- Specialty & Fine Chemicals

- Ziegler-Natta Catalyst Market

Ziegler-Natta Catalyst Market Size, Share, and Growth Forecast, 2026 - 2033

Ziegler-Natta Catalyst Market by Product Type (Polyethylene (PE), Polypropylene (PP)), Application (Films, Wraps, Bottles, Containers), End-User (Packaging, Automotive, Construction), and Regional Analysis for 2026 - 2033

Ziegler-Natta Catalyst Share and Trends Analysis

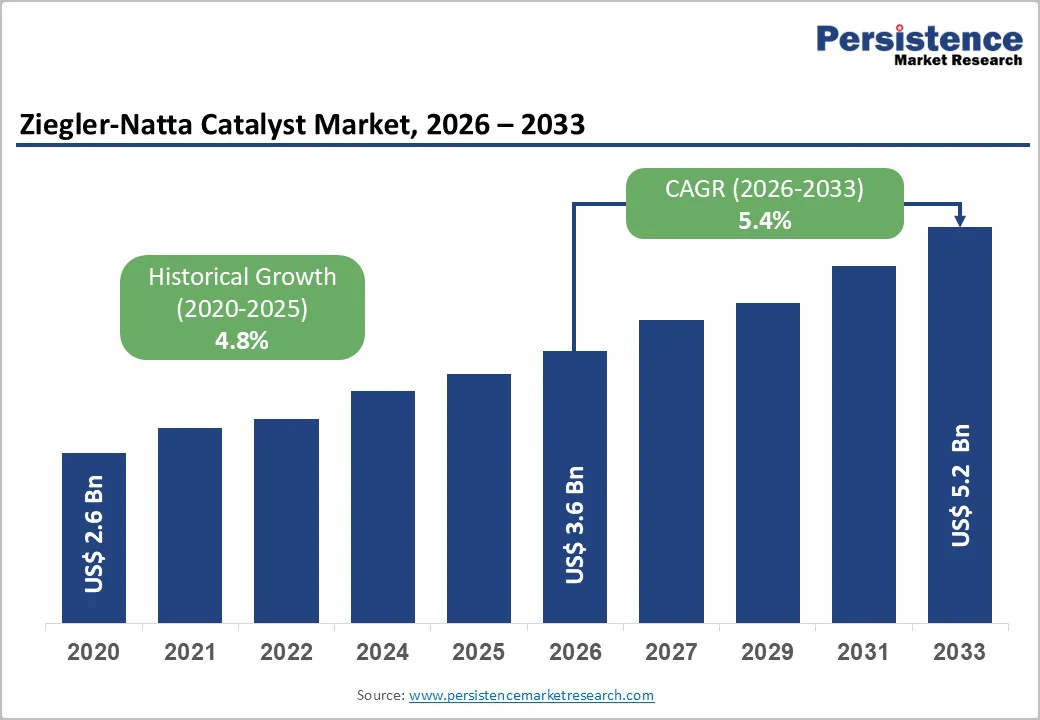

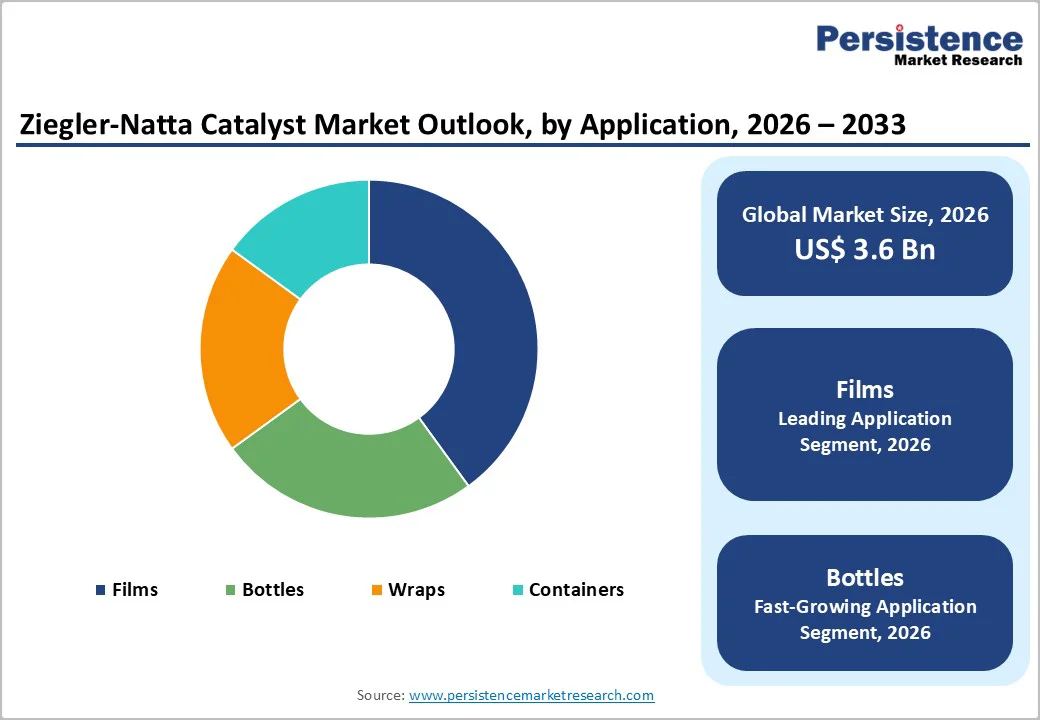

The global Ziegler-Natta catalyst market size is likely to be valued at US$ 3.6 billion in 2026 and is estimated to reach US$ 5.2 billion by 2033, growing at a CAGR of 5.4% during the forecast period 2026 - 2033.

Steadily rising polyolefin production for packaging, automotive, and construction applications drives this expansion. Capacity additions across Asia and the Middle East reinforce supply availability. Manufacturers increasingly emphasize lightweight, durable plastics and cost-efficient high-yield catalysts to optimize production economics, creating a sustained demand for advanced Ziegler-Natta systems that deliver superior performance.

Regulatory pressure for resource efficiency and lower emissions accelerates innovation toward higher-activity and more sustainable catalyst formulations. Policymakers and end-users demand solutions that reduce energy consumption and environmental impact. This shift compels suppliers to develop next-generation Ziegler-Natta technologies that maintain polymer quality while improving process efficiency.

Key Industry Highlights

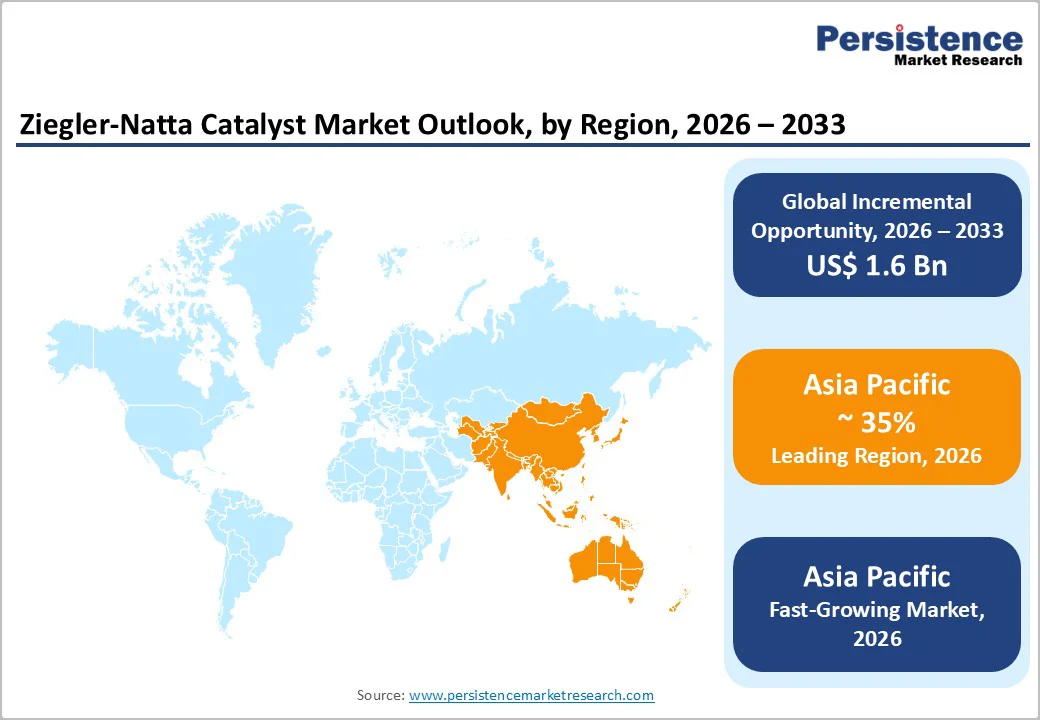

- Dominant Region: Asia Pacific is expected to command about 35% market share in 2026, supported by broad-based downstream consumption growth in packaging.

- Fastest-growing Regional Market: Asia Pacific is likely to be the fastest-growing market through 2033, driven by policy support and stringent regulations in China and India.

- Leading & Fastest-growing Product Types: Polypropylene is set to lead with an approximate 60% revenue share in 2026, while polyethylene is likely to grow the fastest from 2026 to 2033.

- Leading & Fastest-growing Applications: Films are slated to dominate with an approximate 40% share in 2026, whereas bottles are expected to be the fastest-growing segment between 2026 and 2033.

- Market Drivers: Expanding polyolefin demand in packaging and automotive reflects a broad shift toward lightweight, efficient materials that reduce cost and improve performance across supply chains.

- Market Opportunities: Ongoing innovation in Ziegler-Natta technology focuses on achieving higher catalyst activity, improved selectivity, and longer lifespans, directly improving polyolefin production.

| Key Insights | Details |

|---|---|

| Ziegler-Natta Catalyst Market Size (2026E) | US$ 3.6 Bn |

| Market Value Forecast (2033F) | US$ 5.2 Bn |

| Projected Growth (CAGR 2026 to 2033) | 5.4% |

| Historical Market Growth (CAGR 2020 to 2025) | 4.8% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Expanding Polyolefin Demand in Packaging and Automotive

Expanding demand for polyolefins in packaging and automotive reflects a broad shift toward lightweight, efficient materials that reduce costs and improve performance across supply chains.

Global consumption of polyethylene (PE) and polypropylene (PP) continues to rise as converters and brand owners replace heavier substrates such as glass and metal with polyolefin solutions for films, wraps, bottles, containers, and a wide range of automotive components.

In vehicles, plastics play a central role in light weighting, helping manufacturers meet fuel-efficiency and emissions targets by lowering overall vehicle mass while maintaining safety and design flexibility.

Ziegler-Natta catalysts remain the dominant technology for large-scale PP production and an important part of PE output, especially in commodity and mid-performance grades. This steady growth in resin volumes feeds directly into higher catalyst demand across integrated petrochemical complexes.

Long qualification cycles, process-license linkages, and the cost effectiveness of Ziegler-Natta systems reinforce this connection, creating a stable, volume-driven growth platform for catalyst suppliers as packaging and automotive plastics usage expands worldwide.

Environmental and Regulatory Pressure on Plastics

Environmental and regulatory pressure on plastics is reshaping demand for virgin polyolefin and, in turn, Ziegler-Natta catalysts, particularly in developed markets. Governments and international organizations increasingly regard current levels of virgin plastic production and use as unsustainable because of their contribution to carbon emissions, persistent waste, and marine pollution.

In response, they have introduced a growing set of policies that target plastic waste, single-use packaging, and lifecycle emissions. These measures encourage recycling, reuse, and material substitution, which slows the long-term growth of traditional polymer consumption and softens the outlook for virgin polyolefin demand.

This policy shift creates new strategic requirements and opportunities for catalyst suppliers. Stricter recyclability and recycled rules increase compliance complexity and introduce demand uncertainty that must be incorporated into capacity planning, utilization assumptions, and procurement strategies.

Suppliers that can demonstrate environmental benefits, support traceability, and collaborate with resin producers and brand owners on circular-economy objectives are better positioned to maintain relevance and margins as policy pressure on plastics intensifies.

Growing Emphasis on Innovation to Improve Catalyst Efficiency

Ongoing innovation in Ziegler-Natta technology is focused on achieving higher catalyst activity, better selectivity, and longer lifespans, which directly improves the polyolefin production. More active and durable catalysts allow producers to use smaller quantities per ton of polymer, extend reactor run times, and improve control over polymer properties.

This helps lower operating costs and energy consumption, making Ziegler-Natta systems more attractive to manufacturers that already rely on established PP and PE process technologies. In cost-sensitive commodity and mid-performance segments, such performance gains strengthen the position of Ziegler-Natta catalysts versus alternative systems.

At the same time, emerging markets in Asia Pacific, particularly China and India, are becoming major demand centers for polyolefin. Rapid industrialization and urbanization increase requirements for packaging, pipes, films, and molded parts used in housing, infrastructure, consumer goods, and mobility.

The construction sector needs durable piping, sheets, and geomembranes, while the expanding automotive industry uses polypropylene extensively in interiors, bumpers, and structural components.

Category-wise Analysis

Product Type Insights

Polypropylene is expected to be the leading segment, accounting for approximately 60% of the Ziegler-Natta catalyst market revenue share in 2026, as it combines considerably higher end-use demand with a strong technical and economic fit for the Ziegler-Natta technology.

PP is a core material in rigid packaging, such as containers, caps, and closures, as well as in automotive components, appliances, textiles, and other sectors that value low weight, chemical resistance, and good mechanical properties. Its global consumption is high and diversified across these sectors.

This broad, stable demand base ensures high, continuous PP throughput in polymerization plants, which directly translates into substantial, recurring catalyst requirements.

Polyethylene is likely to be the fastest-growing segment from 2026 to 2033, because it is tightly linked to rising demand for high-density polyethylene (HDPE) and linear low-density polyethylene (LLDPE) films and pipes in fast-developing economies.

Large-scale investments in construction, water infrastructure, and agriculture in regions such as Asia and the Middle East are driving strong consumption of PE films, geomembranes, and pressure pipes. At the same time, Ziegler-Natta PE catalysts continue to improve, supporting high-performance packaging.

Application Insights

Films are slated to be the dominant application with an approximate 40% market share revenue in 2026.

Polyethylene and polypropylene films are extensively used for food packaging, lamination, industrial wraps, agricultural covers, and e-commerce mailers, driving very high, continuous resin throughput and thus strong Ziegler-Natta-based demand. PE and PP films dominate because they combine low cost, processability, and good moisture-barrier performance, making them standard materials for pouches, bags, liners, laminates, and agricultural films.

Bottles are expected to be the fastest-growing segment between 2026 and 2033, since they are widely utilized for beverages, household chemicals, personal care, and selected food products. Rising consumption of packaged liquids and cleaning products in emerging markets, together with a shift from glass and metal to lighter, shatter-resistant plastics, is accelerating demand for polyolefin bottles.

As brands push for recyclable, lightweight formats that run efficiently on existing filling lines, HDPE and PP bottles continue to gain share, driving above-average growth in both resin consumption and associated Ziegler-Natta catalyst usage.

End-User Insights

Packaging is projected to remain the leading application segment, capturing around 55% of the market in 2026 as polyolefin use expands across consumer goods, food packaging, logistics, and e-commerce. This dominance reflects heavy reliance on high-volume polymers manufactured using Ziegler-Natta catalysis, which supports consistent quality and cost-effective large-scale production.

As supply chains modernize, companies increasingly prioritize protective, durable, and lightweight packaging formats that safeguard products during transport and extend shelf life. A practical implication for value-chain participants is the need to align material portfolios and catalyst capabilities with brands’ expectations for performance, recyclability, and regulatory compliance.

Automotive applications are expected to deliver the fastest growth over the 2026 - 2033 period, as manufacturers accelerate the shift from metal to lightweight polymer components to improve efficiency and meet emissions targets. Polypropylene stands out for its versatility, supporting interior trims, battery housings, and under-the-hood parts where heat resistance and mechanical strength are critical.

Tightening efficiency and emissions standards across Europe and Asia encourage deeper penetration of advanced PP formulations that balance weight reduction with durability and safety. For catalyst and material suppliers, this creates a clear opportunity to co-develop precision PP grades with automakers, focusing on processability, long-term stability, and compatibility with emerging electric vehicle architectures.

Regional Insights

Asia Pacific Ziegler-Natta Catalyst Market Trends

Asia Pacific is positioned to lead the polyolefin catalyst market revenues, with an estimated 35% share in 2026, driven by the region’s status as the world’s largest polyolefin production hub. The region’s strong downstream demand spans packaging, automotive, construction, textiles, and consumer goods, all of which rely on large-scale, cost-effective polyolefin manufacturing.

China, India, Japan, and ASEAN countries have built extensive integrated petrochemical complexes powered by low-cost feedstock sources, competitive labor, and supportive government policies. These capabilities supply a rapidly growing manufacturer base that supports urbanization, e-commerce, and infrastructure development, ensuring sustained investment in high-activity PP and PE catalysts, including Ziegler-Natta systems.

Alongside capacity growth, policy initiatives and stricter regulations in China and India are shifting catalyst selection toward advanced Ziegler-Natta technologies. Chinese government programs are prioritizing the localization of high-end polyolefin and catalyst technologies, with significant investments in new polyolefin and elastomer plants designed around domestically developed catalyst platforms.

This strategy is reducing reliance on imports and expanding the regional market for advanced Ziegler-Natta formulations. As a result, suppliers in Asia Pacific are well positioned to capture both domestic and export opportunities, supported by a dynamic ecosystem of innovation, regulatory alignment, and long-term industrial growth.

Europe Ziegler-Natta Catalyst Market Trends

Europe exerts strong influence in the Ziegler-Natta catalyst market since it pairs an established polyolefin industry with stringent policy and deep research & development (R&D) capability. Germany, the United Kingdom, France, and Spain combine large resin producers, automotive original equipment manufacturers (OEMs), and packaging converters with universities and industrial research centers that focus on higher-performance and more sustainable polymer grades.

The European Union (EU) Green Deal and circular economy priorities push the plastics value chain to lower carbon intensity, improve recyclability, and limit hazardous substances, which raises performance expectations for catalyst selection in polypropylene and polyethylene production.

For suppliers, this environment favors offerings that deliver tight property control, support design-for-recycling goals, and reduce compliance risk across multiple end markets such as mobility and packaging.

The EU is also tightening harmonized requirements for plastics, recycling, and waste management, including minimum recycled-content rules for packaging and other uses. These measures encourage Ziegler-Natta and hybrid catalyst systems that preserve product consistency when producers increase recycled feedstock usage, especially where variability can degrade process stability or end-use performance.

Companies can strengthen positioning by validating catalyst performance across a range of recycled input quality, then aligning grade development with mechanical and chemical recycling pathways to protect margins and accelerate customer qualification cycles.

North America Ziegler-Natta Catalyst Market Trends

North America maintains a prominent position in the Ziegler-Natta catalyst market, anchored by the efficient polymer production infrastructure, feedstock cost advantages, and downstream innovation in the U.S.

The regional market benefits from abundant, low-cost natural gas liquids derived from shale development, which supports economical, large-scale manufacturing of PE and PP, which are heavily dependent on the Ziegler-Natta technology.

Robust demand from major end-use sectors such as packaging, automotive, and consumer goods reinforces this foundation, as manufacturers rely on consistent polyolefin supply for flexible films, rigid containers, and lightweight vehicle components.

Competitive dynamics reflect the dominance of multinational chemical producers, integrated petrochemical complexes, and technology licensors with extensive R&D resources and established supply partnerships. Investment activity remains centered along the U.S. Gulf Coast, where companies are expanding capacity, modernizing facilities, and advancing catalyst technologies to enhance operational efficiency and material performance.

This regional ecosystem supports the development of specialized catalyst grades tailored to evolving market needs, such as improved stiffness-impact balance or enhanced processability. These elements solidify North America’s strategic role in the global market and ensure steady, long-term demand for high-performance Ziegler-Natta catalyst systems.

Competitive Landscape

The global Ziegler-Natta catalyst market structure exhibits moderate consolidation, with leading companies such as LyondellBasell Industries Holdings B.V., W. R. Grace & Co., Clariant AG, and Mitsui Chemicals, Inc. collectively commanding roughly 50% of the total market share.

These established players leverage extensive manufacturing scale, proprietary catalyst formulations, and global distribution networks to serve high-volume polyolefin producers across packaging, automotive, and industrial applications.

Continuous innovation remains central to competitive positioning, as firms develop next-generation systems that enhance polymer yield, narrow molecular weight distribution, and support sustainable feedstock without sacrificing process economics.

Strategic partnerships, mergers, and acquisitions define the landscape, enabling companies to broaden technology portfolios and penetrate new regional markets. Emerging startups introduce specialized solutions focused on niche performance attributes, such as improved recyclability or bio-based compatibility, which intensify pressure on incumbents to accelerate R&D investment.

For market participants, success hinges on balancing breakthrough innovation with reliable supply chain execution, as end-users increasingly prioritize catalysts that deliver measurable gains in efficiency, regulatory compliance, and lifecycle environmental impact.

Key Industry Developments

- In October 2025, Mitsui Chemicals acquired all shares of Nippon Aluminum Alkyls (NAA) from Ketjen, making NAA a wholly owned subsidiary to strengthen its position in organometallics such as alkyl aluminum, which are used as co-catalysts for polyolefins, synthetic rubber, pharmaceuticals, and electronic materials.

- In March 2025, LyondellBasell announced the launch of Pro-fax EP649U, a new polypropylene impact copolymer aimed at the rigid packaging market. The grade is formulated for thin-walled injection molding, offering high flow, fast crystallization, efficient mold release, and good impact and stacking strength, all important for packaging applications.

- In March 2025, SIBUR announced plans to start construction of Russia's first polymerization catalysts plant in Q2 2025, producing over 1,000 tons annually of chromium, metallocene, and titanium catalysts for polyethylene and polypropylene to achieve technological independence amid projected polymer output doubling to over 15 million tons by 2030.

Companies Covered in Ziegler-Natta Catalyst Market

- LyondellBasell Industries Holdings B.V.

- W. R. Grace & Co.

- Clariant AG

- Albemarle Corporation

- BASF SE

- Evonik Industries AG

- Dow Chemical Company

- AkzoNobel N.V.

- INEOS Group

- Mitsui Chemicals, Inc.

- Sinopec

- Sumitomo Chemical Co., Ltd.

- Hanwha Total Petrochemical

- Japan Polypropylene Corporation

Frequently Asked Questions

The global Ziegler-Natta catalyst market is projected to reach US$ 3.6 billion in 2026.

Soaring polypropylene and polyethylene demand in packaging, automotive, and consumer goods, supported by high-activity, cost-effective catalyst technology, is driving the market.

The market is poised to witness a CAGR of 5.4% from 2026 to 2033.

Key opportunities include advanced catalysts for lightweight, recyclable plastics, specialty polymers, and rapid polyolefin capacity growth in Asia Pacific and the Middle East.

LyondellBasell Industries Holdings B.V., W. R. Grace & Co., Clariant AG, and Mitsui Chemicals, Inc. are some of the key players in the market.