- Media & Entertainment

- Cinema Point of Sale (POS) Solutions Market

Cinema Point of Sale (POS) Solutions Market Size, Share, and Growth Forecast 2026 - 2033

Cinema Point of Sale (POS) Solutions Market by Solution (On-premise POS Software, Cloud based POS Solution, Mobile POS Solution), by Business Model (License Based, Subscription based, Professionally Managed), Application (Ticketing & Seat Booking, Food & Beverage Sales, Merchandise and Retail, Membership & Loyalty Management), and Regional Analysis, 2026 - 2033

Cinema Point of Sale (POS) Solutions Market Size and Trend Analysis

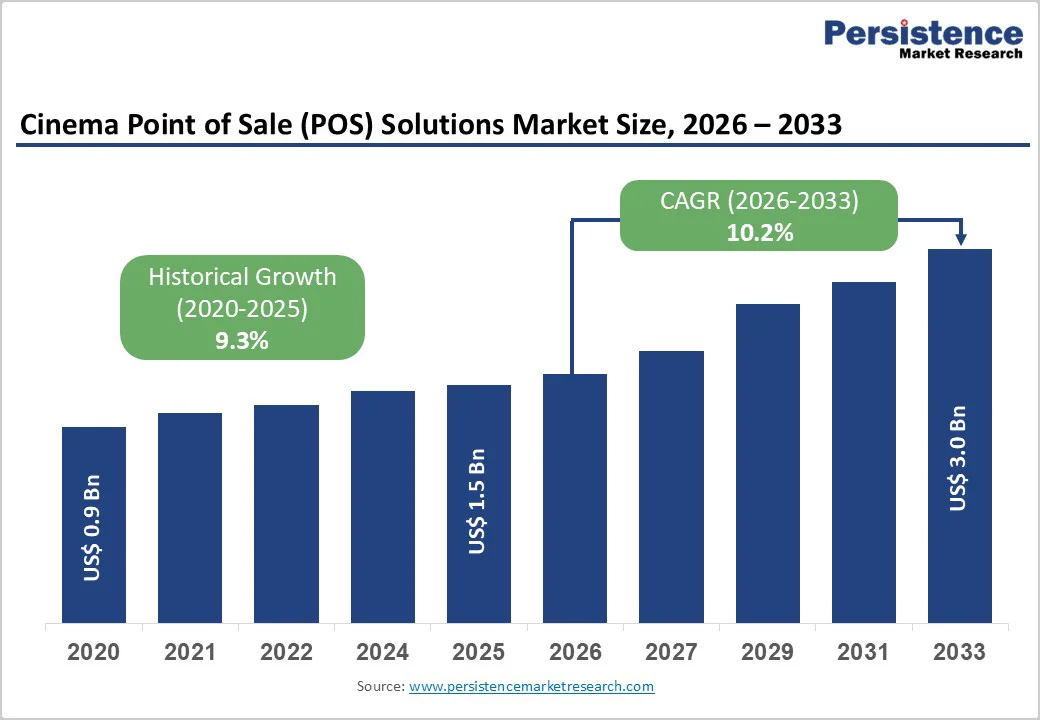

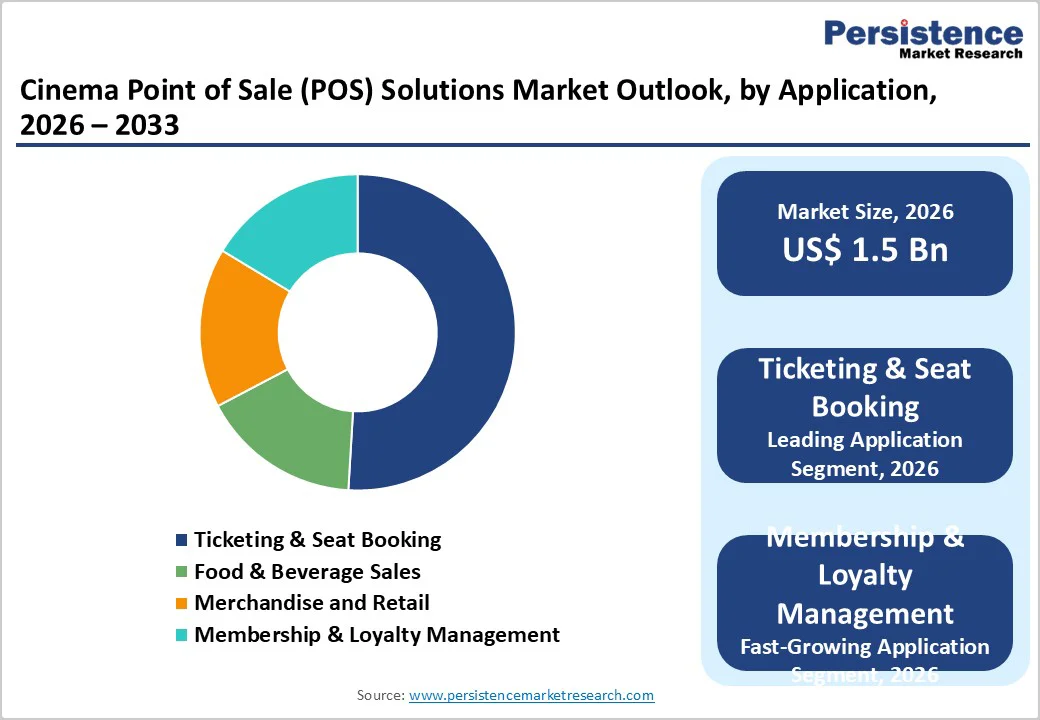

The global cinema point of sale (POS) solutions market size is likely to be valued at US$ 1.5 billion in 2026 and projected to reach US$ 3.0 billion by 2033, growing at a CAGR of 10.2% between 2026 and 2033.

The market is primarily driven by the accelerated adoption of cloud-based systems, increasing demand for contactless and mobile payment solutions, and the integration of advanced analytics for enhanced customer experience. Cinema operators are increasingly prioritizing digital transformation initiatives to streamline ticketing operations, optimize concession sales, and implement comprehensive loyalty management programs.

Key Market Highlights

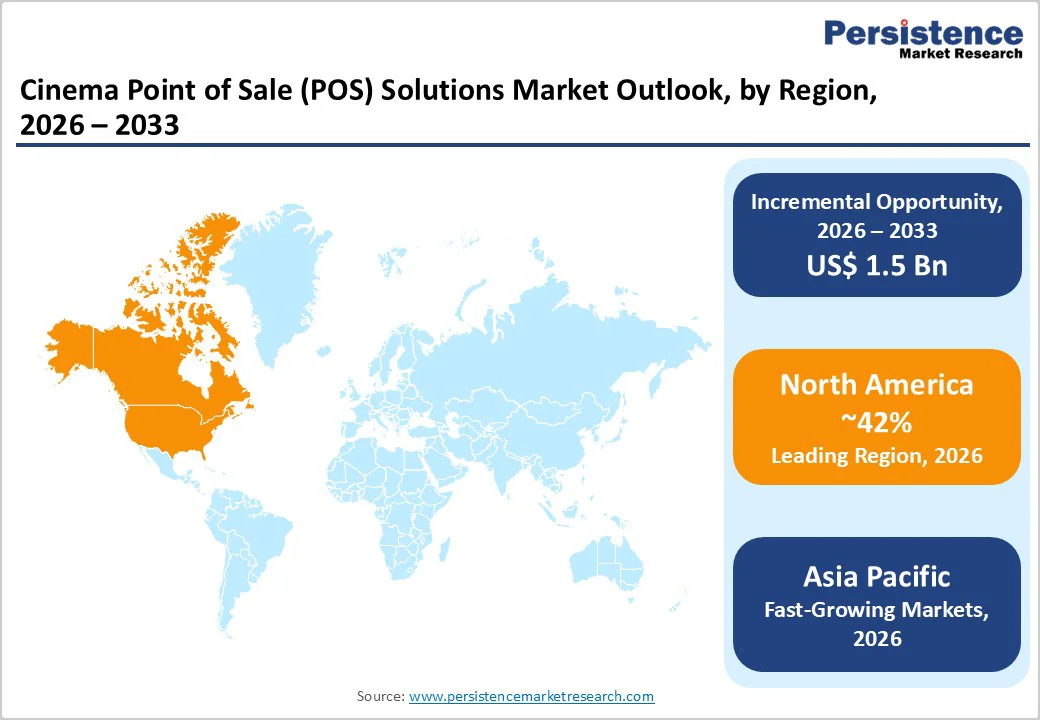

- North America market leadership: North America maintains the dominant regional position with approximately 42% global market share in 2025, driven by mature cinema infrastructure, high technology adoption rates, substantial consumer entertainment spending, and early adoption of cloud-based POS solutions.

- Asia-Pacific fastest growth: Asia-Pacific emerges as the fastest-growing region, projected to expand at CAGR of 14% from 2025 to 2032, fueled by rapid urbanization, expanding middle-class demographics, accelerating cinema screen deployment in China and India, and mobile payment ecosystem sophistication.

- Cloud-based solution dominance: Cloud-based POS solutions dominate the market with approximately 70% market share in 2025, driven by superior scalability, flexibility, reduced infrastructure costs, automatic updates, and seamless remote management capabilities.

- Fastest growing business model: Professionally managed service models represent the fastest-growing business category with projected CAGR of 16% from 2025 to 2032, reflecting cinema operator preference for delegating system management and optimization to specialized service providers.

- Loyalty program opportunity: Membership and loyalty management applications represent the fastest-growing business model with CAGR of 17% from 2025 to 2032, driven by cinema operator emphasis on customer retention, repeat visitation frequency, and lifetime value optimization through sophisticated loyalty program integration.

| Key Insights | Details |

|---|---|

| Cinema Point of Sale (POS) Solutions Market Size (2026E) | US$ 1.5 Bn |

| Market Value Forecast (2033F) | US$ 3.0 Bn |

| Projected Growth CAGR (2026 - 2033) | 10.2% |

| Historical Market Growth (2020 - 2025) | 9.3% |

Market Dynamics

Drivers - Digital Transformation and Omnichannel Customer Experience Expectations

The cinema industry is experiencing rapid digital transformation driven by evolving consumer expectations for seamless, integrated ticketing and concession purchasing experiences across multiple touchpoints. Modern moviegoers expect the ability to purchase tickets via mobile apps, websites, self-service kiosks, and traditional box office counters, with consistent pricing and loyalty program integration across all channels. The global box office reached USD 42.5 billion in 2019 and continues a recovery trajectory, providing substantial demand for advanced POS infrastructure.

Cinema operators recognize that integrated POS solutions enable real-time inventory synchronization, preventing overbooking across channels and ensuring consistent customer experiences. Additionally, the integration of mobile ticketing with QR code scanning technology has become standard, reducing physical contact points and improving operational efficiency. Cinemas implementing omnichannel POS platforms report operational efficiency improvements of up to 25% through automated transaction processing and real-time data analytics capabilities.

Rising Adoption of Cloud-Based Solutions and Mobile Payment Technologies

Cloud-based cinema POS solutions have emerged as the dominant deployment model, capturing approximately 60-65% market preference due to superior scalability, flexibility, and reduced infrastructure costs. Cloud architecture enables cinema operators to access sophisticated analytics dashboards, real-time reporting, and remote management capabilities from any location via internet connectivity. The proliferation of mobile payment options including Apple Pay, Google Pay, Samsung Pay, and contactless payment cards has driven consumer expectations for frictionless payment experiences.

Mobile POS functionality enables cinema staff to process transactions, verify customer loyalty status, and manage inventory from anywhere within the venue, substantially reducing transaction processing times and improving customer satisfaction. The shift from perpetual licensing models to subscription-based SaaS offerings has democratized access to enterprise-grade cinema management systems, enabling independent and smaller cinema chains to compete with major multiplex circuits through affordable, feature-rich cloud solutions.

Restraints - High Implementation Costs and Complex System Integration Challenges

Despite significant technological advantages, the substantial costs of implementing advanced cinema POS systems present significant barriers to adoption, particularly for independent cinema operators and smaller regional chains. Enterprise-grade cinema management platforms require significant capital investments in hardware infrastructure, software licensing, staff training, and data migration services. Integration complexity arises from the necessity to connect new POS systems with existing ticketing platforms, loyalty databases, accounting software, and third-party payment processors.

Smaller cinema operators frequently operate on constrained budgets with limited IT resources, making extended implementation timelines and technical complexity significant adoption barriers. Legacy system compatibility issues often require complete infrastructure replacement rather than system upgrades, multiplying total cost of ownership for cinema operators. These factors create extended procurement decision-making processes and implementation delays, particularly among independent theatres and regional chains operating with limited capital expenditure budgets.

Cybersecurity Vulnerabilities and Data Privacy Compliance Requirements

Cinema POS systems handle sensitive customer payment data, personal information, and transaction histories, creating substantial cybersecurity risks and regulatory compliance obligations. Cinema operators must implement comprehensive security frameworks including PCI DSS (Payment Card Industry Data Security Standard) compliance, end-to-end encryption, secure payment gateway integration, and robust access controls. Data breaches exposing customer payment information and personal details result in significant financial penalties, regulatory sanctions, and reputational damage.

Smaller cinema operators frequently lack dedicated cybersecurity personnel and advanced threat detection capabilities, creating vulnerability to ransomware attacks and data theft incidents. The increasing prevalence of cybersecurity threats targeting retail POS systems creates substantial concerns about cloud-based solution security, with some cinema operators preferring expensive on-premises solutions for perceived control and security advantages. These cybersecurity and compliance challenges disproportionately impact smaller cinema operators and independent theatres, restraining market adoption among this critical customer segment.

Market Opportunities

AI-Driven Personalization and Dynamic Pricing Strategies for Revenue Optimization

Artificial intelligence and machine learning technologies are creating substantial opportunities for cinema operators to implement sophisticated pricing strategies and personalized customer engagement initiatives.

AI-powered POS analytics enable real-time prediction of ticket demand, optimal pricing recommendations based on historical trends, capacity utilization patterns, and competitive dynamics, enabling cinema operators to maximize revenue through dynamic pricing.

Machine learning algorithms analyze customer purchase histories, movie preferences, and demographic patterns to generate personalized promotional recommendations, increasing customer lifetime value and repeat visitation rates. Cinema operators implementing AI-driven personalization report substantial improvements in customer engagement, with predictive analytics enabling targeted email campaigns, personalized mobile app recommendations, and tailored loyalty program offers.

The integration of AI-powered chatbots and virtual assistants within cinema POS interfaces enables 24/7 customer support for ticketing questions, concession recommendations, and loyalty program inquiries. Advanced analytics dashboards providing real-time business intelligence enable cinema operators to make data-driven decisions regarding concession pricing, inventory optimization, and promotional strategies.

Companies successfully developing AI-enhanced cinema POS solutions are positioned to capture significant market share among tech-forward cinema operators and major multiplex circuits seeking competitive advantages through data-driven decision-making.

Expanded Integration with Third-Party Entertainment Platforms and Experiential Revenue Streams

Cinema POS systems are evolving beyond traditional ticket and concession sales to encompass broader entertainment and experiential revenue streams, creating substantial market expansion opportunities. Integration with streaming platforms, concert ticketing services, sports event broadcasting, and alternative content programming enables cinema operators to generate incremental revenue from non-traditional film content. The emergence of immersive experiences including virtual reality pre-show experiences, metaverse-based promotional content, and augmented reality interactive elements creates opportunities for POS systems to facilitate novel revenue streams.

Biometric authentication technologies including facial recognition and fingerprint scanning are being integrated into cinema POS interfaces to enable faster, more secure transactions while supporting frictionless customer experiences. Market participants developing POS solutions addressing these emerging revenue opportunities are positioned to capture disproportionate market share growth from forward-thinking cinema operators seeking revenue diversification beyond traditional ticket and concession sales.

Category-wise Analysis

Solution Insights

Cloud-based POS solutions dominate the cinema market, commanding approximately 70% market share in 2025, driven by superior scalability, flexibility, accessibility, and reduced infrastructure costs compared to on-premises alternatives. Cloud deployment enables cinema operators to implement sophisticated systems without substantial upfront capital expenditures for server infrastructure, ensuring automatic software updates, seamless remote management capabilities, and enhanced business continuity through redundant data centers. The cloud-based segment continues attracting substantial investment from major enterprise software vendors who recognize the recurring revenue potential of subscription-based models.

Business Model Insights

Subscription-based pricing models emerge as the leading business model, capturing approximately 55% market share in 2025, reflecting cinema operators' preference for predictable recurring costs, flexible service scalability, and elimination of large upfront capital expenditures. Subscription-based SaaS cinema POS platforms have democratized access to enterprise-grade systems previously available exclusively to large multiplex circuits, enabling independent and regional cinema operators to compete effectively through affordable, feature-rich solutions. The subscription model benefits cinema operators through continuous feature enhancements, automatic security updates, and vendor-provided technical support included within recurring subscription fees.

Application Insights

Ticketing and seat booking emerges as the dominant application, commanding approximately 50% market share in 2025, reflecting the fundamental importance of efficient ticket sales operations for cinema revenue generation and customer experience optimization. Sophisticated ticketing applications enable reserved seating, dynamic pricing based on demand forecasting, promotional bundling, and integration with third-party ticketing platforms including aggregators and fan community platforms. Food and beverage sales represent the second-largest application segment, capturing approximately 30-35% market share, driven by the substantial profit margins generated from concession operations compared to ticket sales. Advanced food and beverage POS functionalities enable integrated concession ordering, inventory management, kitchen display systems, and supply chain optimization.

However, membership and loyalty management applications represent the fastest-growing segment with projected CAGR of 17% from 2025 to 2032, reflecting cinema operator focus on customer retention, repeat visitation frequency, and lifetime value optimization through sophisticated loyalty programs. Loyalty management applications enable points-based rewards, tiered membership structures, personalized promotional targeting, and behavioral analytics enabling cinema operators to implement sophisticated customer relationship management strategies that differentiate offerings and drive customer loyalty.

Regional Insights

North America Cinema Point of Sale (POS) Solutions Market Trends

North America dominates the global cinema POS solutions market, commanding approximately 42% market share in 2025, driven by mature cinema infrastructure, high technology adoption rates, and substantial consumer discretionary spending on entertainment. The United States represents the largest regional market, with approximately 40,000 cinema screens generating substantial demand for advanced POS infrastructure. North American cinema operators prioritize cloud-based solutions, with approximately 70% of upgrading circuits transitioning to cloud deployment architectures. The region’s technological sophistication drives early adoption of emerging technologies including AI-powered personalization, biometric authentication, and omnichannel integrations.

Cinemark Holdings announced in May 2025 a strategic partnership with Vista Entertainment Solutions to deploy Vista’s cinema management platform across its U.S. and international circuits, exemplifying major cinema operator commitments to advanced POS infrastructure. GDC Technology announced in March 2025 the acquisition of CineManager, strengthening its end-to-end software stack for cinema operations through enhanced scheduling and ticketing capabilities. North American cinema operators focus heavily on premium experiences through laser projection retrofits, recliner installations, and luxury lobby redesigns, all supported by sophisticated POS systems enabling dynamic pricing and revenue optimization. The region’s innovation ecosystem continues driving continuous POS platform enhancements, with major vendors investing substantially in AI integration, mobile capabilities, and experiential revenue stream enablement.

Europe Cinema Point of Sale (POS) Solutions Market Trends

Europe represents the second-largest regional market characterized by diverse cinema market structures across Germany, United Kingdom, France, and Spain. Germany commands the largest European market share, with robust cinema attendance patterns supporting substantial POS platform investments. The United Kingdom demonstrates strong demand for cloud-based solutions, with NHS sustainability initiatives and government-backed digital transformation programs creating procurement momentum. France emphasizes premium cinema experiences with IMAX, Dolby Cinema, and specialized screening formats requiring sophisticated pricing and inventory management capabilities.

European cinema operators prioritize compliance with GDPR (General Data Protection Regulation) requirements, driving preference for POS solutions with robust data privacy frameworks, secure data residency options, and transparent data handling practices. Regulatory harmonization efforts across European Union member states are encouraging standardized POS platform adoption, enabling cinema chains to implement unified systems across multiple countries. European cinema operators increasingly implement contactless payment options and mobile ticketing, addressing post-pandemic health and safety concerns while improving transaction processing efficiency. Vendor consolidation trends in the European market are driving supply rationalization, with major multinational POS vendors expanding regional presence through acquisitions and partnerships with established cinema software providers.

Asia Pacific Cinema Point of Sale (POS) Solutions Market Trends

Asia-Pacific emerges as the fastest-growing regional market, projected to expand at CAGR of 14% from 2025 to 2032, driven by rapid urbanization, expanding middle-class demographics, and accelerating cinema infrastructure development. China dominates regional cinema expansion, with approximately 15,000 cinema screens installed in 2024 alone, creating extraordinary demand for POS infrastructure. Chinese cinema operators prioritize mobile ticketing integration, reflecting the region’s advanced mobile payment ecosystem dominated by Alipay and WeChat Pay. India represents a critical emerging market, with approximately 8,500 cinema screens and rapidly growing audience demographics supporting substantial POS platform investments.

Japan and Australia demonstrate strong demand for premium POS solutions, with cinema operators in these developed markets emphasizing technological sophistication and customer experience optimization. ASEAN markets including Vietnam, Thailand, and Indonesia represent emerging opportunities as cinema infrastructure development accelerates in conjunction with urbanization and income growth. Asian cinema operators increasingly implement sophisticated loyalty programs and behavioral analytics, capitalizing on advanced mobile technology adoption and consumer acceptance of digital engagement. Regional vendors developing POS solutions adapted to local payment ecosystems, regulatory environments, and operational preferences are capturing disproportionate market share growth through localization and regional partnership strategies.

Competitive Landscape

The cinema POS solutions market reflects a moderately consolidated structure, with over half of global revenue concentrated among large platform providers that offer end-to-end ticketing, concessions, and operational management systems. Despite this concentration, a sizeable segment of regional and niche vendors remains competitive by focusing on flexible deployments, customized workflows, and specialized features tailored to independent or boutique cinemas.

Leading vendors continue to strengthen their market position through cloud migration, integrated analytics, omnichannel capabilities, and strategic partnerships that expand their reach and enhance interoperability across ticketing, loyalty, and content management ecosystems. Competitive strategies increasingly emphasize intuitive user interfaces, real-time data intelligence, and seamless integration with third-party platforms to support streamlined operations and improved guest experiences. Business models are shifting toward subscription-based SaaS offerings, bundled managed services, and modular solution suites, enabling operators to scale functionality with lower upfront investments. Vertical specialization is also rising as vendors tailor solutions for emerging alternative entertainment venues.

Key Market Developments

- March 2025: GDC Technology announced acquisition of CineManager, strengthening its end-to-end cinema operations software stack and enhancing scheduling, ticketing, and reporting capabilities for global cinema operators managing complex multi-screen facilities.

- May 2025: Cinemark Holdings established strategic partnership with Vista Entertainment Solutions deploying Vista’s comprehensive cinema management platform across Cinemark’s U.S. and international circuits, exemplifying enterprise adoption of cloud-based POS solutions.

- September 2024: NCR Corporation launched enhanced cloud-based cinema POS platform featuring integrated AI-powered demand forecasting, dynamic pricing recommendations, and personalized customer engagement tools enabling cinema operators to optimize revenue and operational efficiency.

Companies Covered in Cinema Point of Sale (POS) Solutions Market

- NCR Corporation

- Vista Entertainment Solutions

- CenterEdge Software

- GDC Technology

- Ticketmaster

- Cinemark Holdings

- TicketSoft

- EnTelegra

- CineManager

- Movie Magic

- Cinedigm

- Screenvision

- Diamond Ticketing Systems

- Retriever Solutions

- Ardhas Technology

- Titan Technology

- OMNITERM

- Allure - A Christie Company

Frequently Asked Questions

The market is projected to reach US$ 3.0 billion by 2033 from US$ 1.5 billion in 2026.

Digital transformation and adoption of scalable cloud-based systems are the main drivers.

Membership and loyalty management is the fastest-growing application segment.

North America leads the market with about 42% share in 2025.

Expanding loyalty and membership programs offer the most significant opportunity.

Leading market players include NCR Corporation, Vista Entertainment Solutions, CenterEdge Software, GDC Technology, Ticketmaster, Cinemark Holdings, TicketSoft, EnTelegra, CineManager.