- Biotechnology

- Vectorized Antibodies Market

Vectorized Antibodies Market Size, Share, and Growth Forecast 2026 - 2033

Vectorized Antibodies Market by Antibody Type (Monoclonal antibodies, Polyclonal antibodies, Recombinant antibodies, Others), by Vector (Viral vectors, Non-viral vectors, Others), by Application (Oncology, Infectious diseases, Autoimmune diseases, Neurological & rare diseases, Others), by End User (Pharmaceutical & biotechnology companies, Research laboratories & institutes, Hospitals & clinics), by Regional Analysis, 2026-2033

Vectorized Antibodies Market Size, Share, and Growth Forecast 2026 - 2033

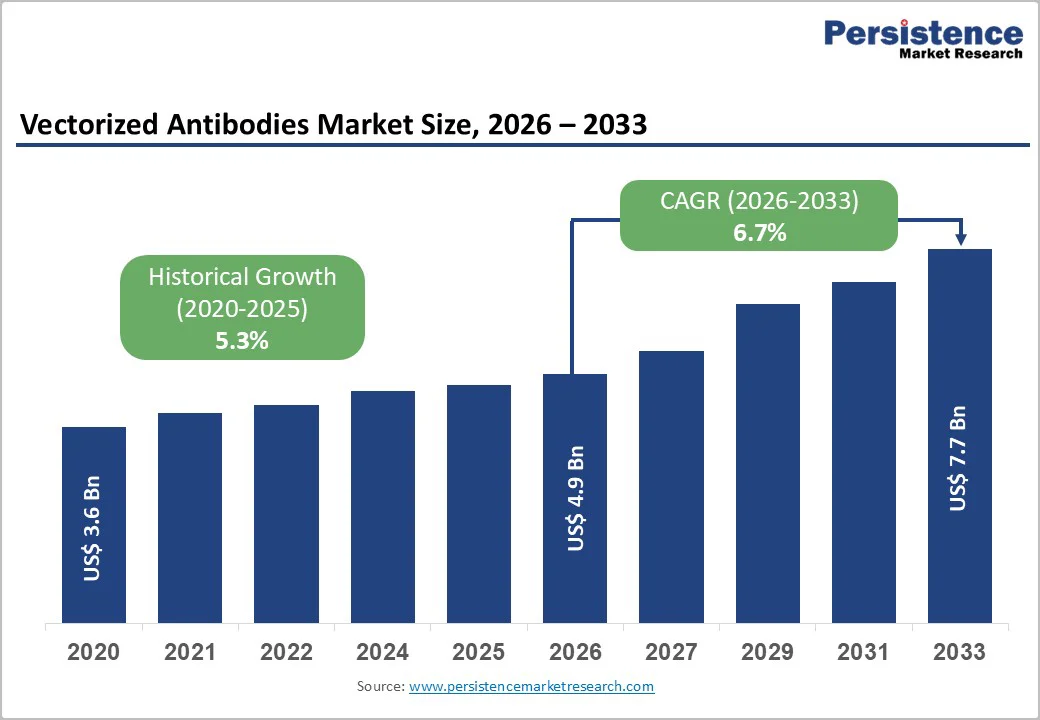

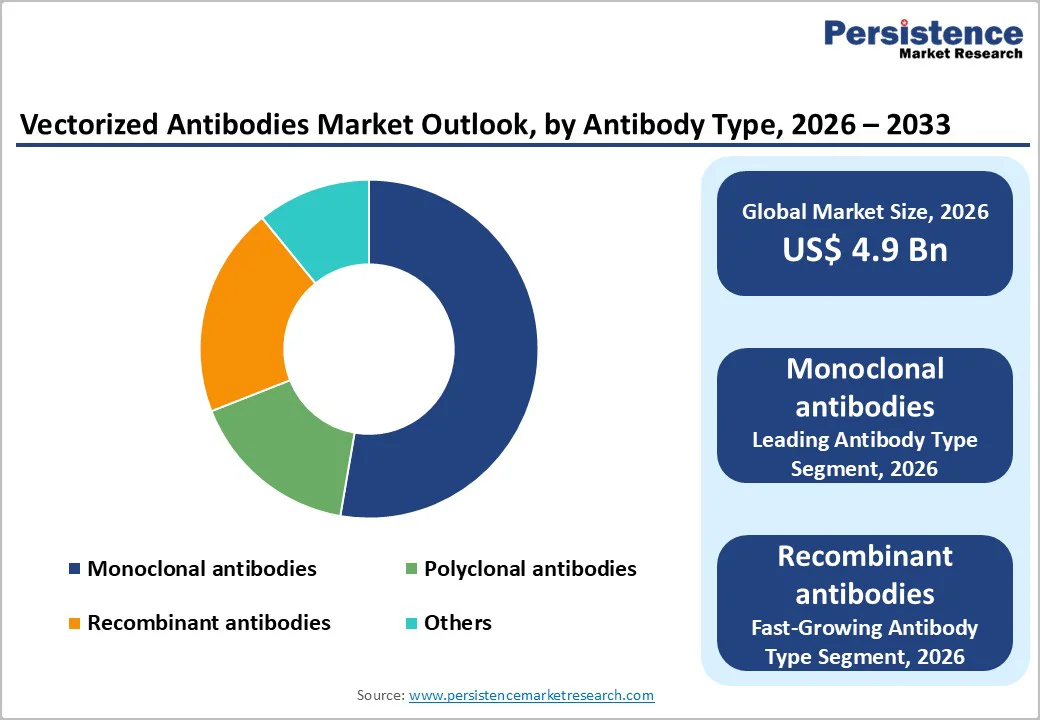

The global Vectorized Antibodies Market size is expected to be valued at US$ 4.9 billion in 2026 and projected to reach US$ 7.7 billion by 2033, growing at a CAGR of 6.7% between 2026 and 2033.

Rising demand for targeted gene therapies drives this expansion, as vectorized antibodies enable sustained in vivo expression, reducing frequent dosing needs. Advancements in viral vectors like AAV improve delivery efficiency, supported by increasing clinical trials in oncology and neurological diseases. Chronic disease prevalence, including cancer cases projected to rise 70% by 2040 per WHO, further accelerates adoption.?

Key Market highlights

- Vectorized antibodies enable long-term in-vivo antibody expression, reducing dosing frequency and improving patient compliance.

- Oncology remains the primary application, driven by targeted tumor suppression and combination therapy potential.

- Viral vectors dominate delivery methods due to high efficiency, durability, and clinical validation.

- Neurological and rare diseases are emerging rapidly with advances in blood–brain barrier–penetrating vectors.

- Strong regulatory support for gene therapies accelerates clinical development and approval timelines globally.

- Growing biotech investments are fueling innovation in vector engineering and antibody payload optimization.

- Single-dose treatment potential positions vectorized antibodies as cost-effective long-term therapeutic solutions.

| Key Insights | Details |

|---|---|

|

Vectorized Antibodies Market Size (2026E) |

US$ 4.9 billion |

|

Market Value Forecast (2033F) |

US$ 7.7 billion |

|

Projected Growth CAGR(2026-2033) |

6.7% |

|

Historical Market Growth (2020-2025) |

5.3% |

Market Dynamics

Advancements in Gene Delivery Technologies

Innovations in viral vectors, particularly AAV and lentiviral systems, propel the vectorized antibodies market by enhancing transduction efficiency and safety profiles. AAV vectors achieve episomal persistence for long-term antibody expression without genomic integration risks, as demonstrated in preclinical models reducing tumor growth via VEGF inhibition. Clinical successes, like Pfizer/BioNTech mRNA strategies achieving 94% efficacy, underscore vector potential in sustained delivery. These technologies bypass blood-brain barriers, enabling CNS applications, with non-human primate studies showing robust retinal transduction. Such progress supports scalable manufacturing, fostering broader therapeutic adoption in chronic conditions.?

Rising Prevalence of Chronic Diseases

The surge in oncology, autoimmune, and infectious diseases fuels demand for precise therapies, with vectorized antibodies offering targeted, durable responses. WHO reports cancer incidence rising 70% over two decades, straining traditional treatments. Vectorized platforms address this by enabling in situ antibody production, as seen in glioblastoma models where AAVrh.10 vectors reduced tumors synergistically with chemotherapy. Increased healthcare spending and biologics shift amplify growth, positioning vectorized antibodies as vital for unmet needs in rare diseases.?

Restrains- High Development and Production Costs

Complex manufacturing of vectorized antibodies imposes significant barriers, with specialized GMP facilities for viral vectors driving expenses. Production requires expertise in molecular biology, escalating costs for scalability. Lentiviral and AAV processes demand bioreactors and quality controls, limiting small biotechs. Pre-existing immunity triggers innate responses via PAMPs, complicating transduction and necessitating costly immunomodulation.?

Regulatory and Immunogenicity Challenges

Stringent approvals for gene therapies delay commercialization, as vectors face scrutiny for insertional mutagenesis and off-target effects. FDA and EMA demand extensive non-clinical data, prolonging timelines. Immune restrictions like APOBEC3G block lentiviral integration, reducing efficacy by up to 90% in some cells. Preclinical toxicity studies add hurdles, deterring investment.?

Opportunity- Oncology and Neurological Gene Therapies

The vectorized antibodies market presents strong growth opportunities driven primarily by advances in oncology and neurological gene therapies. In oncology, vectorized antibodies are increasingly used to target tumor-specific pathways such as VEGF and EGFR, enabling sustained in-vivo antibody expression. Clinical studies using platforms like AAVrh.10 have demonstrated synergistic effects when combined with chemotherapy, enhancing treatment efficacy and durability. Industry data indicate that over 42% of gene therapy vectors are currently focused on oncology, highlighting its dominance as a development area. Rising biotech investments in China and India, along with regulatory momentum such as FDA approvals for candidates like 4D-150, further support market expansion. Strategic collaborations, including partnerships with Eli Lilly to improve CNS delivery, are accelerating innovation and commercialization timelines through 2033.

In parallel, neurological and rare diseases represent a rapidly emerging opportunity. Advances in blood–brain barrier-penetrating vectors have enabled new treatment approaches for conditions such as ALS. Significant funding activity, including VectorY Therapeutics’ €129 million raise in 2024, and FDA clearance of early-phase trials for vectorized ALS antibodies, underscore growing confidence in this segment. AAV-based platforms enabling intravitreal and CNS delivery, supported by strong Asia-Pacific R&D growth, position neurological applications as a key long-term growth driver.

Category-wise Insights

By Antibody Type, Monoclonal antibodies Segment is leading in the Market

Monoclonal antibodies account for the highest market share because they offer high specificity, consistent performance, and strong clinical effectiveness across multiple disease areas. These antibodies are designed to target a single, well-defined antigen, which reduces off-target effects and improves safety compared with polyclonal products. Monoclonal antibodies are extensively used in oncology, autoimmune diseases, infectious diseases, and inflammatory disorders, making them central to modern biologic therapy. A large number of regulatory-approved monoclonal antibody drugs are already available, and many are included in standard treatment guidelines, supporting widespread adoption. Strong pharmaceutical industry investment, along with well-established manufacturing processes, has enabled large-scale production and global commercialization. Additionally, monoclonal antibodies benefit from long patent lifecycles, premium pricing, and high reimbursement acceptance in major markets, which significantly boosts revenue share. Continuous innovation, such as antibody-drug conjugates and bispecific monoclonal antibodies, further strengthens their dominance. Their proven clinical success, combined with physician familiarity and expanding indications, ensures sustained demand and reinforces monoclonal antibodies as the leading segment in the vectorized antibodies and broader antibody therapeutics market.?

By Vector, Monoclonal antibodies Segment is leading in the Market

Viral vectors account for the highest share in the vectors segment because they offer superior gene-delivery efficiency, long-term expression, and proven clinical reliability compared with non-viral alternatives. Platforms such as adeno-associated viruses (AAVs) and lentiviral vectors are highly effective at delivering antibody-encoding genes directly into target cells, enabling sustained in-vivo production of therapeutic antibodies after a single administration. These vectors exhibit strong tissue tropism, allowing precise targeting of organs such as the liver, eye, muscle, and central nervous system, which is critical for oncology, neurological, and rare disease applications.

Viral vectors also benefit from a well-established regulatory and manufacturing ecosystem, with multiple FDA-approved gene therapies already using AAV or lentiviral platforms, increasing physician and developer confidence. Extensive clinical validation, scalable production capabilities, and growing investment in viral vector manufacturing facilities further strengthen adoption. Additionally, ongoing innovations in capsid engineering and vector design have improved safety, reduced immunogenicity, and expanded therapeutic reach. Together, these factors make viral vectors the most mature, effective, and commercially viable delivery option, driving their dominant market share in the vectorized antibodies market.

Regional Insights

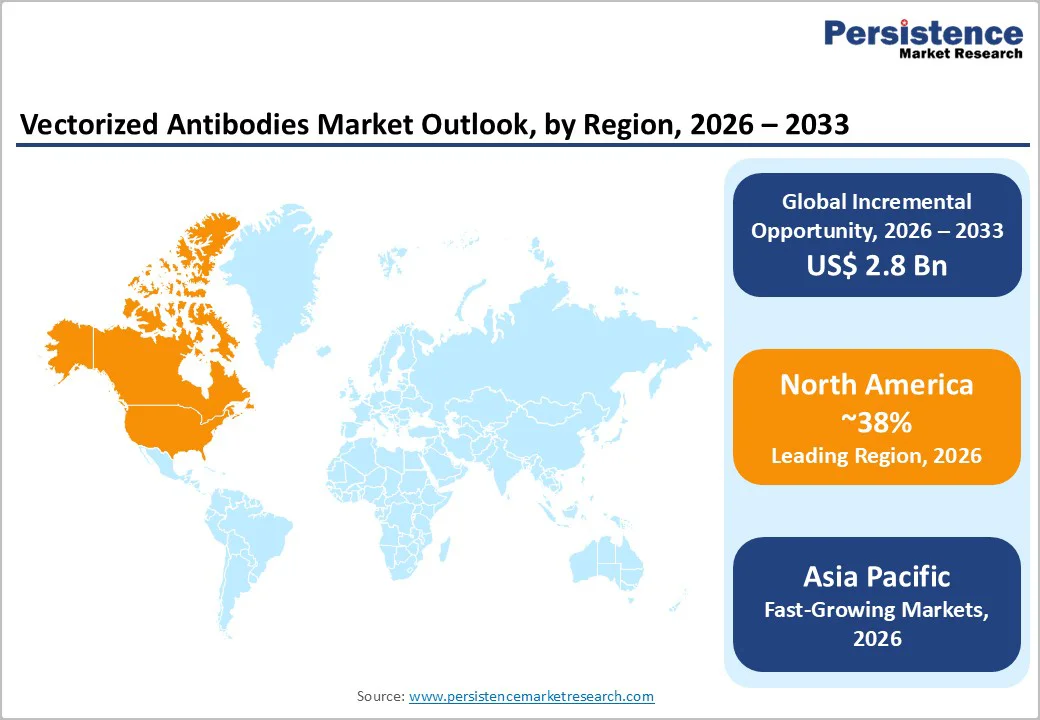

North America Vectorized Antibodies Market Trends

The North America vectorized antibodies market is witnessing strong momentum, driven by rapid innovation in gene therapy, robust clinical pipelines, and favorable regulatory support. The region benefits from a highly developed biotechnology ecosystem, advanced viral vector manufacturing capacity, and strong collaboration between academic institutions and biopharmaceutical companies. Increasing focus on in-vivo antibody expression for oncology, ophthalmology, and neurological disorders is accelerating adoption of AAV-based platforms. North America also leads in early-phase and late-stage clinical trials for vectorized antibodies, supported by significant venture capital funding and strategic partnerships.

From a U.S. perspective, the market is particularly shaped by FDA regulatory leadership, with clear guidance on gene therapy development, fast-track designations, and orphan drug incentives encouraging innovation. The U.S. hosts many key developers working on next-generation vectorized antibody programs targeting cancer, ALS, and retinal diseases. Rising investment in domestic viral vector manufacturing and CDMO capabilities is reducing supply bottlenecks and enabling faster commercialization. Additionally, strong reimbursement potential for breakthrough biologics and growing demand for long-acting, single-dose therapies are reinforcing market growth. Collectively, these factors position North America—especially the U.S. as a global hub for vectorized antibody development and commercialization.

Asia Pacific Vectorized Antibodies Market Trends

The Asia Pacific vectorized antibodies market is emerging as a high-growth region, supported by expanding biotechnology capabilities, rising healthcare investment, and increasing focus on advanced gene therapies. Countries such as China, Japan, South Korea, and India are strengthening their positions through government-backed biotech programs, favorable regulatory reforms, and growing clinical research activity. The region is witnessing increasing adoption of viral vector–based antibody delivery for oncology and rare disease indications, driven by the need for cost-effective, long-lasting treatment options. Rapid expansion of local biopharmaceutical manufacturing infrastructure and partnerships with global biotech firms are further accelerating technology transfer and commercialization.

Asia Pacific also benefits from a large patient population and rising incidence of cancer and neurological disorders, creating strong demand for innovative therapies. Regulatory agencies across the region are streamlining approval pathways for gene and cell therapies, enabling faster entry into clinical development. Additionally, growing investment from domestic venture capital and multinational pharmaceutical companies is supporting early-stage research in vector engineering and antibody design. Increasing participation in global clinical trials and improving healthcare access position Asia Pacific as a key emerging market, expected to contribute significantly to the long-term growth of the global vectorized antibodies market.

Competitive Landscape

Market Structure Analysis

The competitive landscape of the vectorized antibodies market is characterized by intense innovation, early-stage clinical development, and strategic collaborations aimed at advancing in-vivo antibody expression technologies. Market competition is driven by continuous improvements in viral vector engineering, antibody optimization, and tissue-targeting capabilities to enhance efficacy and safety. Companies are focusing on differentiated platforms that enable long-lasting antibody production with single-dose administration, particularly in oncology and neurological disorders. Strategic partnerships with academic institutions, contract development organizations, and large pharmaceutical players are accelerating clinical progress and reducing development risks.

Key Market Developments

- In September 2025, VectorY Therapeutics entered into an option and license agreement that granted the company an exclusive option to evaluate Shape’s deep-brain-penetrating adeno-associated virus (AAV) capsid, SHP-DB1, for vectorized antibody payloads targeting three therapeutic indications. Upon successful evaluation, VectorY could obtain an exclusive license to use SHP-DB1 for the delivery of vectorized antibodies against these targets.

Companies Covered in Vectorized Antibodies Market

- 4D Molecular Therapeutics

- AbbVie

- Adverum Biotechnologies

- AstraZeneca

- BioNTech

- CureVac

- Eli Lilly and Company

- Genmab

- GlaxoSmithKline (GSK)

- Generation Bio

- Adagio Therapeutics

- Voyager Therapeutics

- VectorY Therapeutics

- Vironexis

Frequently Asked Questions

The global Vectorized Antibodies Market is expected to reach US$ 4.9 billion in 2026.

Key drivers include advancements in AAV delivery and rising chronic disease prevalence, like cancer surges per WHO.

North America holds the leading 38% share in 2025, powered by U.S. biotech innovation.

Oncology gene therapies hold significant potential, with vectors that effectively inhibit tumors.

Leaders include 4D Molecular Therapeutics, AbbVie, VectorY Therapeutics, and Voyager Therapeutics.