- Industrial Machinery

- Vertical Lift Module Market

Vertical Lift Module Market Size, Share, and Growth Forecast 2026 - 2033

Vertical Lift Module Market by Delivery Type (Single Delivery Type, Dual Delivery Type), by Solution Type (Automatic Vertical Lift Modules, Semi-Automatic Vertical Lift Modules), by Load Capacity (Light Duty, Medium Duty, Heavy Duty), Application (Automotive, Electronics & Electrical, Aerospace & Defense, Healthcare & Pharmaceuticals, Food & Beverage, Retail & E-commerce, Logistics & Warehousing, Manufacturing, Others), Regional Analysis, 2026 - 2033

Vertical Lift Module Market Size and Trend Analysis

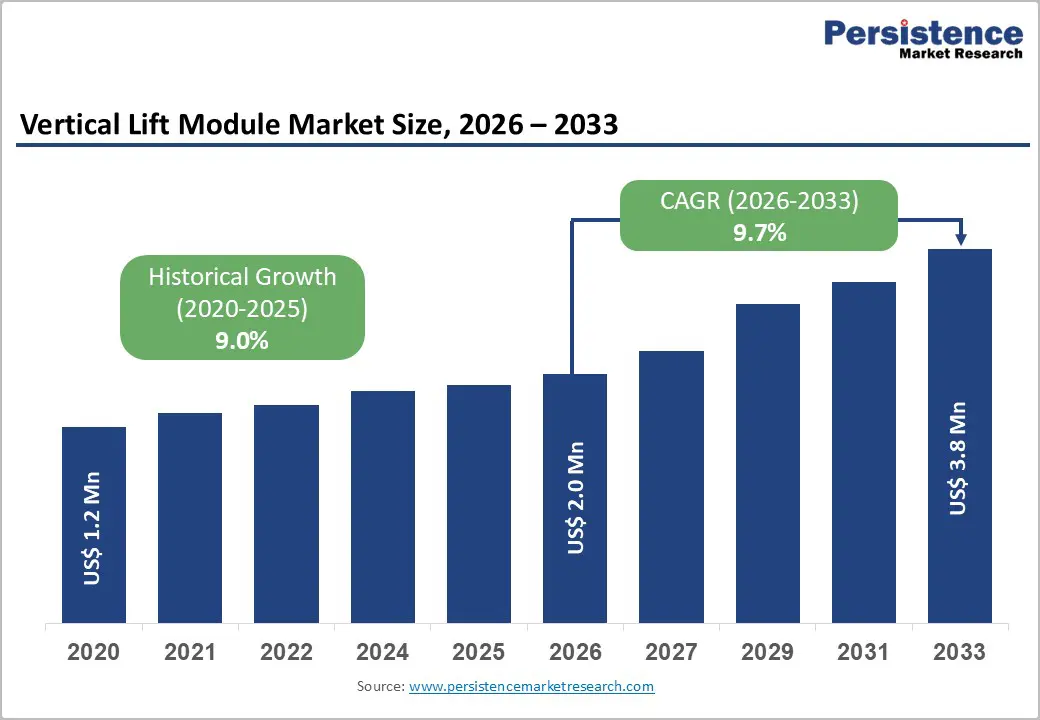

The global vertical lift module (VLM) market is expected to be valued at US$ 2.0 million in 2026 and projected to reach US$ 3.8 million by 2033, growing at a CAGR of 9.7% between 2026 and 2033.

Market expansion is driven by accelerating e-commerce demand, critical labor shortages across developed economies, and the imperative to optimize space in high-cost urban real estate markets. The explosive growth of e-commerce has catalyzed demand for automated storage solutions, with industry forecasts indicating that more than 4 million robots will be deployed in more than 50,000 warehouses globally by 2025, representing a dramatic expansion from approximately 4,000 robotic warehouses in 2018.

The integration of AI-powered predictive maintenance, real-time data analytics, and IoT sensors is enabling return-on-investment periods under 24 months in select applications, thereby accelerating capital equipment procurement decisions across logistics, manufacturing, and healthcare sectors.

Key Industry Highlights:

- Leading Region Position: North America leads the vertical lift module market with approximately 29% share, supported by mature logistics infrastructure, advanced system integration capabilities, and strong capital availability driving adoption across e-commerce, automotive, and healthcare sectors.

- Fastest Growing Region: Asia Pacific represents the fastest-growing region, expanding at a 12.3% CAGR through 2033, driven by greenfield smart factories in China, industrial corridor development in India, labor shortages in Japan and South Korea, and rapid quick-commerce expansion across ASEAN.

- Dominant Delivery Segment: Single-delivery vertical lift modules dominate the market with around 57% share, reflecting their cost efficiency, manufacturing simplicity, and broad suitability for small to mid-scale operations across multiple industries.

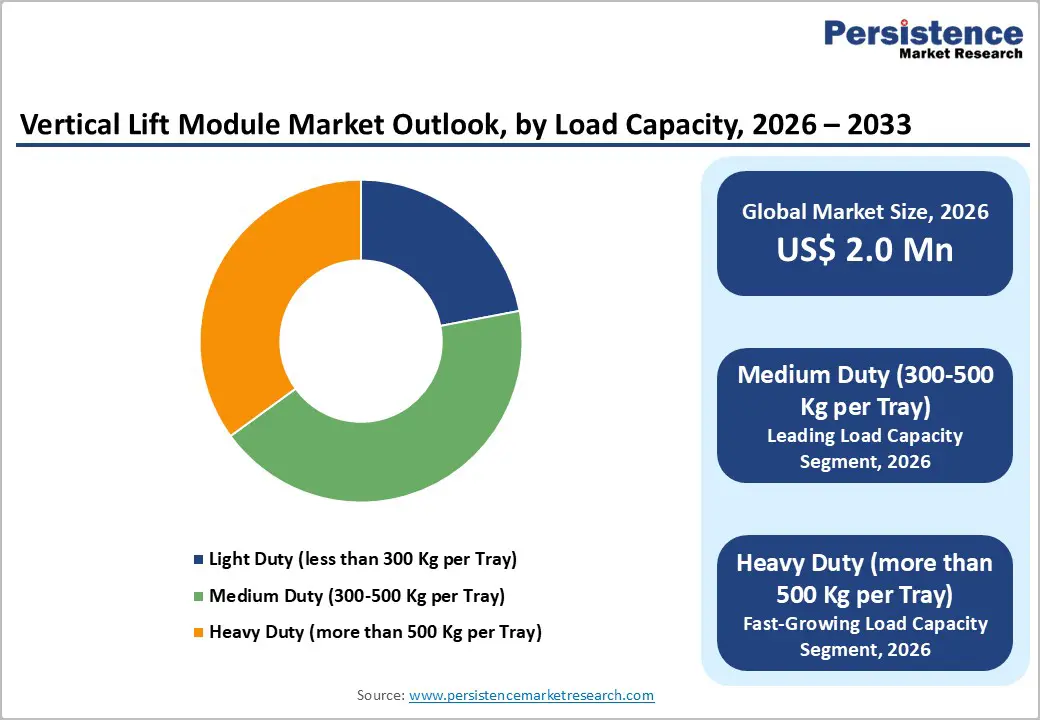

- Dominant Load Capacity Segment: Medium-duty vertical lift modules rated at 300-500 kg per tray account for approximately 43% market share, supported by their versatility across automotive, e-commerce, and pharmaceutical applications and strong economies of scale.

- Key Opportunity: Automotive manufacturing represents a key opportunity, contributing nearly 29% of application-based demand due to just-in-time production requirements and the role of VLMs as core infrastructure for efficient, synchronized manufacturing operations.

| Key Insights | Details |

|---|---|

| Vertical Lift Module Market Size (2026E) | US$ 2.0 million |

| Market Value Forecast (2033F) | US$ 3.8 million |

| Projected Growth CAGR (2026 - 2033) | 9.7% |

| Historical Market Growth (2020 - 2025) | 9.0% |

Market Dynamics

Drivers - Explosive E-Commerce Expansion and Omnichannel Retail Demand for High-Speed Order Fulfillment Infrastructure

The rapid expansion of e-commerce and omnichannel retail is fundamentally reshaping warehouse automation requirements and driving strong demand for vertical lift module systems capable of high-speed and high-accuracy order fulfillment. Quick-commerce operators across India and Southeast Asia are aggressively scaling dark-store networks, with Flipkart Minutes planning expansion from 300 to 800 locations by end-2025 and Blinkit targeting nearly 2,000 locations by FY26.

Industry surveys indicate that around 85% of supply-chain teams intend to deploy warehouse automation within 12 months to support sub-15-minute delivery commitments. VLM systems directly address these requirements through goods-to-person operations that reduce handling time by 40-60% relative to traditional shelving and improve order accuracy to nearly 99.9%, compared with 95-97% in manual setups. Additionally, floor-space savings of up to 90% are increasingly valuable for urban logistics hubs facing sharply rising real estate costs.

Critical Labor Shortage Crisis in Developed Economies Creating Acute Demand for Operator-Displacement Technologies

Demographic shifts and regulatory constraints across developed economies have led to a persistent labor shortage in warehouse and logistics operations, thereby significantly accelerating demand for operator-displacement technologies such as vertical lift modules. Japan’s “2024 Problem,” which limits annual truck-driver overtime, is projected to result in nearly 35% freight nondelivery capacity by 2030 without automation-led productivity gains. In South Korea, the National Logistics Basic Plan has driven automation adoption, with autonomous system sales increasing by 44% annually and CJ Logistics reporting productivity improvements of approximately 20% in technology-enabled facilities.

Europe faces similar pressures, particularly in Germany and Scandinavia, where aging populations and reduced labor mobility are constraining workforce availability. VLM systems allow facilities to maintain throughput by displacing the equivalent of 3-5 full-time operators per unit while enhancing accuracy and safety. In high-wage markets, ROI periods of 18-24 months are increasingly common, accelerating capital investment decisions.

Restraints - High Initial Capital Investment and Extended Payback Periods Limiting Accessibility for Small and Medium-Sized Enterprises

Despite clear operational advantages, the high upfront investment required for deploying vertical lift modules remains a significant barrier, particularly for small and medium-sized enterprises. Advanced automatic VLM systems typically cost between US$ 250,000 and US$ 500,000 per unit, and full-scale deployments often require multiple systems along with integration infrastructure, pushing total project costs beyond US$ 1-2 million. Return-on-investment timelines of 24-36 months exceed the capital justification thresholds of many SMEs, particularly in developing regions where access to financing is limited.

Additional expenditures associated with integrating VLMs with warehouse management and ERP systems increase project complexity and the total cost of ownership. Training requirements for operators and maintenance staff further add to ongoing expenses. In markets with relatively low labor costs, these financial considerations reduce the economic attractiveness of automation, restricting adoption primarily to large enterprises and well-capitalized logistics operators.

Physical Infrastructure Limitations and Technical Integration Challenges Constraining Installation Feasibility in Existing Facilities

Physical infrastructure constraints within existing warehouses significantly limit the feasible deployment of vertical lift module systems, thereby moderating overall market growth. Many brownfield facilities, particularly in Europe, face roof-height limitations that prevent installation of tall VLM units designed to maximize vertical space utilization. Structural reinforcement requirements, including floor strengthening and foundation upgrades, can add 15-25% to total project costs.

Environmental control needs such as temperature stability, humidity regulation, and dust control are often incompatible with older facility designs, necessitating costly retrofits. Integration with legacy warehouse management and enterprise systems frequently requires extensive software customization and data migration, increasing implementation timelines and operational risk. As a result, VLM adoption is more practical in new-build warehouses or major modernization projects than in retrofitting existing facilities, thereby limiting penetration into established logistics infrastructure.

Opportunities - Artificial Intelligence and Predictive Maintenance Integration Enabling Substantial After-Sales Revenue and Enhanced System Reliability

The integration of artificial intelligence, machine learning, and IoT sensor technologies into vertical lift module systems is creating a major growth opportunity by strengthening system reliability while unlocking high-margin, recurring after-sales revenue streams. AI-driven predictive maintenance solutions enable early identification of component wear and performance degradation, allowing preventive interventions that reduce unplanned downtime by 60-80% compared to reactive maintenance practices. Advanced data analytics platforms processing millions of pick cycles daily further enhance operational efficiency by optimizing task sequencing and throughput, delivering productivity gains of 15-25%.

Cloud-based warehouse management and control platforms are also gaining traction by enabling centralized monitoring of distributed VLM fleets, improving inventory visibility and replenishment accuracy. Leading manufacturers are increasingly shifting toward software-centric business models that integrate analytics, mobile access, and open integration ecosystems.

As a result, software and services are expected to expand from roughly 20% of current revenues to 35-40% by 2033, supporting margin expansion and long-term revenue stability.

Emerging Market Expansion in Asia Pacific and Latin America Driven by Industrial Corridor Development and Logistics Infrastructure Investment

Rapid industrialization and large-scale logistics infrastructure development across the Asia Pacific and Latin America are creating strong growth opportunities for vertical lift module adoption, particularly in greenfield manufacturing and warehousing projects. Government-led industrial corridor initiatives and smart manufacturing programs are accelerating investments in modern warehouse capacity and automation-ready facilities.

India’s push to add approximately 1.2 billion square feet of modern warehouse space by 2027 is driving demand for automated storage solutions, while China’s smart factory initiatives are increasing the penetration of VLMs in newly built production facilities.

Southeast Asian economies such as Vietnam, Thailand, and Indonesia are witnessing fast expansion of quick-commerce and organized logistics networks, further supporting demand for high-density storage systems. In Latin America, investments in industrial zones and logistics hubs across Mexico, Brazil, and Chile are improving automation readiness.

Greenfield construction, limited legacy infrastructure constraints, and supportive government policies create favorable conditions for suppliers expanding regional manufacturing, service networks, and localized financing models.

Category-wise Analysis

Delivery Type Insights

Single delivery type vertical lift modules maintain market leadership, accounting for approximately 57% of global market share in 2025, due to their cost efficiency, simplified architecture, and broad operational applicability. These systems utilize a single access opening for sequential tray handling, enabling straightforward workflows that require minimal operator training and lower integration complexity. Their reduced manufacturing and installation costs make them well-suited for moderate-throughput environments, typically supporting 50-150 transactions per hour.

Single delivery systems are widely deployed across manufacturing, healthcare, aerospace, and mid-scale e-commerce facilities, particularly in developing economies where capital discipline and faster ROI requirements prevail. The segment continues to dominate overall installations, even as higher-throughput alternatives gain traction in large-scale fulfillment environments.

Solution Type Insights

Automatic vertical lift modules constitute the dominant solution category, accounting for nearly 64% of the global market share in 2025, owing to their superior throughput and minimal human intervention. These systems operate on a fully autonomous goods-to-person model, enabling significantly higher retrieval rates than semi-automatic systems while improving consistency and accuracy. Automatic VLMs enhance workplace safety and ergonomics by eliminating repetitive manual handling and reducing labor dependency.

Seamless integration with WMS and ERP platforms supports advanced inventory optimization and real-time process control. Despite 40-60% higher capital costs, high-volume operations achieve ROI within 18-24 months, sustaining strong adoption. Ongoing integration of AI, predictive maintenance, and software-driven capabilities is expected to reinforce segment leadership through 2033.

Load Capacity Insights

Medium-duty vertical lift modules rated at 300-500 kg per tray dominate the market, accounting for approximately 43% share in 2025, reflecting their versatility across the widest range of industrial applications. This capacity range aligns with typical storage needs for automotive parts, e-commerce totes, pharmaceuticals, and general manufacturing components.

Medium-duty systems can be installed in standard warehouse environments without specialized structural reinforcement, significantly reducing deployment costs and complexity. Their standardized design enables economies of scale for manufacturers while ensuring consistent reliability for end users. These systems form the backbone of multi-industry VLM adoption, although demand for heavy-duty variants is rising, with systems above 500 kg projected to grow at a 12.6% CAGR through 2033.

Application Insights

Automotive manufacturing represents the largest application segment for vertical lift modules, accounting for approximately 29% of global demand in 2025, driven by just-in-time production and high component variability. Automotive plants require rapid, accurate retrieval of diverse parts to support multiple platforms and customization requirements.

VLM systems enable compact storage, high picking accuracy approaching 99.9%, and deterministic retrieval times aligned with assembly line sequencing. OEMs and tier suppliers increasingly deploy VLMs to reduce inventory footprint and improve material flow efficiency, achieving productivity gains of 20-30% in component staging operations. Continued growth in electric vehicle production and platform diversification is expected to sustain automotive manufacturing’s leading position through 2033.

Regional Insights

North America Vertical Lift Module Market Trends and Insights

North America holds a strong position with 29% share in the global vertical lift module market, supported by sustained investments in warehouse automation across e-commerce, automotive manufacturing, and healthcare logistics. The United States leads regional demand as logistics operators increasingly deploy VLM systems to mitigate persistent labor shortages and rising wage pressures in warehousing and manufacturing. Large e-commerce players are installing multi-unit VLM configurations in distribution centers to support same-day and next-day delivery requirements while improving order accuracy and space utilization.

The region benefits from a mature regulatory environment, well-established equipment supply chains, and advanced system integration capabilities with warehouse management and enterprise platforms. Cold chain warehouse modernization in food and beverage distribution is further supporting adoption of VLMs for temperature-controlled storage. Innovation leadership from U.S. and Canadian manufacturers positions North America as a technology hub, with strong emphasis on AI integration, predictive maintenance, and premium automation solutions.

Europe Vertical Lift Module Market Trends and Insights

Europe represents a mature and technologically advanced market for vertical lift modules, underpinned by a strong manufacturing base and a long-standing commitment to industrial automation. Germany plays a central role, where VLM systems are embedded within smart factory and Industry 4.0 initiatives aimed at enhancing manufacturing efficiency and competitiveness.

Italy has emerged as a global technology center for VLM development, with domestic manufacturers recognized for engineering precision, reliability, and modular system design.

European adoption is strongly influenced by regulatory focus on workplace safety, ergonomics, and labor protection, driving demand for automatic systems that reduce manual handling and injury risks. Urban logistics development across major European cities is also supporting VLM deployment, as space constraints and sustainability regulations encourage compact storage solutions. Additionally, nearshoring strategies and supply chain resilience initiatives are prompting manufacturers to invest in automated warehousing as a long-term competitive advantage.

Asia Pacific Vertical Lift Module Market Trends and Insights

Asia-Pacific is the fastest-growing regional market for vertical lift modules, projected to grow at a 12.3% CAGR through 2033, driven by rapid industrialization, e-commerce expansion, and tightening labor constraints. China dominates regional demand, accounting for approximately 43% of the market, supported by widespread greenfield smart factory construction and large-scale quick-commerce infrastructure development. VLM systems are increasingly integrated into electric vehicles, semiconductor, and advanced manufacturing facilities from the design stage.

India is emerging as a high-growth market, with adoption projected to grow at an estimated 8.91% CAGR, supported by industrial corridor development and investment in logistics infrastructure. Japan and South Korea are adopting VLMs as strategic responses to aging workforces and rising labor costs. ASEAN economies such as Vietnam, Thailand, and Indonesia are deploying automation-intensive warehouses from inception, creating strong opportunities for suppliers entering the region.

Competitive Landscape

The vertical lift module market is characterized by a moderately consolidated structure, with a limited number of established manufacturers accounting for a substantial share of global revenues. Competition is shaped by high entry barriers stemming from specialized engineering requirements, long product lifecycles, and the need for extensive after-sales service networks. Leading participants focus on technology differentiation, portfolio breadth, and global service coverage to secure long-term enterprise contracts, particularly with multinational customers.

Strategic priorities increasingly center on software-led value creation, including AI-enabled system optimization, predictive maintenance, and cloud-based fleet management platforms that generate recurring revenue.

Market consolidation is progressing through partnerships and technology alliances, especially with warehouse management system providers and robotics firms, enabling integrated automation solutions. Capacity expansion and regional manufacturing localization are key growth strategies, supporting faster delivery and reduced lifecycle costs in priority markets.

Meanwhile, emerging and regional players compete through energy-efficient designs, customization capabilities, and sustainability positioning, targeting niche applications and cost-sensitive customers while gradually strengthening their competitive footprint.

Key Developments:

- February 2025: Modula Inc. officially commenced construction on a 170,000-square-foot expansion to its Ohio facility, representing a US$ 36+ million investment designed to double production capacity and consolidate manufacturing and logistics operations, with completion targeted for early 2026 and annual capacity reaching 1,600 vertical lift modules.

- March 2024: Greenspace Industrial (Canada) launched the Modula VLM in North American markets, introducing fully computerized vertical storage systems employing goods-to-person principles and supporting operations on multiple levels simultaneously, addressing regional labor shortage mitigation and warehouse space optimization requirements.

Companies Covered in Vertical Lift Module Market

- Kardex Group

- Hänel Storage Systems

- Modula Inc. (System Logistics)

- SSI SCHÄFER Systems International Inc.

- Ferretto Group S.p.A.

- AutoCrib Inc.

- Weland Lagersystem AB

- Automha S.p.A.

- Stanley Black & Decker Storage Solutions

- Green Automated Solutions Inc.

- Intertex Maschinenbau GmbH

- ICAM srl

- Mecalux S.A.

- Godrej

- Koerber Logistics Solutions

- Daifuku

- Dematic Corporation

- Schaefer Group

- Jungheinrich

- Vidir Storage Systems

Frequently Asked Questions

The vertical lift module market is expected to reach US$ 2.0 million in 2026, growing from US$ 1.2 million in 2020 at a 9.7% CAGR driven by e-commerce growth, labor shortages, and space optimization needs.

Key drivers include rapid e-commerce fulfillment expansion, acute labor shortages in developed economies, urban space constraints, and AI- and IoT-enabled automation delivering ROI within 24 months.

North America and Europe dominate due to mature automation infrastructure, while Asia Pacific is the fastest-growing region at 12.3% CAGR driven by smart factories, industrial corridors, and quick-commerce growth.

Major opportunities lie in AI-enabled predictive maintenance, cloud-based warehouse platforms, robotics integration, and expansion into emerging markets and high-precision industries.

Leading manufacturers include Kardex Group, Modula Inc., SSI SCHÄFER, Hänel, and Ferretto Group, Stanley Black & Decker Storage Solutions, Godrej and Koerber Logistics Solutions.