- Technology

- DIY Home Security Solutions Market

DIY Home Security Solutions Market Size, Trends, Share, and Growth Forecast 2026 - 2033

DIY Home Security Solutions Market by Product (Monitoring and Alarming Systems, DIY Security Cameras, Others), by Component (Hardware, Software, Services), by Distribution Channel (Online Retail, Offline Retail), by Regional Analysis, 2026 - 2033

DIY Home Security Solutions Market Size and Trend Analysis

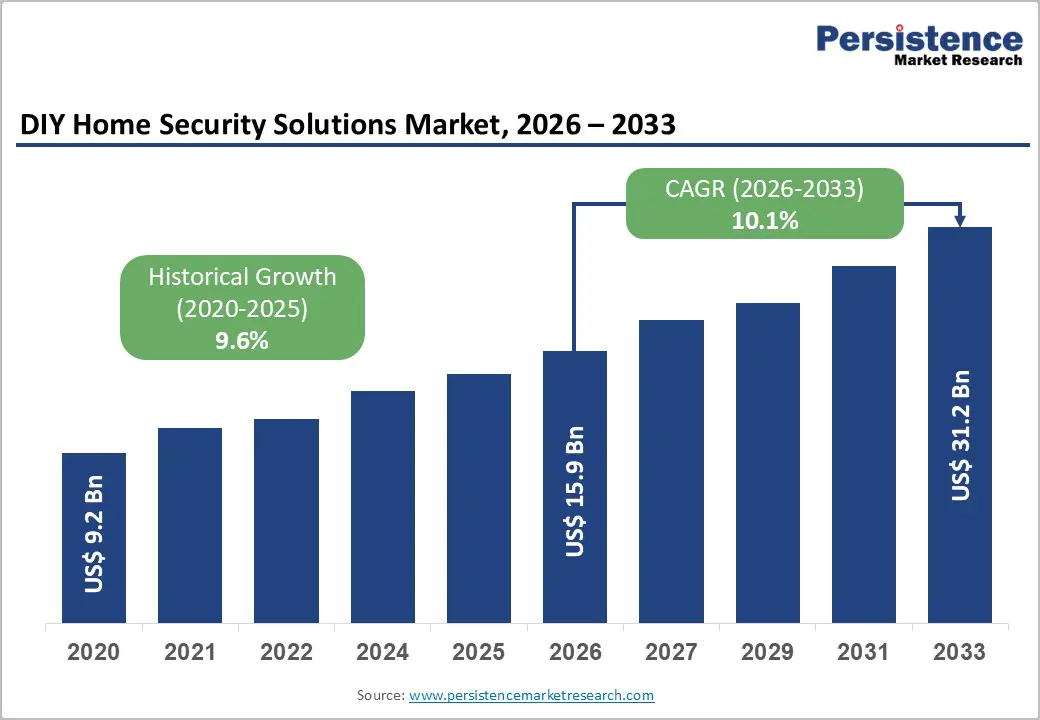

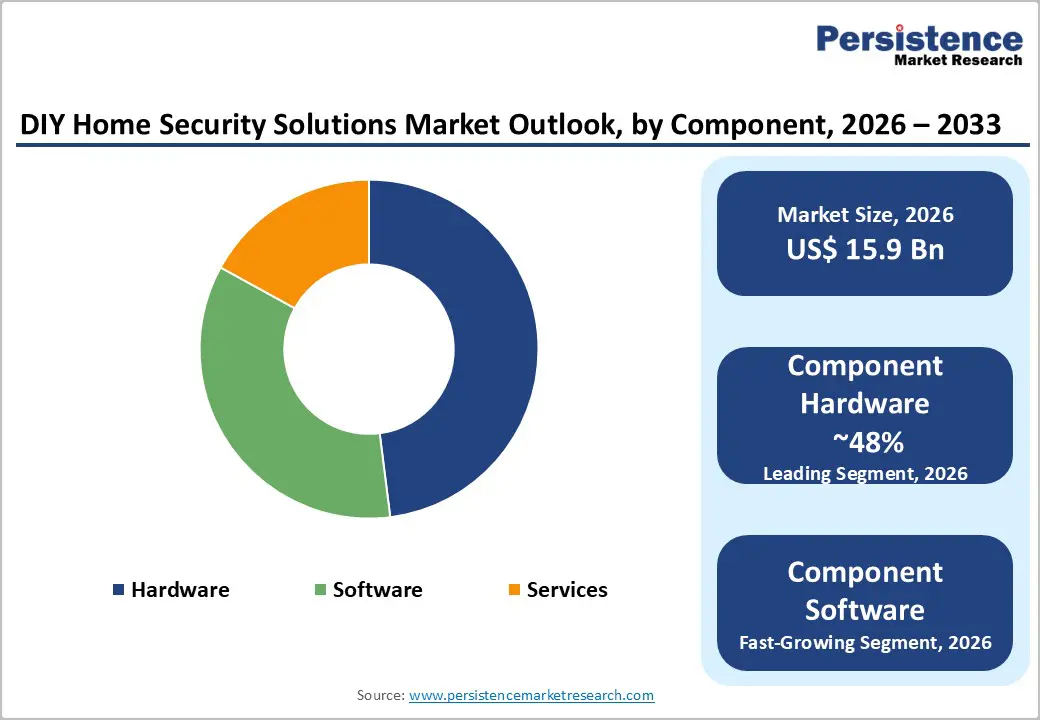

The global DIY home security solutions market size is projected to reach US$ 15.9 billion in 2026 and expand to US$ 31.2 billion by 2033, registering a CAGR of 10.1%.

Growth is driven by rising consumer awareness of home safety, rapid advancements in wireless and IoT-enabled devices, and a strong shift toward affordable, self-installed security systems. Increasing property crime rates, urbanization, and higher disposable incomes, especially in developing regions, are prompting homeowners to invest more in residential protection. The growing demand for flexible, user-friendly, and cost-effective security options continues to accelerate the global market’s adoption.

Key Industry Highlights:

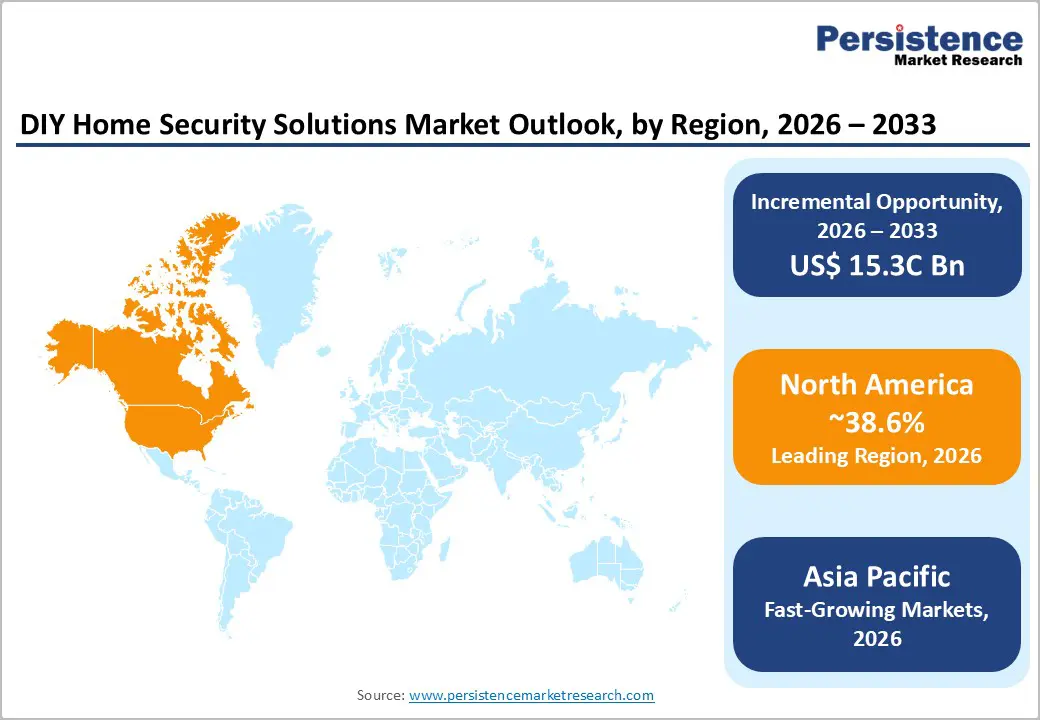

- Leading Region: North America leads with a 38.6% share, supported by high awareness, strong purchasing power, and advanced adoption of integrated DIY smart security solutions.

- Fastest Growing Market: Asia Pacific records the highest expansion momentum, holding 32.6% share, driven by urbanization, rising middle-class demand, and extensive smart city initiatives.

- Dominant Segment: DIY Security Cameras remain the top product segment with strong adoption levels, reflected by 38% of U.S. households using smart security cameras.

- Fastest Growing Segment: Software & services represent the fastest-expanding category, driven by rising demand for AI analytics, cloud storage, and subscription-based monitoring solutions.

- Key Opportunity: AI-enabled video analytics offers the strongest opportunity, enhancing real-time detection, predictive insights, and premium subscription value.

| Key Insights | Details |

|---|---|

| DIY Home Security Solutions Market Size (2026E) | US$ 15.9 Billion |

| Market Value Forecast (2033F) | US$ 31.2 Billion |

| Projected Growth CAGR (2026 - 2033) | 10.1% |

| Historical Market Growth (2020 - 2025) | 9.6% |

Market Dynamics

Drivers - Rising Consumer Demand for Smart Home Integration and Remote, Real-Time Monitoring Capabilities

Growing consumer expectations for convenient, connected home environments are accelerating demand for smart DIY security systems. With smartphones and mobile apps becoming central to home management, homeowners increasingly value real-time monitoring, live video access, and instant alerts. Nearly 87% of smart home users configure custom zones and notifications, demonstrating a clear preference for personalized, on-demand security visibility.

The integration of DIY security solutions with broader smart home ecosystems covering lighting, smart locks, sensors, and voice assistants further enhances user experience and safety confidence. More than half of homeowners report feeling significantly safer with connected security systems installed. Unified mobile platforms that consolidate multiple smart functions into a single interface strengthen the value proposition, motivating consumers to adopt scalable, easy-to-install DIY cameras and monitoring devices.

Declining Hardware Costs, Increased Product Affordability, and Wider Consumer Accessibility

Advancements in wireless technology, camera sensors, and IoT components have substantially reduced the cost of manufacturing smart security devices. As 4K imaging components, batteries, and cloud storage become more affordable, companies now offer high-performance DIY systems at accessible prices for middle-income households. This downward cost trend has eliminated traditional affordability barriers and broadened mainstream adoption. Flexible payment models and subscription-based monitoring starting as low as US$ 4.99 per month further ease adoption for budget-conscious consumers. These affordability benefits allow homeowners to build comprehensive, professional-grade DIY protection without large upfront expenses.

Restraints - Privacy Concerns and Data Security Vulnerabilities in Connected DIY Security Ecosystems

Rising consumer anxiety about data security continues to restrain market growth, with nearly 72% of users expressing concern over how personal information from smart home devices is collected and transmitted. Modern security cameras and sensors capture extensive audio-video data, elevating fears of unauthorized access, misuse, or surveillance. These concerns are reinforced by the fact that 31% of users cite privacy as their top concern.

The increasing prevalence of cyberattacks further intensifies hesitation, as an estimated 9% of smart homes experienced at least one breach attempt during 2024 - 2025. The interconnected nature of smart home ecosystems, where camera data may pass through third-party platforms, deepens distrust. This perceived vulnerability discourages adoption among privacy-focused consumers, particularly those wary of cloud-based storage and remote monitoring features.

Interoperability Limitations and Standardization Challenges Across Smart Home Security Devices

The DIY home security market remains hindered by fragmented device ecosystems and inconsistent compatibility across brands. Consumers often find themselves tied to platforms such as Amazon Alexa, Google Home, or Apple HomeKit, with limited ability to mix and match devices. Proprietary wireless protocols and communication standards further complicate multi-brand integration, creating confusion for users seeking seamless system management.

The lack of universal standards for connectivity and data exchange also weakens user experience, especially when attempting to integrate older security components with newer devices. These technical gaps can force homeowners to rely on a partial professional setup, raising overall costs. Such complexities reduce the appeal of DIY installations and deter consumers seeking simple, cohesive, and fully interoperable home security solutions.

Opportunity - Artificial Intelligence Integration and Advanced Video Analytics as High-Value Growth Accelerators

Artificial intelligence and machine learning are transforming DIY security systems into proactive, highly responsive solutions. Modern AI-enabled cameras use real-time computer vision to distinguish between people, vehicles, and animals with far greater precision, dramatically reducing false alarms. Innovations such as Arlo Secure 5, which offers advanced object and behavior detection, highlight the shift toward personalized, context-aware residential security experiences.

These capabilities allow devices to identify anomalies, trigger automated actions such as siren activation, and integrate smoothly with broader smart home systems. As cloud-based AI platforms from providers such as AWS Rekognition and Google Vision AI advance, more consumers are adopting subscription-based premium analytics. This trend supports a transition toward recurring service revenues, creating a strong opportunity for brands to move beyond hardware-centric business models.

Expanding Asia Pacific Urbanization and Rise in Middle-Class Adoption Driving Regional Growth

The Asia Pacific region presents exceptional growth potential as accelerating urbanization, rising incomes, and growing security awareness fuel demand for DIY residential protection solutions. India is witnessing strong traction, propelled by the expansion of the middle class and the widespread availability of affordable smart home devices through e-commerce channels.

China remains a dominant regional force due to its large-scale manufacturing ecosystem and high domestic demand. Government-backed smart city initiatives, rapid infrastructure development, and declining hardware costs are further widening opportunities across emerging markets. With major players like Dahua, Hikvision, and EZVIZ driving technological innovation, the Asia Pacific is positioned to be the fastest-growing region contributing the largest incremental revenue to the global DIY home security market during the forecast period.

Category-wise Analysis

Product Insights

DIY security cameras lead the product category, accounting for about 52% of the total market share. Their dominance is reinforced by high adoption rates 38% of U.S. households use smart cameras and 33% use video doorbells. Affordable pricing, simplified installation, and continuous upgrades in HD imaging, wireless connectivity, and cloud storage keep cameras the most preferred product type in home security ecosystems.

Monitoring and Alarming Systems represent the fastest-growing category, driven by the rising need for intrusion detection and whole-home protection. Additionally, specialized devices such as environmental sensors and multi-functional smart safety tools are gaining traction as consumers expand beyond basic surveillance and seek fully integrated, automated security environments.

Component Analysis

Hardware is the leading component category, representing approximately 48% of total market revenues. This dominance stems from sustained consumer demand for essential security equipment, such as cameras, sensors, wireless modules, and alarm devices that form the physical backbone of any security system. Continuous innovation in camera sensors, long-range connectivity, and battery life also reinforces hardware’s central market position.

Software and cloud-based services remain the fastest-growing category as consumers increasingly adopt AI analytics, cloud storage, emergency alerts, automated event detection, and subscription-based monitoring. These value-added digital layers enhance system intelligence and convenience, accelerating the industry-wide transition toward software-driven, recurring-revenue security models.

Distribution Channel Insights

Online Retail is the dominant distribution channel, holding an estimated around 62% market share. Its leadership is fueled by consumers’ preference for convenient purchasing, price comparison tools, verified reviews, tutorial access, and doorstep delivery. E-commerce retail also aligns perfectly with the DIY nature of the segment, enabling buyers to select and install systems independently.

Offline Retail is the fastest-growing channel as consumers seek hands-on demonstrations, immediate product availability, and in-store expert guidance. Electronics retailers and home improvement chains benefit from shoppers who prefer physical inspection, personalized consultation, or optional assisted installation before finalizing purchases.

Regional Insights

North America DIY Home Security Solutions Trends

North America maintains its position as the largest and most mature market for DIY home security. It remains the largest and most technologically mature market, holding 38.6% share, supported by high consumer awareness, strong purchasing power, and early adoption of smart home ecosystems. Widespread use of wireless cameras, smart alarms, and self-install kits reflects growing demand for flexible, subscription-based monitoring alternatives. Major players such as Ring, SimpliSafe, ADT, and Google Nest dominate regional sales momentum.

Government grants and supportive regulations further strengthen adoption, especially in the U.S. Programs under FEMA, DHS, and local cybersecurity funding lower cost burdens for households upgrading security infrastructure. Partnerships between homebuilders and security device manufacturers accelerate deployment in new constructions, while stringent frameworks such as CCPA enhance consumer trust. Collectively, these drivers ensure the region maintains long-term leadership in DIY home security solutions.

Europe DIY Home Security Solutions Trends

Europe represents a privacy-driven, regulated ecosystem with consumers prioritizing secure, compliant DIY security solutions. The region expands at 10.5% CAGR, fueled by rising smart home penetration and growing adoption of wireless surveillance tools. Germany, the U.K., and France collectively drive demand, particularly for solutions aligning with privacy-by-design standards and interoperable home automation platforms.

Strict regulatory frameworks, including GDPR, the DSA, and DMA, shape market requirements by mandating strong data protection and transparency for device operation. These rules build higher consumer confidence, encouraging the adoption of AI-enabled cameras and connected sensors across urban households. As privacy concerns remain paramount, manufacturers that emphasize secure data handling and compliance-ready product design continue to gain a competitive advantage across diverse European markets.

Asia Pacific DIY Home Security Solutions Trends

Asia Pacific is the fastest-growing market, supported by rapid urbanization, expanding internet connectivity, and rising residential security awareness. The region accounts for a 32.6% share, driven by high-volume manufacturing, affordable product availability, and strong adoption in China, India, and Japan. Increasing smartphone penetration and 5G rollout further accelerate uptake of cloud-connected home security ecosystems.

China leads as both a major consumer and manufacturing hub, while India’s growing middle class drives strong demand for budget-friendly smart cameras and sensors. Government-led smart city development and competitive pricing by local brands like Hikvision, Dahua, and EZVIZ boost market expansion. International companies increasingly invest in regional integration strategies, recognizing the Asia Pacific as the primary engine of incremental global revenue growth.

Competitive Landscape

The DIY home security solutions market is moderately consolidated, supported by strong brand recognition, advanced technology capabilities, and extensive distribution networks. Leading players focus on continuous innovation in connected devices, AI-enabled analytics, and flexible subscription models, strengthening their competitive edge. Emphasis on seamless integration with broader smart home ecosystems remains a core differentiator as consumers prioritize convenience, automation, and data privacy.

Rising R&D investments in intelligence-driven detection, customizable alerts, and cloud-based monitoring further intensify competition. Strategic collaborations with complementary smart home technology providers enhance interoperability and product value. Meanwhile, cost-focused entrants gain traction through affordable, feature-rich offerings, and traditional security providers are shifting toward hybrid DIY-professional models to align with evolving consumer preferences.

Key Market Developments:

- In May 2025, ADT collaborated with Yale and the Z-Wave Alliance to introduce the Yale Assure Lock 2 Touch with Z-Wave, the only fingerprint-controlled smart lock leveraging the newly developed Z-Wave User Credential Command Class, enabling users to unlock and disarm security systems using biometric authentication.

- In March 2025, Yale announced the Yale Smart Lock with Matter, designed specifically for Google Home users, featuring extended battery life, multiple unlocking options including entry codes and apps, and seamless integration with Matter-certified smart home platforms, building on the popular Nest x Yale Lock partnership.

- In September 2024, Arlo Technologies unveiled Arlo Secure 5, the next generation of smart home security powered by Arlo Intelligence, introducing industry-first AI features including custom detections, vehicle recognition, and person recognition to provide highly personalized protection and meaningful alerts.

Companies Covered in DIY Home Security Solutions Market

- Ring

- SimpliSafe

- Arlo Technologies

- Wyze Labs

- Google Nest

- ADT

- Brinks Home Security

- Vivint Smart Home

- Frontpoint Security

- Eufy Security

- Dahua Technology

- Hikvision / EZVIZ

- Samsung SmartThings

- Yale

- Abode Systems

- Cove

- Blink Home

- Logitech Circle

Frequently Asked Questions

The DIY home security solutions market is valued at US$ 15.9 billion in 2026, expected to reach US$ 31.2 billion by 2033, supported by rising demand for affordable, self-installed smart security systems.

Growth is fueled by declining hardware costs, increasing smart home adoption, AI-enabled threat detection, and rising consumer focus on real-time remote monitoring.

DIY Security Cameras lead the market, strengthened by 38% adoption among U.S. households and growing demand for wireless, cloud-integrated surveillance.

North America remains the top regional market with a 38.6% share, while Asia Pacific is the fastest growing, holding 32.6% share, driven by rising urbanization and smart city initiatives.

AI-powered video analytics presents the strongest opportunity by enabling predictive, real-time threat detection and supporting premium subscription models.

Leading market participants include Ring, SimpliSafe, Arlo Technologies, Wyze Labs, and Google Nest.