- Specialty & Fine Chemicals

- Zircon Coating Market

Zircon Coating Market Size, Share, and Growth Forecast, 2025 - 2032

Zircon Coating Market by Formulation Type (Solvent-Based Coatings, Water-Based Coatings, Solvent-Free Coatings), Application (Foundries & Refractories, Aerospace & Aviation, Automotive, Power Generation, Electronics & Industrial Equipment), Functionality (Thermal Barrier Protection, Corrosion Resistance, Wear Resistance, Electrical Insulation), and Regional Analysis for 2025 - 2032

Zircon Coating Market Share and Trends Analysis

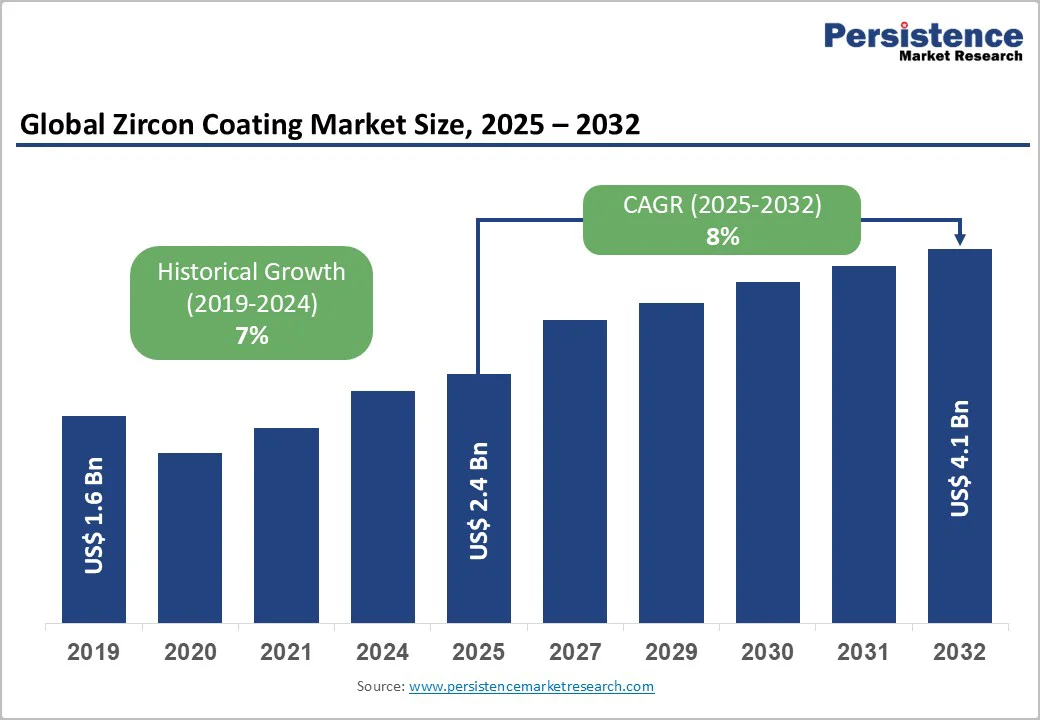

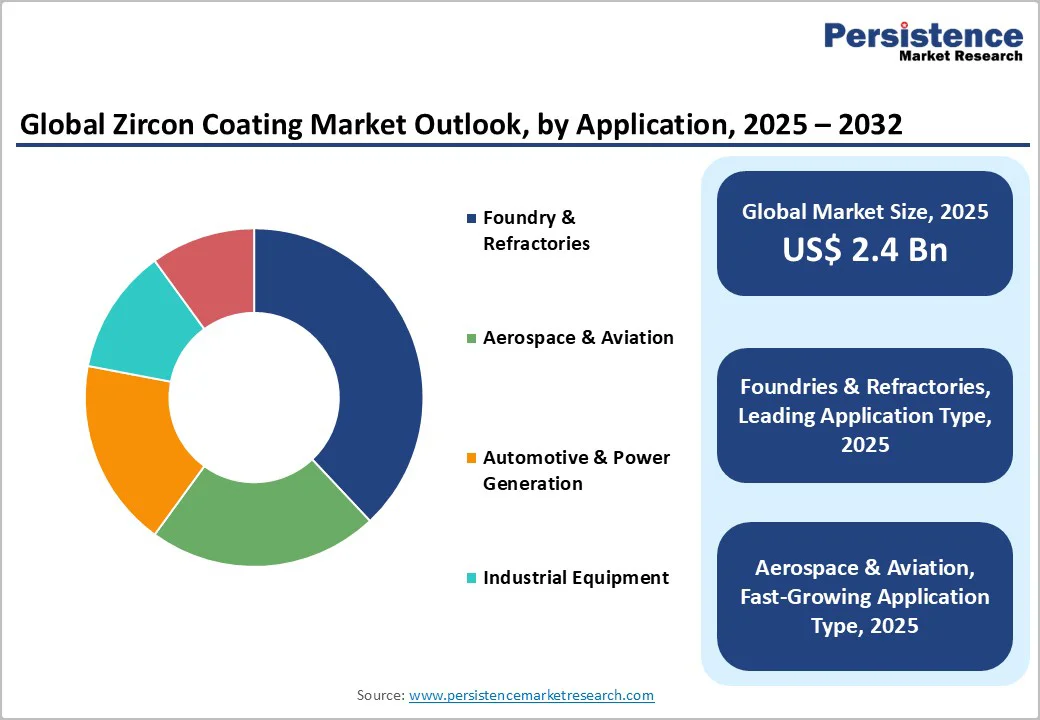

The global zircon coating market size is likely to be valued at US $ 2.4 billion in 2025, and is projected to reach US $ 4.1 billion by 2032, growing at a CAGR of 8% during the forecast period 2025-2032.

The growth is driven by rising demand for high-performance coatings in aerospace, automotive and industrial end markets, increasing regulatory pressure for durable and thermal resistant coatings, and expanding manufacturing capacity, particularly in Asia Pacific.

Key Industry Highlights

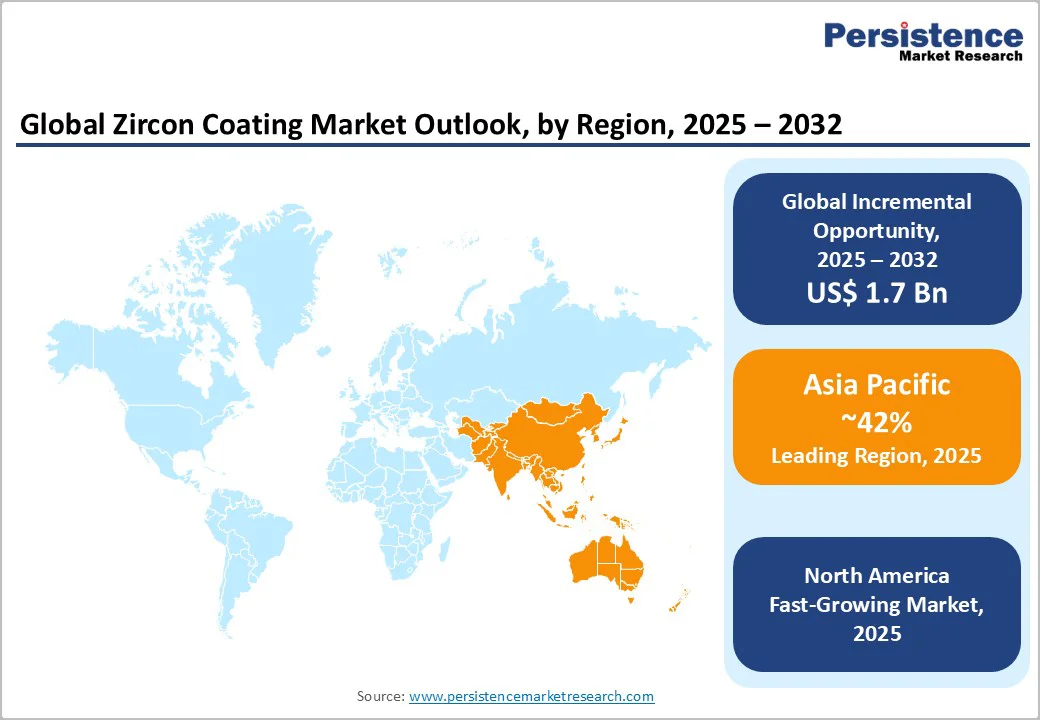

- Leading Region: Asia Pacific leads with a commanding 42% of the market share in 2025, driven by strong growth in foundry, ceramics, and aerospace manufacturing.

- Dominant Formulation Type: Solvent-based coatings hold nearly 60% of the revenue share in 2025, owing to their superior heat resistance, surface finish quality, and compatibility with industrial applications.

- Leading Application: The foundries & refractories segment accounts for around 38% of market revenue in 2025, driven by the widespread use of zircon coatings in metal casting, mold preparation, and high-temperature processing industries.

- Leading Functionality: Thermal barrier & corrosion resistance contributes over 45% of the total market demand, as manufacturers prioritize coatings that extend component life in high-temperature and corrosive environments.

- Key Driver: Rising demand for high-performance and heat-resistant coatings across aerospace, energy, and automotive sectors, along with growing adoption of zircon-based ceramics and refractories in industrial applications, mainly fuels the market.

- Growth Opportunity: Rapid shift toward eco-friendly and solvent-free zircon formulations, supported by stringent VOC regulations, and emerging applications in electronics, renewable energy systems, and advanced manufacturing, are opening high-value opportunities.

| Key Insights | Details |

|---|---|

|

Zircon Coating Market Size (2025E) |

US$ 2.4 Bn |

|

Market Value Forecast (2032F) |

US$ 4.1 Bn |

|

Projected Growth (CAGR 2025 to 2032) |

8.0 % |

|

Historical Market Growth (CAGR 2019 to 2024) |

7.0 % |

Market Factors – Growth, Barriers, and Opportunity Analysis

Strong Demand for High-Performance Industrial Coatings

The demand for zircon-based coatings is surging across aerospace, automotive, and power generation sectors due to their exceptional durability, heat resistance, and corrosion protection. These coatings enhance component longevity and operational efficiency, especially as industries shift toward lightweight materials and high-temperature applications. The global push toward electric vehicle manufacturing and advanced turbine technologies further boosts the adoption of zircon coatings for their superior thermal stability and oxidation resistance, making them indispensable in modern industrial processes.

Technological advancements in application methods such as plasma spraying and solvent-free formulations are revolutionizing zircon coating production by enhancing efficiency and consistency while reducing waste. Concurrently, stricter environmental regulations and volatile organic compound (VOC) limits are accelerating a shift to eco-friendly, low-emission zircon coating formulations. Manufacturers investing in sustainable, high-performance zircon solutions gain significant competitive advantages as industries prioritize green manufacturing and align procurement with sustainability goals.

Cost Pressures and Supply Chain Vulnerabilities

The zircon coating market growth faces significant cost challenges mainly driven by the high price of raw zircon materials and the complex processing techniques required for application. Advanced coating methods and rigorous quality control protocols further increase production expenses, making these coatings less accessible to cost-sensitive manufacturers or regions with limited industrial budgets. This cost barrier restricts broader market penetration, particularly in emerging markets where competitive pricing is crucial.

Furthermore, the market is also grappling with supply chain instability due to the geographic concentration of zircon mineral deposits, which introduces risks to consistent availability and price fluctuations. Competitive pressure is heightened by substitute materials, such as chromite and silica-based coatings, which offer acceptable performance at lower costs. These alternatives can limit the widespread adoption of zircon coatings, forcing manufacturers to innovate and optimize production to maintain market share in a highly competitive landscape focused on balancing performance, cost, and sustainability.

Expanding Industrialization and Manufacturing Growth in Asia Pacific

Asia Pacific is rapidly becoming the epicenter for zircon coating demand, driven by accelerated industrialization in China, India, and Southeast Asia. These markets experience strong activity across automotive, foundry, and construction sectors, where high-performance coatings are essential for durability and operational efficiency. Local availability of raw materials, coupled with cost-effective labor, enhances regional competitiveness and attracts global manufacturers to establish production facilities. Government-led infrastructure projects and robust foreign direct investment further stabilize long-term demand, creating substantial opportunities for capacity expansion and integrated supply chains.

Simultaneously, environmental concerns and regulatory tightening on VOCs are driving innovation towards eco-friendly zircon coatings, including water-based and solvent-free formulations. Manufacturers developing these sustainable products can achieve both high performance and compliance, appealing to increasingly environmentally conscious industries. Advanced multifunctional coatings offering thermal, electrical, and wear resistance are also opening new application fronts in electronics, aerospace, and renewable energy sectors. This convergence of sustainability requirements and advanced performance capabilities positions zircon coatings as a critical growth area with strong potential for next-generation, compliant formulations that align with global industrial trends.

Category-wise Analysis

Formulation Type Insights

Solvent-based zircon coatings continue to dominate the market, favored for their proven durability in high-temperature and heavy-duty industrial environments such as metal casting, power generation, and aerospace. Their seamless integration with existing coating systems and reliable protective properties under extreme conditions make them the preferred choice for many industrial applications. This established performance ensures their sustained market leadership despite emerging trends.

However, the market is progressively shifting toward water-based and solvent-free zircon coatings, stimulated largely by tightening environmental regulations and the global push for sustainability. These newer formulations reduce VOC emissions and enhance workplace safety, appealing to manufacturers committed to greener production without compromising on coating efficiency. This transition reflects a broader industry evolution balancing environmental responsibility with high-performance demands, positioning eco-friendly zircon coatings as critical growth drivers in coming years.

Application Insights

Zircon-based coatings remain essential in the foundry and refractory industries due to their ability to enhance mold surface smoothness, durability, and thermal stability during metal casting processes. These coatings protect molds and cores from high-temperature erosion, reduce casting defects, and extend mold lifespan, supporting consistent quality and efficient production. The demand from traditional foundry sectors continues to bolster overall market revenues, fueled by global infrastructure projects and automotive manufacturing growth.

Simultaneously, aerospace and aviation applications represent the fastest-growing segment in the zircon coatings market through 2032. The increasing requirements from these sectors for advanced thermal barrier coatings and oxidation-resistant layers in turbine blades and jet engine components are driving innovation and adoption. This emerging domain underscores the critical role played by zircon coatings in enhancing high-performance materials, positioning aerospace as a key frontier for market expansion fueled by ongoing advancements in coating technologies tailored for extreme operational environments.

Functionality Insights

Corrosion resistance and thermal barrier performance remain the cornerstone properties of zircon coating that are stoking their adoption across industries subjected to extreme heat, wear, and oxidative environments. These attributes make these coatings indispensable in sectors such as foundries, power generation facilities, and aerospace systems, where extending the longevity of critical components directly impacts operational efficiency and maintenance costs. By providing robust protection against harsh thermal cycling and corrosive exposure, zircon coatings help safeguard high-value equipment, enabling improved reliability and reduced downtime.

Beyond these fundamental functions, wear resistance and electrical insulation capabilities are gaining traction as key differentiators, especially amid advancements in renewable energy, electronics manufacturing, and precision industrial processes. The emergence of multifunctional zircon coatings that integrate thermal protection, mechanical durability, and electrical insulating properties is opening transformative opportunities across high-technology and sustainable industries. This evolution reflects a broader market shift toward coatings that not only protect but also enhance the performance of components in complex operating environments, positioning zircon coatings as a critical enabler of next-generation industrial innovations.

Regional Insights

North America Zircon Coating Market Trends

North America is the fastest-growing regional market for zircon coatings, driven by strong momentum in aerospace, defense, and advanced automotive manufacturing sectors. The United States leads in both innovation and application, leveraging a highly developed industrial base alongside stringent environmental and performance standards. This robust ecosystem supports widespread adoption of durable coatings across critical systems such as turbines, engines, and power components, ensuring operational excellence and regulatory compliance.

The competitive landscape in North America is marked by technologically advanced coating manufacturers and research collaborations, bolstered by rigorous regulatory oversight and a focus on sustainable manufacturing goals. Significant investments in automation, research and development, and local supply chain integration throughout the U.S. and Canada are accelerating market growth. Companies that emphasize localized production, high performance, and regulatory compliance are well-positioned to capture expanding opportunities in this premium, innovation-driven region, reinforcing North America's leadership as a hub for coating advancements.

Europe Zircon Coating Market Trends

The Europe zircon coating market is mature but continues to see steady growth, driven by strong automotive, aerospace, and industrial equipment sectors in key countries such as Germany, the U.K., and France. The region's stringent environmental regulations, including ECHA and REACH frameworks, are accelerating the shift toward eco-friendly, solvent-free coatings that align with Europe's ambitious sustainability goals. This regulatory focus ensures that zircon coatings not only meet performance standards but also comply with evolving environmental requirements, fostering innovation within the market.

While growth rates are moderate compared to emerging markets, the Europe market benefits from ongoing infrastructure upgrades and technology replacements that enhance market resilience and longevity. The competitive landscape includes specialized European coating manufacturers and active research partnerships aimed at advancing product compliance and innovation. Companies that emphasize regulation adherence, technical innovation, and region-specific customization are best positioned to strengthen their market presence and capitalize on Europe’s quality-focused and environmentally conscious zircon coating sector.

Asia Pacific Zircon Coating Market Trends

Asia Pacific remains the dominant regional market for zircon coatings in 2025, commanding the largest global share, powered by its vast foundry, ceramics, and electronics manufacturing sectors. China and India anchor this leadership with their abundant raw materials, lower production costs, and rapidly growing industrial ecosystems that favor the adoption of cost-effective coatings. Although market growth is stabilizing as these markets mature, strong infrastructure investments in renewable energy and advanced manufacturing continue to drive demand. Collaborative ventures between global and local manufacturers further strengthen the region's competitive landscape. Companies that develop localized production capacities and tailor coatings for high-volume, price-sensitive applications are well-positioned to sustain Asia Pacific’s market leadership.

The region’s dominance is further bolstered by government initiatives and foreign direct investment (FDI) that ensure long-term demand stability and provide opportunities for capacity expansion and supply chain integration. This robust industrial foundation, combined with strategic partnerships, enables stakeholders operating in Asia Pacific to leverage cost advantages and technological innovation, fostering a conducive environment for continued zircon coating market growth. As infrastructure and advanced industries expand, Asia Pacific's leadership in manufacturing zircon coatings will likely deepen, ensuring the region remains central to the global market’s future trajectory.

Competitive Landscape

The global zircon coating market landscape is characterized by the presence of several global material science leaders alongside a wide base of regional and mid-sized coating manufacturers. Major companies collectively account for an estimated 30–40% of total market share, while the rest is distributed among specialized firms that focus on niche industrial or functional applications.

Competition is largely shaped by technical capability, formulation innovation, and manufacturing scale. Companies with strong R&D foundations and expertise in high-performance material engineering hold a clear competitive advantage, particularly in sectors requiring precise thermal, corrosion, or wear resistance properties. At the same time, the diversity of players presents opportunities for strategic collaborations, technology licensing, and capability expansion, enabling firms to strengthen their position in both mature and emerging markets.

Key Industry Developments

- In November 2025, scientists at Tomsk Polytechnic University (TPU) developed advanced high-entropy ceramic coatings made from hafnium and zirconium carbides alloyed with aluminum, chromium, and tantalum, achieving exceptional oxidation resistance at 1100°C. This breakthrough addresses the longstanding oxidation limitations of traditional ceramic materials, enhancing their suitability for aviation and space applications.

- In May 2025, Nanoe acquired the Upryze Shock ceramic powder, a line of ultra-high-toughness zirconia-based material, from Saint-Gobain Zirpro, expanding its portfolio of advanced ceramic materials. This acquisition enhances Nanoe's capabilities in supplying high-performance ceramic powders for applications in sectors such as automotive, aerospace, and electronics, strengthening its position in the specialty materials market.

- In February 2025, Rimsa introduced Ecozir Sand, a premium zirconium silicate product designed for use in friction materials such as brake pads and clutches. Ecozir Sand offers enhanced thermal stability, wear resistance, and environmental benefits compared to traditional abrasives. This product aims to improve friction material performance while supporting sustainable manufacturing practices in the automotive and industrial sectors.

Companies Covered in Zircon Coating Market

- VITCAS

- Metal Aids®

- IVP LIMITED

- Vesuvius

- ZIRCAR Ceramics Inc.

- Bhartia Group

- Jyoti Ceramic

- Ceraflux India Pvt. Ltd.

- Saint-Gobain ZirPro

- Refcotec Refractory Coatings

- Tosoh Corporation

- Imerys Fused Minerals

- H.C. Starck GmbH

- Zircomet Limited

Frequently Asked Questions

The global zircon coating market is estimated to reach US$ 2.4 billion in 2025.

Expanding aerospace and automotive production, regulatory pressure for energy-efficient and long-life coatings, and rising industrial manufacturing activity in Asia Pacific are driving the market.

The market is poised to witness a CAGR of 8% from 2025 to 2032.

The rise of solvent-free and water-based zircon coatings, which are driven by environmental regulations, presents significant potential for sustainable product innovation and can open up new market opportunities.

Saint-Gobain ZirPro, Vesuvius PLC, AkzoNobel N.V., and PPG Industries Inc. are some of the key players in the market.