- Technology

- UVC LED Market

UVC LED Market Size, Share, and Growth Forecast, 2026 - 2033

UVC LED Market by Power Output (Low Power (1–50 mW), Medium Power (50–100 mW), High Power (>100 mW), Application (Water Disinfection / Purification, Air Disinfection / Purification, Food & Beverage Processing, Medical Equipment Sterilization, Surface Disinfection, Miscellaneous (Object/Tool, Lab, Consumer Electronics, Others),End User (Residential, Commercial, Industrial), and Regional Analysis for 2026 - 2033

UVC LED Market Size and Trends Analysis

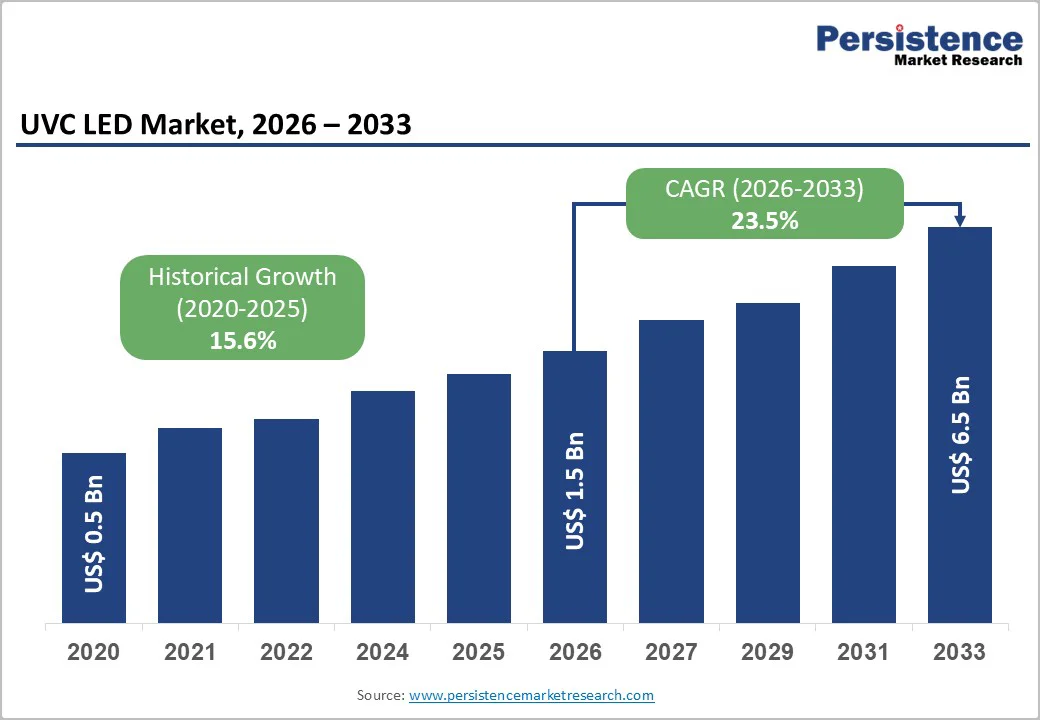

The Global UVC LED Market size was valued at US$1.5 billion in 2026 and is projected to reach US$6.5 billion by 2033, growing at a CAGR of 23.5% between 2026 and 2033. This exceptionally rapid expansion reflects the convergence of three critical market forces: stringent regulatory mandates phasing out mercury-containing lamps across developed economies, technological breakthroughs enabling higher-power UV-C LED outputs with extended operational lifespans, and accelerating global demand for chemical-free, energy-efficient disinfection solutions across water treatment, air purification, and healthcare applications.

The transition from legacy mercury-vapor lamp technology to solid-state UV-C LED solutions is driven by environmental regulations EU RoHS exemption expiring February 2027, Minamata Convention mercury phase-out commitments, and expanding US state-level fluorescent lamp bans and economic advantages including instantaneous on/off capability versus 15-minute mercury lamp warmup periods, reduced maintenance costs, and elimination of mercury contamination risks.

Key Industry?Highlights:

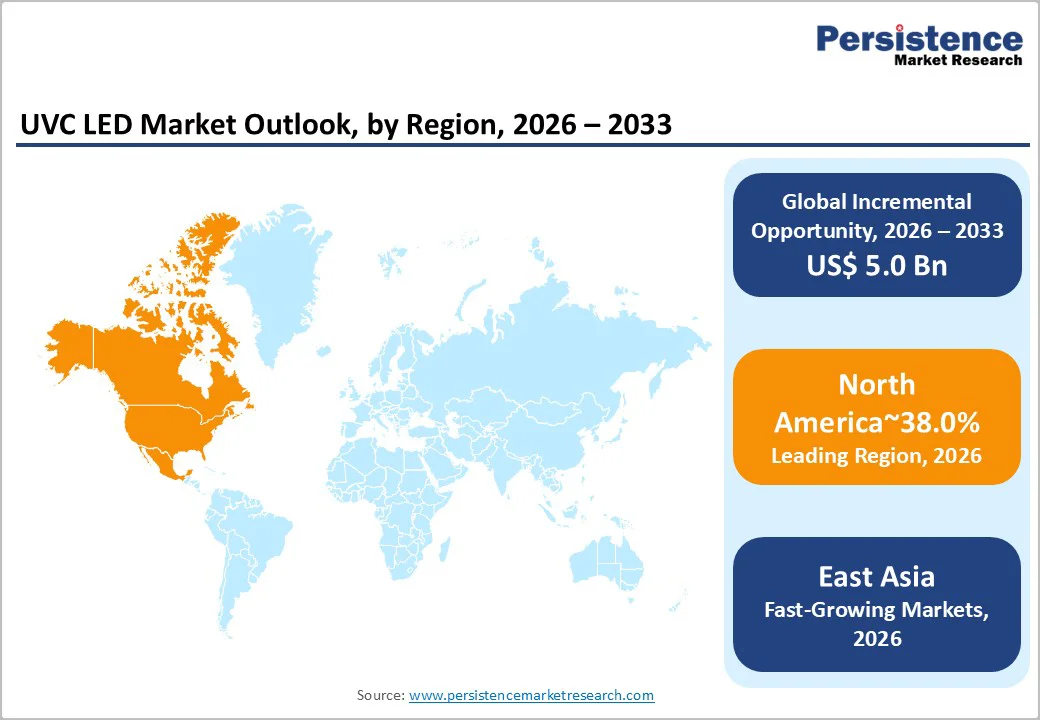

- Regional Leadership: North America leads with ~38% market share, driven by advanced healthcare infrastructure, regulatory mercury phase-out, and strong consumer adoption of UV-C LED devices.

- Fastest Growth Region: East Asia holds ~26% share and exhibits the fastest growth due to China’s water infrastructure modernization, government health initiatives, and semiconductor manufacturing capacity.

- European Market: Europe accounts for ~22% share, propelled by stringent environmental regulations, EU Mercury Regulation 2024/1849, and high institutional adoption in healthcare and water treatment.

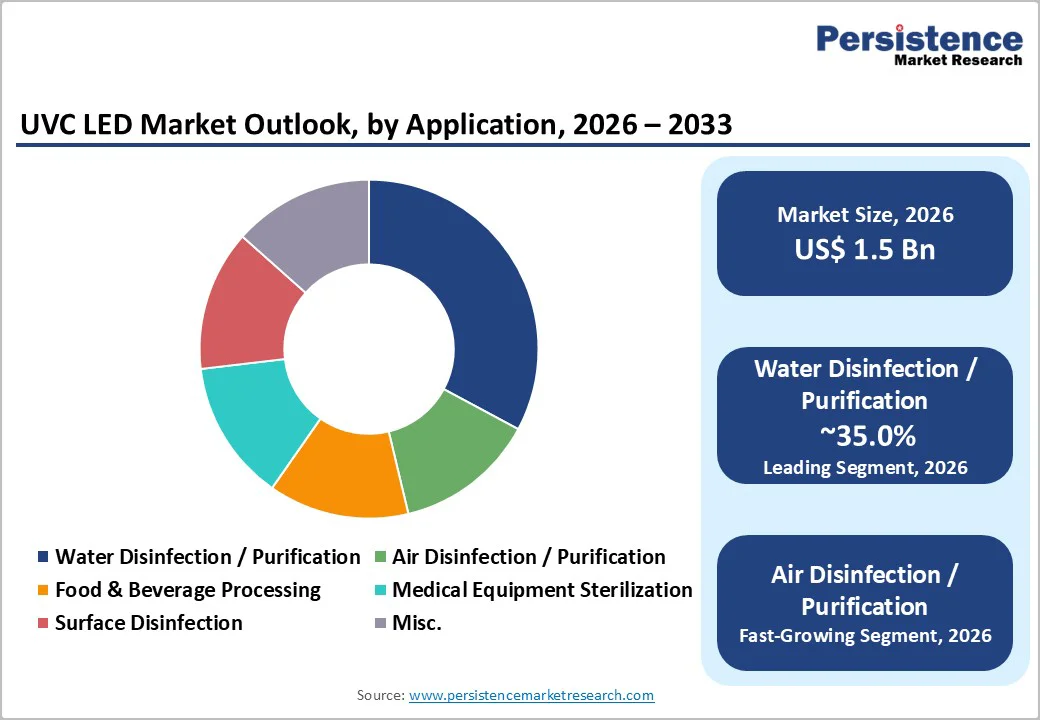

- Leading Application Segment: Water disinfection dominates with ~35% share, reflecting regulatory mandates and established use in municipal, industrial, and decentralized treatment systems.

- Fastest Expanding Segment: Air disinfection and purification is the fastest-growing application, driven by pandemic awareness, indoor air quality mandates, and institutional adoption in healthcare and high-occupancy spaces.

- Power Output Trends: Low-power LEDs (1–50 mW) dominate ~46% of the market, while high-power LEDs are rapidly expanding due to technological breakthroughs enabling single-device primary disinfection.

| Global Market Attributes | Key Insights |

|---|---|

| UVC LED Market Size (2026E) | US$ 1.5 Bn |

| Market Value Forecast (2033F) | US$ 6.5 Bn |

| Projected Growth (CAGR 2026 to 2033) | 23.5% |

| Historical Market Growth (CAGR 2020 to 2025) | 15.6% |

Market Dynamics

Growth Drivers

Regulatory Phase-Out of Mercury-Containing Disinfection Systems

Government mandates and international treaties are systematically eliminating mercury-containing lamp technologies, creating structural demand for the UVC LED Market as the primary mercury-free alternative. The Minamata Convention on Mercury, signed in 2013 and enforced since August 2017, establishes binding international commitments requiring signatory nations to phase out mercury use across multiple product categories, with particular emphasis on lighting applications where technically viable alternatives exist.

The European Union's revised Mercury Regulation (2024/1849), effective July 2024, specifies a critical decision point on February 24, 2027, when existing exemptions for mercury-containing UV discharge lamps for disinfection purposes expire, and the European Commission will assess whether to renew, narrow, or eliminate the exemption with industry analysis indicating realistic extension probability to 2032 but increasing likelihood of complete phase-out thereafter.

In North America, the United States Environmental Protection Agency (EPA) maintains regulatory focus on mercury inventory tracking through the Toxic Substances Control Act (TSCA), with no comprehensive ban currently in place but enforcement discretion creating market uncertainty and incentivizing manufacturers to develop mercury-free alternatives.

The United States has implemented progressive fluorescent lamp bans, with screw-base compact fluorescent lamps (CFLs) prohibited from sale since January 1, 2025, and pin-based CFLs banned starting January 1, 2026, accelerating institutional and consumer adoption of mercury-free disinfection technologies. Canada's regulatory timeline is more prescriptive: between 2025 and 2030, the import, manufacture, and sale of major mercury-containing lamp types are progressively prohibited, creating a clear adoption timeline that manufacturers and institutional buyers are responding to by transitioning UV-C disinfection systems to LED technology within the UVC LED Market.

These regulatory drivers translate directly to market expansion as water utilities, healthcare facilities, and consumer product manufacturers face compliance deadlines or anticipate future restrictions. Municipal water treatment plants globally are replacing mercury vapor lamps with UV-C LED systems to ensure regulatory compliance and reduce mercury contamination risks in treated water. Over half of China's urban population is already served by water treatment plants utilizing UV disinfection technology, providing baseline infrastructure that increasingly incorporates LED systems as retrofit replacements for aging mercury lamp installations. Healthcare institutions prioritize mercury-free solutions due to occupational safety requirements and regulatory compliance mandates, with medical equipment sterilization applications driving premium pricing for reliability and certified performance within the UVC LED Market.

Water Quality Mandates and Emerging Market Hygiene Infrastructure Investment

Global concerns regarding waterborne pathogens and elevated awareness of pathogenic contamination are driving institutional and consumer investment in water disinfection infrastructure incorporating UV-C LED technology. China's formalized standards framework for UV disinfection equipment (GB/T 19,837-2019, updated from 2005 standards) establishes specific technical requirements for municipal water and wastewater treatment systems, specifying that UV biological verification dose for drinking water disinfection must not be less than 40 mJ/cm², creating standardized performance benchmarks that accelerate technology adoption across the UVC LED Market.

The standard's establishment reflects government recognition of UV technology's critical role in public health and water safety, with implementation across China's vast water treatment infrastructure creating procurement volumes that incentivize LED manufacturer investment and cost reduction.

India presents comparable institutional drivers: diabetes prevalence is estimated at 537 million adults globally, with India representing approximately 15% of this population and requiring frequent water quality management in healthcare settings. The Indian government's "Ayushman Bharat" health insurance scheme, targeting 500 million beneficiaries, is systematically expanding healthcare infrastructure into tier-II and tier-III cities and rural areas, with water purification and disinfection infrastructure as foundational components.

This macroeconomic shift is accelerating adoption of point-of-use UV-C LED water disinfection systems in decentralized healthcare delivery settings, where compact, mercury-free, minimal-maintenance UV-C LED solutions offer operational advantages unavailable with mercury lamp systems. Investment trends reflect this momentum: India's UV-C LED market is expected to achieve compound annual growth rates of 39.5%, substantially exceeding global averages, driven by government health infrastructure spending and private sector healthcare modernization.

Market Restraining Factors

Elevated Manufacturing and System Integration Complexity

The transition from established mercury lamp manufacturing to UV-C LED production requires substantial capital investment in advanced semiconductor packaging and thermal management infrastructure, creating structural cost barriers that limit manufacturer participation and slow technology adoption in price-sensitive segments. UV-C LED manufacturing demands precision control over aluminum gallium nitride (AlGaN) deposition, flip-chip assembly, and thermal substrate integration to optimize photon extraction efficiency and device reliability process complexity substantially exceeding standard LED manufacturing and requiring semiconductor cleanroom facilities operating at precision levels comparable to high-end logic semiconductor production.

Scaling production from research-level outputs (laboratory prototypes) to industrial manufacturing volumes requires investment in specialized equipment for wafer-scale processing at the 150mm diameter and larger, with yields and cost structures reflecting immature manufacturing processes relative to mature commodity LED production. This manufacturing complexity creates cost barriers preventing price-competitive products suitable for cost-sensitive emerging markets, limiting market penetration in regions with high price elasticity.

System integration complexity represents an additional restraint, as UV-C LED disinfection systems require specialized optical design, thermal management, and wavelength customization per application that contrasts with plug-compatible mercury lamp replacement. Unlike mercury lamps emitting broad-spectrum UV radiation suitable for diverse microbial populations, UV-C LEDs emit narrow wavelength bands (typically ±10nm around peak wavelength), requiring engineered customization for specific pathogenic targets technical complexity that increases system development costs and extends time-to-market for novel applications within the UVC LED Market.

Key Market Opportunities

Emerging Market Water Infrastructure Decentralization and Point-of-Use Treatment Systems

Emerging economies in Asia and Sub-Saharan Africa are establishing decentralized water treatment infrastructure incorporating UV-C LED technology, driven by the prohibitive costs of centralized water utility expansion and the affordability advantages of compact, off-grid UV-C LED systems powered by renewable energy sources.

India's water infrastructure challenge involves serving 1.4 billion individuals with heterogeneous access to centralized municipal water treatment, creating market opportunity for decentralized point-of-use (POU) UV disinfection systems suitable for household, community, and small-scale institutional applications. Innovators including AquiSense and solar-powered SolarAQ systems are developing portable UV-C LED water treatment modules powered by solar arrays and battery storage, enabling off-grid disinfection in rural areas lacking electrical grid connectivity applications ideally suited to UV-C LED technology's compact form factor, instantaneous operation, and minimal maintenance requirements compared to mercury lamp alternatives.

India's government initiatives including "Make in India" manufacturing incentives and the Ayushman Bharat health insurance scheme are catalyzing private sector investment in localized water treatment technology manufacturing, positioning UV-C LED systems as preferred solutions due to their mercury-free status (eliminating hazardous waste management requirements under Indian environmental regulations) and scalability to distributed manufacturing models.

The Asia-Pacific region is experiencing digital health funding acceleration, with Q2 2025 investment reaching US$1.2 billion across 102 deals, with 63% allocation to AI-powered diagnostic and treatment innovations. Within this investment momentum, UV-C LED water disinfection and air purification systems are attracting venture capital and corporate investment as components of integrated smart health and environmental monitoring systems leveraging IoT connectivity and cloud data analytics. This technological convergence enables smart UV-C LED systems with real-time pathogenic load monitoring, automated dosing optimization, and remote performance tracking creating differentiated value propositions and premium pricing for the UVC LED Market in institutional and commercial segments.

Convergence with Digital Health Ecosystems and Wearable/Personal Disinfection Integration

UV-C LED technology is progressively integrating with digital health ecosystems and consumer electronics, creating compound growth opportunities as wearable devices, personal electronics, and connected health systems incorporate disinfection capabilities. Smartphone and personal device disinfection represents an emerging consumer application, with manufacturers incorporating UV-C LED arrays into smartphone sanitization chambers marketed for pathogenic surface inactivation of frequently touched personal electronics.

Portable UV-C LED wearable devices for personal protective applications (UV-sterilized breathing masks, hand-sanitization wearables with UV-C integration) represent incipient product categories attracting early-stage venture investment and technology development partnerships.

The UVC LED Market is positioned as a foundational technology for autonomous robotic systems in healthcare, hospitality, and public infrastructure, where multi-technology convergence creates compelling value propositions for institutional buyers. Hospitals and healthcare networks are increasingly deploying UV-C LED autonomous disinfection robots for terminal room disinfection, reducing manual labor requirements and enabling 24/7 continuous disinfection capability.

Connected UV-C systems with cloud-based monitoring enable facility managers to track disinfection performance, schedule preventive maintenance, and document compliance with regulatory hygiene standards digital ecosystem integration that creates stickiness and recurring revenue opportunities for equipment manufacturers through software-as-a-service (SaaS) models.

Category-wise Analysis

Power Output Insights

Low-power UV-C LEDs (1–50 mW output range) represent 46% market share in 2025, the dominant segment within the UVC LED Market, reflecting the widespread deployment of these devices in consumer electronics, portable disinfection products, and point-of-use water treatment applications where compact form factor and minimal heat generation drive design preferences.

The prevalence of low-power LEDs reflects both historical technology constraints early-generation UV-C LEDs delivered limited radiant flux and continued applicability to distributed disinfection where multiple low-power modules are aggregated to achieve system-level disinfection targets rather than relying on individual high-power devices. LG Innotek's deployment of 50,000 UV LED modules to a Japanese water purifier manufacturer with zero defects and IPX8 waterproof certification exemplifies the commercial maturity of low-power UV-C LED modules, with integration into consumer water filtration devices achieving efficient 200–400nm germicidal sterilization across diverse consumer markets.

High-power UV-C LEDs represent the fastest-expanding segment within the UVC LED Market, driven by recent technological breakthroughs enabling radiant flux outputs that rival or exceed legacy mercury lamp systems while delivering operational advantages unavailable with mercury technology.

Toyoda Gosei's April 2024 development of 275nm UV-C LEDs achieving 200 milliwatts per chip at 350 milliamperes establishes a quantitative inflection point where single-device UV-C LED outputs transition from supplementary lighting to primary disinfection source enabling system architects to replace multiplex low-power configurations with simplified high-power device designs that reduce bill-of-materials costs, system complexity, and thermal management requirements.

Application Segment Insights

Water disinfection and purification represent the largest application segment within the UVC LED Market, accounting for approximately 35.0% of market share in 2026, reflecting historical reliance on UV technology for pathogenic inactivation in municipal water treatment and established regulatory frameworks requiring UV disinfection in specific applications groundwater treatment, recycled water systems.

The segment encompasses diverse use cases: municipal water utilities treating billions of liters daily, decentralized community water treatment systems serving villages and rural populations lacking centralized infrastructure, point-of-use household water purifiers for arsenic/pathogen removal, and industrial applications including food/beverage processing water supplies, pharmaceutical manufacturing ultra-pure water systems, and aquaculture water sterilization.

Air disinfection and purification represent the fastest-expanding application segment within the UVC LED Market, propelled by pandemic-accelerated awareness of airborne pathogenic transmission, building occupancy normalization post-COVID, and emerging regulatory mandates for enhanced indoor air quality in healthcare and high-occupancy settings.

Regional Insights and Trends

North America Market Trend

North America commands 38% of the global UVC LED Market share, reflecting advanced healthcare infrastructure, established regulatory frameworks supporting mercury phase-out, and significant capital investment in both institutional disinfection systems and consumer product innovation.

The United States market is expanding , driven by multiple reinforcing dynamics: accelerating state-level fluorescent lamp bans , institutional healthcare sector investment in mercury-free disinfection systems, and consumer awareness of UV-C sterilization capabilities in personal electronics and household applications.

The North American regulatory environment is progressively tightening mercury restrictions while maintaining enforcement discretion rather than categorical bans, creating dynamic market conditions where manufacturers and institutional buyers are proactively transitioning to UV-C LED alternatives ahead of definitive regulatory deadlines. EPA’s ongoing inventory tracking of mercury-added products and periodic regulatory assessments signal likely future restrictions, incentivizing capital investment in mercury-free disinfection infrastructure.

Healthcare facilities across North America representing significant institutional buyers of disinfection technology are leveraging pandemic-accelerated operational budgets to install permanent UV-C LED disinfection systems across HVAC networks, surface disinfection applications, and medical equipment sterilization processes, driven by both regulatory compliance and occupational safety requirements. The presence of major UV-C LED manufacturers and suppliers such as Crystal IS/Asahi Kasei in the US, ams OSRAM with US operations has established supply chain infrastructure and technical support networks reducing implementation barriers for institutional adoption.

East Asia Market Trend

East Asia represents 26% of global UVC LED Market share and is experiencing the fastest regional growth trajectory, driven by government health infrastructure investment, manufacturing capacity expansion, and accelerating consumer demand in China, Japan, and South Korea.

China's UV disinfection equipment market is systematically integrating LED technology into municipal water treatment infrastructure modernization, with government-backed water quality improvement initiatives and environmental protection plans creating procurement demand for UV-C LED systems. The nation's semiconductor manufacturing ecosystem provides foundational capabilities for UV-C LED chip production, with manufacturers including Sanan Optoelectronics scaling production to support both domestic disinfection infrastructure and export markets throughout Asia and globally.

Japan and South Korea are pioneering advanced UV-C LED technology development and integration into smart, AI-powered disinfection systems. Seoul Viosys, headquartered in South Korea, has achieved and sustained the global No.1 market position in UV LED manufacturing for six consecutive years through 2024, leveraging over 6,000 global patents and full-spectrum UV solutions across UVA, UVB, and UVC wavelengths. The company's Violeds brand represents technological leadership in UV-C LED chip design and packaging, with strength in high-power and specialized-wavelength applications. Japan's established consumer electronics manufacturing base and healthcare industry focus are driving adoption of UV-C LED disinfection in personal devices, household appliances, and medical equipment market segments where Japanese manufacturers including Nichia Corporation, Toyoda Gosei, and Stanley Electric hold competitive positions.

Europe Market Trend

Europe represents 22% of global UVC LED Market share, characterized by stringent regulatory standards, advanced healthcare infrastructure, and strong environmental commitment driving rapid transition to mercury-free disinfection systems.

The European Union's regulatory framework including RoHS Directive, In Vitro Diagnostic Regulation (IVDR), General Data Protection Regulation (GDPR), and revised Mercury Regulation 2024/1849 establish the world's most comprehensive restrictions on hazardous substances and most demanding compliance requirements for medical/diagnostic devices. The EU Mercury Regulation 2024/1849 (effective July 2024) establishes February 24, 2027 as the critical decision date for mercury lamp exemption review, creating a deadline by which institutional buyers must either transition to compliant disinfection systems or plan long-term procurement strategies for exempted equipment.

Competitive Landscape

The global UVC LED market is moderately consolidated with fragmented elements, dominated by a few technology?intensive leaders while numerous smaller players compete in niche applications. Key companies such as Sensor Electronic Technology, Inc. (SETi), Crystal IS (Asahi Kasei), HexaTech, Seoul Viosys, and LG Innotek hold significant market share due to advanced semiconductor capabilities and early investments in deep?UV technology.

Firms like Nichia Corporation and OSRAM GmbH also play major roles, leveraging strong R&D and distribution networks. Mid?sized and emerging players, including Rayvio, NIKKISO, and AquiSense Technologies, focus on specific applications like water treatment, medical sterilization, and consumer devices. Competitive dynamics are driven by technological upgrades, IP development, and strategic partnerships.

Key Industry Developments

- March 25, 2025 – AIXTRON partners in GraFunkL project for graphene-enhanced UVC LEDs: AIXTRON SE joined the GraFunkL research project to develop UVC LEDs with graphene layers, improving light output and energy efficiency for applications such as decontaminating hospital pathogens, indoor air, wastewater, and surfaces. The project, funded by Germany’s BMBF with €2.1?million, aims to scale graphene integration on wafers up to 150?mm for industrial UVC LED production.

- October 23, 2024 – ams OSRAM launches OSLON™ UV 3535 UV-C LED: ams OSRAM unveiled its OSLON™ UV 3535, delivering 115?mW output at 265?nm with 5.3% wall-plug efficiency and an R70B50 lifetime exceeding 20,000 hours. Designed for compact, efficient UV-C disinfection of air, water, and surfaces, the LED combines high germicidal effectiveness, instant-on capability, and advanced flip-chip technology, reinforcing ams OSRAM’s leadership in mercury-free UV-C solutions.

Companies Covered in UVC LED Market

- Toyoda Gosei Co., Ltd.

- Samsung Electronics Co. Ltd

- Lumex Inc. (ITW Inc.)

- NKFG Corporation

- Nitride Semiconductor Co. Ltd

- Crystal IS Inc. (Asahi Kasei Group)

- Nikkiso Co., Ltd.

- Photon Wave Co., Ltd.

- Nichia Corporation

- ams OSRAM AG

- High Power Lighting Corp.

- Asahi Kasei Corporation

Frequently Asked Questions

The global UVC LED Market is projected to be valued at US$ 1.5 Bn in 2026.

The Water Disinfection / Purification Segment is expected to account for approximately 35% of the global UVC LED Market by Application in 2026.

The market is expected to witness a CAGR of 23.5% from 2026 to 2033.

The UVC LED Market include Regulatory phase-out of mercury lamps and rising global demand for water and air disinfection, particularly in emerging markets, are driving UVC LED market growth.

Key Market Opportunities in the UVC LED include Decentralized water treatment and point-of-use UV-C LED systems in emerging markets, integration with digital health ecosystems, wearable/personal disinfection devices, and autonomous UV-C LED disinfection solutions for institutional and commercial applications.

The key players in the UVC LED Market include Toyoda Gosei Co., Ltd., Samsung Electronics Co. Ltd, Lumex Inc. (ITW Inc.), Crystal IS Inc. (Asahi Kasei Group), Nichia Corporation, ams OSRAM AG.