- Automotive Components & Materials

- V-Belt Market

V-Belt Market Size, Share, and Growth Forecast, 2026 - 2033

V-Belt Market by Material Type (Rubber, Polymer, Polyurethane, Neoprene), End-user (Automotive, Industrial, Agriculture,), End-User (Original Equipment Manufacturer, Aftermarket), and Regional Analysis for 2026-2033

V-Belt Market Share and Trends Analysis

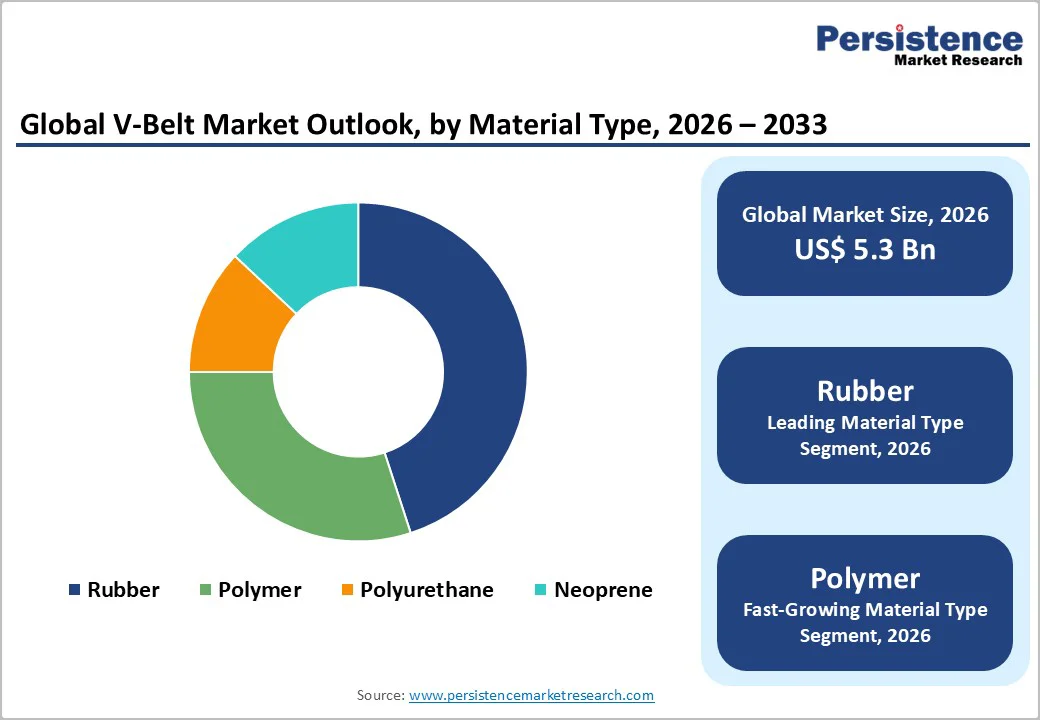

The global V-belt market size is likely to be valued at US$ 5.3 billion in 2026, and is estimated to reach US$ 6.7 billion by 2033, growing at a CAGR of 5.2% during the forecast period 2026−2033. Steady replacement demand from aging industrial machinery, ongoing expansion of automotive and agricultural equipment fleets, and the need for cost-effective solutions to transmit mechanical power all drive consistent volume growth. As industries modernize, investments in industrial automation, heating, ventilation, and air conditioning (HVAC), and advanced material handling systems further boost demand, particularly in Asia Pacific and other emerging manufacturing centers where production capacity is rapidly expanding. Technological advancements are also gradually transforming the market landscape, aided by a clear shift toward higher-efficiency belt designs and more durable materials, which are being adopted across both original equipment manufacturer (OEM) and aftermarket channels.

Key Industry Highlights

- Dominant & Fastest-growing Materials: Rubber is likely to lead with about 35% market revenue share in 2026, while polymer is poised to be the fastest-growing between 2026 and 2033.

- Leading & Fastest-growing End-Users: Automotive is slated to command around 42.3% of the revenue share in 2026, with the industrial segment expanding the fastest from 2026 to 2033.

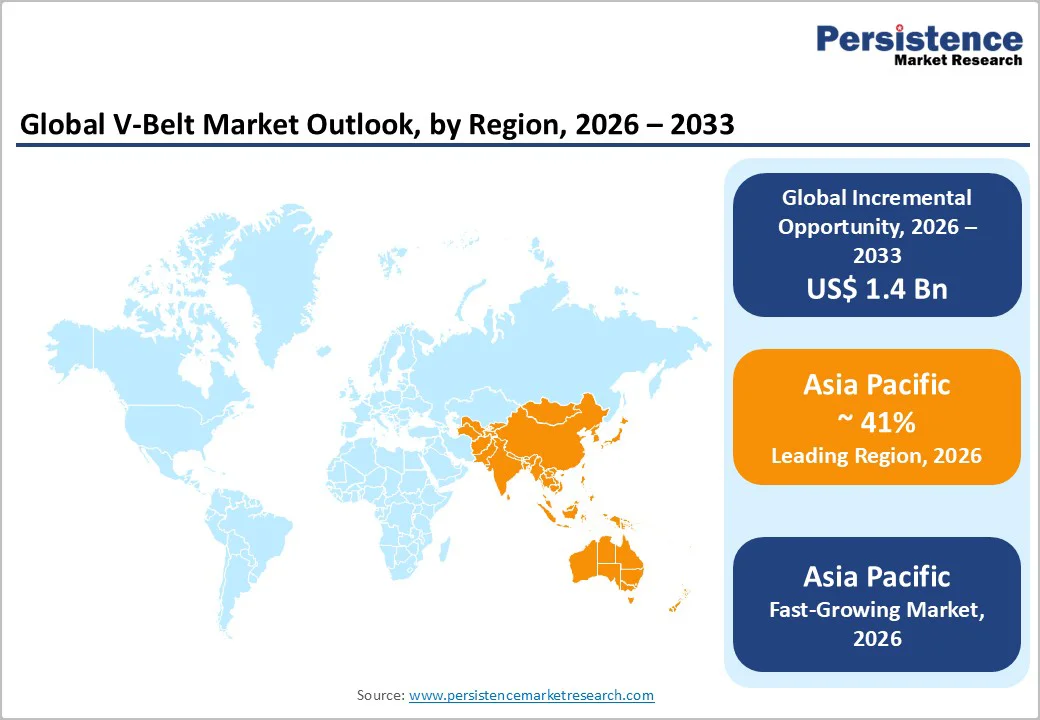

- Dominant Region: North America is expected to command about 41% market share in 2026, supported by deep-rooted manufacturing strengths.

- Fastest-growing Regional Market: Asia Pacific is poised to be the fastest-growing market through 2033, due to the large-scale production of machinery, vehicles, and agricultural equipment in China and India.

- Key Driver: Industrialization and automation enable factories, plants, and infrastructure systems to operate equipment for longer hours, creating a steady demand for V-belts.

- Major Opportunities: In several emerging economies, industries are increasing the number of machines, vehicles, and farm equipment, which rely on V-belts to keep running smoothly, opening new market opportunities.

| Key Insights | Details |

|---|---|

| V-Belt Market Size (2026E) | US$ 5.3 Bn |

| Market Value Forecast (2033F) | US$ 6.7 Bn |

| Projected Growth (CAGR 2026 to 2033) | 5.2% |

| Historical Market Growth (CAGR 2020 to 2025) | 4.9% |

Market Factors – Growth, Barriers, and Opportunity Analysis

Industrialization to Drive V-Belt Demand through Installed Base Expansion

Rapid industrialization and automation mean factories, processing plants, and infrastructure assets now operate more motors, compressors, pumps, conveyors, fans, and machine tools for longer hours than ever before. V-belt drives sit between these motors and driven components. They provide a simple, flexible way to transmit power across a broad mix of applications, from light workshop machinery to heavy industrial equipment. Operations and maintenance leaders often view them as a practical default for many drive systems. This preference stems from straightforward installation, affordable stocking, and easy replacement during planned shutdowns. For capital projects and line upgrades, V-belts balance upfront cost, design simplicity, and service ease across multi-site portfolios.

Once equipment is in place, the installed base becomes a recurring source of demand as teams work to keep production stable and avoid unplanned downtime. Maintenance staff routinely inspect belt condition, verify alignment, adjust tension, and change components that show wear or slippage. They integrate these tasks into preventive or predictive maintenance schedules. Every additional shift, throughput increase, or new production line adds to the population of drives that will eventually require replacement. This creates a consistent aftermarket pull. Operators who standardize belt types, optimize spares inventories, and collaborate with suppliers on upgrade paths to more efficient or longer-life designs can lower lifecycle costs while improving uptime and energy performance.

Raw Material Volatility and Low-Quality Substitutes to Make Vendor Protocols Stricter

V-belts are primarily manufactured using rubber and synthetic polymers, such as neoprene or polyurethane, as their main components. These materials are combined with reinforcing cords and fabrics to enhance strength and durability. The cost of producing V-belts is highly sensitive to fluctuations in the prices of these raw materials. Natural rubber is sourced from rubber plantations, while synthetic polymers are derived from petrochemical feedstock. Both types of inputs are subject to volatility caused by global supply chain disruptions, changes in energy markets, and environmental factors affecting plantation yields. When input prices spike, belt manufacturers experience reduced profit margins, which can limit their ability to invest in research and development or expand production facilities.

In certain regions, the market is flooded with low-cost V-belts that may not consistently meet established performance and durability standards. This often results in unreliable drive performance, increased equipment failures, and higher maintenance requirements for end users. To mitigate these risks, leading equipment manufacturers and large industrial customers implement rigorous supplier qualification processes. They maintain approved vendor lists and enforce strict testing protocols before integrating V-belts into their systems. These measures help ensure system reliability and protect the reputation of their brands by minimizing the risk of operational disruptions due to substandard components.

Industrial Growth in Developing Economies to Fuel V-Belt Aftermarket Surge

Emerging economies rapidly expand their industrial sectors by deploying more machines, vehicles, and agricultural equipment, all of which depend on V-belts for smooth operation. Factories, transport fleets, and farming operations build a vast installed base of active machinery. This base generates steady replacement needs as belts wear from continuous use. Aftermarket demand accelerates with higher equipment utilization rates and prolonged operational hours. Manufacturers gain a strategic edge by prioritizing durable, application-specific belts to capture this expanding segment.

This trend stands out in nations such as China, India, Southeast Asia, Latin America, the Middle East, and Africa, where construction booms and infrastructure investments thrive. Operators face greater reliance on prompt, dependable spare belts amid extended plant shifts and longer fleet routes. Distributors succeed by stocking locally suited products and streamlining supply chains for fast delivery. Forward-thinking suppliers focus here to secure long-term revenue, as original equipment sales yield to recurring aftermarket volumes. Clients benefit from tailored solutions that cut downtime and boost productivity.

Category-wise Analysis

Material Type Insights

Rubber is set to command approximately 35% of the V-belt market revenue share in 2026. This dominance stems from its optimal balance between performance and cost for most applications. Its inherent flexibility and resilience enable belts to conform precisely to pulleys, maintain reliable grip, and dampen vibration effectively. These characteristics ensure smooth, quiet drive operation across diverse settings. Rubber compounds tolerate routine temperature fluctuations and absorb shock loads without degradation. This versatility allows a single construction to serve workshops, factories, agricultural equipment, and vehicles with minimal modification. Advanced reinforcements and enhanced rubber formulations further improve wear resistance, stabilize performance under heat and oil exposure, and significantly extend operational life.

Polymer is likely to emerge as the fastest-growing material from 2026 to 2033. Modern machinery demands lighter yet stronger components, driving this shift. Polymer V-belts excel in resisting wear, chemicals, and severe environmental conditions compared with traditional alternatives. This superior durability makes them ideal for challenging industrial environments where heat, oils, and contaminants are prevalent. Their consistent performance maintains drive stability and reliability even under extreme operating conditions. Machine builders increasingly specify polymer belts to reduce weight, extend maintenance intervals, and improve overall system efficiency in demanding applications.

End-User Insights

Automotive applications are expected to dominate the V-belt market landscape with an estimated 42.3% revenue share in 2026. V-belts serve as critical engine and accessory components, powering systems such as the alternator, water pump, and air conditioning (AC) compressor. These components ensure reliable vehicle operation in everyday driving conditions. Modern vehicle designs impose stricter requirements for durability, noise reduction, and compact packaging. The global vehicle fleet continues to expand steadily, creating substantial aftermarket opportunities. Service networks increasingly prioritize preventive maintenance programs to extend component life and reduce unexpected failures. This shift toward proactive replacement strategies ensures consistent demand for high-quality automotive belts that meet evolving performance standards.

Industrial applications are anticipated to grow the fastest from 2025 to 2033. Manufacturers deploy V-belts extensively in conveyors, compressors, pumps, and production machinery where they deliver dependable power transmission and operational adaptability. The accelerating adoption of industrial automation and smart manufacturing technologies drives demand for premium V-belts that maintain consistent efficiency and minimize production interruptions. Companies invest heavily in equipment upgrades and process optimization to enhance competitiveness. These investments require advanced belt solutions that withstand intensive operating cycles, reduce energy consumption, and support predictive maintenance systems. Forward-thinking suppliers position themselves to capture this growth by developing application-specific products that align with Industry 4.0 requirements.

Distribution Channel Insights

The OEM segment is expected to command approximately 60% of the V-belt market share in 2026. This leadership results from the integration of V-belts into newly produced machinery, vehicles, and equipment during assembly. OEMs emphasize high-quality, durable, and reliable components that meet strict performance specifications and regulatory standards. Ongoing manufacturing expansion and the continuous introduction of advanced machinery and vehicle models sustain robust demand in this segment. Furthermore, increasing adoption of innovative materials and customized product designs allows OEMs to tailor solutions for specific performance requirements, boosting reliability and enhancing brand differentiation across industries.

The aftermarket segment is projected to be the fastest-growing during the forecast period 2026-2033. Every V-belt installed in operational machinery or vehicles eventually experiences wear and requires replacement to maintain efficiency and uptime. With global growth in manufacturing, logistics, and agricultural activities, the number of assets operating daily continues to rise, expanding the installed base that drives recurring replacement cycles. This recurring nature of aftermarket demand provides a stable revenue stream that is less dependent on new equipment production. Both global manufacturers and regional distributors view this trend as a long-term opportunity to strengthen customer relationships through locally available, application-specific, and rapid-response replacement belt solutions.

Regional Insights

Asia Pacific V-Belt Market Trends

Asia Pacific is predicted to lead the V-belt market with an estimated 41% share in 2026. This dominance stems from the region’s large-scale industrial activity, rapid economic expansion, and well-established manufacturing ecosystems. Dense networks of factories, industrial parks, and supply chains depend heavily on belt-driven equipment for production, material handling, and utility systems. Significant investments in infrastructure projects, including roads, rail, ports, power, and construction materials, widen demand as more conveyors, pumps, compressors, and mixers are deployed and operated for extended periods. The widespread and continuous use of belt-driven systems makes belt consumption a foundational element of the region’s industrial economy.

China and India serve as key production and export centers for machinery, vehicles, and agricultural equipment. V-belts are integrated into a broad range of platforms during manufacturing, and their repeated replacement throughout the operational life of these assets further amplifies demand. Japan contributes to high-end demand by producing advanced automotive and industrial machinery that often requires premium belt specifications. As agricultural mechanization and modern farming practices spread across Asia Pacific, more tractors, harvesters, and stationary equipment are put into service, expanding the installed base of belt-dependent machinery.

Europe V-Belt Market Trends

Europe holds a robust position in the market for V-belts, as regional automotive and industrial equipment manufacturers specify highly engineered solutions for precision machinery, vehicles, and automated production lines. These customers look for belts that deliver high efficiency, low noise, and long service life, and they often collaborate directly with suppliers on application-specific designs. The region’s strong engineering tradition encourages close technical partnerships between V-belt producers and OEMs, which helps align product performance with demanding quality standards. For suppliers, success in Europe usually requires strong design support, co-engineering capabilities, and the ability to validate performance through rigorous testing.

Regulatory harmonization through European Union (EU) frameworks, including the Registration, Evaluation, Authorisation and Restriction of Chemicals (REACH) regulation and machinery safety directives, shapes material selection and product design. These rules push manufacturers toward compliant, lower emission compounds and safer constructions, which in turn favor experienced producers that can formulate advanced rubber and polymer blends. Competition in the region features established local brands and multinational groups that differentiate through engineering support, customization, and integration into OEM supply chains. Investment priorities in sustainability, automation, and digitalization create openings for premium and smart belt offerings, such as products with higher energy efficiency, longer replacement intervals, and compatibility with condition monitoring systems.

North America V-Belt Market Trends

North America represents a mature, high-value market for V-belts, supported by its advanced industrial sectors and extensive history of manufacturing. The United States and Canada are the primary demand centers, where belt-driven systems are integral to factories, processing plants, HVAC installations, agriculture, and transportation. A robust network of OEMs and their suppliers integrates V-belts into new machinery and vehicles. Simultaneously, a well-developed aftermarket, consisting of distributors and service providers, manages consistent replacement demand from the vast installed base of equipment.

Regulatory mandates and technological advancements are key factors shaping regional demand. Energy efficiency standards and emissions regulations compel operators to adopt high-performance belts that minimize power loss, reduce operational noise, and improve drive reliability. This trend is particularly evident in industrial and HVAC applications. The region also leads in adopting smart technologies. For instance, predictive maintenance platforms and IoT-enabled monitoring systems allow users to track belt condition in real time, schedule replacements proactively, and prevent unplanned operational downtime.

Competitive Landscape

The global V-belt market structure exhibits intense competition and considerable fragmentation, with leading manufacturers such as Gates Corporation, Continental AG, The Timken Company, and Mitsuboshi Belting Ltd. together commanding around 45% of the total market share. This concentration among key players reflects both the capital requirements for manufacturing scale and the technical expertise needed for product development. However, the remaining market remains distributed across regional producers, specialized suppliers, and emerging competitors. This landscape creates distinct competitive pressures. Established manufacturers leverage their scale, brand recognition, and distribution networks to defend market position, while mid-sized and regional players compete on cost, customization, and local customer relationships.

Industry leaders are pursuing multifaceted strategies to strengthen their competitive standing. Product innovation remains central, with manufacturers investing heavily in R&D to build high-performance V-belts featuring enhanced durability, improved energy efficiency, and superior resistance to extreme operating conditions. Strategic partnerships with OEMs and system integrators enable suppliers to influence specifications during the product design phase. Market expansion into emerging economies, particularly in Asia Pacific and Latin America, provides growth avenues beyond mature developed regions. The integration of smart technologies has also rapidly emerged as a critical differentiator.

Key Industry Developments

- In October 2025, Ammega announced the development of mass-produced circular belting solutions that use recycled materials and closed-loop designs to cut waste and reduce carbon footprint, with an aim of scaling these technologies across conveyor and power transmission belts.

- In August 2025, Universal Rubber Belts Manufacturing opened a high-specification production hub in Dubai to provide locally made, precision-engineered rubber belts for automotive and industrial customers across the Gulf Cooperation Council (GCC), improving supply chain resilience and shortening lead times.

- In June 2025, Hutchinson entered the bicycle drivetrain market with its Crossdyn belt-drive system for e-bikes and urban bikes, drawing on decades of belt-production experience in automotive and industrial applications.

Companies Covered in V-Belt Market

- Gates Corporation

- Continental AG

- SKF Group

- The Timken Company

- Fenner Drives

- Optibelt GmbH

- Mitsuboshi Belting Ltd.

- Bando Chemical Industries, Ltd.

- Dayco Products LLC

- Pix Transmissions Ltd.

- Megadyne

- Goodyear Rubber Products

- Tsubakimoto Chain Co.

- Volta Belting Technology Ltd.

Frequently Asked Questions

The global V-belt market is projected to reach US$137.2 Billion in 2026.

Industrialization and automation across manufacturing, automotive, and agriculture, combined with recurring replacement needs in a growing installed base of belt‑driven equipment, are driving the market.

The market is poised to witness a CAGR of 5.2% from 2026 to 2033.

Creating high‑performance and eco‑friendly belt designs, expanding aftermarket services in emerging economies, and integrating smart, maintenance‑oriented solutions with digital monitoring capabilities can open novel market opportunities.

Gates Corporation, Continental AG, The Timken Company, Mitsuboshi Belting Ltd. are some of the key players in the market.