- Industrial Machinery

- Winches Market

Winches Market Size, Share, and Growth Forecast, 2026 – 2033

Winches Market by Operation (Manual, Hydraulic, Pneumatic, Electric), Pulling Capacity (Below 2000 lbs., 2000–4000 lbs., 4000–8000 lbs., 8000–12000 lbs., 12000–16000 lbs., 16000–20000 lbs., 20000–40000 lbs., 40000–80000 lbs., Above 80000 lbs.), Application (Military, Commercial Recovery, Work Boat, Mobile Crane, Utility, Others), and Regional Analysis for 2026-2033

Winches Market Share and Trends Analysis

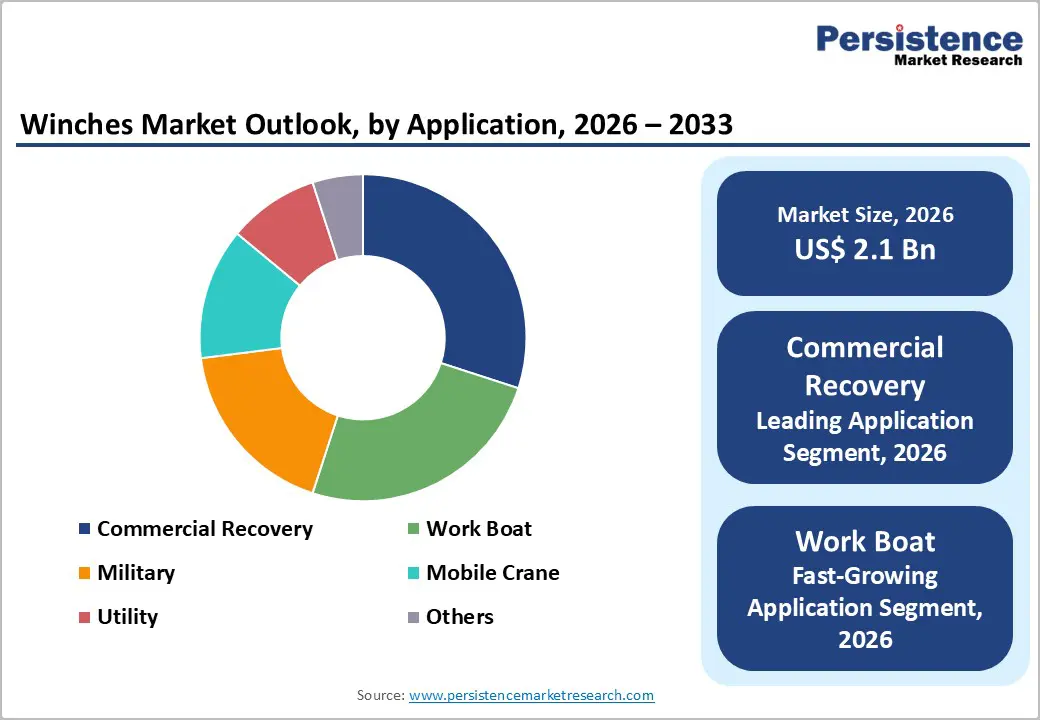

The global winches market size is likely to be valued at US$ 2.1 billion in 2026, and is projected to reach US$ 2.8 billion by 2033, growing at a CAGR of 4.2% during the forecast period 2026−2033.

The market trajectory reflects expanding industrial mechanization requirements across marine, construction, utility, and defense environments where controlled lifting and pulling functions are mission-critical. Growth momentum is primarily driven by rising infrastructure modernization, increased adoption of mechanized material-handling systems, and sustained capital expenditure in maritime logistics and offshore operations. Urban expansion and industrial automation initiatives are translating into higher demand for reliable load-handling equipment capable of ensuring operational safety and productivity continuity.

Technology integration remains a central catalyst, as digitally enabled winching systems improve precision control, reduce operational downtime, and enhance workforce safety compliance. Regulatory emphasis on occupational safety standards across construction, mining, and port operations is accelerating replacement cycles for legacy manual systems. Integration of electric and hydraulic systems supports operational efficiency while aligning with energy optimization mandates across industrial settings.

Key Industry Highlights

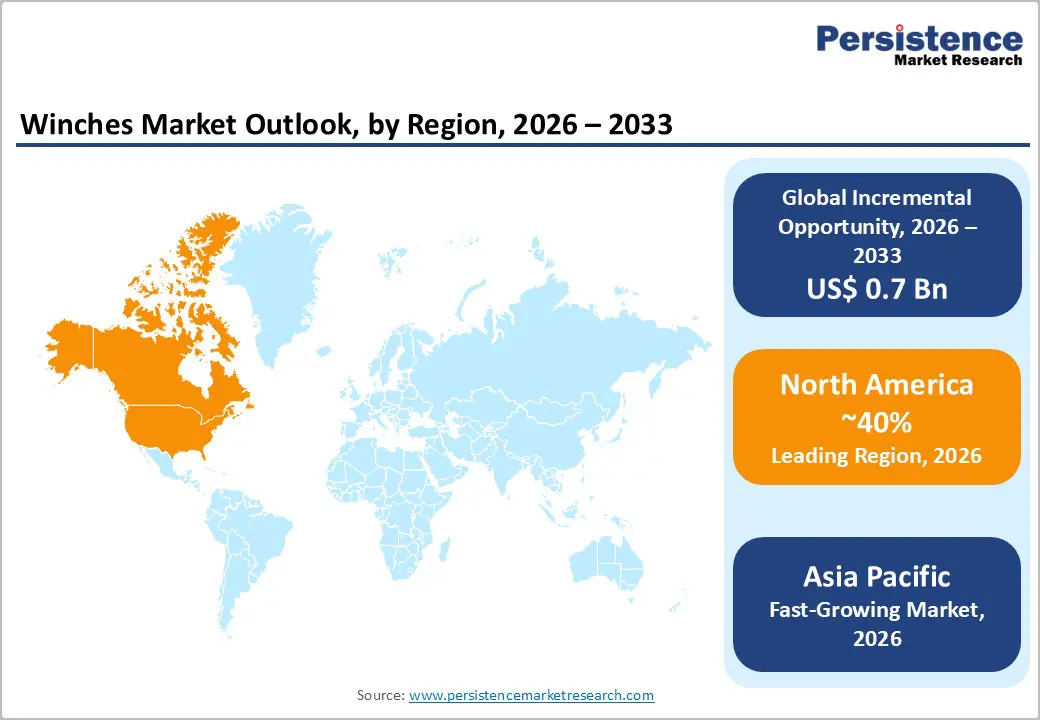

- Dominant Region: North America is expected to hold around 40% of the winches market share in 2026, driven by strong demand from industrial and maritime sectors.

- Fastest-growing Market: Asia Pacific is forecasted to be the fastest-growing market between 2026 and 2033, fueled by soaring demand for heavy-duty lifting and pulling equipment.

- Leading Application: Commercial recovery is expected to secure 30% of the revenue share in 2026, supported by consistent demand in towing, roadside assistance, and fleet operations.

- Fastest-growing Application: The work boat segment is forecasted to be the fastest-growing through 2033, owing to port expansion, offshore maintenance, and inland waterway development.

- August 2025: Straatman acquired Kraaijeveld Winches, expanding its portfolio in marine cargo handling equipment and reinforcing its position in the global deck machinery market.

| Key Insights | Details |

|---|---|

| Winches Market Size (2026E) | US$ 2.1 Bn |

| Market Value Forecast (2033F) | US$ 2.8 Bn |

| Projected Growth (CAGR 2026 to 2033) | 4.2% |

| Historical Market Growth (CAGR 2020 to 2025) | 3.6% |

Market Factors – Growth, Barriers, and Opportunity Analysis

Industrial Mechanization and Infrastructure Expansion

Industrial mechanization and expansion of infrastructure projects stimulate demand for lifting, pulling, and material-handling equipment across sectors such as construction, manufacturing, and transportation. Government capital expenditure allocations, such as India’s INR 11.21 lakh crore (approximately 3.1% of GDP) capital outlay for infrastructure in the 2025–26 fiscal year, underscore a strong public investment commitment to build highways, urban transit, energy networks, and industrial parks. Higher infrastructure spending drives procurement of mechanized solutions to improve productivity, reduce cycle times, and lower risks associated with manual labor, leading to broader adoption of powered equipment in construction and industrial operations.

Mechanized equipment, including powered hoists, pulleys, and specialized winches, enables contractors and fabricators to handle heavier loads with precision and safety on expansive job sites. As infrastructure projects scale in scope and complexity, mechanization becomes essential to meet execution timelines and quality standards set by government agencies and private developers. The effects of mechanization extend into manufacturing facilities where automated systems enhance throughput and integrate with digital control frameworks, reinforcing capital investment in smart material-handling assets.

Technology Integration and Safety Compliance Requirements

Technology integration and safety compliance requirements act as a primary growth catalyst as regulatory authorities continue to tighten operational control over lifting and pulling equipment used in critical applications. In 2025, the International Maritime Organization (IMO) confirmed enforcement of revised Safety of Life at Sea Convention provisions, stating that newly installed shipboard lifting appliances, including winches, must comply with certified design, testing, and inspection standards from January 2026 onward, as documented in official maritime safety notices issued by national administrations aligned with the Convention . This regulatory direction elevates equipment selection criteria from cost focused procurement toward compliance driven investment, where digital load monitoring, automated braking systems, and sensor based diagnostics support mandatory inspection and verification protocols.

Technology integration supports structured safety governance by enabling traceable performance data and predictable operational behavior. Embedded control systems deliver real time visibility into load stress, rope condition, and mechanical efficiency, supporting compliance with documented inspection cycles mandated by maritime, construction, and energy authorities. Government regulators emphasize risk reduction through engineering controls rather than procedural dependence, shifting responsibility toward equipment capability rather than operator discretion. This policy orientation encourages manufacturers to embed safety logic, automated cut off mechanisms, and remote operation functionality as standard features. Procurement teams increasingly evaluate equipment against regulatory readiness metrics, audit compatibility, and lifecycle compliance cost rather than standalone mechanical capacity.

Operational Complexity and Skilled Workforce Dependence

Complex equipment such as winches often require sophisticated setup, operation, and maintenance protocols that elevate operational complexity and create a dependence on a highly trained workforce. Government workplace-safety regulators such as the U.S. Occupational Safety and Health Administration (OSHA) mandate that heavy equipment operators must be trained, certified, and able to demonstrate practical competency before assignment, with certified training becoming an enforceable compliance requirement in 2025 for many heavy equipment roles including rigging and signalperson duties. These requirements reflect the intricate controls, varied configurations, and potential hazards associated with powered industrial equipment, which are difficult to manage without structured instruction and hands-on competence.

The interplay between technical intricacy and workforce skill gaps translates into measurable restraint on industry growth. Advanced winch systems often incorporate automated features, load monitoring, and safety interlocks that require diagnostic skills beyond basic equipment handling. In many regions, documented safety rules within construction codes explicitly require competent persons to manage winch operations and related safety practices, reinforcing that inadequate skills can lead to misuse, accidents, or enforcement issues. A workforce lacking formal training may increase downtime, maintenance costs, and compliance risk, contributing to slower adoption of advanced systems.

Supply Chain Sensitivity and Component Dependence

Industrial strategy and public policy frameworks highlight disruptions in the procurement and delivery of specialised inputs as structural constraints on manufacturing operations. Critical inputs such as precision machined parts, high grade steel alloys, and control system components often originate from a concentrated set of suppliers or regions. The UK Department for Business and Trade Critical Imports and Supply Chains Strategy states recent events severely disrupted supply chains which the economy relies on for critical imports, stressing that reliable flows of essential inputs remain vital to economic stability and competitive operations. Limited supplier diversification increases exposure to single points of failure, extending lead times and elevating procurement costs when disruptions occur.

Public sector actions reflect recognition that concentrated supply sources for specialized materials and parts pose systemic risk for industrial sectors. The United States Department of the Interior 2025 List of Critical Minerals identifies materials at high risk of supply chain disruption, indicating policy focus on stabilizing access to essential inputs for manufacturing and infrastructure projects. Where production of key components is geographically concentrated, export policy shifts, natural disasters, or quality control issues can delay deliveries and stall production lines. Extended procurement cycles challenge contract fulfilment timelines, undermine customer confidence, and erode competitive positioning.

Electrification and Digital Control System Adoption

Integration of electric drives with digital control systems enhances equipment efficiency, reliability, and operational precision. Electric systems offer consistent torque delivery, lower energy loss, and smoother performance compared with conventional mechanical or hydraulic alternatives. Digital controls enable real-time monitoring, remote operation, and predictive maintenance, which reduces downtime and improves overall asset utilization. Automated safety mechanisms embedded in control software manage load limits, detect faults, and alert operators, supporting compliance with increasingly stringent industrial safety regulations.

Advanced control architectures facilitate seamless integration with enterprise systems and Internet of Things (IoT) networks, generating actionable operational data that supports decision-making and performance optimization. Electrically driven systems reduce maintenance burdens and increase operational longevity due to fewer moving parts and enhanced reliability. Data-driven insights allow for predictive analytics, energy optimization, and workflow enhancements, driving higher return on investment and improving throughput.

Expansion across Emerging Industrial and Maritime Hubs

Industrial and maritime hubs are driving demand as they become focal points for integrated infrastructure investment, efficient supply chains, and manufacturing-trade linkages. Government programs such as Sagarmala are designed to develop port-proximate industrial clusters, improve port connectivity, and enable port-led industrialization, which lowers logistics cost and time for exporters and manufacturers by co-locating production capacity near deep-water facilities and multimodal transport networks.

The expansion of trade and industrial activities linked to maritime hubs also strengthens supporting industries, including logistics, fabrication, heavy machinery, and equipment supply, by lowering transportation delays and operational costs. Co-located industrial areas generate concentrated demand for specialized equipment and technological solutions capable of handling large-scale material movement, lifting, and storage. These hubs also attract foreign and domestic investment in ancillary services such as maintenance, repair, and skilled labor training, further stimulating economic activity within the ecosystem.

Category-wise Analysis

Operation Insights

Electric winches are poised to lead with approximately 38% of the winches market revenue share in 2026, owing to operational efficiency, precision control, and compatibility with automated systems. Electric drive technology supports consistent load handling, reduced manual intervention, and enhanced safety compliance across construction, utility, and industrial environments. Provider preference reflects simplified integration with cranes, recovery vehicles, and fixed installations where electrical power availability ensures continuous operation. Accessibility improves through standardized designs suitable for indoor and outdoor applications, while innovation in motor efficiency and braking systems reinforces reliability. Treatment effectiveness parallels emerge through predictable performance and reduced operational variability, positioning electric winches as the preferred operational format across regulated sectors.

Hydraulic winches are anticipated to be the fastest-growing segment between 2026 and 2033, fueled by suitability for high-load, continuous-duty applications within marine, offshore, and heavy industrial environments. Adoption accelerates where operational conditions demand high torque and resilience under harsh environments. Provider acceptance increases due to durability and load consistency under variable pressures. Innovation in hydraulic control systems enhances precision and responsiveness, improving adherence to safety protocols. Accessibility expands through integration with existing hydraulic infrastructure on vessels and mobile equipment, supporting sustained growth momentum.

Application Insights

The commercial recovery segment is slated to hold a dominant position, with an anticipated approximately 30% market share in 2026, driven by consistent demand across towing, roadside assistance, and fleet operations. Sustained growth is supported by structured service protocols that ensure controlled pulling, precise load management, and minimization of operational risks. Standardization across fleet networks promotes uniform adoption of high-performance recovery equipment. Digitalization of dispatch operations allows real-time tracking, route optimization, and enhanced equipment utilization, reducing downtime and service delays. Combined with cost-efficient operation models and wide accessibility, commercial recovery applications continue to serve as a dependable anchor for equipment demand in multiple sectors.

Work boats are forecasted to be the fastest-growing end-user segment between 2026 and 2033, boosted by port expansion, offshore maintenance activities, and inland waterway development. Growth is reinforced by technology-driven service delivery that enhances both safety and operational reliability in complex marine environments. Integration of digital navigation tools and load-monitoring systems supports compliance with maritime safety standards and improves operational efficiency. Vessel modernization programs, including automation and equipment upgrades, accelerate adoption among operators. Expansion of training initiatives and standardized operational protocols further strengthens performance consistency, driving increased reliance on work boats for commercial and industrial maritime applications.

Regional Insights

North America Winches Market Trends

North America is expected to dominate with an estimated around 40% of the winches market share in 2026, reflecting strong demand from established industrial and maritime operations and high value deployment of advanced winching systems. Growth is driven by capital intensive sectors such as offshore energy exploration, construction, and automotive recovery which require robust high capacity mechanical solutions that meet rigorous operational and safety standards. Strict regulatory frameworks on equipment performance and workplace safety accelerate adoption of automation enabled and remote controlled winches, increasing replacement cycles and driving revenue concentration. Buyers prioritize longer operational life, reduced downtime, and integration with digital asset management tools for predictive maintenance, reinforcing consistent demand for technologically advanced units.

A well-developed original equipment manufacturing and service network strengthens this position by enabling faster delivery of customized high performance winches and comprehensive aftermarket support. Diverse applications including marine logistics, fleet operations, and industrial lifting benefit from technical depth and reliability, lowering total cost of ownership through integrated monitoring, load management, and safety enhancements. Adoption of electric drive systems and advanced control technologies is rising, reflecting emphasis on operational efficiency, environmental compliance, and lifecycle optimization.

Europe Winches Market Trends

Europe demonstrates steady growth in the winches market, supported by well-established industrial, marine, and construction sectors that prioritize safety, efficiency, and regulatory compliance. Demand is largely driven by offshore energy operations, port activities, and urban infrastructure projects that require high-capacity mechanical solutions for lifting, towing, and load handling. Advanced manufacturing capabilities enable production of precision-engineered winches, including electric, hydraulic, and hybrid systems, tailored for specific industrial applications. Operators emphasize integration with monitoring systems, predictive maintenance, and load management technologies to reduce downtime and improve operational reliability.

Maritime operations and shipbuilding activities further strengthen demand, as advanced winching solutions are required for mooring, deck operations, and cargo handling in commercial and offshore vessels. Investments in modernization programs for ports and inland waterways increase throughput and operational efficiency, supporting adoption of technologically enhanced systems. Additionally, a mature service and aftermarket network provides repair, maintenance, and customization solutions, allowing extended service life and cost-effective asset management. Focus on automation, remote operation, and energy-efficient systems encourages operators to adopt solutions that align with both operational and sustainability objectives.

Asia Pacific Winches Market Trends

Asia Pacific is forecasted to be the fastest-growing market for the winches market between 2026 and 2033, stimulated by rapid industrialization, infrastructure development, and expansion of maritime and inland transport networks. Sustained investment in highways, ports, and inland waterways is generating significant demand for heavy-duty lifting and pulling equipment. Urbanization and large-scale construction projects, including commercial, industrial, and municipal developments, require reliable winching solutions that can operate under diverse environmental and load conditions. Manufacturing hubs across key economies contribute to high-volume application across multiple sectors, ranging from resource extraction and vehicle recovery to plant operations and logistics.

Infrastructure modernization in port and shipbuilding sectors further accelerates adoption, with growth driven by new vessel production, offshore servicing, and cargo handling requirements. Investment by governments and private developers to improve operational efficiency and cargo throughput at key maritime gateways strengthens the commercial rationale for advanced winching equipment. Localized manufacturing ecosystems support cost efficiency by producing specialized solutions that meet regional operational standards while remaining competitive in price and performance.

Competitive Landscape

The global winches market structure features moderate fragmentation, where no single player commands a dominant market share. Market dynamics are influenced by the ability of companies such as Ingersoll Rand, Columbus McKinnon Corporation, WARN, PACCAR Inc., Kito Corp., Ramsey Industries, and Dover Corporation to integrate advanced technologies into winch systems, including automation, remote control, and safety-enhancing features. Manufacturers differentiate themselves through diverse capacity offerings, catering to a wide range of applications from light-duty industrial operations to heavy-duty construction and marine environments. Aftermarket service capabilities, such as maintenance, repair, and replacement parts, also play a crucial role in shaping customer preference and fostering brand loyalty.

Key players emphasize strategic initiatives, including product portfolio expansion, geographic penetration, and collaboration with industrial partners, to enhance competitiveness. Continuous investment in research and development allows these companies to improve winch efficiency, durability, and operational safety, aligning with industry standards and customer expectations. Service networks and training programs contribute to long-term engagement and reliability perception. The moderately fragmented nature of the market creates opportunities for both established players and emerging entrants to capture niche segments by offering specialized solutions.

Key Industry Developments

- In February 2026, WARN launched the ZEON XC Big Winch, a compact and intelligent winching solution engineered for off-road and utility vehicles that delivers robust pulling power in a smaller package. The new model integrates advanced design features to enhance performance, durability, and ease of use on rugged terrain.

- In January 2026, Dover Corporation’s unit TWG launched the new Pullmaster 40 M/H Planetary Winch, a 40,000 pound capacity model in its M & H Series designed to bridge the gap between its 25,000 and 50,000 pound winches for demanding marine, industrial, recovery, energy, and natural resources applications.

- In May 2025, Kongsberg Maritime unveiled a new electric towing winch for harbor tugboats at the TUGTECHNOLOGY ’25 Conference in Antwerp, Belgium, designed to deliver up to 35 tons of pulling force with enhanced efficiency and reduced environmental impact compared with traditional hydraulic systems.

Companies Covered in Winches Market

- Ingersoll Rand

- Columbus McKinnon Corporation.

- WARN

- PACCAR Inc.

- Kito Corp.

- Ramsey Industries.

- Dover Corporation

Frequently Asked Questions

The global winches market is projected to reach US$ 2.1 billion in 2026.

Rising industrial automation, growing demand for heavy‑load handling, and adoption of advanced, safety-enhanced winch technologies are driving the market.

The market is poised to witness a CAGR of 4.2% from 2026 to 2033.

Surging demand for electric and high-capacity winches, expanding marine and construction applications, and technological advancements in automation present key market opportunities.

Some of the key market players include Ingersoll Rand, Columbus McKinnon Corporation, WARN, PACCAR Inc., Kito Corp., Ramsey Industries, and Dover Corporation.