- Beauty & Personal Care

- Waterless Cosmetics Market

Waterless Cosmetics Market Size, Share, and Growth Forecast 2026 - 2033

Waterless Cosmetics Market by Product Type (Skincare, Hair Care, Makeup, and Others), Nature (Natural/ Organic and Synthetic), Price Range (Economy (Below US$ 30), Mid-Range (US$ 30 to US$ 60), and Premium (Above US$ 60)), Distribution Channel (Offline and Online), and Regional Analysis for 2026 - 2033

Waterless Cosmetics Market Size and Share Analysis

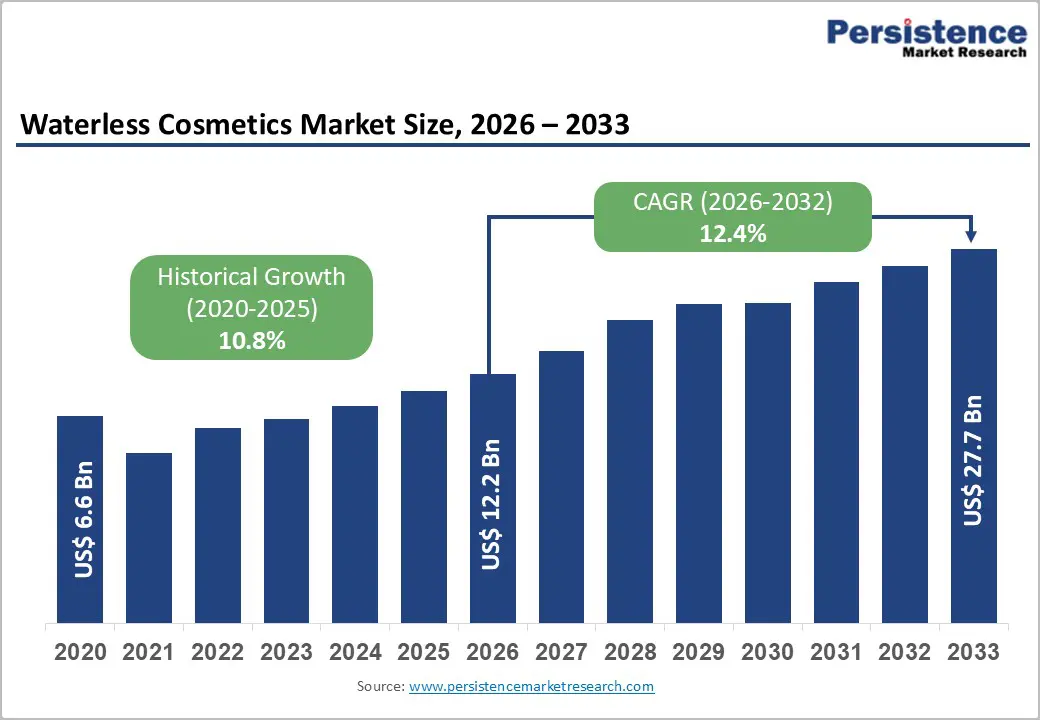

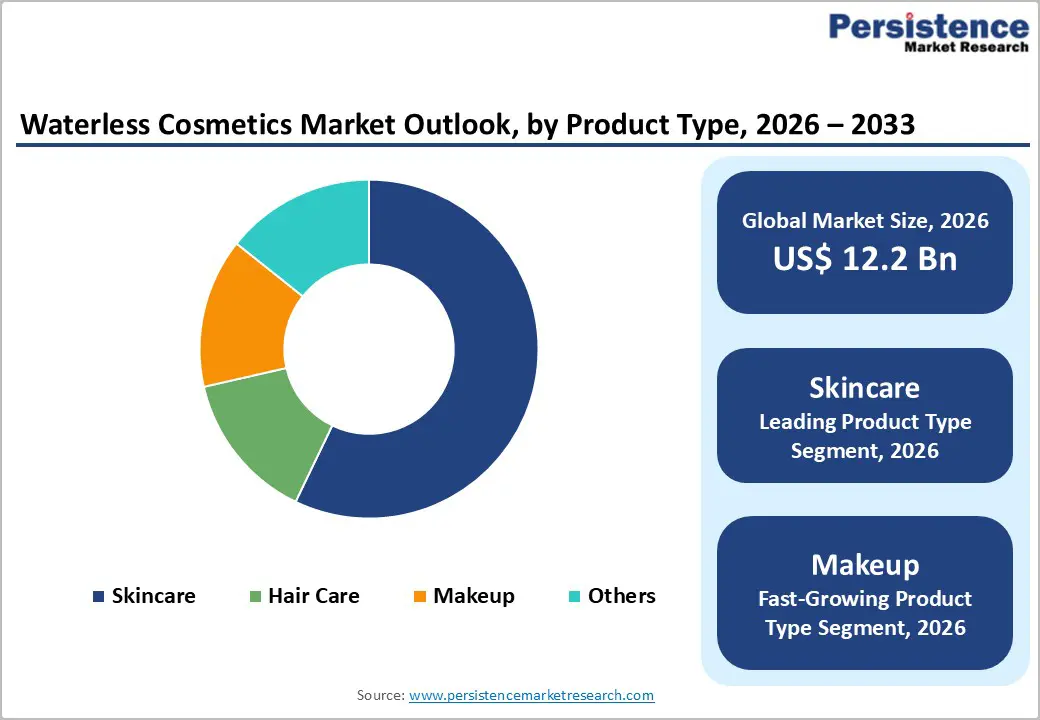

The global waterless cosmetics market size is likely to be valued at US$ 12.2 billion in 2026 and is projected to reach US$ 27.7 billion by 2033, growing at a CAGR of 12.4% between 2026 and 2033.

Market expansion is driven by the rise in consumer awareness of water scarcity and sustainability imperatives, with traditional skincare products containing up to 80% water as a compelling value proposition. Rising demand for natural and organic ingredients combined with elimination of synthetic preservatives and emulsifiers characteristic of waterless formulations creates alignment with clean beauty movement.

Key Market Highlights

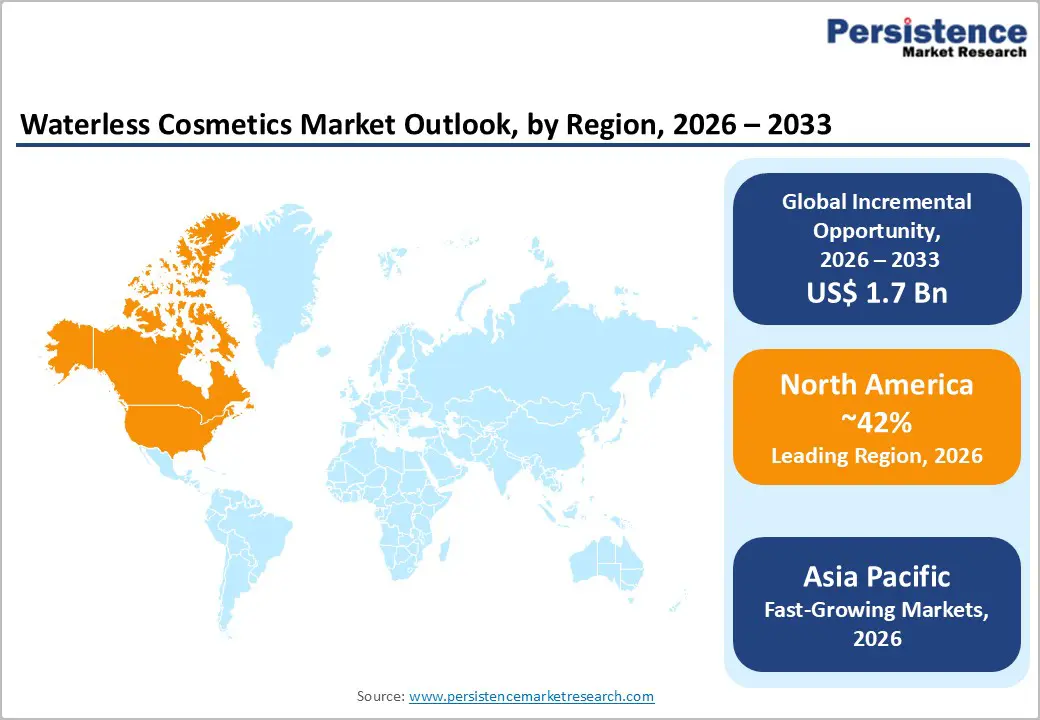

- Leading Region: North America maintains market leadership driven by the United States water scarcity awareness, premium consumer positioning, strong direct-to-consumer brand success, regulatory framework emphasis on sustainability, and affluent demographics supporting higher price points and margin profiles.

- Fastest Growing Region: Asia Pacific commands fastest expansion with India at 24.1% CAGR and China at 23.3% CAGR for waterless powders, driven by water scarcity intensity, rising disposable incomes, younger demographic concentration, e-commerce platform excellence, and emerging market industrialization.

- Dominant Product Type: Skincare products command market dominance with 42% market share in 2026, driven by consumer prioritization of face and body care, concentrated active ingredient formulations, premium pricing tolerance, and direct-to-consumer brand proliferation.

- Growing Product Type: Makeup segment experiences fastest expansion at 10.3% CAGR, propelled by waterless foundation powders, solid blushes, dry eyeshadows, concentrated pigment benefits, and eco-conscious consumer appeal among younger demographics.

- Key Market Opportunity: Asia Pacific market expansion and premium product positioning acceleration, with India and China representing world's fastest-growing markets at 24.1% and 23.3% CAGR, respectively, driven by emerging middle-class expansion and digital commerce excellence.

| Key Insights | Details |

|---|---|

|

Global Waterless Cosmetics Market Size (2026E) |

US$ 12.2 Bn |

|

Market Value Forecast (2033F) |

US$ 27.7 Bn |

|

Projected Growth CAGR(2026-2033) |

12.4% |

|

Historical Market Growth (2020-2025) |

10.8% |

Market Dynamics

Drivers - Clean Beauty Movement and Premium Product Positioning Accelerating Market Expansion

Rising consumer demand for natural, organic, and vegan ingredient formulations reflecting heightened awareness of synthetic chemical health impacts. Elimination of synthetic preservatives and emulsifiers inherent to waterless formulations creates health-conscious consumer appeal, particularly among millennial and Gen-Z demographics prioritizing clean beauty alignment with personal wellness values. Concentrated active ingredient formulations in waterless products deliver superior efficacy compared to traditional water-based alternatives, establishing performance validation supporting premium pricing strategies.

Luxury brand entry into waterless market, exemplified by Estée Lauder's $500 million acquisition of Korean waterless brand Dr Jart+ in September 2023, demonstrates premium market validation and strategic capital allocation supporting market legitimacy. Global cosmetics market size exceeding US$ 335 billion in 2024 combined with waterless segment representing approximately 3.6% market share establishes substantial white space opportunity for market expansion and category penetration growth through forecast period.

E-Commerce Growth, Travel Convenience, and Supply Chain Efficiency

Rapid expansion of e-commerce and direct-to-consumer (DTC) beauty channels is another significant driver of the global waterless cosmetics market. Waterless products, such as solid bars, powders, sticks, and balms, are typically lighter, more compact, and less prone to leakage or spillage compared to liquid formulations. These characteristics reduce shipping costs, breakage rates, and return risks, making them highly attractive for online retail logistics. As digital beauty sales continue to rise globally, brands are increasingly favoring waterless formats to improve fulfillment efficiency and profitability. Travel convenience is further accelerating adoption, particularly among urban consumers and frequent travelers. Waterless cosmetics comply easily with airline carry-on liquid restrictions, enhancing their appeal for travel-size and on-the-go applications.

The growing popularity of minimalist lifestyles and capsule beauty routines supports demand for multifunctional, concentrated products that deliver extended usage from smaller formats. This trend is especially strong in Asia Pacific and Europe, where compact living and mobility-driven consumption patterns are prevalent. Waterless cosmetics offer longer shelf life, reduced microbial risk, and lower storage complexity, improving inventory management for both manufacturers and retailers. Reduced reliance on preservatives and simplified cold-chain requirements enhance operational efficiency across global distribution networks. These logistical and commercial advantages, combined with the continued growth of digital retail and travel-oriented consumption, are positioning waterless cosmetics as a strategically favorable product category, supporting sustained market growth over the forecast period.

Restraint - Limited Consumer Awareness and Educational Barriers Impeding Market Penetration

Lack of effective awareness campaigns and marketing strategies communicating waterless cosmetics benefits and product efficacy creates consumer knowledge gaps limiting market penetration, particularly among mainstream consumer segments accustomed to traditional water-based formulations. Consumer skepticism regarding performance equivalence with established brands and concerns about product consistency and stability in waterless formats present psychological barriers to trial and adoption. Retail shelf allocation challenges and limited product visibility in traditional distribution channels restrict market access for emerging waterless brands competing against established cosmetics manufacturers with dominant retail relationships and shelf presence.

Formulation Complexity and Product Development Challenges Creating Market Entry Barriers

Technical complexity in waterless formulation development requiring innovative ingredient sourcing and alternative bases including oils, butters, and botanical extracts creates elevated research and development requirements and extended product development timelines. Regulatory compliance complexity across divergent global standards and varying regional certification requirements increases market entry costs and technical expertise requirements, particularly impacting smaller brand competitors lacking established regulatory infrastructure. Supply chain sourcing challenges for specialized waterless formulation ingredients and sustainable packaging materials create operational complexity and cost pressures limiting market expansion velocity.

Opportunity - E-Commerce Expansion and Direct-to-Consumer Distribution Model Proliferation

E-commerce platform dominance commanding more than 51% market share in 2026 establishes exceptional growth opportunity for waterless cosmetics brands leveraging digital-first distribution strategies to bypass traditional retail intermediaries and establish direct customer relationships. Online retail platform accessibility enables geographic expansion beyond traditional distribution boundaries, creating international market penetration opportunities for emerging waterless brands. Social media platform utilization for consumer education and brand storytelling communicates sustainability narratives and clean beauty positioning, driving viral adoption among digitally native consumer segments.

Subscription and refillable model integration supported by cloud-based consumer engagement platforms creates recurring revenue opportunities and long-term customer lifetime value expansion. Amazon, Sephora, and specialty beauty e-commerce platforms representing aggregation points for waterless product discovery establish distribution opportunity concentration supporting market penetration acceleration through forecast period.

Expansion into Emerging Markets through Affordable, Climate-Resilient Beauty Solutions

The global waterless cosmetics market presents a significant opportunity for expansion across emerging economies in Asia Pacific, Latin America, and the Middle East & Africa, where water scarcity, hot climates, and infrastructure limitations directly impact conventional cosmetic usage and distribution. In many of these regions, inconsistent water availability and high temperatures accelerate product spoilage in traditional water-based formulations, creating strong demand for climate-resilient, long-shelf-life beauty products. Waterless cosmetics, with their enhanced stability and reduced preservative requirements, are well positioned to address these challenges. Affordable waterless formats such as powders, solid bars, and concentrated sticks offer cost-effective solutions by delivering more uses per unit and minimizing packaging and transportation costs. This enables brands to introduce entry-level and mid-priced products tailored to price-sensitive consumer segments while maintaining acceptable margins.

Rising urbanization, growing middle-class populations, and increasing awareness of hygiene and personal grooming in emerging markets further strengthen demand potential. Localized formulation using regionally sourced ingredients and culturally aligned product concepts can accelerate adoption and brand acceptance. As global and regional beauty players seek growth beyond saturated mature markets, strategic expansion of waterless cosmetics into emerging regions represents a scalable, long-term growth opportunity with strong alignment to sustainability, affordability, and resilience objectives.

Category-wise Analysis

Product Type Insights

Skincare products command market dominance, representing approximately 42% market share in 2024, driven by consumer prioritization of face and body care addressing core skincare concerns including hydration, anti-aging, and targeted treatment applications. Waterless skincare formulations leveraging natural oils, botanical extracts, and innovative solid presentations deliver concentrated active ingredients enabling superior efficacy relative to traditional water-based alternatives. Cleansers, moisturizers, serums, and masks formulated without water require innovative ingredient bases including botanical butter combinations and oil-based delivery systems enabling complete product efficacy without water dependency.

Premium pricing tolerance among skincare consumers seeking concentrated, multi-benefit formulations supports higher margin profiles and brand profitability relative to haircare and makeup categories. Direct-to-consumer skincare brand proliferation leveraging sustainability positioning and clean ingredient communication establishes market segment momentum supporting continued leadership position throughout forecast period.

Nature Insights

Synthetic waterless formulations command market dominance with 63.7% revenue share in 2026, driven by technological advancement enabling high-performance formulations and ingredient stability supporting product shelf life extension and consumer satisfaction. Advanced synthetic actives including silicones, amino acids, and polymer technologies deliver performance characteristics difficult to achieve through natural ingredient formulations alone, supporting premium brand positioning and professional efficacy validation. Consistency and reproducibility advantages of synthetic formulations enable quality assurance and regulatory compliance supporting large-scale manufacturing and commercial viability.

Organic and natural segment representing fastest-growing category reflects consumer preference shift toward clean beauty and sustainable sourcing, with natural waterless formulations commanding premium pricing and brand loyalty despite smaller current market share. Hybrid approach combining synthetic performance actives with natural ingredient bases represents emerging market trend supporting broader consumer appeal and market expansion through forecast period.

Price Range Insights

Premium waterless cosmetics priced above US$ 60 represent fastest-growing price segment, driven by luxury brand market entry and professional-grade formulation positioning. Estée Lauder's $500 million acquisition of Dr Jart+ establishes premium market validation and luxury brand commitment to waterless innovation, enabling aspirational positioning and premium pricing power.

Dermatology-aligned and clinical-grade waterless formulations command premium pricing reflecting superior ingredient quality and efficacy validation supporting health-conscious, affluent consumer segments. Limited-edition and exclusive waterless product launches create scarcity-driven demand supporting premium margins and brand prestige. Mid-range price segment (US$ 30-60) representing growing market sweet spot balances affordability with quality perception, attracting mainstream consumer adoption and volume growth opportunity.

Distribution Channel Insights

E-commerce channels commanding more than 51% market share by 2026 establish dominant distribution mode for waterless cosmetics, driven by digital commerce convenience, product discovery through social platforms, and direct brand-consumer relationships. Online-first waterless brands including True Botanicals, Clensta, and The Waterless Beauty Company leverage digital marketing and sustainability storytelling to build brand communities and drive customer loyalty. Sephora and Amazon serving as aggregation platforms for waterless product discovery enable mainstream consumer access to emerging brands previously constrained by traditional retail distribution limitations.

Offline retail channels maintaining significant market share remain important for trial and immediate purchase satisfaction, particularly for prestige and luxury brands leveraging premium retail environments to communicate brand positioning. Hybrid omnichannel strategies combining online accessibility with experiential retail environments establish competitive advantage supporting sustained market growth through forecast period.

Regional Insights

North America Waterless Cosmetics Market Trends

North America is estimated to account for approximately 42% of global waterless cosmetics revenue in 2026, reflecting its premium pricing, early adoption of clean beauty innovations, and continued expansion of DTC channels. The region represents a developed, high-value market for waterless cosmetics, led overwhelmingly by the United States, where consumer awareness around water scarcity, climate change, and environmental footprint is well established, particularly in drought-prone western states such as California, Arizona, and Nevada. Sustainability messaging resonates strongly with educated, urban consumers, accelerating acceptance of waterless formats including solid cleansers, powders, and concentrated skincare products.

The region benefits from strong purchasing power, enabling premium and luxury positioning of waterless cosmetics, with consumers demonstrating a willingness to pay higher prices for clean, sustainable, and high-efficacy formulations. Direct-to-consumer (DTC) brand success plays a critical role in regional growth. Brands such as True Botanicals and Allies Group leverage advanced digital marketing, influencer partnerships, and subscription-based models to build loyal, sustainability-focused consumer communities. North America’s mature e-commerce infrastructure, combined with transparent ingredient disclosure and clinical efficacy claims, supports strong brand trust and repeat purchases.

Europe Waterless Cosmetics Market Trends

Europe represents a mature, regulation-driven, sustainability-centric market for waterless cosmetics, characterized by strong institutional and consumer alignment on environmental responsibility. Countries such as Germany and the United Kingdom are leading adoption, with Germany registering a 10.4% CAGR and the UK achieving a 13.9% CAGR, driven by heightened consumer scrutiny of product sustainability and packaging waste. European consumers demonstrate strong preference for eco-certified, water-efficient, and low-impact beauty products, reinforcing demand for waterless alternatives.

Regulatory pressure is a defining market force. European Union-wide sustainability policies, including Ecodesign and circular economy frameworks, are compelling beauty brands to reduce water usage, packaging volume, and carbon intensity across the value chain. This regulatory environment accelerates waterless formulation adoption not only among niche clean beauty brands but also across established premium and mass-market players.

Asia Pacific Waterless Cosmetics Market Trends

Asia Pacific is the fastest-growing regional market for waterless cosmetics, supported by rapid urbanization, digital commerce penetration, and rising environmental awareness. The region demonstrates exceptional growth momentum, with India recording a 24.1% CAGR and China achieving a 23.3% CAGR for waterless powder-based cosmetic products. High population density, climate variability, and water conservation concerns amplify consumer receptivity to compact, shelf-stable, and travel-friendly cosmetic formats.

The market growth in India is further strengthened by domestic manufacturing capabilities and government support initiatives such as Make in India, which encourage local production of clean and sustainable beauty products. The presence of innovative domestic brands such as Ruby’s Organics highlights India’s emerging leadership in clean and waterless beauty within developing markets.

Competitive Landscape

The waterless cosmetics market exhibits a moderately consolidated competitive structure with global beauty conglomerates commanding substantial market share alongside innovative startups disrupting traditional category boundaries. Tier 1 leaders including Unilever, L'Oréal, Procter & Gamble, and Kao Corporation leverage established distribution networks, research capabilities, and brand portfolios to drive waterless category adoption across mainstream consumer segments. Strategic acquisition activity, exemplified by Estée Lauder's $500 million Dr Jart+ acquisition and L'Oréal's Gjosa acquisition, demonstrates capital commitment to waterless innovation and market consolidation.

Emerging startups including True Botanicals, Clensta, and The Waterless Beauty Company establish competitive differentiation through sustainability positioning, clean ingredient transparency, and digital-native brand strategies. Competitive strategies emphasize innovation in powder cleansers, oil-based masks, and solid moisturizers, AI-driven personalization, and refillable packaging integration supporting sustained differentiation and market share expansion.

Key Market Developments:

- In October 2025, Voshbon Beauty Vashon introduced a new line of freeze-dried, waterless beauty products formulated using advanced lyophilisation technology, enabling concentrated solid or granule formats that activate with water at the time of use. The launch includes targeted hair, face, and body washes designed to significantly reduce water usage in both production and consumer application.

- In February 2024, L'Oréal SA announced significant expansion of waterless product offerings including waterless shampoos, conditioners, and skincare products targeting water consumption reduction during production and consumer use, strengthening sustainable beauty positioning.

- In May 2024, The Procter & Gamble Company introduced Cleansing Melts and HiBar Solid Oil Cleanser under Olay beauty brand, advancing waterless skincare innovation and addressing modern skincare sustainability needs through water elimination.

Companies Covered in Waterless Cosmetics Market

- Unilever Plc

- The Waterless Beauty Company

- L’Oreal SA

- Kao Corporation

- The Procter & Gamble Company

- Loli

- Clensta

- Ruby’s Organics

- Carter + Jane

- Taiki USA

- Ktein

- Niconi

- True Botanicals

- Allies Group Pte. Ltd.

- Lavedo Cosmetics

- No Cosmetics

- May Coop

- Azafran Innovacion

Frequently Asked Questions

The global waterless cosmetics market is projected to reach US$ 27.7 billion by 2032, expanding from US$ 12.2 billion in 2025 at a CAGR of 12.4%, driven by water scarcity awareness, sustainability consciousness, concentrated formulation efficacy, e-commerce expansion, and Asia Pacific market acceleration.

Market demand growth is driven by multiple converging factors including water scarcity awareness with traditional skincare containing up to 80% water, environmental sustainability consciousness and ESG commitments, concentrated active ingredient formulations delivering 15-20% higher efficacy, clean beauty movement and organic ingredient preference, e-commerce platform dominance.

Skincare products command market dominance with approximately 42% market share in 2026, driven by consumer prioritization of face and body care, concentrated active ingredient formulations, premium pricing tolerance, and direct-to-consumer brand proliferation supporting continued segment leadership.

North America maintains market leadership anchored by United States market dominance, supported by water scarcity awareness, premium consumer positioning, strong direct-to-consumer brand success, and regulatory framework emphasis on sustainability establishing sustained developed market leadership.

Major market opportunities include Asia Pacific expansion, e-commerce platform dominance, premium product positioning commanding highest growth and margin profiles; AI-driven personalization and formulation innovation; and refillable packaging system integration supporting direct-to-consumer relationship strengthening.