- Metals & Minerals

- Bismuth Market

Bismuth Market Size, Share, Trends, and Growth Forecast 2026 - 2033

Bismuth Market by Derivative Type (Oxides, Nitrates, Oxychloride, Subcarbonate, Aluminate), Application (Pharmaceuticals, Cosmetics, Industrial Pigments, Metallurgical Additives, Fusible Alloys), Regional Analysis, 2026 - 2033

Bismuth Market Size and Trend Analysis

The global bismuth market size is likely to be valued at US$ 512.4 billion in 2026 and projected to reach US$ 730.7 billion by 2033, growing at a CAGR of 5.2% between 2026 and 2033.

The market expansion is fundamentally driven by accelerating pharmaceutical demand for bismuth compounds as gastroprotective and antimicrobial agents, expanding cosmetics applications driven by consumer preference for non-toxic, eco-friendly ingredients, and growing metallurgical applications where bismuth replaces toxic materials like lead.

Rising global focus on sustainable manufacturing, stringent environmental regulations restricting lead usage, and the emergence of advanced bismuth-based technologies in electronics and renewable energy sectors are creating substantial growth opportunities.

Government initiatives promoting eco-friendly substitutes for hazardous materials and increasing investment in pharmaceutical research and development are propelling market momentum across developed and developing regions.

Key Market Highlights

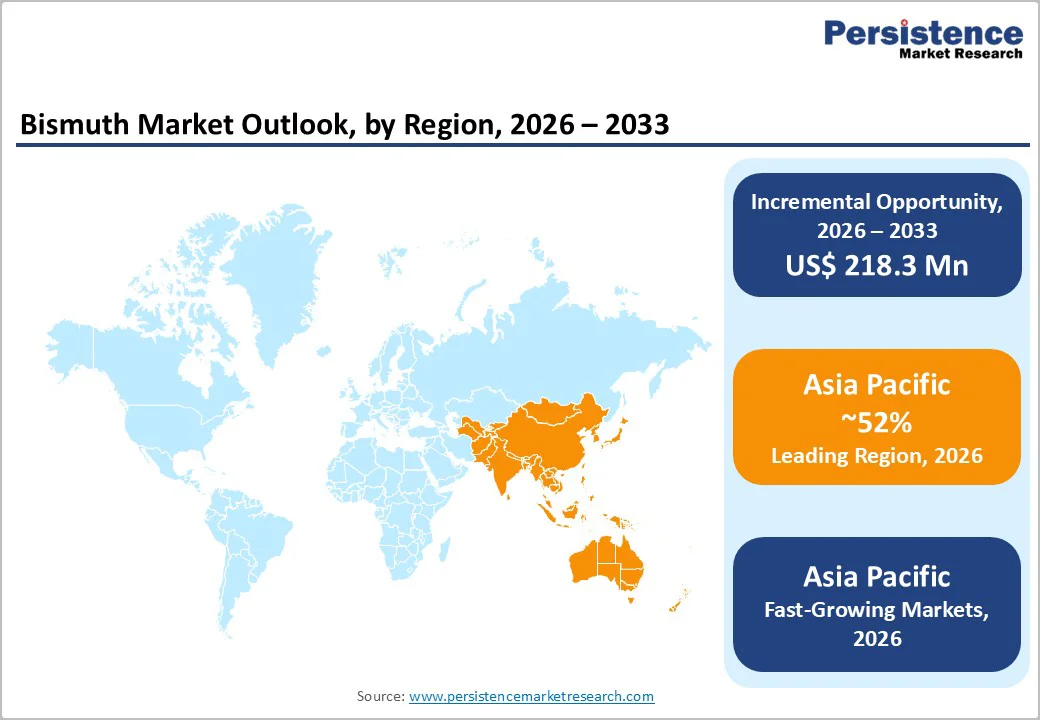

- Leading Region: Asia Pacific leads the global bismuth market with 52% share in 2025, driven by China’s industrial base, India’s growing pharmaceutical and cosmetics sectors, and Vietnam’s Nui Phao Mining supply.

- Fastest Growing Region: Asia Pacific is the fastest-growing market at a projected 7.2% CAGR through 2033, fueled by pharmaceutical and cosmetics demand, industrial bismuth adoption, and supportive government initiatives.

- Dominant Segment: Bismuth oxides hold a 42% market share in 2025, supported by applications in pharmaceuticals, pigments, ceramics, glass, and environmental remediation, and serving as precursors for other derivatives.

- Fastest Growing Segment: Pharmaceuticals are the fastest-growing application at 5.8% CAGR through 2033, driven by demand for gastrointestinal therapeutics, emerging markets’ production, and new antimicrobial applications.

- Key Market Opportunity: Regulatory restrictions on hazardous materials and sustainability trends offer growth potential for lead-free industrial uses and eco-friendly cosmetics applications of bismuth globally.

| Key Insights | Details |

|---|---|

| Bismuth Market Size (2026E) | US$ 512.4 Bn |

| Market Value Forecast (2033F) | US$ 730.7 Bn |

| Projected Growth CAGR (2026 - 2033) | 5.2% |

| Historical Market Growth (2020 - 2025) | 4.0% |

Market Dynamics

Driver - Pharmaceutical Industry Expansion and Gastrointestinal Health Applications

The pharmaceutical sector represents the largest and fastest-growing demand driver for bismuth compounds, primarily through applications in treating gastrointestinal disorders. Bismuth subsalicylate, recognized globally under the brand name Pepto-Bismol, has been prescribed for over 100 years and was first FDA-approved in 1939, with continued widespread over-the-counter availability in major markets.

According to the National Institutes of Health (NIH), bismuth therapy demonstrates efficacy against two major gastrointestinal disorders: peptic ulcer disease and diarrhea, with recent clinical studies showing that bismuth compounds combined with conventional antibiotics produce elimination of Helicobacter pylori, histological improvement, and symptom amelioration lasting longer than one year.

The American Gastroenterological Association reports that gastrointestinal conditions affect approximately 60-70 million Americans annually, with substantial portions seeking over-the-counter remedies, creating consistent demand for bismuth-based medications.

Traveler’s diarrhea affects over 50% of tourists in developing countries according to epidemiological data, with bismuth subsalicylate demonstrating superior efficacy compared to placebo in clinical trials involving 2,500+ patients, significantly reducing stool frequency and time to symptom relief.

Emerging pharmaceutical applications for advanced bismuth-based compounds in cancer therapeutics and antimicrobial resistance management are expected to generate substantial incremental demand through 2033.

Lead Substitution and Environmental Regulatory Compliance Driving Industrial Adoption

Environmental regulations restricting hazardous material usage are catalyzing substantial bismuth adoption across industrial sectors, particularly in replacing toxic lead in multiple applications.

Bismuth possesses critical properties making it ideal as lead substitute: non-toxic characteristics, favorable thermal properties with a melting point of 271°C, a unique expansion coefficient of 3.3% upon solidification, and an established safety profile in pharmaceutical and food processing applications.

The European Union’s Restriction of Hazardous Substances (RoHS) Directive and similar regulations in North America, Japan, South Korea, and emerging markets explicitly restrict lead in electrical and electronic components, driving manufacturers to adopt bismuth-based alternatives.

According to the Circular Rare Materials Alliance, bismuth is increasingly utilized in fusible alloys (28% of total uses), low-temperature solders, radiation shielding materials, and fishing weights as lead-free substitutes, with growing adoption in aerospace applications requiring specialized low-melting-point alloys for jet engine blade machining and cast pattern molds.

The U.S. Environmental Protection Agency (EPA) regulations on lead content in drinking water infrastructure have driven transition to bismuth-based alternatives in plumbing applications, with bismuth copper water pipes increasingly preferred in municipal and residential construction projects.

Research from the National University of Singapore demonstrates that bismuth-based low-melting eutectic alloys exhibit superior dimensional stability during solidification compared to legacy lead-based systems, providing technical justification for equipment upgrades and process reformulations.

Government procurement initiatives favoring eco-friendly materials in defense, aerospace, and infrastructure projects are further accelerating bismuth adoption across industrialized nations.

Restraint - Supply Chain Dependency and Bismuth Production Concentration Creating Market Constraints

The bismuth market faces significant supply constraints due to extreme geographic concentration and byproduct dependency characteristics. According to the United States Geological Survey (USGS), China dominates global bismuth refinery production with 82% market share in recent years, followed distantly by Laos and Republic of Korea, creating substantial concentration risk.

Bismuth production operates almost exclusively as a byproduct of lead, tungsten, fluorspar, and tin ore processing, meaning bismuth supply remains intrinsically dependent on primary metal production cycles beyond bismuth producers’ direct control.

Nui Phao Mining Company Limited in Vietnam, operated by Masan High-Tech Materials, represents the world’s largest dedicated bismuth-producing facility outside China as a global strategic asset producing tungsten, copper, and bismuth concentrates from its poly-metallic mine in Thai Nguyen Province.

Supply chain disruptions from geopolitical tensions affecting Chinese exports, environmental regulations impacting smelting operations, and resource nationalism policies in key producing regions create persistent market vulnerabilities.

Bismuth Price Dynamics

The global bismuth market has experienced notable price volatility in recent years, driven by supply constraints and rising industrial demand. According to the U.S. Geological Survey (USGS), average Rotterdam in-warehouse prices increased from approximately

US$ 3.89 per pound in January 2024 to US$ 6.29 per pound by October, resulting in a 2024 annual average of around US$ 5.30 per pound, marking a nearly 30% increase over 2023 and the highest level since 2018. In China, the world’s leading bismuth producer, 99.99% purity bismuth metal prices reached ¥100,000-110,000 per ton (approximately US$ 13,781-15,159 per ton) in early 2025, reflecting tightening domestic supply and export limitations.

These price trends are driven by growing industrial demand for bismuth as a non-toxic replacement for lead in automotive, electronics, and plumbing applications, alongside expanding pharmaceutical and cosmetic uses. Environmental regulations and competition for high-purity feedstock further contribute to upward pressure on global bismuth prices.

Opportunity - Cosmetics and Personal Care Expansion Through Non-Toxic Ingredient Demand

Growing consumer preference for non-toxic, natural, and eco-friendly cosmetics is driving substantial bismuth demand in the personal care sector, particularly through bismuth oxychloride applications.

Bismuth oxychloride (BiOCl) is extensively utilized in mineral makeup formulations, including face powders, foundations, bronzers, blush, and eye shadows due to its distinctive pearlescent appearance, plate-like crystal structure creating light-wave interference effects, and fine white powder texture providing shimmering and luminous finishes.

The global cosmetics market exceeds US$ 600 billion annually according to major industry tracking organizations, with the personal care market segment growing at 8% CAGR through 2032, particularly in the Asia Pacific.

Regulatory bodies, including the U.S. Food and Drug Administration (FDA) recognize bismuth oxychloride as safe for cosmetic use, with its inclusion in the FDA Color Additives Status List providing regulatory certainty that supports manufacturer adoption.

The European Cosmetics Regulation (EC 1223/2009) explicitly permits bismuth oxychloride in cosmetic formulations, with widespread adoption across European cosmetics manufacturers, particularly in Germany, France, Spain, and Italy.

Bismuth oxychloride also finds applications in paints and coatings where it provides distinctive visual effects, white pearlescent finishes, and enhanced aesthetics valued in automotive finishes, decorative coatings, and specialty paints. Premium skincare and color cosmetics segments specifically show accelerating bismuth oxychloride adoption due to consumer willingness to pay premiums for natural, non-toxic ingredients and superior aesthetic properties.

Aerospace and Defense Applications Driving Demand for Specialized Bismuth Alloys

Aerospace and defense sectors are generating expanding demand for advanced bismuth-based alloys with specialized properties unavailable from conventional materials.

Bismuth-based fusible alloys with low melting points are extensively utilized in aerospace manufacturing for specialized applications, including jet engine blade machining fixtures, cast pattern molds, and precision tooling requiring dimensional stability during solidification and minimal volume change during phase transitions.

The U.S. aerospace industry generates annual revenues exceeding US$ 230 billion according to the Aerospace Industries Association, with manufacturers continuously demanding advanced materials offering superior performance characteristics.

Bismuth’s unique property of expanding 3.3% upon solidification creates critical advantages in aerospace applications where conventional lead-based alloys exhibit volume contraction causing dimensional inaccuracies, compromising precision manufacturing tolerances.

Defense applications, including X-ray shielding in medical equipment, radiation protection systems, and specialized ordnance applications, increasingly rely on bismuth-based materials as toxicity-free alternatives to historical lead formulations.

Government defense spending globally exceeds US$ 2.4 trillion annually, according to Stockholm International Peace Research Institute (SIPRI), with procurement budgets increasingly incorporating sustainability and health-safety criteria favoring bismuth-based solutions.

NATO allied nations have implemented acquisition policies restricting hazardous material usage, creating standardized procurement requirements that advantage bismuth-based materials in military equipment manufacturing.

Category-wise Analysis

Derivative Type Insights

Bismuth oxides dominate the derivative segment with a 42% share in 2025, serving as the primary precursor for other bismuth compounds. Their thermal stability, refractive properties, and chemical versatility enable widespread industrial use in ceramics, glass, pigments, and cosmetics.

In pharmaceuticals, bismuth oxides are significant for synthesizing compounds such as bismuth subsalicylate used in gastrointestinal therapies. Emerging applications leverage their photocatalytic properties for environmental remediation, including water purification and pollutant degradation. With broad applicability across industries, bismuth oxides are projected to grow at 6.1% CAGR through 2033, outpacing other derivative types.

Application Insights

Pharmaceuticals are the leading application segment, accounting for 39% of the market in 2025, driven by widespread use of bismuth compounds in gastrointestinal therapies. Bismuth subsalicylate, derived from bismuth oxides, is globally used in hospitals and pharmacy channels for managing peptic ulcers and Helicobacter pylori infections.

Emerging research on bismuth nanoparticles and bismuth-peptide complexes supports antimicrobial and anti-cancer applications. Growth in India’s pharmaceutical sector at a 11% CAGR further boosts bismuth demand for generic drug manufacturing and exports. Pharmaceuticals are expected to maintain dominance through 2033, with a projected 5.8% CAGR.

Regional Insights

North America Bismuth Market Trends

North America represents a mature, technologically advanced bismuth market, with the United States leading due to extensive pharmaceutical and industrial demand. U.S. pharmaceutical manufacturers rely on bismuth compounds for over-the-counter gastrointestinal remedies, while aerospace and precision manufacturing sectors increasingly adopt bismuth-based fusible alloys and lead-free materials.

Regulatory frameworks, including FDA oversight of bismuth medicines and EPA lead-reduction mandates, further drive industrial adoption.

Canada contributes through domestic suppliers and government-backed eco-friendly initiatives, supporting consistent bismuth procurement for generic drug production and exports.

Cross-border trade harmonization under USMCA ensures standardized product quality and efficient commerce, while innovation hubs in California, Texas, and the Northeast are developing advanced bismuth-containing composites and materials for aerospace, defense, and high-tech industrial applications. Collectively, these factors position North America as both a major consumer and innovation leader in bismuth-based products.

Europe Bismuth Market Trends

Europe’s bismuth market is mature and highly regulated, accounting for roughly 18% of global share in 2025, with Germany leading due to its pharmaceutical, precision manufacturing, and automotive sectors. Bismuth compounds are widely used in gastrointestinal therapeutics, supported by a pharmaceutical market of approximately US$ 287 billion in 2024, and in industrial applications as lead substitutes aligned with EU RoHS and REACH regulations.

Cosmetic demand for bismuth oxychloride in France and Spain is growing due to consumer preference for non-toxic mineral makeup. Post-Brexit UK manufacturers are developing independent material sourcing strategies, emphasizing eco-friendly alternatives.

Research institutions such as ETH Zurich, University of Cambridge, and Max Planck Institute are advancing bismuth-based technologies in nanomaterials and environmental remediation. These regulatory and innovation-driven trends collectively make Europe a stable, high-value market with strong adoption of bismuth for pharmaceuticals, industrial alloys, and emerging applications.

Asia Pacific Bismuth Market Trends

Asia Pacific dominates the global bismuth market with a 52% share in 2025 and is the fastest-growing region at a projected 7.2% CAGR through 2033.

China leads consumption with 40% global share, supported by large-scale pharmaceutical manufacturing, cosmetics production, and industrial applications in electronics, automotive, and construction. Government policies, including Made in China 2025, encourage domestic extraction, high-purity compound production, and advanced materials development.

India is the fastest-growing market, driven by a 11% CAGR in pharmaceuticals and 10% CAGR in cosmetics, with demand for bismuth compounds in generic medications and mineral makeup formulations expanding rapidly.

Vietnam’s Nui Phao Mining facility supplies 8,000-10,000 tonnes annually, serving regional and global markets, while Japan maintains steady demand in electronics and precision manufacturing. Strong government support, industrial growth, and strategic production hubs position the Asia Pacific as the primary driver of global bismuth demand and innovation.

Competitive Landscape

The global bismuth market demonstrates a moderately consolidated structure, with a mix of multinational corporations and specialized regional producers competing primarily through product quality, technological differentiation, and geographic reach.

Leading players collectively hold around 60-65% market share, leveraging established distribution networks, long-standing customer relationships, and diversified product portfolios. Business strategies focus on high-purity and specialty bismuth compounds for pharmaceutical, electronics, and industrial applications, while regional producers exploit cost advantages and proximity to raw materials to serve domestic and export markets.

Companies increasingly emphasize regulatory compliance, supply chain integration, and innovation in derivative synthesis and applications. Additionally, emerging players in India and Southeast Asia are entering via contract manufacturing for pharmaceutical and cosmetic sectors, enhancing market accessibility and intensifying pricing competition.

Overall, the competitive landscape is shaped by a combination of technology-driven differentiation, quality positioning, and strategic expansion into emerging markets, positioning innovation and supply chain efficiency as key determinants of market success.

Key Market Developments:

- May 2025: A Hunan-based company, Hunan Shizhuyuan Nonferrous Metals Co., Ltd. won a bid for 1,000 metric tons of bismuth concentrate, securing the lot in two rounds of 500 tons each, a sign of renewed market interest.

Companies Covered in Bismuth Market

- Hunan Jinwang Bismuth Industry Co. Ltd

- Hunan Bismuth Co. Ltd

- Hunan Shizhuyuan Nonferrous Metals Co., Ltd.

- Hunan Huaxin Rare & Precious Metals Technologies Co., Ltd.

- Hunan YuTeng Nonferrous Metals Co., Ltd.

- Nui Phao Mining Company Limited

- Met-Mex Peñoles, S.A. de C.V.

- 5N Plus Inc.

- VIAVI Solutions Inc.

- BASF SE

- Xianyang Yuehua Bismuth Co., Ltd.

- Fortune Minerals

- Jinchuan Group Co. Ltd.

- Yunnan Tin Group Co. Ltd.

- China Bismuth High-Tech Co. Ltd.

- BiMetals Corp.

- Industrias Peñoles

- China Northern Rare Earth Group

Frequently Asked Questions

The global Bismuth Market is projected to reach US$ 730.7 million by 2033, growing at a CAGR of 5.2% from US$ 512.4 million in 2026.

Demand is driven by pharmaceutical uses, cosmetics applications, metallurgical replacements for toxic materials, regulatory restrictions on hazardous substances, and environmental remediation.

Bismuth oxides (Bi2O3) dominate with around 42% market share due to applications in pharmaceuticals, pigments, cosmetics, and environmental remediation.

Asia Pacific leads with about 52% market share, driven by China’s production, India’s pharmaceutical growth, and Vietnam’s Nui Phao Mining operations.

Opportunities include lead-free applications, cosmetics expansion, antimicrobial pharmaceuticals, advanced materials for electronics and renewable energy, environmental remediation, and emerging market growth.

Key players include 5N Plus Inc., BASF SE, Nui Phao Mining Company, Xianyang Yuehua Bismuth, Met-Mex Peñoles, Hunan Bismuth Co., and VIAVI Solutions Inc.