- Oil & Gas

- Xenon Gas Market

Xenon Gas Market Size, Trends, Share, and Growth Forecast, 2025 - 2032

Xenon Gas Market by Supply Mode (Cylinders, On-Site, Bulk & Micro Bulk, and Drum Tank sand), Industry (Healthcare, Electrical & Electronics, Aerospace & Aircraft, Automotive & Transportation, Manufacturing Processes, Construction, and Others), and Regional Analysis for 2025 - 2032

Xenon Gas Market Size and Trends Analysis

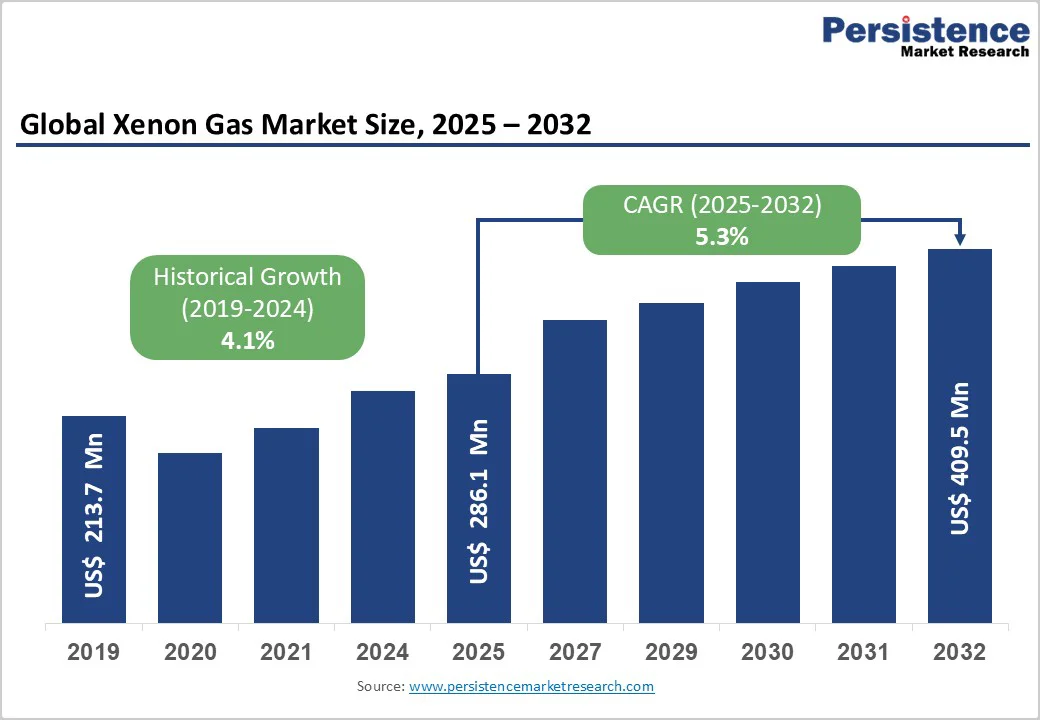

The global xenon gas market size is likely to value at US$ 286.1 million in 2025 and is projected to reach US$ 409.5 million, growing at a CAGR of 5.3% between 2025 and 2032.

Driven by rising demand across healthcare and electronics, expanding aerospace applications, and technological advancements in cryogenic gas production, the market demonstrates resilient growth.

Key Industry Highlights:

- Worldwide healthcare spending surpassed US$ 9.8 trillion in 2024, significantly increasing demand for xenon-based medical imaging and diagnostic technologies.

- The healthcare sector dominates xenon gas consumption, contributing over 30% of global revenue in 2025, primarily due to its use in MRI imaging, anesthesia, and respiratory diagnostics.

- The electrical and electronics segment is the fastest-growing end-use category, forecast to expand at a 7.5% CAGR through 2032, driven by semiconductor fabrication and display manufacturing.

- Global healthcare spending surpassed US$ 9.8 trillion in 2024, significantly boosting demand for xenon-based diagnostic and imaging technologies.

- The global semiconductor industry, valued at over US$ 600 billion in 2024, fuels xenon demand for EUV lithography, ion propulsion, and plasma etching processes.

- Xenon remains a high-cost specialty gas, often priced above US$ 100 per liter, due to its extremely low atmospheric concentration and complex extraction requirements.

- Air Liquide and Messer are strengthening their market leadership through large-scale investments in ultra-pure gas facilities and cryogenic purification technologies.

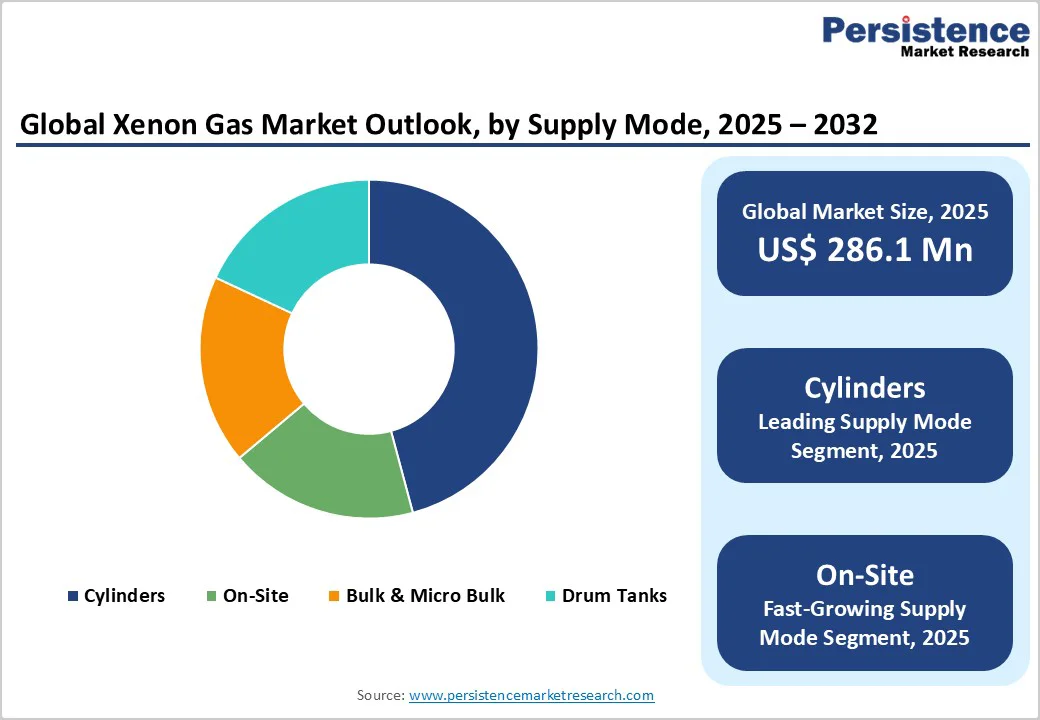

- On-site xenon generation systems are gaining traction, expected to account for up to 28% of global supply by 2032, reducing logistics costs and ensuring consistent gas purity.

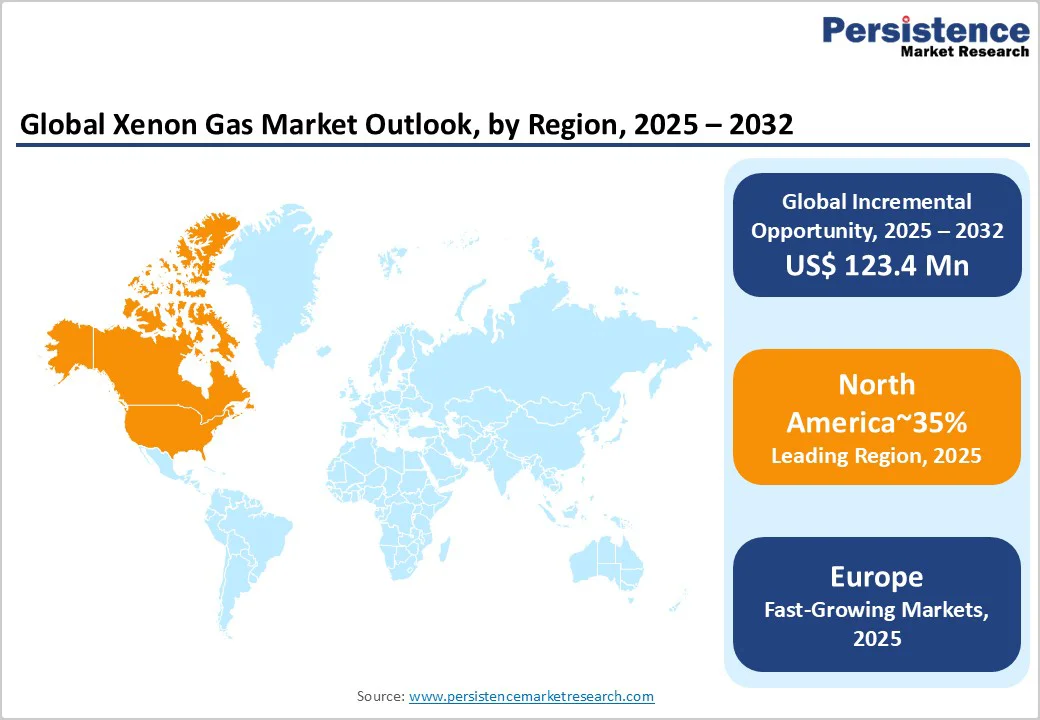

- North America leads the global market with over 35% share in 2025, driven by advancements in healthcare, aerospace, and semiconductor manufacturing.

- Europe is the fastest-growing regional market, supported by strict EU quality standards, technological innovation, and investments in high-purity gas facilities.

- The global xenon gas market remains moderately consolidated, with leading suppliers controlling over 65% of total volume through forward integration, R&D, and strategic geographic expansion.

| Key Insights | Details |

|---|---|

| Xenon Gas Market Size (2025E) | US$ 286.1 Mn |

| Market Value Forecast (2032F) | US$ 409.5 Mn |

| Projected Growth (CAGR 2025 to 2032) | 5.3% |

| Historical Market Growth (CAGR 2019 to 2024) | 4.1% |

Market Dynamics

Drivers - Healthcare Expansion and Diagnostic Innovation

The Xenon gas market benefits significantly from its pivotal role in medical diagnostics, notably magnetic resonance imaging (MRI) and anaesthesia applications. With healthcare expenditure rising globally, exceeding US$ 9.8 trillion in 2024 according to the World Health Organization, the adoption of advanced imaging modalities is accelerating.

Xenon’s bio-inert nature enables the development of non-invasive diagnostic tools. As medical device manufacturers enhance imaging resolution and safety protocols, demand for ultra-high purity xenon surges, supporting annual growth rates above 6% in healthcare end use. Strategic collaborations between gas suppliers and medical device OEMs continue to drive application expansion and market penetration.

Technological Advancements and Semiconductor Industry Growth

Rapid developments in the electronics and semiconductor sectors act as a growth catalyst; xenon is critical for plasma etching, ion propulsion, and insulative coating processes. In 2024, the semiconductor market exceeded US$ 600 billion and is forecast to grow at 7%+ CAGR through 2030 (SEMI, World Semiconductor Trade Statistics).

The advent of EUV lithography and increased chip miniaturization necessitate higher purity xenon, underpinning substantial procurement agreements. Recent investments, such as Air Liquide’s ultra-pure gas facility announced in 2024, have reinforced market potential within electronics and space industries.

Restraint - High Production Costs, Supply Chain Vulnerability, and Regulatory Constraints

Xenon gas production is inherently complex and energy-intensive, requiring advanced cryogenic air separation and purification systems. The extraction yield is extremely low only a few parts per billion in the atmosphere making xenon one of the most expensive rare gases, with costs often exceeding US$ 100 per liter.

These high production costs significantly limit adoption beyond premium applications such as medical imaging, aerospace propulsion, and semiconductor lithography. Additionally, the market is highly exposed to supply chain disruptions and price volatility, as xenon availability depends heavily on global natural gas output and the operation of air separation units (ASUs) in the petrochemical sector.

Any slowdown in these upstream industries can create sharp fluctuations in xenon supply and pricing.

Moreover, strict regulatory and environmental frameworks further intensify market challenges. Compliance with purity and safety standards established by agencies such as the U.S. Food and Drug Administration (FDA) and the European Medicines Agency (EMA) imposes high operational and testing costs on suppliers.

Environmental regulations aimed at reducing carbon emissions also compel producers to adopt cleaner, more energy-efficient processes and transport systems, thereby raising the overall cost base. Collectively, these factors create significant barriers for smaller manufacturers, restraining large-scale market expansion and sustaining xenon’s status as a niche, high-value industrial gas.

Opportunities - Emerging Technologies, On-Site Supply Expansion, and Policy Incentives Driving Xenon Market Growth

Emerging technologies and supportive policies are creating new growth avenues for the xenon gas market. Breakthroughs in quantum computing and advanced medical diagnostics are expanding xenon’s role in high-precision applications such as photon detection systems and optically pumped magnetometers, expected to unlock US$ 40-60 million in additional demand by 2032.

Major OEMs are developing specialized xenon gas blends and delivery systems to meet research and equipment manufacturing needs.

At the same time, the rise of on-site gas generation and micro-bulk supply systems notably in Asia-Pacific and Eastern Europe is reshaping delivery models with faster setup, lower logistics costs, and reduced carbon footprints. These systems could capture up to 28% of global market share, adding more than US$ 115 million in new revenue streams by 2032.

Additionally, policy incentives such as Europe’s Hydrogen Valley initiatives and the U.S. CHIPS Act are promoting semiconductor and specialty gas industries. Such government-backed programs and tax benefits may generate another US$ 45 million in market value, driving Xenon’s integration into advanced industrial ecosystems.

Xenon Gas Market Insights and Trends

Supply Mode Insights

The cylinders segment remains the leading supply mode in the global xenon gas market, accounting for over 55% of total revenue share in 2025. Their dominance is attributed to their ease of transportation, standardized safety design, and broad compatibility across end-user sectors such as healthcare, research laboratories, and aerospace applications.

Cylinder-based distribution systems are preferred by hospitals and laboratories for their portability and regulated flow control. In addition, suppliers are focusing on enhancing cylinder technology through improved valve sealing mechanisms, advanced materials for corrosion resistance, and tighter impurity control all of which contribute to superior reliability and gas purity levels during storage and use.

Conversely, the on-site generation segment is emerging as the fastest-growing category, projected to register a positive CAGR between 2025 and 2032. This growth is primarily driven by increasing adoption among industrial and electronics manufacturers seeking uninterrupted xenon supply with consistent purity.

On-site systems eliminate dependency on external cylinders or bulk deliveries, thereby reducing downtime and transportation costs. Furthermore, technological advancements in cryogenic air separation units, automated quality monitoring systems, and energy-efficient purification processes are strengthening the economic and operational viability of on-site generation models.

As a result, the segment is expected to play a crucial role in reshaping xenon gas supply strategies in the coming years.

Industry Insights

Healthcare Dominates Xenon Gas Consumption While Electrical & Electronics Segment Emerges as the Fastest-Growing Industry

The healthcare sector remains the leading end-use segment in the xenon gas market, accounting for over 30% of total revenue share in 2025. This dominance is driven by strong demand for xenon in MRI imaging, anesthesia, and respiratory diagnostics, where its inert and non-toxic properties are highly valued.

The ongoing expansion of healthcare infrastructure globally, coupled with regulatory approvals for xenon-based medical technologies, continues to sustain robust market growth. Rising medical research activities and the adoption of advanced imaging modalities further reinforce the healthcare sector’s position as the primary consumer of xenon gas.

Conversely, the electrical and electronics industry represents the fastest-growing segment, expected to register an impressive CAGR of around 7.5% through 2032. Growth in this sector is fueled by escalating demand from semiconductor fabrication, flat panel display manufacturing, and chip packaging processes, where xenon is essential for plasma etching, ion propulsion, and lithography applications.

OEM partnerships, the expansion of regional semiconductor fabs, and the requirement for ultra-high purity process gases are accelerating xenon consumption across Asia-Pacific and North America. This segment’s rapid expansion underscores its strategic importance in the evolving high-tech and digital manufacturing landscape.

Regional Insights and Trends

North America Dominates the Global Xenon Gas Market Driven by Advanced Healthcare, Electronics, and Aerospace Developments

North America leads the global xenon market, capturing more than 35% share in 2025. The U.S. remains the hub for advanced healthcare, electronics, and aerospace developments, fueling sustained demand for ultra-high purity xenon. Robust regulatory frameworks by agencies such as the FDA and EPA, combined with a strong innovation ecosystem, reinforce market leadership.

Key investments such as Messer’s 2024 acquisition of federal helium assets and operational expansion in Amarillo, Texas strengthen regional supply chains and technical capabilities. Investment flows target both traditional gas production and next-generation applications, with market concentration favoring established providers.

Europe Strengthens its Position as the Fastest-Growing Hub for Xenon Gas Through Regulatory Alignment and Technological Advancements

Europe emerges as the fastest-growing region, led by high-value markets in Germany, France, and the United Kingdom. The region’s harmonized regulatory environment, underpinned by strict EU safety standards, supports consistent quality and traceability. Air Liquide’s development of a high-purity krypton and xenon facility in Cheonan demonstrates the continent’s commitment to technological advancement and industry innovation.

Spain and Eastern European countries are also investing in microbulk and on-site generation facilities, leveraging cost advantages and favorable policy frameworks. Competitive dynamics reflect gradual consolidation, with leading players expanding geographic reach amidst rising import and export activity.

Competitive Landscape

The xenon gas market remains moderately consolidated, with established global leaders and a few regional specialists holding the majority share. Leading suppliers control more than 65% of the overall market volume. Competitive positioning centers on advanced cryogenic technologies, scalable production and distribution, and relentless focus on quality and regulatory compliance.

Market leaders emphasize innovation in cryogenic purification, strategic geographic expansion, and cost leadership across supply chains. Reliance on forward integration and proprietary technology platforms allows providers to maintain differentiation, while emerging business models accelerate the adoption of on-site supply solutions and service-based contracts.

Key Industry Developments:

- April 2024: Air Liquide (France) began constructing a state-of-the-art krypton and xenon purification plant in Cheonan, South Korea. The plant, due for completion in 2025, will produce ultra-high purity gases for semiconductor and space applications, advancing the company’s position in the extreme cryogenics segment.

- February 2024: Air Liquide deployed 62 new small gas production units in the industrial merchant and electronics sectors, responding to surging demand and introducing tailored solutions for continuous supply and reduced emissions in key markets.

- February 2024: Messer (Germany) became the preferred bidder for the U.S. Federal Helium Assets, with operational control of the Cliffside Gas Plant in Amarillo, Texas. This move consolidates Messer’s U.S. footprint and reinforces its supply credentials in mission-critical sectors.

Companies Covered in Xenon Gas Market

- Air Liquide

- Linde plc

- Air Products and Chemicals, Inc.

- Messer Group

- Iceblick Ltd.

- Proton Gases (India) Pvt. Ltd.

- Coregas Pty Ltd.

- Matheson Tri-Gas, Inc.

- Electronic Fluorocarbons LLC

- American Gas Products (AGP LLC)

- RasGas Company Limited

- Bhuruka Gases Ltd.

- Buzwair Industrial Gases Factories

- Dubai Industrial Gases Co LLC

- Gulf Cryo Holding C.S.C.

- Iwatani Corporation

- Praxair, Inc.

- Taiyo Nippon Sanso Corporation

- Mitsui Chemicals, Inc.

- Showa Denko K.K.

- Other Market Players

Frequently Asked Questions

The Xenon Gas market is estimated to be valued at US$ 574.4 Mn in 2025.

The primary demand driver for the Xenon Gas market is the rising popularity of outdoor living and entertainment spaces. Homeowners, resorts, and restaurants are increasingly investing in aesthetic and functional outdoor décor to enhance ambiance and create inviting social environments.

In 2025, the North America region will dominate the market with an exceeding 35% revenue share in the global Xenon Gas market.

Among placements, Standing holds the highest preference, capturing beyond 45% of the market revenue share in 2025, surpassing other placements.

LAMPLIGHT FARMS INC., Fire Fly Fuels, Inc., Burnaby Manufacturing Ltd, blomus, H POTTER, and Desert Steel are a few leading players.