In the U.S., over 1 million invasive coronary angiography and PCI procedures are performed annually. These procedures require real-time X-ray imaging and precise fluoroscopy guidance, making C-arms essential in cath labs and interventional suites. The growing prevalence of cardiovascular diseases, which remain a leading cause of morbidity and mortality, ensures consistent demand for angiographic procedures. As hospitals expand catheterization and interventional labs to accommodate increasing patient volumes, both fixed and mobile C-arm systems are extensively deployed. This widespread reliance on C-arms for angiography reinforces the application’s dominance, positioning it as the primary driver of market demand and technological adoption across healthcare facilities globally.

Regional Insights

North America Fluoroscopy and C - Arms Market Trends

North America dominates the fluoroscopy and C - Arms market with 38.1% share in 2025, for their advanced healthcare infrastructure and widespread adoption of imaging-guided procedures. As of 2024, approximately 36–40% of global fluoroscopy systems are installed in the region. In the U.S., over one million percutaneous coronary and angiographic procedures are performed annually, most requiring real-time fluoroscopy guidance. The region’s ageing population drives higher demand for orthopedic, cardiovascular, and minimally invasive interventions. Hospitals and surgical centers in North America have strong investment capacity, enabling rapid adoption of digital flat-panel and mobile C-arm systems. High procedural volumes, well-established reimbursement frameworks, and skilled medical personnel further reinforce the region’s market dominance. Consequently, North America maintains the largest share in the global Fluoroscopy and C-Arms market, leading both in usage and technological penetration.

Europe Fluoroscopy and C - Arms Market Trends

Europe is a leading market due to high procedural volumes and robust healthcare infrastructure. Cardiovascular disease is the leading cause of death, accounting for approximately 3.9 million deaths annually, driving strong demand for interventional imaging. In 2022, around 1.06 million percutaneous coronary angioplasty procedures were performed across the EU, most requiring real-time fluoroscopy or C-arm guidance. The ageing population and rising prevalence of chronic conditions such as orthopedic disorders, vascular diseases, and cancer further increase the need for minimally invasive procedures. Well-established hospitals, strong public healthcare expenditure, and widespread availability of interventional suites support consistent adoption of C-arm systems. Europe remains a critical market for current usage and future growth of fluoroscopy and C-arm technologies.

Asia Pacific Fluoroscopy and C - Arms Market Trends

Asia Pacific is the fastest-growing region in the fluoroscopy and C-Arms market due to rapid expansion of healthcare infrastructure, increasing surgical volumes, and rising disease burden. The region has an average of 2.6–2.8 hospital beds per 1,000 population, improving access to inpatient and interventional care. Cardiovascular diseases account for over 30% of total deaths, driving demand for angiography, interventional cardiology, and minimally invasive procedures that rely on real-time imaging. Governments and private healthcare providers are investing heavily in modern hospitals and clinics equipped with advanced imaging technologies. Rising awareness, affordability of procedures, and increasing procedural volumes across orthopedics, cardiology, and trauma care further fuel adoption. These combined factors position Asia Pacific as the fastest-growing market for fluoroscopy and C-arm systems globally.

Competitive Landscape

Leading companies in the fluoroscopy and C-Arms market focus on precision engineering, advanced imaging technologies, and stringent quality standards. They invest in developing mobile, mini, and fixed C-arm systems, enhance image clarity and dose efficiency, and partner with hospitals. R&D emphasizes reliability, versatility, and cost-effectiveness, supporting wider adoption across surgical, orthopedic, and interventional procedures globally.

Key Industry Developments:

- In July 2025, The FDA granted clearance to Siemens Healthineers for its new radiography and fluoroscopy systems. This approval allowed the company to introduce the advanced imaging solutions in the U.S., aimed at improving diagnostic accuracy and workflow efficiency.

- In November 2024, GE HealthCare announced advanced imaging innovations for its OEC 3D C-arm, aimed at enhancing precision care in interventional pulmonology. The upgrades improved 3D imaging capabilities, enabling clinicians to navigate complex pulmonary procedures with greater accuracy and efficiency.

- In March 2024, Siemens Healthineers received FDA clearance for its CIARTIC Move, a self-driving mobile C-arm. The approval allows the company to commercialize the autonomous imaging system in the United States, highlighting its innovation in surgical imaging and minimally invasive procedures.

Companies Covered in Fluoroscopy and C - Arms Market

- Siemens Healthineers

- GE Healthcare

- Philips Healthcare

- Ziehm Imaging

- Canon Medical Systems Corporation

- Shimadzu Corporation

- Hologic, Inc.

- OrthoScan, Inc.

- Eurocolumbus S.r.l.

- Allengers Medical Systems Limited

- DMS Imaging

- BMI Biomedical International

- MS Westfalia GmbH

- Technix S.p.A.

- Others

Frequently Asked Questions

The global fluoroscopy and C - Arms Market is projected to be valued at US$ 3.7 billion in 2026.

Rising minimally invasive surgeries, increasing chronic diseases, technological advancements, aging population, and expanding hospital infrastructure drive the global C‑Arms market.

The global fluoroscopy and C - Arms Market is poised to witness a CAGR of 5.0% between 2026 and 2033.

Opportunities include hybrid ORs, mobile and mini C-arms, AI integration, emerging markets, advanced imaging technologies, and service-based revenue streams.

Siemens Healthineers, GE Healthcare, Philips Healthcare, Ziehm Imaging, Canon Medical Systems Corporation, Shimadzu Corporation.